Texas Service Sector Growth Holds Steady in July

Texas Service Sector Outlook Survey

Texas Service Sector Growth Holds Steady in July

For this month’s survey, Texas business executives were asked supplemental questions on labor market conditions. Results for these questions from the Texas Manufacturing Outlook Survey, Texas Service Sector Outlook Survey and Texas Retail Outlook Survey have been released together. Read the special questions results.

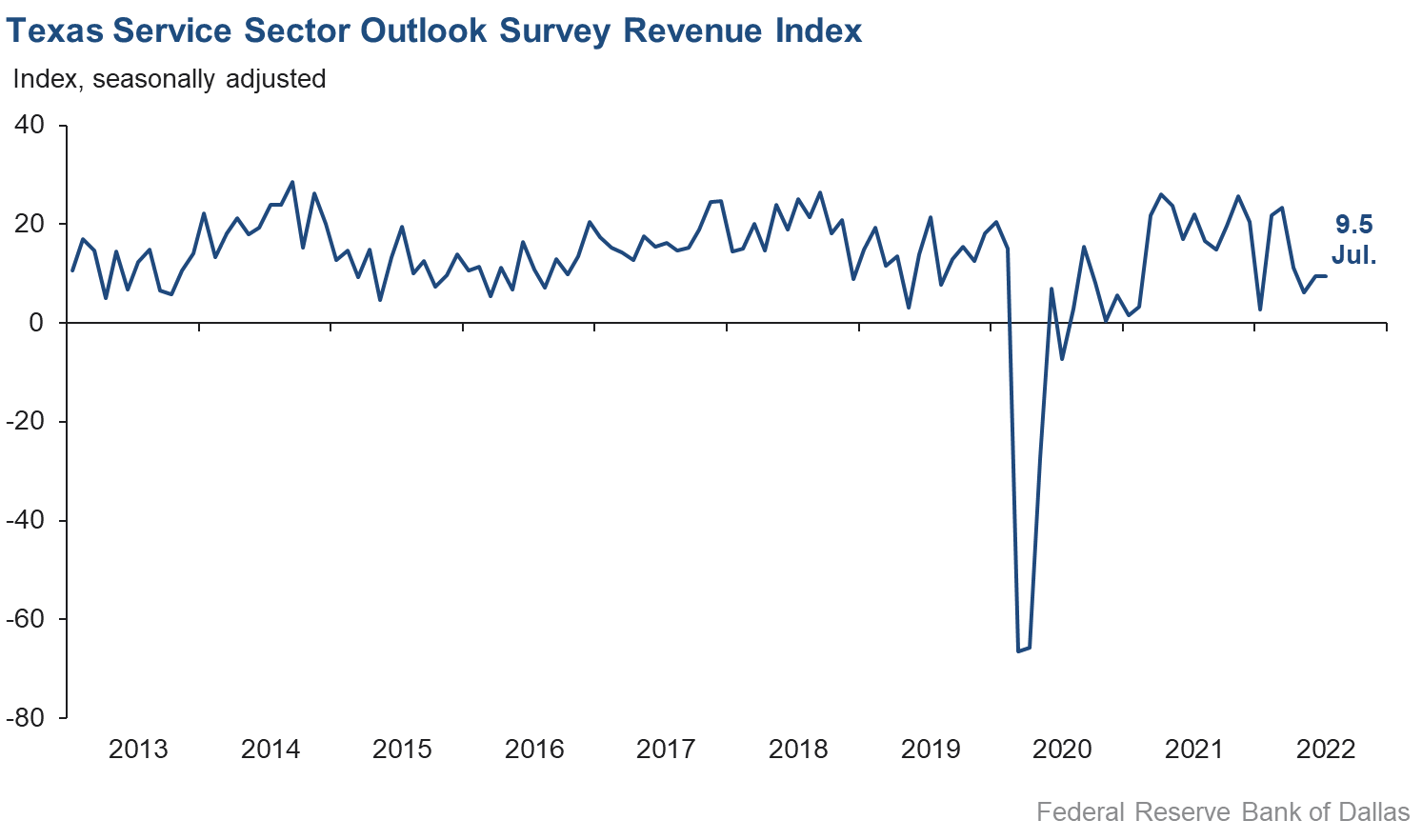

Activity in the Texas service sector increased moderately in July, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, was roughly unchanged at 9.5 in July, and the share of firms reporting increasing revenues was 31 percent.

