Banking Conditions Survey

For this survey, Eleventh District banking executives were asked supplemental questions on deposits, credit standards, commercial real estate lending and liquidity. Read the special questions results.

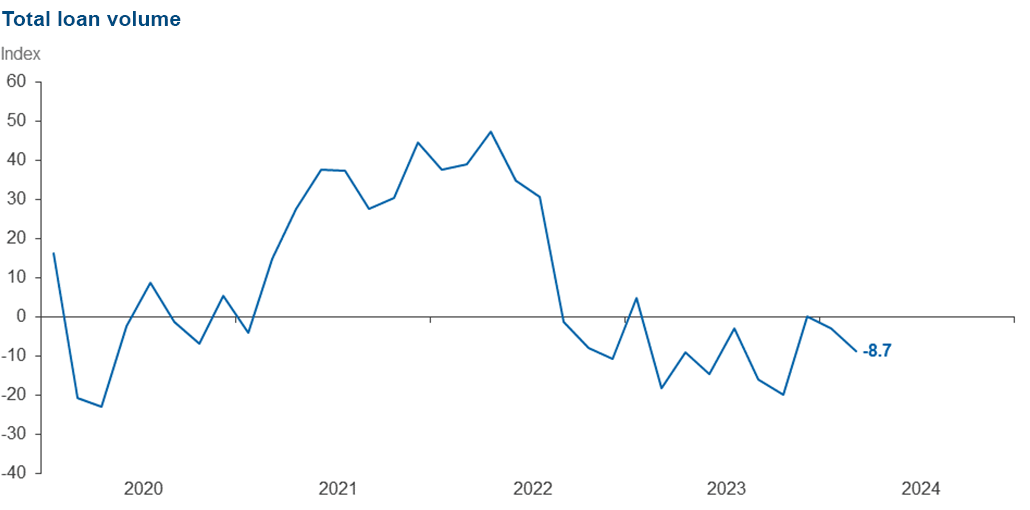

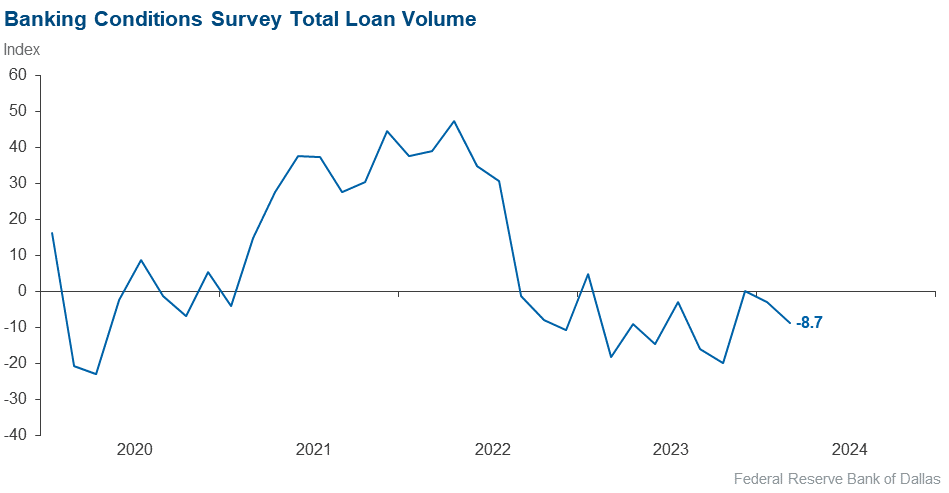

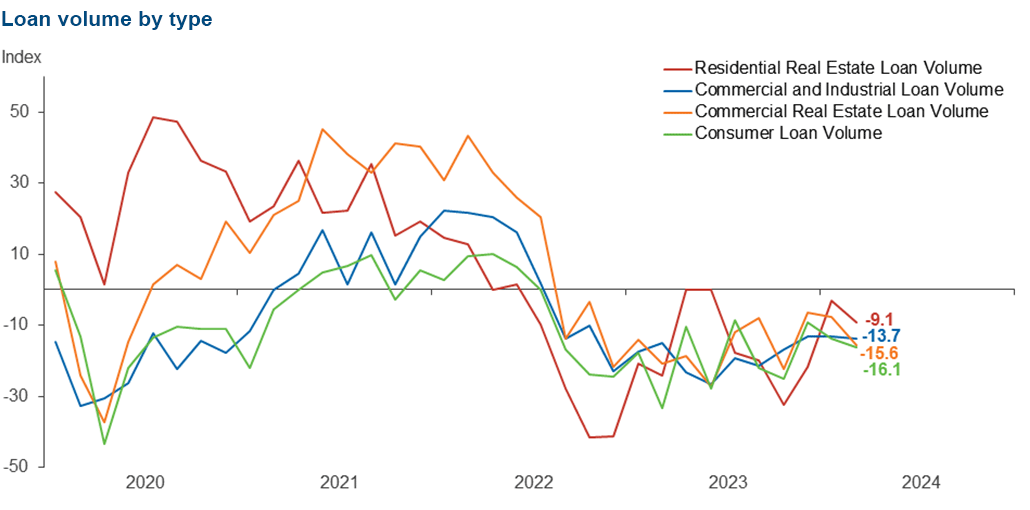

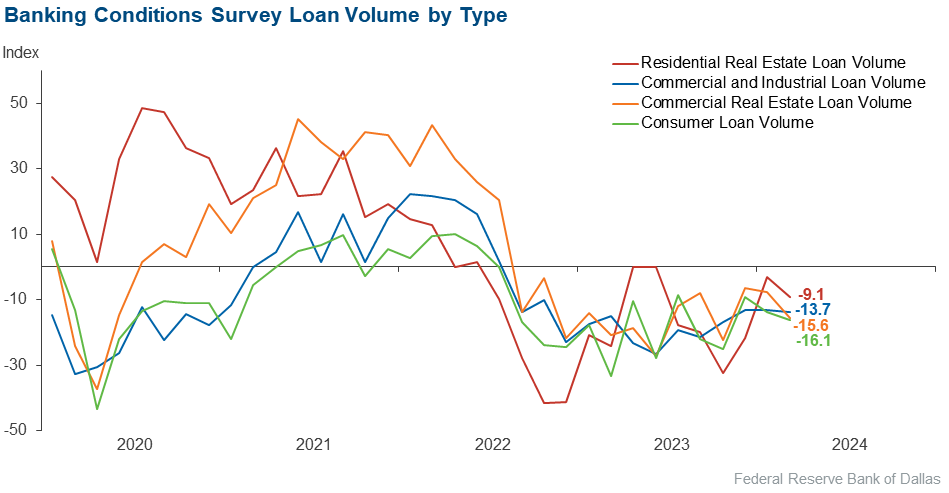

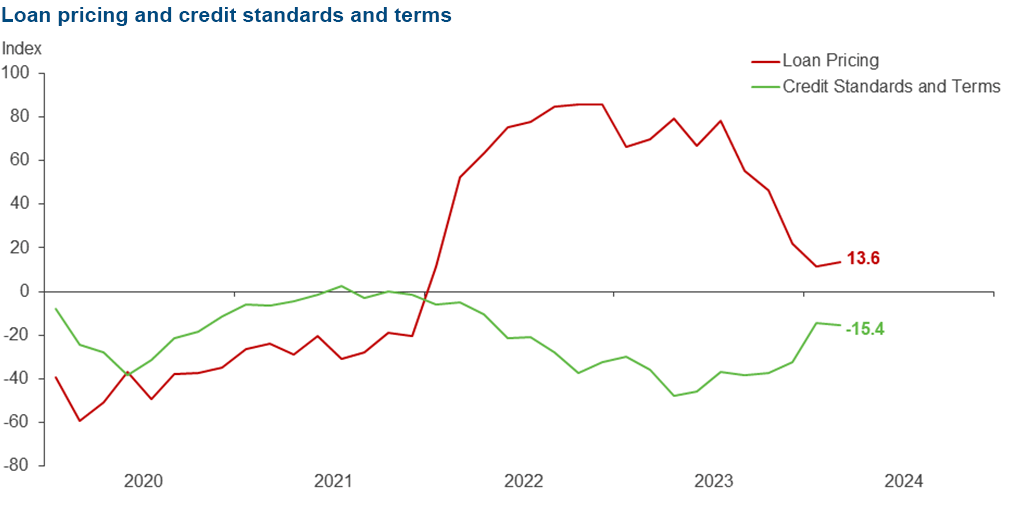

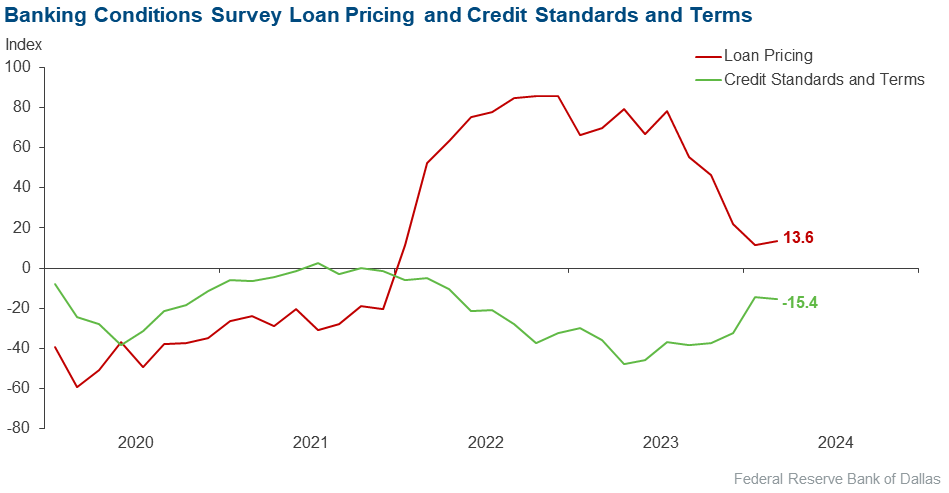

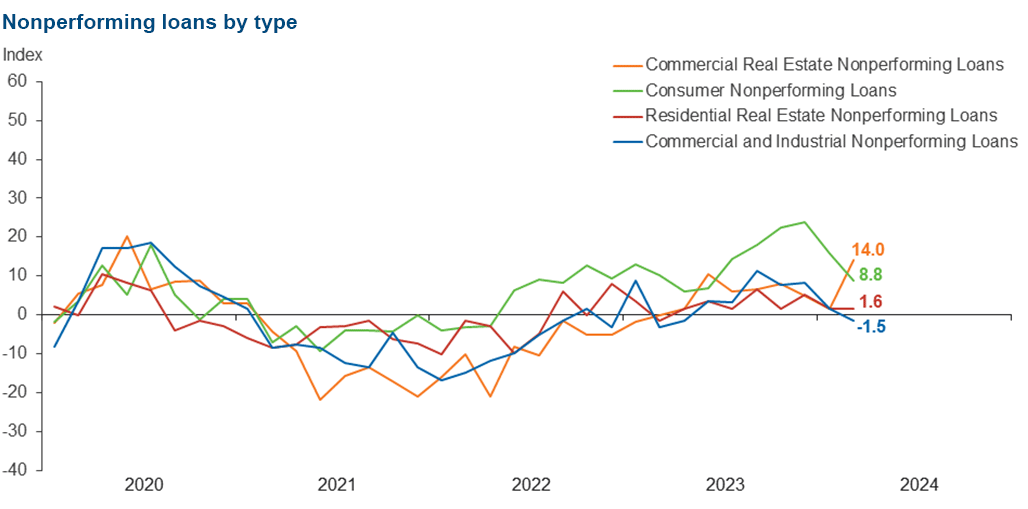

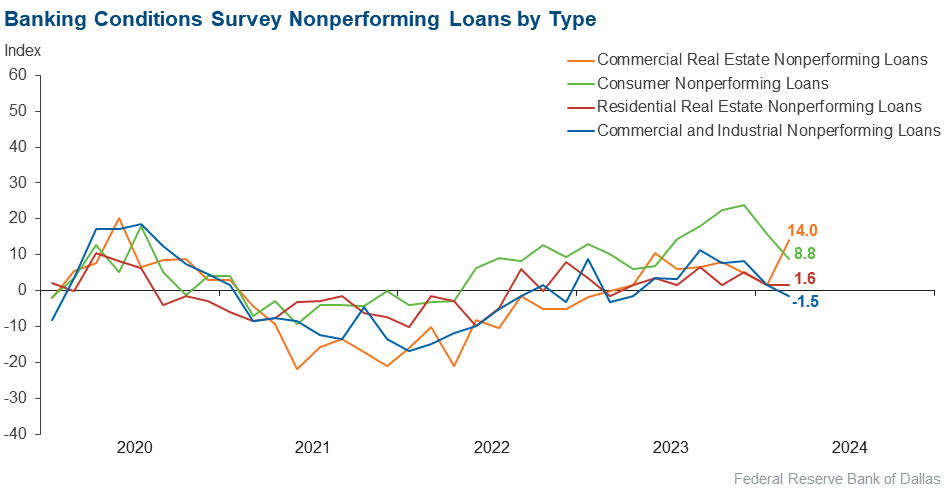

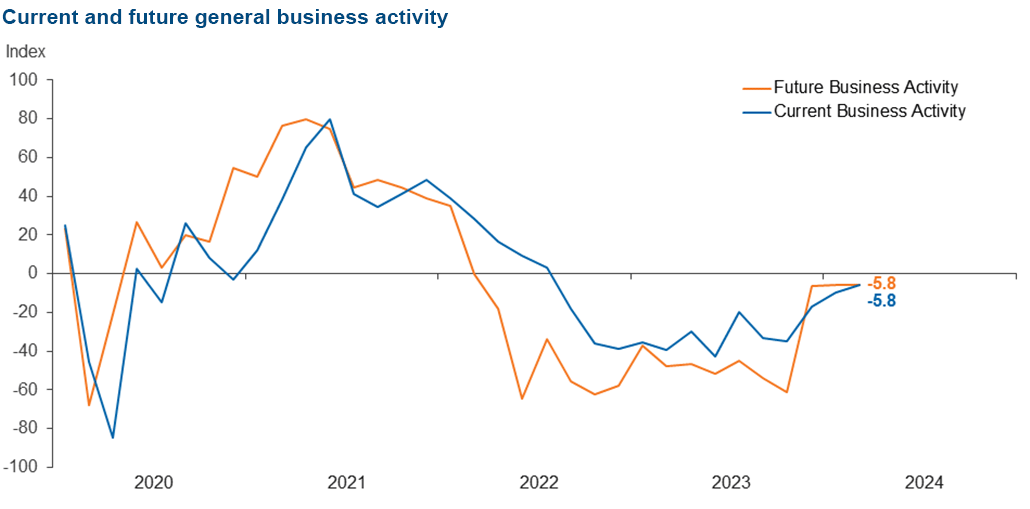

