Comments on Monetary Policy and 'Too Big to Fail' (With a Tribute to Irving Kristol)

February 27, 2013 New York, N.Y.

Thank you, Professor [Merit] Janow. The title of this lectureship far overstates my standing and capacity—I am unworthy of being considered “distinguished” at anything other than having helped raise four children whose talents far surpass my own. But I thank you for this momentarily hyperbolic honor.[1]

As Merit mentioned, we go back a long way. Yet my involvement with Columbia University and Morningside Heights goes back much further. After I graduated from Harvard in 1971, I needed money to pay for Oxford, so I spent most of a year working as a busboy and bartender and doing a number of odd jobs in Washington, D.C.—testimony to the immediate benefits of a Harvard degree in economics! Starved for intellectual sustenance as I waited to return to academia, I found comfort in reading about public policy, especially in the essays of what was then a new journal, The Public Interest.

The Public Interest was the brainchild of Irving Kristol and Daniel Bell (subsequently joined by Nathan Glazer)—originally young Trotskyites who had spent their days as students at the City College of New York (CCNY), the “Harvard of the Proletariat”—“trying to understand how the socialist ideal of political and economic justice had ended in Joseph Stalin’s murderous tyranny.”[2] They later migrated to what we would now consider prototypical Roosevelt-cum-Lyndon Johnson liberalism, and then evolved into “neoconservatives.” These three men were becoming iconic public intellectuals, and The Public Interest was something of a personal journal of lessons they learned during their ideological transformation.

Kristol and Bell ran a series of evening seminar/workshops here on this campus and at CCNY. At every opportunity, I would take an afternoon off, jump on a bus to New York, attend their evening talks, find some kindly student to let me sleep in a dorm room and return by bus to Washington the next morning. All this is by way of saying that I have been coming to Columbia for over 40 years, almost as many years as the number of consecutive games lost in the historical losing streak of your illustrious football team.

I was especially captivated by Irving Kristol. His book, Two Cheers for Capitalism, praised capitalism because, one, “it works, in a quite simple, material sense;” and two, it is “congenial to a large measure of personal liberty.”[3] Kristol famously described himself as “a liberal who had been mugged by reality.” In writing a loving homage to Kristol when he died, David Brooks of the New York Times summarized the basis for Kristol’s epiphany in more colorful language. “The elemental Jewish commandment” in the working-class neighborhood where Kristol grew up was: “Don’t be a schmuck. Don’t fall for fantastical notions that have nothing to do with the way people really are.”[4]

As a member of the team of earnest men and women who form the Federal Open Market Committee (FOMC), I consider myself a central banker who has been mugged by the reality of having been an investor and market operator. I am constantly wary of fantastical notions that seem cogent in economic or monetary theory but run counter to what I learned in the marketplace or run the risk of departing from practice in the real economy—of possibly having nothing to do with the way people and businesses, those who actually operate our economy, really are.

Today, I am going to discuss two such risks as I see them: the current program of quantitative easing and the effect of the Dodd–Frank legislation aimed at preventing “too big to fail.” I’ll do this in short order and as provocatively as possible so as to give professors Calomiris and Svejnar plenty of ammo to use during the inquisition that will follow my remarks.

Monetary Policy and Quantitative Easing

I have argued against what I have called “Buzz Lightyear” monetary policy—pledging to hold the federal funds rate at zero seemingly to infinity and beyond, while purchasing longer-term Treasury securities at a pace of $45 billion per month, reinvesting principal payments on all agency debt and agency mortgage-backed securities (MBS) and purchasing MBS at a pace of $40 billion per month.[5] Indeed, other than our initial program to underpin a recovery in the housing market with our initial tranche of purchases of MBS, I have opposed all other large-scale asset purchases or quantitative easing (QE) programs. Why have I been so obstinate in my opposition to this well-intended program?

I fully understand its theoretical underpinnings. But I question its efficacy.

Confined as the Fed is at the “zero bound,” the only means of adding monetary fuel to the economy has been to purchase Treasury and MBS securities. When we buy something, we pay for it, putting money into the economy. That money—backed by an assurance that the FOMC will hold interest rates at zero and continue large-scale asset purchases for a prolonged period—should, theoretically, be put to use: a) by banks’ lending to consumers and to businesses that will expand employment, or b) by investors who, rediscounting valuations in the fixed-income and equity markets, will drive those markets higher in price, creating a “wealth effect.” This wealth effect should lead to further consumption as well as greater employment by businesses whose balance sheets have been reconfigured and enriched both by the cheapest leverage in American history and by booming prices for their stock.