Labor market indicators were positive, with accelerated employment growth and a continued increase in hours worked. The employment index jumped seven points to 14.5, with nearly one quarter of respondents noting increased payrolls compared with June. The part-time employment index was flat at 1.6, while the hours worked index was similarly unchanged at 5.0.

Perceptions of broader business conditions remained negative in July, although they were somewhat less pessimistic than in June. The general business activity index inched up from -12.4 to -10.9, while the company outlook index improved from -14.7 to -5.2; the share of firms reporting a worsened outlook fell from 27 percent to 19 percent. The outlook uncertainty index dropped sharply from 41.2 to 22.3.

Price and wage pressures moderated slightly in July, though the relevant indexes remain well above historical averages. The selling prices index fell four points to 25.7, while the input prices index dropped six points to 49.9. The wages and benefits index fell over six points to 28.0, as the share of respondents reporting wage increases fell from 37 percent to 31 percent.

Respondents’ expectations regarding future business activity were mixed in July, with some indicators pointing to more optimism. The future general business activity index improved by over 16 points but was still in negative territory at -7.5. The future revenue index rebounded from 19.0 to 35.3, with over half of respondents expecting higher revenues six months from now. Other future service sector activity indexes such as employment and capital expenditures picked up, suggesting some recovery in expectations for growth in the rest of the year.