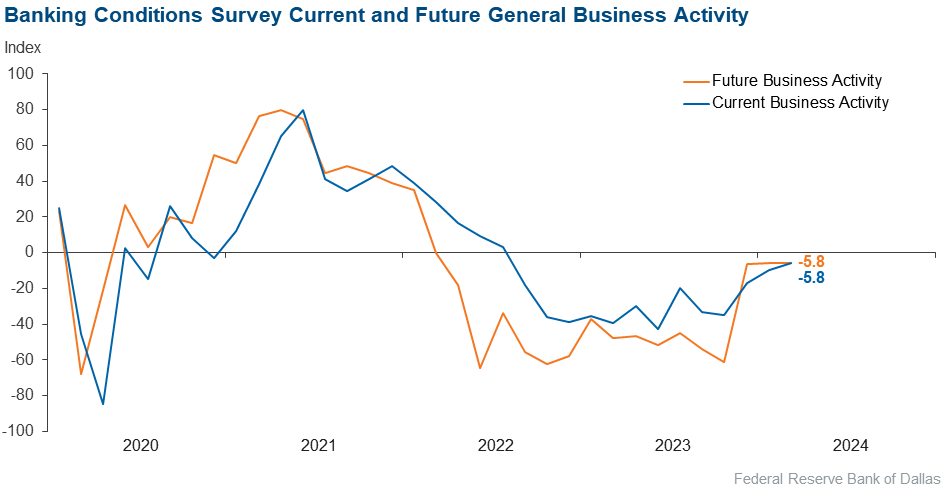

Loan volumes declined after having largely stabilized in the two prior surveys. Credit standards continued to tighten, and loan pricing continued to rise. While credit tightening accelerated for commercial and industrial loans and commercial mortgages, it decelerated for residential mortgages and consumer loans. Loan nonperformance picked up slightly overall, with commercial real estate experiencing a significant increase in past-due loans. Bankers’ outlooks remain mixed: they expect an increase in loan demand six months from now but a deterioration in loan performance and overall business activity.

Next release: May 13, 2024

Data were collected March 19–27, and 69 financial institutions responded to the survey. The Federal Reserve Bank of Dallas conducts the Banking Conditions Survey twice each quarter to obtain a timely assessment of activity at banks and credit unions headquartered in the Eleventh Federal Reserve District. CEOs or senior loan officers of financial institutions report on how conditions have changed for indicators such as loan volume, nonperforming loans and loan pricing. Respondents are also asked to report on their banking outlook and their evaluation of general business activity.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease (or tightening) from the percentage reporting an increase (or easing). When the share of respondents reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior reporting period. If the share of respondents reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior reporting period. An index will be zero when the number of respondents reporting an increase is equal to the number reporting a decrease.

Results Summary

Historical data are available from March 2017.

| Total Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –8.7 | –2.8 | 23.2 | 44.9 | 31.9 |

