"Not to Be Used Externally, but Also Harmful if Swallowed": Projecting the Future of the Economy and Lessons Learned from Texas and Mexico

March 5, 2012 Dallas, Texas

I have been asked to speak about the economy. I am going to take a different approach than is typical for a Federal Reserve speech. I’ll eschew making the prototypical forecast, except to note that from my perch at the Federal Reserve Bank of Dallas, I presently see that: a.) On balance, the data indicate improving growth and prospects for job creation in 2012. However, the outlook is hardly “robust” and remains constrained by the fiscal and regulatory misfeasance of Congress and the executive branch and is subject to a now well-known, and likely well-discounted, list of possible exogenous shocks—the so-called “tail risks”—posed by possible developments of different sorts in the Middle East, Europe, China and elsewhere. And b.) While price stability is being challenged by the recent run-up in gasoline prices—which has yet to be reflected in the personal consumption expenditure and consumer price indexes but may well make for worrisome headlines when February data are released—the underlying trend has been converging toward the 2 percent long-term goal formally adopted by the Federal Open Market Committee (FOMC) at its last meeting.[1]

As to the outlook envisioned by the entire FOMC, you might wish to consult the forecasts of all 17 members, which include those of yours truly, that were made public after the January meeting—though I think a puckish footnote appended to the internal document laying out a component of the December 1966 FOMC forecast might still apply: “Not to be used externally, but also harmful if swallowed.”[2]

Speaking of harmful if swallowed, I might add that I am personally perplexed by the continued preoccupation, bordering upon fetish, that Wall Street exhibits regarding the potential for further monetary accommodation—the so-called QE3, or third round of quantitative easing. The Federal Reserve has over $1.6 trillion of U.S. Treasury securities and almost $848 billion in mortgage-backed securities on its balance sheet. When we purchased those securities, we injected money into the system. Most of that money and more has accumulated on the sidelines: More than $1.5 trillion in excess reserves sit on deposit at the 12 Federal Reserve banks, including the Dallas Fed, for which we pay private banks a measly 25 basis points in interest. A copious amount is being harbored by nondepository financial institutions, and another $2 trillion is sitting in the cash coffers of nonfinancial businesses.

Trillions of dollars are lying fallow, not being employed in the real economy. Yet financial market operators keep looking and hoping for more. Why? I think it may be because they have become hooked on the monetary morphine we provided when we performed massive reconstructive surgery, rescuing the economy from the Financial Panic of 2008–09, and then kept the medication in the financial bloodstream to ensure recovery. I personally see no need to administer additional doses unless the patient goes into postoperative decline. I would suggest to you that, if the data continue to improve, however gradually, the markets should begin preparing themselves for the good Dr. Fed to wean them from their dependency rather than administer further dosage.

I am well aware of the salutary effect of accommodative monetary policy on the equity and fixed-income markets—remember, I am the only member of the FOMC who used to be on the other side. My firms’ record of substantially outperforming the equity and fixed-income indexes over a prolonged period before I hung up my investment business and entered public service in 1997 was achieved by focusing on the long-term fundamentals of the real economy and the underlying value of the securities we purchased or sold—not by depending on central bank largesse. Counting on the Fed to perpetually float returns is a mug’s game.

From my present perspective on the side of the angels, as a member of the policymaking team on the FOMC, I believe adding to the accommodative doses we have applied rather than beginning to wean the patient might be the equivalent of medical malpractice. Having never before pursued this course of healing, we run the risk of painting ourselves further into a corner from which we do not know the costs of exiting. It is my opinion that we should run that risk only in the most dire of circumstances, and I presently do not see those circumstances obtaining.

So much for forecasting and monetary policy. Let me now walk you through an overview of the Texas economy to set the stage for a broader discussion of what I believe continues to bedevil a lasting recovery and more efficient job creation in the United States.

I will use some slides to illustrate key points.