Texas Retail Outlook Survey

Decline in Texas Retail Sales Accelerates in July

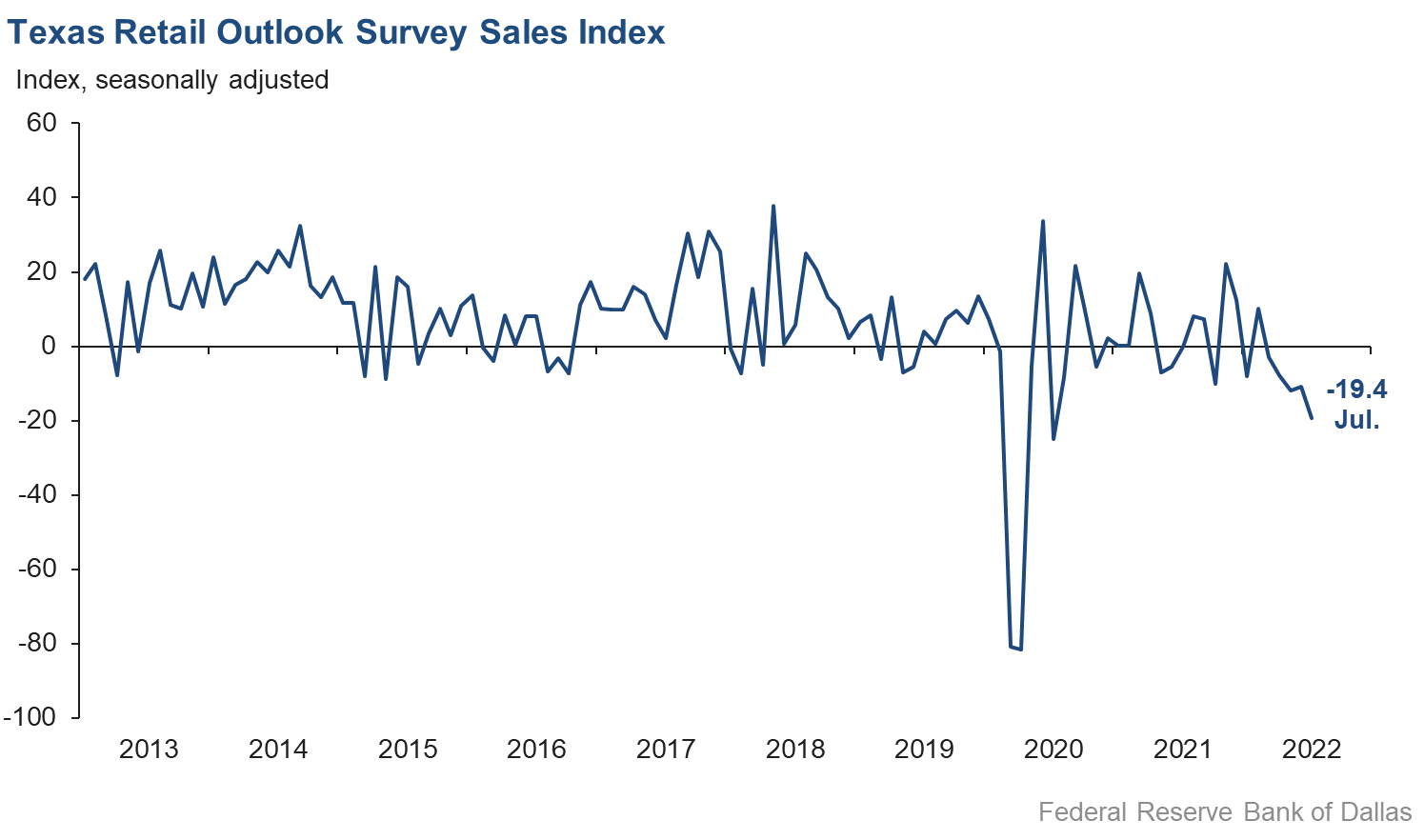

July retail sales activity continued to decline, according to business executives responding to the Texas Retail Outlook Survey. The sales index, a key measure of state retail activity, plunged eight points to -19.4—its weakest reading since July 2020. Retailers’ inventories increased for the first time since late 2021, with the inventories index surging from a near-zero reading to 13.2.

Retail labor market indicators were mixed in July. The employment index rebounded from negative territory to 5.4, while the part-time employment index increased seven points to -1.1. The hours worked index picked up from -6.1 to 0.3, suggesting little net change in average employee hours worked.

Retailers’ perceptions of broader business conditions remained negative in July. The general business activity index increased nearly three points but remained negative at -22.6, while the company outlook index picked up from -22.2 to -16.5. The outlook uncertainty index fell to a three-month low of 14.2.

Retail price and wage pressures eased in July. The selling prices index decreased five points to 31.9, while the input prices index plunged 10 points to 39.7—its lowest reading in over a year. The wages and benefits index softened from 30.4 to 19.2, with just over a quarter of firms noting increased labor compensation costs this month compared with nearly 40 percent of firms in June.

Expectations for future retail growth were mixed in July. The future general business activity index picked up over 10 points but remained negative at -16.3, while the future sales index bounced back somewhat, rising from 0.9 to 17.6. Other indexes of future retail activity were mostly positive, suggesting expectations that growth will pick up over the next six months from the weak pace seen recently.

The Texas Retail Outlook Survey is a component of the Texas Service Sector Outlook Survey that uses information only from respondents in the retail and wholesale sectors.

Next release: August 30, 2022

Data were collected July 12–20, and 287 Texas service sector business executives, of which 58 were retailers, responded to the survey. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease. Data have been seasonally adjusted as necessary.

Texas Service Sector Outlook Survey

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 9.5 | 9.4 | +0.1 | 11.3 | 24(+) | 31.3 | 46.9 | 21.8 |

Employment | 14.5 | 7.6 | +6.9 | 6.5 | 24(+) | 23.9 | 66.7 | 9.4 |

Part–Time Employment | 1.6 | 1.9 | –0.3 | 1.6 | 20(+) | 6.7 | 88.2 | 5.1 |

Hours Worked | 5.0 | 4.9 | +0.1 | 2.9 | 23(+) | 10.9 | 83.2 | 5.9 |

Wages and Benefits | 28.0 | 34.6 | –6.6 | 15.4 | 26(+) | 31.1 | 65.8 | 3.1 |

Input Prices | 49.9 | 55.8 | –5.9 | 26.9 | 27(+) | 52.2 | 45.5 | 2.3 |

Selling Prices | 25.7 | 29.4 | –3.7 | 7.0 | 24(+) | 29.6 | 66.5 | 3.9 |

Capital Expenditures | 16.4 | 12.1 | +4.3 | 10.1 | 23(+) | 23.3 | 69.8 | 6.9 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –5.2 | –14.7 | +9.5 | 5.4 | 2(–) | 13.4 | 68.0 | 18.6 |

General Business Activity | –10.9 | –12.4 | +1.5 | 3.9 | 2(–) | 15.7 | 57.7 | 26.6 |

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 22.3 | 41.2 | –18.9 | 12.5 | 14(+) | 33.5 | 55.3 | 11.2 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 35.3 | 19.0 | +16.3 | 37.8 | 27(+) | 51.8 | 31.7 | 16.5 |

