COVID-era eviction moratoriums improved financial well-being … while they lasted

Federal and local governments imposed eviction moratoriums during the height of COVID-19 in 2020, temporarily shielding an estimated 1–2 million U.S. households from the threat of losing their homes. The U.S. Supreme Court struck down the federal moratorium in summer 2021, effectively ending protections in most local areas after nearly a year.

This analysis leverages new eviction and credit data from Dallas County, Texas, to explore the impact of the moratoriums and to examine trends that surfaced once the moratoriums ended. Dallas County is representative of the nation in several ways, including educational attainment levels, unemployment rates and the prevalence of poverty. During the initial year of the pandemic, Dallas County rents increased at near the national average.

We find that the eviction moratoriums in Dallas County produced a “dual benefit”—reductions in both eviction cases and credit card nonpayments—that was more pronounced in communities of color. Finally, we find that when the national mortarium ended, rates of eviction and credit card delinquencies increased swiftly, indicating rising shares of Dallas County households struggling simultaneously with timely rent and credit card payments. Our results are in line with a recent study on the impact of eviction moratoriums on household well-being.

Housing stability emerged as cornerstone of financial well-being

Eviction has been linked to reduced earnings, consumption and access to credit. Studies have also shown eviction lowers the probability of employment, increases the likelihood of homelessness and contributes to diminished health prospects.

Even those who successfully challenge eviction often find they have a blemished rental history which, in turn, diminishes future housing stability. Furthermore, research has presented evidence that race, including the racial composition of a neighborhood, significantly impacts the likelihood of eviction, even when controlling for other factors such as poverty.

When the pandemic hit the U.S. in early 2020, lawmakers enacted eviction moratoriums at the national, state and local levels, seeking to alleviate strain on financially distressed households while reducing virus spread that could accompany housing loss and overcrowding in shelters. At a time when unemployment and inflation surged, rent relief provided households a financial buffer.

Recent research by a Federal Reserve Bank of Dallas economist and co-authors finds that eviction moratoriums during the main portion of the pandemic did indeed reduce eviction filings and, furthermore, helped improve household well-being by allowing households to redirect limited financial resources to immediate consumption for necessities such as food, leading to a reduction in self-reported food insecurity.

Communities of color experience dual benefits

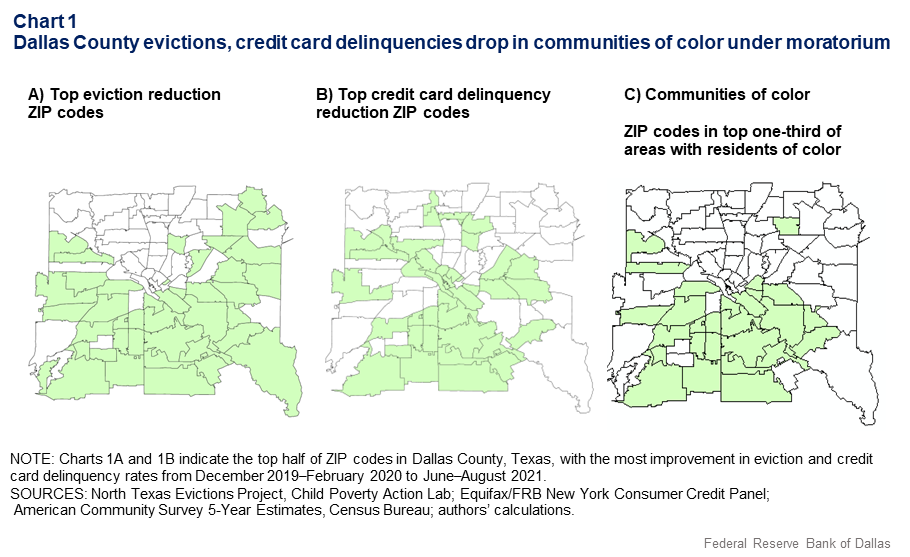

Building on prior research, we turn to Dallas County to explore the localized impact of the pandemic-era eviction moratoriums on ZIP codes with different demographic compositions. Specifically, we look at ZIP codes in the top third in terms of the share of residents of color, which we term “communities of color.”

There is a higher prevalence, on average, of economic disadvantage in Dallas County’s communities of color. For example, poverty and unemployment rates have historically been about twice as high as rates in other ZIP codes in Dallas County. Per capita income is less than $29,000 for 23 out of the 25 communities of color, while per capita income in most of the other ZIP codes exceeds $40,000. We examine how the impacts of eviction protections may differ for these communities of color relative to other Dallas County neighborhoods.

We find that rates of both evictions and credit card delinquency declined in communities of color following imposition of the moratoriums—the simultaneous decline we term dual benefit—based on loan-level data from the Equifax/FRB New York Consumer Credit Panel produced by the credit reporting firm and the Federal Reserve Bank of New York.