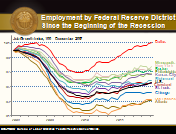

The National Bureau of Economic Research, the arbiter of when recessions begin and end, dates the onset of the Great Recession as December 2007. The economic performance of Texas since December 2007 can be summarized with the chart projected on the screen. It depicts employment growth in the 12 Federal Reserve districts. In the Eleventh Federal Reserve District—or the Dallas Fed’s district—96 percent of economic production comes from the 25.7 million people of Texas. As you can see by the red line, we now have more people at work than we had before we felt the effects of the Great Recession. All told in 2011, Texas alone created 212,000 jobs.[3]

Only two other states can claim they surpassed previous peak employment levels: Alaska and North Dakota.

Readers of this speech abroad—say, in Washington or New York—might think our growth last year came only from the burgeoning oil and gas patch. They would be right to describe it as burgeoning: 30,000 jobs were added in oil and gas and the related support sector last year. Texas now produces 2.1 million barrels of oil per day, the same amount as Norway; we produce 6.7 trillion cubic feet of natural gas a year, only slightly less than Canada.[4]

With 25 percent of U.S. refinery capacity and 60 percent of the nation’s petrochemical production located in Texas, we most definitely benefit from both upstream and downstream energy production.

And yet other sectors gained more jobs than the oil and gas sector and its support functions in 2011: 58,000 jobs were added in professional and business services, nearly 46,000 in education and health services and more than 41,000 in leisure and hospitality. Manufacturing—which accounts for approximately 8 percent of total Texas employment—added over 27,000 jobs.

All told, the private sector in Texas expanded by 266,400 jobs in 2011, while the public sector contracted by 54,800, due primarily to layoffs of schoolteachers. In sum, Texas payrolls grew 2 percent, significantly above the national rate of 1.3 percent.

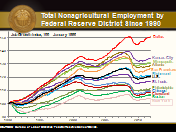

This performance is not unique to last year. As you can see from this graph of nonagricultural employment growth by Federal Reserve district going back to January 1990, the Eleventh District has outperformed the nation on the job front for over two decades. Note the slope of the top line, which depicts job growth in the Eleventh District compared with each of the other districts and, importantly, relative to employment growth for the U.S. as a whole—denoted by the black line, the seventh one down.

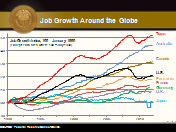

As was pointed out in high relief by the media when a certain Texas governor was briefly in the hunt for his party’s presidential nomination, we do have some serious deficiencies in the Lone Star State. We have a very large number of people earning minimum wage; we have an unemployment rate that, while trending downward, is still too high, abetted by continued inflows of job seekers from less-promising sections of the country. But I’ll bet you that those who constantly enumerate our deficiencies and are given to habitual Texas-bashing would give their right—or should I say, left—arms to have Texas’ record of robust long-term job creation instead of the anemic employment growth of other megastates such as California and New York. Or even the job formation record of many other countries! The following chart shows that over the past two decades, the rate of employment growth in Texas has exceeded that of the euro zone and its two anchors, Germany and France, as well as that of two natural-resource-intensive countries with populations comparable to Texas’, Canada and Australia.

Now, is all this just prototypical Texas brag, or are there lessons the nation can learn from the success that is enjoyed here? Texans are hardly given to modesty, but I believe there are some undeniable lessons being imparted here.

One lesson I draw from comparative state data is that monetary policy is a necessary but insufficient tonic for economic recovery. The Fed has made money cheap and abundant for the entire country. The citizens of Texas and the Eleventh Federal Reserve District operate under the same monetary policy as do our fellow Americans. We have the same mortgage rates and pay the same rates of interest on commercial and consumer loans, and our businesses borrow at the same interest rates as their brethren elsewhere in the country. Which raises an important question: If monetary policy is the same here as everywhere else in the United States, why does Texas outperform the other states?

The answer is no doubt complicated by the fact that Texas is blessed with a comparatively great amount of nature’s gifts, a high concentration of military installations and what some claim are other “unfair” advantages.