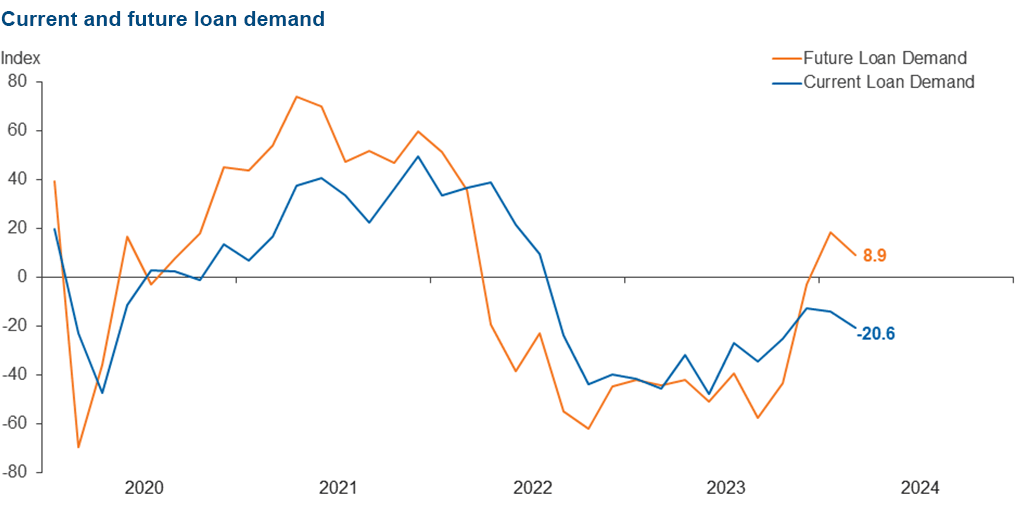

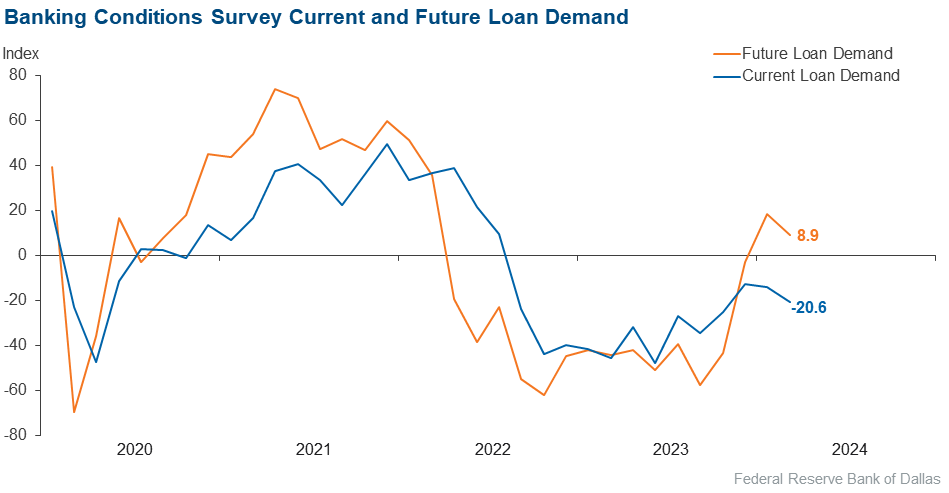

Loan demand | –20.6 | –13.9 | 20.6 | 38.2 | 41.2 |

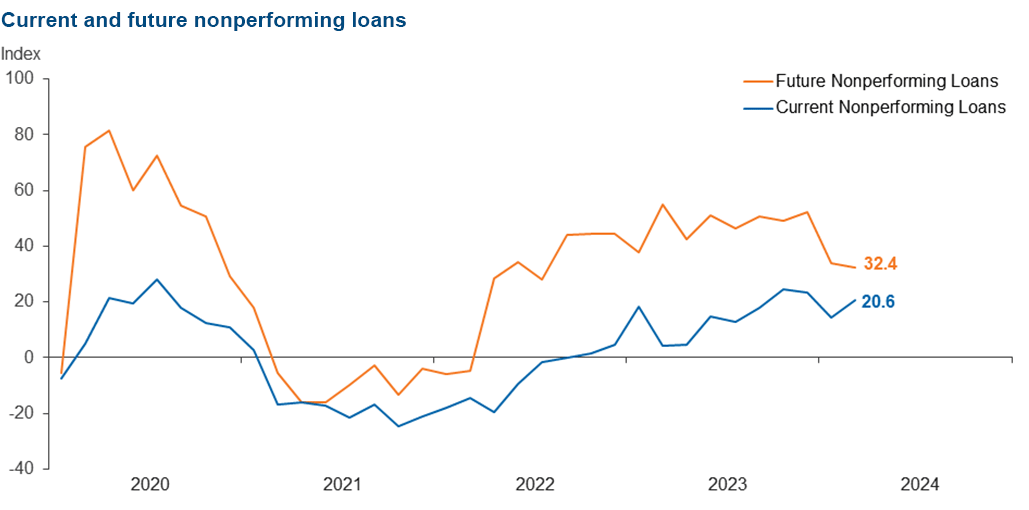

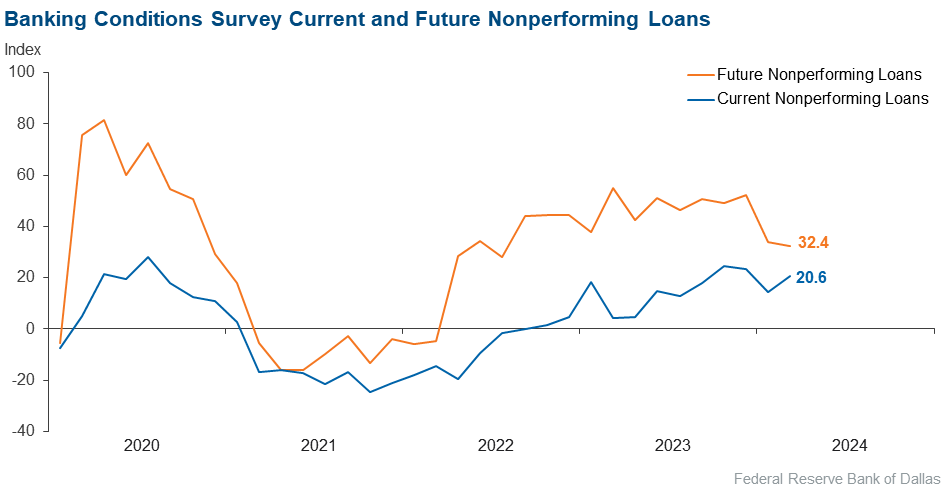