Employment | 31.2 | 23.4 | +7.8 | 23.1 | 27(+) | 38.4 | 54.4 | 7.2 |

Part–Time Employment | 6.3 | –0.3 | +6.6 | 7.0 | 1(+) | 10.5 | 85.3 | 4.2 |

Hours Worked | 3.9 | 2.8 | +1.1 | 6.0 | 27(+) | 10.5 | 82.9 | 6.6 |

Wages and Benefits | 50.8 | 50.5 | +0.3 | 37.1 | 27(+) | 53.3 | 44.2 | 2.5 |

Input Prices | 57.7 | 66.4 | –8.7 | 44.4 | 187(+) | 60.8 | 36.1 | 3.1 |

Selling Prices | 37.0 | 36.6 | +0.4 | 24.2 | 27(+) | 42.7 | 51.6 | 5.7 |

Capital Expenditures | 25.0 | 20.8 | +4.2 | 23.6 | 26(+) | 34.2 | 56.6 | 9.2 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 2.5 | –18.4 | +20.9 | 16.7 | 1(+) | 24.4 | 53.7 | 21.9 |

General Business Activity | –7.5 | –24.0 | +16.5 | 13.8 | 3(–) | 21.6 | 49.2 | 29.1 |

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Retail (versus previous month) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | –19.4 | –11.0 | –8.4 | 5.1 | 5(–) | 20.7 | 39.2 | 40.1 |

Employment | 5.4 | –3.3 | +8.7 | 2.0 | 1(+) | 15.9 | 73.6 | 10.5 |

Part–Time Employment | –1.1 | –8.1 | +7.0 | –1.6 | 2(–) | 8.3 | 82.3 | 9.4 |

Hours Worked | 0.3 | –6.1 | +6.4 | –1.7 | 1(+) | 10.6 | 79.1 | 10.3 |

Wages and Benefits | 19.2 | 30.4 | –11.2 | 10.9 | 24(+) | 26.0 | 67.2 | 6.8 |

Input Prices | 39.7 | 49.9 | –10.2 | 21.8 | 27(+) | 48.8 | 42.0 | 9.1 |

Selling Prices | 31.9 | 37.1 | –5.2 | 13.7 | 26(+) | 44.4 | 43.1 | 12.5 |

Capital Expenditures | 9.6 | 10.4 | –0.8 | 8.1 | 18(+) | 22.6 | 64.4 | 13.0 |

Inventories | 13.2 | –0.2 | +13.4 | 1.9 | 1(+) | 30.9 | 51.4 | 17.7 |

| Companywide Retail Activity | ||||||||

Companywide Sales | –18.3 | –7.8 | –10.5 | 6.5 | 3(–) | 20.2 | 41.3 | 38.5 |

Companywide Internet Sales | –17.4 | –10.4 | –7.0 | 5.4 | 3(–) | 3.9 | 74.8 | 21.3 |

| General Business Conditions, Retail Current (versus previous month) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –16.5 | –22.2 | +5.7 | 3.2 | 5(–) | 5.2 | 73.1 | 21.7 |

General Business Activity | –22.6 | –25.2 | +2.6 | –0.3 | 3(–) | 11.3 | 54.8 | 33.9 |

| Outlook Uncertainty Current (versus previous month) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 14.2 | 42.3 | –28.1 | 10.2 | 14(+) | 32.1 | 50.0 | 17.9 |

| Business Indicators Relating to Facilities and Products in Texas, Retail Future (six months ahead) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | 17.6 | 0.9 | +16.7 | 32.7 | 27(+) | 40.5 | 36.5 | 22.9 |