All these actions are in keeping with the dual mandate that the Federal Reserve was given by the Congress of the United States. It calls for us to operate independently both to maintain price stability and conduct policy in a way that engenders full employment. Given that inflation and, importantly, inflationary expectations are presently “contained,” it would seem theoretically compelling to pursue the policy that we have undertaken.

But a not-so-funny thing has happened on the way to the reality forum. While bankers and other sources of credit have slowly but consistently liberalized their lending practices, borrowers have not been especially keen to put cheap and super-abundant credit to use in expanding payrolls to the degree the FOMC desires.

To be sure, we have, as hoped, seen a reinvigorated housing market. Indeed, FOMC records will show that based on the superb work done by two housing-market experts at the Dallas Fed—John Duca and Anthony Murphy, working with John Muellbauer at Oxford—and thanks to our field soundings with housing and housing-related business leaders, the Dallas Fed was way ahead of others at the FOMC table both in warning of the housing market debacle and then recognizing the housing recovery.[6] The fact that the housing-market gears have now begun to mesh is why I believe we are running the risk of overkill by continuing our mortgage-backed securities purchase program at the current pace and would suggest tapering off those purchases.

As to the more broadly impactful Treasury purchases, occurring as they have simultaneously with a loss of confidence in the euro bond markets—I like to say that, relatively speaking, the U.S. economy has been the “best-looking horse in the glue factory”—they have indeed led to a massive bond and stock market rally. For the ninth time in U.S. history, we have experienced a doubling of the market indexes; corporate borrowing rates are at the lowest levels on record, including those for CCC-rated credits that are just north of default.

That’s the good news. Some sharp market operators have done very well. For private-equity firms, for example, hyper-accommodative monetary policy has offered a chance to go back to the glories of payment-in-kind and other financial techniques that enrich financiers but may not create employment. For the largest banks and financial institutions, policy has helped dig them out of the holes in which they found themselves (including the hole of executive compensation). And for the wealthiest investors, even unto the revered Oracle of Omaha, there has been the windfall of super-abundant credit that, after adjusting for tax deductions on interest and a modicum of inflation, is practically free. Ordinary savers and retirees have benefited from the turnaround in the all-important housing sector, but with the remainder of their savings, they have been waylaid on the sidelines of the zero bound. In addition, the 5,500 or so smaller banks that are the backbone of our communities have seen their interest margins squeezed severely. The wealth effect, in other words, has been unbalanced. Main Street does not seem to have been impacted to the same degree as Wall Street.

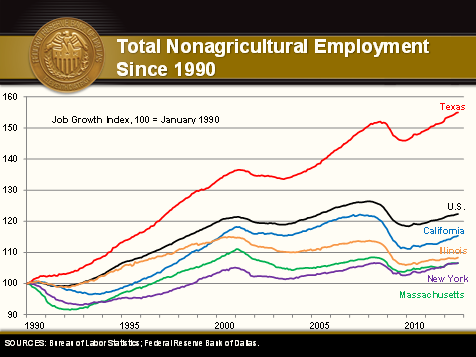

To be sure, as mentioned, businesses have been able to improve their balance sheets and are enjoying higher stock market valuations of their businesses. However, thus far, businesses have pursued payroll-expanding job creation with less enthusiasm than had been hoped for. Unemployment remains annoyingly high. There are some pockets of exception like Texas, which now operates at employment levels 3.1 percent above its prerecession peak and, over the last decade, has created jobs across the entire income spectrum. Nationwide, meanwhile, job creation has been weak and in the important middle-income quartiles has been shrinking.

Employers large and small, privately owned or publicly traded, will tell you that despite access to cheap and abundant capital, they are hesitant to make long-term commitments, including hiring significant numbers of permanent workers. They cite uncertain growth prospects for the goods and services they sell at home, where consumption is retarded by slow growth in employment and, lately, by the increase in payroll taxes. And abroad, these employers point to the dampened consumption stemming from the economic debacle in Europe and its knock-on effects on China and the export-led emerging economies. They are uncertain about fiscal policy, not knowing what their taxes will be and what will happen to all-important federal spending that directly impacts them or their customers. They are uncertain as to the ultimate effect on their cost structures of the seemingly endless expansion of health care and other mandates and regulations, however meritorious their intention. And, for some, there is a deeply imbedded worry that the Fed’s contortion of the yield curve and cost of money cannot last forever, or, if it lasts too long, will eventually result in financial bubbles and/or uncontrollable inflation, adding another uncertainty to the plethora of uncertain factors that already plague them.