But many of these “unfair” advantages are man-made: They derive from a deliberate approach by state and local authorities to enact business-friendly regulations and fiscal policy. For example, if you examine the differences between Texas and two states that have been underperforming for a prolonged period—California and New York—you will note that these former power states have less-flexible labor rules. Due to local taxes, differences in zoning practices and myriad other factors, the cost of housing and the overall cost of living in California and New York are significantly higher than they are here. And due to differences in policies governing education, the scores measuring middle-school students’ proficiency in math are lower in both California and New York than they are in Texas, and in reading, are lower in California and only slightly higher in New York.[5]

Taken together, these factors, alongside whatever natural advantages we may enjoy (though it is hard to compete with the physical beauty of California and the Great Lakes region or the cultural splendor of New York), affect where firms choose to locate and hire and where people choose to raise their families and seek jobs.

I would argue that an additional factor favors Texas: We have a Legislature that under both Democratic and Republican governors has over time deliberately crafted laws and regulations, and tax and spending regimes, encouraging business formation and job creation.

Just last month, Fairfield, Calif.-based vehicle reseller Copart Inc. announced that it will move its headquarters to Texas, citing “greater operational efficiencies.”[6] The CEO for the owner of Hardee’s and Carl’s Jr. restaurants, Andy Puzder, claims it takes six months to two years to secure permits in California to build a new Carl’s Jr., whereas in Texas, it takes six weeks. These two anecdotes from California alone clearly illustrate that firms and jobs will go to where it is easiest to do business—not where it is less convenient and more costly.

Both state and federal authorities need to bear this in mind as they plot changes in the fiscal and regulatory policy needed to restore the job-creating engine of America. As an official of the Federal Reserve charged with making monetary policy for the country as a whole, I am constantly mindful that investment and job-creating capital is free to roam not only within the United States, but to any place on earth where it will earn the best risk-adjusted return. If other countries with stable governments offer more attractive tax and regulatory environments, capital that would otherwise go to creating jobs in the U.S.A. will migrate abroad, just as intra-U.S. investment is migrating to Texas.

Thus, even if one were to somehow have 100 percent certainty about the future course of Federal Reserve policy and be completely comfortable with it, without greater clarity about the future course of fiscal and regulatory policy and whether that policy will be competitive in a globalized world, job-creating investment in the U.S. will remain restrained and our great economic potential will remain unrealized.

I pull no punches here: We have been thrown way off course by congresses populated by generations of Democrats and Republicans who failed the nation by not budgeting ways to cover the costs of their munificent spending with adequate revenue streams. The thrust of the political debate is now—and must continue to be—how to right the listing fiscal ship and put it back on a course that encourages job formation and gets the economy steaming again toward ever-greater prosperity. No amount of monetary accommodation can substitute for the need for responsible hands to take ahold of the fiscal helm. Indeed, if we at the Fed were to abandon our wits and seek to do so by inflating away the debts and unfunded liabilities of Congress, we would only become accomplices to scuttling the economy.

I was in Mexico last week. Mexico has many problems, not the least of which is declining oil production, low school graduation rates and drug-induced violence. But on the fiscal front, the country is outperforming the United States. Mexico’s government has developed and implemented better macroeconomic policy than has the U.S. government.

Mexico’s economy contracted sharply during the global downturn, with real gross domestic product (GDP) plummeting 6.2 percent in 2009. But growth roared back, up 5.5 percent in 2010 and 3.9 percent in 2011, with output reaching its prerecession peak after 12 quarters—three quarters sooner than in the U.S. Mexico’s industrial production passed its prerecession peak at the end of 2010; ours has yet to do so.

Now hold on to your seats: Mexico actually has a federal budget! We haven’t had one for almost three years. Furthermore, the Mexican Congress has imposed a balanced-budget rule and the discipline to go with it, so that even with the deviation from balance allowed under emergencies, Mexico ran a budget deficit of only 2.5 percent in 2011, compared with 8.7 percent in the U.S. Mexico’s national debt totals 27 percent of GDP; in the U.S., the debt-to-GDP ratio computed on a comparable basis was 99 percent in 2011 and is projected to be 106 percent in 2012. Imagine that: The country that many Americans look down upon and consider “undeveloped” is now more fiscally responsible and is growing faster than the United States. What does that say about the fiscal rectitude of the U.S. Congress?