Employment | 14.8 | 10.3 | +4.5 | 13.3 | 27(+) | 26.9 | 61.0 | 12.1 |

Part–Time Employment | 3.0 | –0.8 | +3.8 | 1.7 | 1(+) | 12.3 | 78.4 | 9.3 |

Hours Worked | 4.7 | –7.4 | +12.1 | 3.1 | 1(+) | 14.2 | 76.3 | 9.5 |

Wages and Benefits | 40.3 | 43.6 | –3.3 | 29.1 | 27(+) | 43.5 | 53.3 | 3.2 |

Input Prices | 41.8 | 58.5 | –16.7 | 34.3 | 27(+) | 50.9 | 40.0 | 9.1 |

Selling Prices | 25.5 | 41.5 | –16.0 | 30.1 | 27(+) | 45.5 | 34.5 | 20.0 |

Capital Expenditures | 16.7 | 21.2 | –4.5 | 18.1 | 26(+) | 31.5 | 53.7 | 14.8 |

Inventories | 26.4 | 23.4 | +3.0 | 10.7 | 27(+) | 40.3 | 45.8 | 13.9 |

| Companywide Retail Activity | ||||||||

Companywide Sales | 1.0 | 4.0 | –3.0 | 31.2 | 27(+) | 31.1 | 38.9 | 30.1 |

Companywide Internet Sales | 9.1 | 5.1 | +4.0 | 22.7 | 28(+) | 20.5 | 68.2 | 11.4 |

| General Business Conditions, Retail Future (six months ahead) | ||||||||

| Indicator | Jul Index | Jun Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –10.1 | –13.8 | +3.7 | 17.1 | 3(–) | 15.7 | 58.5 | 25.8 |

General Business Activity | –16.3 | –26.8 | +10.5 | 12.8 | 4(–) | 14.6 | 54.5 | 30.9 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

†Added to survey in January 2018.

Data have been seasonally adjusted as necessary, with the exception of the outlook uncertainty index which does not yet have a sufficiently long time series to test for seasonality.

Texas Service Sector Outlook Survey

Texas Retail Outlook Survey

Texas Service Sector Outlook Survey

Comments from Survey Respondents

These comments are from respondents’ completed surveys and have been edited for publication.

Utilities

- Federal Reserve policy has me worried.

Specialty Trade Contractors

- The supply chain is getting worse, not better.

Warehousing and Storage

- While we're under the belief that the steep increase in interest rates will have a cooling effect on the economy, we don't believe that there will be any cooling of demand for U.S. energy exports, which makes up 90 percent of our business. Thus, while we expect inflationary pressures to be brought under control by six months from now (with the exception of labor costs, which will increase after our January COLA [cost of living adjustment]), we believe shipments and revenue will continue to increase. We just capped our best-ever quarter and first six months [of the year] and expect more of the same going forward.

Publishing Industries (Except Internet)

- We generally have the same views from last month but some thoughts that U.S. stagflation is expected to start soon will exist with an even more damaging recession in the E.U. [European Union] and some other parts of the world; this will have even deeper negative ripple effects on the global economy, plus an even stronger dollar for longer than expected, which will also hurt U.S. operating companies' international business by being even less competitive on pricing.

Credit Intermediation and Related Activities

- The residential mortgage-lending industry has been sustained by refinance business that was set up during the sky-high interest rates of the [President] Carter years. This is quite problematic.

- [There is] continuing concern for regulatory changes and the impact to our institution. The mounting inflationary environment is becoming an issue affecting our clients and our business overhead. The volatility of the markets is certainly a concern for participants in any retirement plan as valuations continue to erode.

- As a provider of long-term fixed-rate capital for commercial real estate, we feel that short-term capital sources may experience headwinds. As a result, we may see customers moving away from their banking sources and toward insurance company sources, which we represent.

- [We are seeing] higher operating costs in most all expense line items, now including interest increases. [Federal Reserve] tightening is having the intended effect.

Securities, Commodity Contracts, and Other Financial Investments and Related Activities

- Leasing demand remains robust. [We are] achieving increases in rental rates but costs of tenant improvements have also increased.

- Cost of financing has increased, but most of our loans are on long-term fixed rates, so the effect on the bottom line is nil.

- There is still a significant lack of qualified candidates.

- M&A [mergers and acquisitions] activity is seemingly picking up in upstream oil and gas and, therefore, my investment banking and consulting services are in higher demand.

- Drought is worse than expected. Labor shortage and supply-chain problems continue at nearly all businesses.

Insurance Carriers and Related Activities

- Uncertainty about the national economy and inflation coupled with the rise in COVID cases causes some concern but not any more than last month.

Real Estate

- Increasing numbers of employees are looking for wage and/or car allowance increases. Unfortunately, revenues are not increasing as fast.

- Besides higher interest rates, inflation and a lack of inventory still, the unrelenting heat is affecting the mindset of buyers. [There are] dead trees and grass and [they have] no desire to be outside.