Nonperforming loans | 20.6 | 14.3 | 26.5 | 67.6 | 5.9 |

Loan pricing | 13.6 | 11.4 | 21.2 | 71.2 | 7.6 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

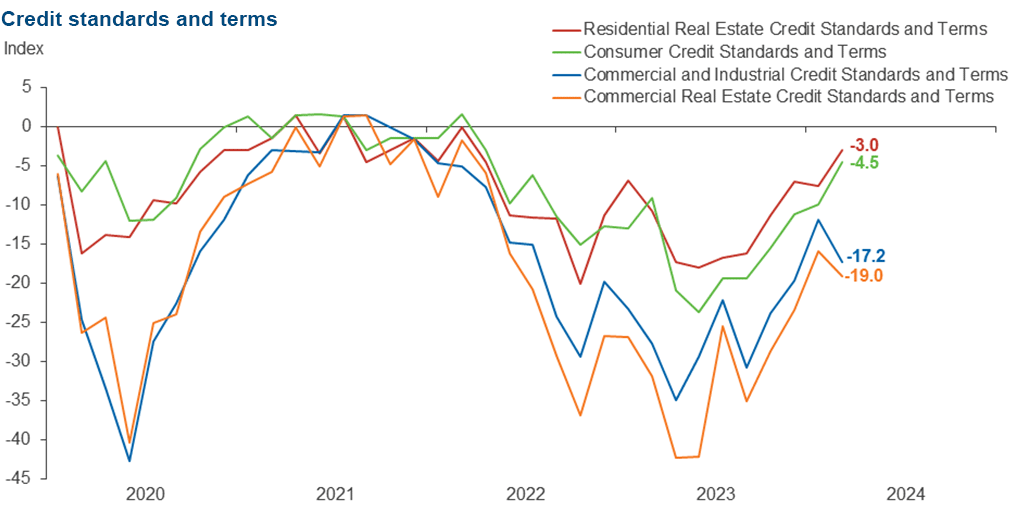