We examine the change in eviction rates by noting the number of evictions among households in specific ZIP codes. We compare the rate from before the moratoriums (December 2019 to February 2020) with the rate over a similar period during the moratoriums (June to August 2021).

Similarly, we measure the change in credit card delinquencies using the share of consumers with at least one late credit card payment in a ZIP code during the same two periods.

Among all ZIP codes in Dallas County, many experienced the dual effect (Chart 1). But in communities of color, this effect was much more pronounced: 100 percent of the communities of color experienced a significant drop in both eviction and credit card nonpayment rates.

Among ZIP codes without a high share of residents of color, just seven out of the 22 with large drops in evictions also experienced large declines in delinquencies. This means that communities of color were three times as likely as those in other ZIP codes to receive the dual benefit.

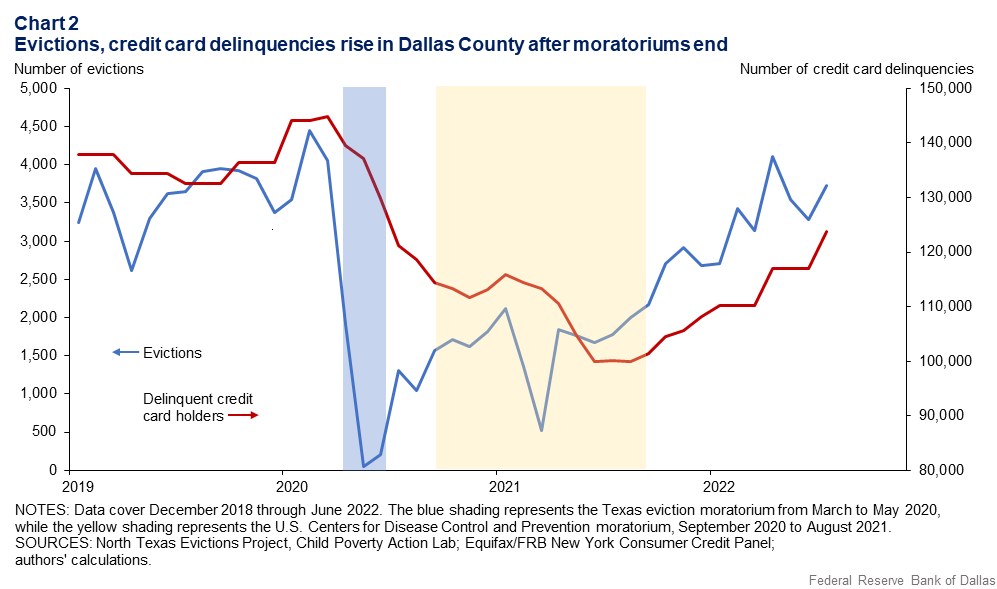

If eviction moratoriums lead to declines in credit card delinquency, the end of the moratorium should reverse the trend and lead to increasing delinquencies. We find supporting evidence in the data.

After moratoriums, credit card delinquencies rise in Dallas County

As might be expected, eviction rates in Dallas County remained low during the local and federal moratoriums but quickly moved higher after the Supreme Court ruling. The number of Dallas County residents with at least one credit card delinquency simultaneously began rising (Chart 2).

By comparison, in Los Angeles County, another major metro with a large share of residents of color, a local eviction moratorium continued past the federal cut-off and was set to end on March 23, 2023. Credit card delinquency rates were little changed there.

The end of moratoriums brings economic challenges

Notably, the eviction moratoriums did not benefit everyone: Some renters were not covered, others may not have known about the protections, and many landlords were left to absorb the ongoing costs of maintenance and property taxes without cash flow from tenants. But for those tenants who were covered, the COVID-era eviction moratoriums appear to have positively affected food security, emotional well-being and financial stability. And their end quickly returned eviction filings to prepandemic levels.

Eviction stress, coupled with recent inflation, will tend to exacerbate the financial stress of low-income households. Renter households in the U.S. have an average net worth of $5,000 and very little cushion to weather a rent increase. Households earning less than $30,000 a year are particularly vulnerable when confronted with rent increases and the chance of eviction.

Our findings suggest a larger effect of eviction moratoriums on credit card delinquencies within communities of color in Dallas County. We consider Dallas County representative of other large urban counties, with similar levels of education, employment, poverty and rent increases as well as similar concentrations of residents of color.

Applying the findings of Dallas County more broadly to other metros in the United States, we find evidence of benefits that could arise should more attention be focused on ensuring housing stability for vulnerable households.

About the authors

Nitzan Tzur-Ilan is a research economist in the Research Department at the Federal Reserve Bank of Dallas.

Emily Ryder Perlmeter is senior advisor in the Community Development at the Federal Reserve Bank of Dallas.

Xiaohan Zhang is a senior economist in the Communications and Outreach Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.