As I walked down memory lane in preparation for this lecture today, I thought of my days at business school in the mid-1970s. Everything we learned in business school was oriented toward operating and growing companies under the assumption of constrained, conservative debt markets and a fundamentals-driven equity market. Today, the opposite obtains: Credit is super-abundant and stock market behavior is conditioned not so much by the fundamental performance of its underlying companies but by increasing doses of monetary Ritalin.[7] Against this backdrop, I am not surprised by the reaction of businesses. Operating in a highly uncertain environment, it is eminently sensible for them to defensively use their newly strengthened balance sheets to buy back shares and pay out dividends or employ them offensively in ways—say, in making acquisitions—that often lead to employee rationalization, not payroll expansion for U.S. workers.

This is how businesses really think; this is the way people really are.

The bottom line is that rather than achieve the intended theoretical effect, I believe the policy of super-abundant money at costs deviating substantially from normal equilibrium levels may ultimately prove to be counterproductive. Or it may restrain the benefits that theory might suggest.

If this is so, should we continue with the current program of QE? I have argued we should not, that we are pushing on a string. But let me qualify this. I was, indeed, against the escalating rounds of QE, questioning their efficacy. But now that we have them in place, and the fixed-income and stock markets are hooked on the monetary Ritalin that we have dispensed in ever-larger doses, it would, in my opinion, do great harm to force a sudden withdrawal. So, I have argued that it would be best to taper the dose of QE so that markets can adjust gradually to the eventual removal of this treatment and return to pricing securities on the basis of fundamentals.

Am I right or wrong? I pose this question to professors Calomiris and Svejnar for the discussion that will follow.

Let me add one more thought for the good professors to contemplate before moving on to the topic of too big to fail (TBTF). This is, admittedly, out of left (or perhaps in the spirit of Irving Kristol, right) field: Having posited that, thus far, the wealth-effect phenomenon has been concentrated in both the housing sector—a Main Street benefit, and a powerful one—and the hands of the savviest operators—those most able to exploit free and abundant money, primarily a smaller base consisting of the big banks and the investment community on Wall Street—and given that private sector job creators are in a defensive crouch and the federal government is likely to remain in cost-containment mode, might there be a way for others charged with fiduciary responsibility to the broader public to capitalize on the current moment?

For example, Texas, with its highly rated government credit, has navigated its 26 million people through the Great Recession with strong fiscal fundamentals and a dynamic economy that has persistently outperformed the United States and, indeed, all other large states for at least the past two decades.[8] Might it make sense for Texas to issue ultra-long bonds at currently prevailing ultra-low rates to finance the state’s longer-term infrastructure needs? I have in mind a Texas Century Bond. The public benefit would come from saving on interest payments that will inevitably rise over time from their unprecedented low levels—certainly sometime in the next 100 years—meanwhile financing highways, water projects, universities and the like that will be needed to continue serving the state’s growing population and expanding economy. If ever there were a window for such an issuance, it surely would be now.

Domestic entities seeking to match longer-term liabilities and commitments as well as sovereign investors like the Norwegians are keen on finding “risk free” dollar-denominated assets of long duration. Mexico and private universities such as the Massachusetts Institute of Technology have placed century bonds. Because the U.S. government cannot capitalize on such demand and is stuck in a rut of issuing short-dated debt so as not to add to its deficits, could or should other dollar-based “sovereign” issuers like the best credit-rated states, especially a large one like Texas, do so? I’ll just throw that out for your contemplation.

Too Big to Fail

Now, on to TBTF.

Everyone and their sister knows that financial institutions deemed TBTF were at the epicenter of the 2007–09 financial crisis. Previously thought of as islands of safety in a sea of risk, they became the enablers of a financial tsunami. Now that the storm has subsided, my colleagues at the Dallas Fed and I submit that they are another key reason accommodative monetary policy and government policies have failed to adequately spur the economic recovery. Our research director, Harvey Rosenblum, and I first wrote about this in an article published in the Wall Street Journal in September 2009, titled “The Blob That Ate Monetary Policy.”[9] Put simply, sick banks don’t lend. Sick—seriously undercapitalized—megabanks severely constricted their usual lending and capital-market activities during the crisis and economic recovery. They brought economic growth to a standstill and spread their sickness to the rest of the banking system.