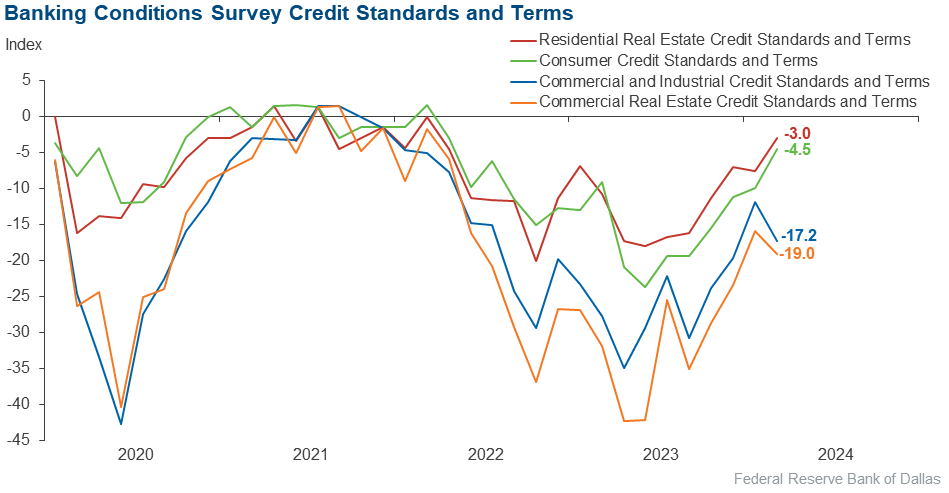

Credit standards and terms | –15.4 | –14.5 | 1.5 | 81.5 | 16.9 |

| Commercial and Industrial Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –13.7 | –13.3 | 13.6 | 59.1 | 27.3 |