Here is the point: As demonstrated by the relative and continued, inexorable outperformance by Texas—which is affected by the same monetary policy as are all of the other 49 states—the key to harnessing the monetary accommodation provided by the Fed lies in the hands of our fiscal and regulatory authorities, the Congress working with the executive branch. As demonstrated by the fiscal posture of Mexico, a nation can effect budgetary discipline and still have growth.

One might draw two lessons here.

The first comes from Germany’s finance minister, Wolfgang Schäuble, who from my perspective was spot on when he said, “If you want more private demand, you have to take people’s angst away” by having responsible and disciplined fiscal and regulatory policy.[7] Clearly, there is less angst involved in conducting business in Texas.

The second is a broader, macroeconomic truism: that fiscal and regulatory policy either complements monetary policy or retards its utility as a propellant for job creation. Mexico is proof positive that good fiscal policy enhances the effectiveness of thoughtfully conducted monetary policy, which is what the Banco de México—whose independence, incidentally, was enshrined by a constitutional amendment in 1994—has delivered under its single mandate of inflation control and by applying the tool of inflation targeting.

I should be injecting some levity into the event, though it is hard to do so when one talks about our feckless fiscal authorities. But there are witty people who have found a way to do so. Take a look at this parody of Congress that my staff found on YouTube: www.youtube.com/watch?v=Li0no7O9zmE.

There you have the prevailing modus operandi of our fiscal authorities: pass the bill rather than the American dream to our children. What a sad tale!

You asked me to talk about the economy. In a nutshell, my answer is this: Monetary policy provides the fuel for the economic engine that is the United States. We have filled the gas tank and then some. And yet businesses will not use that fuel to a degree necessary to realize our job-creating potential and create a better world for the successor generation of Americans until Congress, working with the executive branch, does the responsible thing and pulls together a tax, spending and regulatory program that will induce businesses to step on the accelerator and engage the transmission mechanism of job creation so they and the consumers they create through employment can drive our economy forward.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- Gasoline prices were not a major factor in January’s headline index, at least relative to the normally wild swings we see in the price of gasoline. On a seasonally adjusted basis, gasoline prices increased 0.9 percent in January (not annualized) and contributed roughly 0.3 annualized percentage points to the headline rate. Based on weekly data collected by the Department of Energy, the price of gasoline in February is on pace for an increase of 6.3 percent over January. Given that the typical seasonal pattern has gasoline’s price falling 1.1 percent in February, we should see a roughly 7.4 percent seasonally adjusted increase when personal consumption expenditures (PCE) data for February come out at the end of March. Gasoline alone may end up contributing about 3 annualized percentage points to February’s headline PCE rate.

- FOMC Greenbook forecast, December 1966.

- According to the National Bureau of Economic Research, the nation went into recession in December 2007 and came out in June 2009. According to the Dallas Fed’s Texas Index of Coincident Indicators, Texas went into the recession in August 2008 and came out in December 2009.

- Texas compares with some international producers of oil and gas as follows:

Crude + natural gas liquids

(mb/d)Natural gas

(trillion cu ft, annual)World

84.60 119.39 United States

8.58 22.47 Canada

3.38 6.91 Texas

2.13 6.71 Norway

2.13 3.85 Mexico

2.95 1.72 SOURCE: Energy Information Administration. - See The Nation’s Report Card, http://nationsreportcard.gov.

- “California Auto Parts Company Moving to Texas,” by Steve Brown, Dallas Morning News, Feb. 4, 2012.

- “Q&A: German Finance Minister Takes On Critics,” by Marcus Walker, William Boston and Andreas Kissler, Wall Street Journal, Jan. 29, 2012.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.