- The increase in interest rates and overall inflation of energy, food and housing is hitting families. The cost of warehouse space and employee wages is hitting businesses small and large. The economy is out of control, but it will correct.

- Inflation has been hitting our construction costs very hard. Rental rate increases have saved us until interest rates have increased, and now we are hit hard with an all-stop for new construction. Our yield on cost is now below the cost of funds. We have to wait to watch construction prices drop significantly.

- Employee retention, construction costs, material and equipment shortages, and the availability of utilities to provide services or equipment continue to persist and delay the delivery of projects and increase costs at all levels.

- Inflation and interest rates have clients evaluating the timing to buy.

Rental and Leasing Services

- Capital expenditures have to go down because we cannot get any equipment from our manufacturers to purchase. For example, yesterday we received our allocation of hay harvesting equipment. We typically sell over 300 tractors in a year, but we are allocated 30 tractors for fourth quarter 2022 and first quarter 2023, and we are allocated exactly zero hay equipment for all of 2023. These manufacturers have absolutely fallen into some kind of black hole; I do not know how they survive!

- Our negative outlook is due to renewing our P&C [property and casualty] insurance this month. If Texas does not get it together on these silly superfluous fraudulent nuisance liability claims by the lower 10 percent of every law school's graduating class, there is not going to be any business left in Texas. Our insurance package is up 40 percent this year due to umbrella and liability coverage.

Professional, Scientific and Technical Services

- I'm selling [my firm] to private equity and should close this week. We posted a record month for our over-40-year-old family business—a good way to end that phase of our business life and begin a new one.

- Expectations are for more expensive credit markets for businesses that must continue to make payments on existing adjustable-rate financing plans and limited funding opportunities for growth investments in the current market. Wage pressures are the same [as last month], and we have limited means to pass them along to our customers.

- New queries have slowed down.

- Because of our significant backorder situation due to supply-chain issues, it is hard to accurately predict our July revenue right up until the last minute when we know what is going to ship, but we are seeing multiple items that had been severely backordered start shipping. Due to this, we anticipate a better August, so it seems there may be some light at the end of this tunnel.

- The volume of work is showing some slight slowdown exceeding normal seasonal slowing. Large projects are likely seeing some pullback because of increased interest rates.

- The commercial real estate market, specifically tenant interiors projects, has improved as workers return to the office. We are not sure how strong this move will be with the BA.5 [COVID] variant coming onto the scene.

- The real estate market is still showing signs of slowing down due to the interest rate increases. The residential [market] has been declining the entire year, but now we are starting to see the commercial market slow as well. It is difficult to tell where we are going to land, but we are still on pace to have our second-largest revenue year in our company history. The second half of the year will tell the story.

- Our hours and revenue have remained strong, but we are starting to hear anecdotally of impacts to our clients in real estate (homebuilding) and corporate—specifically, less M&A activity.

- Continued stock market declines the first half of the year have caused decreases in revenues and short-term economic uncertainties. The ability to continue to pay higher wages may be challenging if inflation continues to rise. Effects of the impact of inflation remain to be determined and lend to the uncertainty.

- We are expecting a softening in demand for engineering services in 2023 following a normal business cycle.

Administrative and Support Services

- It's hard to keep up with pricing. Supplier increases are frequent. It has negatively affected margins.

- The current level of business activity and the financial performance of clients bear little resemblance to the media headlines regarding the economy. The main focus is on hiring, training and retaining people and a perceived level of uncertainty (but no real evidence to support the level of uncertainty).

- We are still trying to catch up with inflation. I can't increase my prices fast enough, and we have had layoffs but at the same time are feeling the pressure to increase the wages of those left or we will lose them. It feels like a toxic combination that can only end in recession.

- We are still feeling the effects of supply-chain issues. We cannot purchase test equipment without a lead time of four to six months. This is putting us in more of bind as every month passes.

- Inflation and rising wages are starting to creep into hiring decision-making, and clients are becoming more wary about adding a significant amount of new hires. Hiring still occurs, but the pace seems to be softening.

Educational Services

- Business activity seems to be increasing in some sectors and decreasing in others. Uncertainty remains high, and forecasting is difficult.

- The monetary policy shift has been a welcome relief; however, we are still engaged in accommodative measures via QE [quantitative easing].

- We need to get control of inflation; it's eroding the purchase power of everyday Americans, and it will persist for years to come.