Congress thought it would address the issue of TBTF through the Dodd–Frank Wall Street Reform and Consumer Protection Act. Preventing TBTF from ever occurring again is in the very preamble of the act. We contend that Dodd–Frank has not done enough to corral TBTF banks and that, on balance, the act has made things worse, not better. We submit that, in the short run, parts of Dodd–Frank have exacerbated the weakness in economic growth by increasing regulatory uncertainty in key sectors of the U.S. economy. Despite its good intention, it has been counterproductive, working against solving the core problems it seeks to address.

Let me define what we mean when we speak of TBTF. The Dallas Fed’s definition is financial firms whose owners, managers, creditors, shareholders and customers believe them to be exempt from the processes of bankruptcy and creative destruction. Such firms capture the financial upside of their actions but largely avoid payment—bankruptcy and closure—for actions gone wrong, in violation of one of the basic tenets of market capitalism (at least as it is supposed to be practiced in the United States). Such firms enjoy implicit subsidies relative to their non-TBTF competitors. They are thus more likely to take greater risks in search of profits, protected by the presumption that bankruptcy is a highly unlikely outcome.

The phenomenon of TBTF is the result of an implicit but widely taken-for-granted government-sanctioned policy of coming to the aid of a financial institution deemed to be so large, interconnected and/or complex that its failure could substantially damage the financial system. By reducing a TBTF firm’s exposure to losses from excessive risk taking, such policies undermine the discipline that market forces normally assert on management decisionmaking.

The reduction of market discipline has been further eroded by implicit extensions of the federal safety net beyond commercial banks to their nonbank affiliates. Moreover, industry consolidation, fostered by subsidized growth (and during the crisis, encouraged by the federal government in the acquisitions of Merrill Lynch, Bear Stearns, Washington Mutual and Wachovia), has perpetuated and enlarged the weight of financial firms deemed TBTF. This reduces competition.

Dodd–Frank does not do enough to constrain the behemoth banks’ advantages. Indeed, given the economies of scale in handling regulation, Dodd–Frank’s excessive complexity works to undermine the competitiveness of smaller banks, thereby offsetting some of the act’s other aspects that curtail TBTF banks’ dominance. It unwittingly exacerbates the problem it set out to solve.

Andrew Haldane, the highly respected member of the Financial Policy Committee of the Bank of England, addressed this at last summer’s Jackson Hole, Wyo., policymakers’ meeting in witty remarks titled, “The Dog and the Frisbee.”[10] I highly recommend this speech to you.

Haldane noted that Dodd–Frank comes against a backdrop of ever-greater escalation of financial regulation. He pointed out that nationally chartered banks began to file the antecedents of “call reports” after the formation of the Office of the Comptroller of the Currency in 1863. The Federal Reserve Act of 1913 required state-chartered member banks to do the same, having them submitted to the Federal Reserve starting in 1917. They were short forms; in 1930, Haldane noted, these reports numbered 80 entries. “In 1986, [the ‘call reports’ submitted by bank holding companies] covered 547 columns in Excel; by 1999, 1,208 columns. By 2011 … 2,271 columns.” “Fortunately,” he added wryly, “Excel had expanded sufficiently to capture the increase.”

Though this increasingly complex reporting failed to prevent detection of the seeds of the debacle of 2007–09, Dodd–Frank has layered on copious amounts of new complexity. The legislation has 16 titles and runs 848 pages. It spawns litter upon litter of regulations: More than 8,800 pages of regulations have already been proposed, and the process is not yet done.

In his speech, Haldane noted—conservatively, in my view—that a survey of the Federal Register showed that complying with these new rules would require 2,260,631 labor hours each year. He added: “Of course, the costs of this regulatory edifice would be considered small if they delivered even modest improvements to regulators’ ability to avert future crises.” He went on to argue the wick is not worth the candle, before concluding: “Modern finance is complex, perhaps too complex. Regulation of modern finance is complex, almost certainly too complex. That configuration spells trouble. As you do not fight fire with fire, you do not fight complexity with complexity. [The situation] requires a regulatory response grounded in simplicity, not complexity.”

This case for more effectively treating TBTF is especially compelling given the subsidy these institutions now enjoy by virtue of their protected status.

This TBTF subsidy is quite large and has risen after the financial crisis. Recent estimates by the Bank for International Settlements, for example, suggest that the implicit government guarantee provides the largest U.S. bank holding companies with an average credit rating uplift of more than two notches, thereby lowering average funding costs a full percentage point relative to smaller competitors.[11] Our aforementioned friend, Andy Haldane, estimates the implicit TBTF global subsidy to be roughly $300 billion per year for the 29 global institutions identified by the Financial Stability Board (2011) as “systemically important.”[12] To put that $300 billion estimated annual subsidy in perspective, all the U.S. bank holding companies summed together reported 2011 earnings of $108 billion.