Nonperforming loans | –1.5 | 1.5 | 3.1 | 92.3 | 4.6 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –17.2 | –11.9 | 0.0 | 82.8 | 17.2 |

| Commercial Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –15.6 | –7.6 | 18.8 | 46.9 | 34.4 |

Nonperforming loans | 14.0 | 1.5 | 15.6 | 82.8 | 1.6 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –19.0 | –15.9 | 0.0 | 81.0 | 19.0 |

| Residential Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –9.1 | –3.0 | 18.2 | 54.5 | 27.3 |

Nonperforming loans | 1.6 | 1.6 | 6.1 | 89.4 | 4.5 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –3.0 | –7.6 | 0.0 | 97.0 | 3.0 |

| Consumer Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –16.1 | –13.9 | 11.8 | 60.3 | 27.9 |

Nonperforming loans | 8.8 | 15.7 | 13.2 | 82.4 | 4.4 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –4.5 | –9.9 | 0.0 | 95.5 | 4.5 |

| Banking Outlook: What is your expectation for the following items six months from now? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Total loan demand | 8.9 | 18.3 | 36.8 | 35.3 | 27.9 |

Nonperforming loans | 32.4 | 33.8 | 36.8 | 58.8 | 4.4 |

| General Business Activity: What is your evaluation of the level of activity? | |||||

| Indicator | Current Index | Previous Index | % Reporting Better | % Reporting No Change | % Reporting Worse |

Over the past six weeks | –5.8 | –9.7 | 17.4 | 59.4 | 23.2 |

Six months from now | –5.8 | –5.6 | 29.0 | 36.2 | 34.8 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Respondents were given an opportunity to comment on any issues that may be affecting their business.

These comments are from respondents’ completed surveys and have been edited for publication.

- In times of stress, banks should be working with their customers to get the best results. We fear that there will be regulatory overreach in categorizing all commercial real estate as the same and causing undue pressure when time, restructuring and local knowledge will generate better outcomes.

- Regulators continue to push for more in regard to the Bank Secrecy Act, compliance, fair lending etc. At the same time, the Consumer Financial Protection Bureau (CFPB) is requiring the reduction or even elimination of service fee income needed to provide for the low-cost accounts that provide [services] to lower-income people, our Community Reinvestment Act investments and the cost to get enough minority loans to satisfy the fair lending regulation. The regulators are requiring banks to keep more cash on hand and giving no credit for the liquidity lines set up at the Federal Reserve or Federal Home Loan Bank.

- The current regulatory environment makes it challenging to operate as a community bank and to serve our community.

- I would call it trickle-up inflation. While we have been hearing about inflation for several years, our customers are beginning to become more vocal about its impact. Food cost, restaurant cost and other goods costs are now seeing some very substantial increases. Maybe this inflation is just a wave across the nation, and we are just now feeling the rise in prices. Lately it's being discussed more and more.

- The uncertainty in the market about interest rates, the overhang of an ugly presidential election and uncertainty around who will be the victor have created challenges for our clients and potential prospects. Once rate and political uncertainty are removed, I feel the markets will become more active.

- The regulatory environment is once again causing some concerns. The CFPB proposed rules limiting credit card late fees is a concern. Although not directly impacted by this as we do not issue credit cards, the underlying consequences of limiting any “deterrent fee” can lead to unwanted consumer behavior. What lender wants to make a loan when there is no incentive for the borrower to make their payment on time?

- Continued high rates are impacting the residential real estate and mortgage business.

Historical data can be downloaded dating back to March 2017. For the definitions, see data definitions.

NOTE: The following series were discontinued in May 2020: volume of core deposits, cost of funds, non-interest income and net interest margin.

Questions regarding the Banking Conditions Survey can be addressed to Mariam Yousuf at mariam.yousuf@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Banking Conditions Survey is released on the web.