- Packaging equipment is up 25–35 percent. We are looking heavily at more automation to reduce labor, and we are working harder on efficiency gains to maintain or grow margins. Labor has settled some, and workers are going back to work. Transportation is difficult, but [there is a] stabilizing in pricing. Services are spotty. Sales are stable, but with transportation costs, we have lost some customers due to freight costs.

Ambulatory Health Care Services

- [We are] really struggling with new hires. [There is] still an IV [intravenous] contrast shortage for our CT [computed tomography] patients.

- Clients started laying off employees—large layoffs, 40 percent of the labor force.

Amusement, Gambling and Recreation Industries

- It is nearly impossible to hire employees part time. We cannot even hire full-time employees.

Accommodation

- Inflation appears to be negatively impacting leisure travel, resulting in lower occupancies and rates.

- For consumers, many factors are in play: inflation, gas prices, disposable income. It is very hard to say with any certainty what will happen in the near term. What is happening today is a softening of demand; therefore, our ability to drive pricing is minimal at best.

Food Services and Drinking Places

- July is a terrible month for us. August [usually] improves (for us) because we participate in Houston Restaurant Weeks. Prices, in some cases, are coming down. The weather has been awful, and it has been difficult to keep the restaurants cool.

- Main issues of lower business travel and downtown office occupancy remain and show little sign of improvement. That said, other leisure-time-related business remains better than the past two years. Input costs continue to increase with no sign of improvement, labor costs are at all-time highs, and supply-chain problems continue to make business life miserable. I don't know how much more I can increase my prices before it causes long-term damage to the business.

- Paper supply lines continue to be an issue. However, eggs and bacon seem to have stabilized as well as prices on those items. Avocado and cheese [prices] continue to rise.

- There is a lack of understanding and leadership to help lead us out of this economic crisis. It is probably going to get a lot worse before it gets better.

- Construction costs for new cafes have increased by 25–40 percent over 2019 (most recent comparable). Labor costs continue to rise; we are initiating a $1-per-hour wage increase for all hourly positions to attract and retain employees. Managers can still demand significant wage increases (7–10 percent). Supplies and raw material costs are still rising. Job applicant volume has increased in the past two weeks—encouraging. Transaction volume for June was steady; the average ticket [amount] was down by 10–15 percent.

Personal and Laundry Services

- Capital expenditures are increasing due to new locations under construction.

Merchant Wholesalers, Durable Goods

- A strong dollar and the continued high fuel prices have hurt [the economy].

- Commodity pricing has dropped substantially. Vendor/tradesman/parts availability is still very limited. We have seen more interest in open positions, so hiring may get easier.

- I believe a recession is coming.

- We are still experiencing major supply-chain problems, and the supply of semiconductors remains a key challenge.

Merchant Wholesalers, Nondurable Goods

- Although many employees have headed back to the workplace, many are still staying and working remotely from home. It is extremely hard getting information to them to let them know they can still purchase from us instead of automatically turning to the big boxes that market so effortlessly.

- We are still seeing supply-chain issues (orders delayed, orders underfilled, etc.), but the frequency and degree of pain is lessening. Where the pain meter has been sitting at an 8 for the last 18 months, I would put it at a 7 [now]. Not a huge change, but the trend is moving in the right direction in the food supply chain.

Motor Vehicle and Parts Dealers

- Supply-chain issues, particularly chips, continue to adversely affect the automobile business. Until these issues start to resolve themselves, I don't expect our business to improve much.

- [We are] expecting inventories to improve based on the forecast from manufacturers. If not, the industry is in real trouble.

- Demand continues to exceed supply in both new and preowned vehicles.

- We are seeing some softening of retail sales demand and traffic.

- Workforce challenges and supply distribution issues remain a huge headwind. We need qualified technicians badly.

Electronics and Appliance Stores

- I am thinking about 1981–85. Stay out of debt and don't buy anything you do not need.

Building Material and Garden Equipment and Supplies Dealers

- You [the Federal Reserve] are overshooting rates like you always do. Keep it up and watch this economy crash and burn.

Health and Personal Care Stores

- With an impending recession and fixed drug prices, we worry about our patients’ ability to access medical care and the medications needed to manage their conditions.

Nonstore Retailers

- I think that that the increase in net sales will come from increased prices due to inflation, not more actual sales. Also, the drought will hurt our sales.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Christopher Slijk at christopher.slijk@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.