Harvey Rosenblum and I, and our team at the Dallas Fed, have proposed a simple amendment to Dodd–Frank to remedy the TBTF pathology. We would eliminate the mumbo-jumbo, ineffective and costly complexity of the law; relieve the regulatory imposition it imposes on non-TBTF banks that do not pose systemic or broad risk to the economy or financial system; and eliminate the unfair subsidy the TBTF holding companies enjoy at the expense of their smaller competitors. Our proposal would effectively level the playing field for all banking organizations and provide better protection for taxpaying citizens.

I laid our proposal out in a speech in Washington, D.C., on Jan. 16. You might access it and study its details.[13] In a nutshell, we recommend that within a complex bank holding company, only the commercial banking operations that intermediate short-term deposits into longer-term loans would benefit from federal deposit insurance and access to the Federal Reserve’s discount window. All other operations of a complex bank holding company and all “shadow banking” affiliates of that company would not have this protection or access to the Fed’s window. To reinforce the understanding that taxpayers will not come to the aid of the risks taken by those entities, every customer, creditor and counterparty of every shadow-banking affiliate and of the senior holding company would be required to sign a new covenant, a simple disclosure that need be no more complex than this: “Conducting business with this affiliate of XYZ bank holding company carries NO federal deposit insurance or other government protection or guarantees. The counterparty herein fully understands that in conducting business with XYZ’s banking affiliate, it has NO federal government protection or guarantees, and its investment is totally at risk.”

Unfortunately, established customer relationships are slow to change. To accelerate the transition to a more competitive financial system, our proposal has a third element to help level the playing field. Specifically, we recommend that the largest financial institutions be restructured so that every one of their corporate entities is subject to a speedy bankruptcy process, and in the case of banking entities, that each be of a size that is “too small to save.” This would underscore to customers and creditors that a credible regime shift has taken place, and the reign of TBTF policies is over.

To circle back to Irving Kristol, I believe this suggested remedy to the pathology of TBTF “works, in a quite simple, material sense” and is “congenial to a large measure of personal liberty.” It most certainly dispenses with fantastical notions of the way people really are.

I have thrown a lot at you in this long speech. Thank you for tolerating me. Now, in the best tradition of central bankers, I will do my utmost to avoid answering any questions you and the good professors present may ask.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- Columbia University’s School of International and Public Affairs, Spring 2013 Distinguished Speaker in International Finance and Economic Policy.

- “About the film: Finding My Way to the Alcoves (1999),” by director Joseph Dorman, PBS Online.

- Two Cheers for Capitalism, by Irving Kristol (New York: Basic Books 1978).

- “Three Cheers for Irving,” by David Brooks, New York Times, Sept. 22, 2009, p. A31.

- See “The State of the West (With Reference to George Shultz, Eisenhower, Buzz Lightyear, George Strait, the San Francisco Fed and Adam and Eve),” speech by Richard W. Fisher, Nov. 15, 2012.

- See, for instance, “When Will the U.S. Housing Market Stabilize?” by John V. Duca, David Luttrell and Anthony Murphy, Federal Reserve Bank of Dallas Economic Letter, vol. 6, no. 8, 2011.

- Ritalin is a psychoactive drug classified with cocaine and morphine as highly addictive. It is widely used to treat children and is considered by many to be overprescribed.

- See chart below:

- See “The Blob That Ate Monetary Policy,” by Richard W. Fisher and Harvey Rosenblum, Wall Street Journal, Sept. 27, 2009.

- See “The Dog and the Frisbee,” by Andrew G. Haldane and Vasileios Madouros, Bank of England, paper presented at “The Changing Policy Landscape” symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyo., Aug. 30-Sept. 1, 2012.

- Bank for International Settlements 2011/2012 Annual Report, June 24, 2012, pp. 75–6.

- See “On Being the Right Size,” speech by Andrew Haldane, Bank of England, at the 2012 Beesley Lectures, Institute of Economic Affairs’ 22nd Annual Series, London, Oct. 25, 2012.

- See “Ending ‘Too Big to Fail’: A Proposal for Reform Before It’s Too Late (With Reference to Patrick Henry, Complexity and Reality),” speech by Richard W. Fisher, Jan. 16, 2013.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.