The Status of the U.S. Economy and a Perspective on 'The Modern Monetarism' (With Reference to Sheila Copps, Thomas Jefferson, Paul Volcker and William Shakespeare)

January 16, 2013 Toronto

Thank you, Hugh (MacKinnon). I am honored to speak to this annual directors’ dinner of the C.D. Howe Institute and on the second day of Stephen Poloz becoming the governor of the Bank of Canada. Evan Siddall, his special adviser, is here tonight to keep an eye on me!

Thank You, Canada

Before getting to my formal remarks, I want to say something about Canada that has nothing to do with monetary policy. On Sept. 11, 2001, I was on a flight, returning from the celebration of the opening of the Jewish Museum in Berlin two days earlier.

On the morning of that fateful day, my flight was en route to New York City when we were suddenly redirected to Toronto. We had been prevented from landing in New York, the pilot announced, because of “severe headwinds.” We were told nothing more. After landing and deplaning at Pearson and going through an extensive screening process, we were ushered into a briefing room and only then learned what little was known at the time of the horrors that had occurred. Your government and our consular officials said that we were to remain in Toronto until order in America was restored, adding they were confident we would be well cared for as guests of a very compassionate Canada.

Sure enough, when we exited the airport, we found a line of cars driven by private citizens who had spontaneously come to the airport to take any and all of their American brethren into their homes and care for us while we waited anxiously to learn more of what had happened and why.

From the home of my Canadian host, I somehow managed to get through by cell phone routed through Dallas to my wife, Nancy. She was hiding with our two youngest children in the basement of our house in Washington, D.C. With the passage of time, it is easy to forget how chaotic and frightful that day was. It was unclear if all of Washington was under attack; rumors abounded that the Capitol and the White House were targeted. Our son had seen the images from Flight 77’s crash into the Pentagon and had run home from school with his frightened little sister in tow.

I wanted to make sure my wife and children were safe. She reported they were and then asked if I was. I remember saying, “I am safe in the hands of our Canadian brothers and sisters.”

Every chance I get, I thank Canadians for the caring and unconditional friendship you and your countrymen showed the United States on that infamous day. For the rest of my life, Canada will hold a special place in my heart.

Indeed, I love this country so much that I have even found it possible to forgive Sheila Copps for forcing me to listen to endless re-loops of songs by Gordon Lightfoot when I was deputy U.S. trade rep and negotiated with her during her reign as minister of Canadian heritage![1]

The Predicament of the U.S. Economy: Growth …

Now, on to the status of the U.S. economy and monetary policy—of special interest to you because we account for three-quarters of Canada’s goods exports and a substantial amount of Canadian direct and portfolio investment.

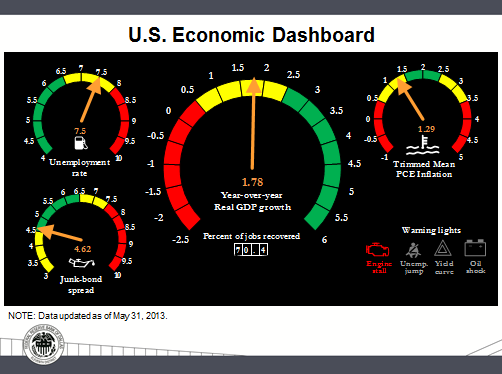

Here is a handy graphic we use at the Dallas Fed as a simple indicator of the current predicament of the U.S. economy:

As shown, the most recent data for real gross domestic product (GDP) and inflation—as measured by the Trimmed Mean Personal Consumption Expenditures (PCE) Index, the Dallas Fed’s preferred indicator—have both increased less than 2 percent year over year after first-quarter GDP growth was revised to 2.4 percent and the 12-month run rate for Trimmed Mean PCE inflation came in at 1.3 percent at the end of April.

The dashboard indicates that the U.S. economy is cruising along at what appears to be near-stall speed—note the “Engine stall” red warning light. The unemployment rate gauge is not red because it declined to 7.5 percent in April. As indicated by the odometer box, we have traveled some distance in job creation, even though we have not seen the job creation we might have hoped for in a typical recovery: 70.4 percent of jobs lost in the recent recession have been recovered, up from about 50 percent only a year ago.

The warning light for the yield curve should be pink, if not yet red, for, if anything, it is robust to the point of possibly becoming problematic in giving rise to speculative impulses. Despite the most recent widening, junk-bond spreads are below 5 percent, as shown; nominal yields for even the lowest-grade bonds (CCC-rated credit that is one notch above default) have fallen to below 7 percent from double digits only a year ago. This is of interest because, according to Dealogic, we have had $187 billion of junk bonds issued in the U.S. so far this year, a record.[2] Further, covenant-light lending is on a tear. And unless you’ve been living on another planet, you know we have experienced a roaring bull market for equities. Thus the “oil lamp,” shown in the lower left corner of the dashboard, depicts that the Fed has supplied plenty of lubrication for the engine of job creation.

Over the four years since the recession ended in June 2009, GDP growth has averaged just 2.1 percent, hewing to a narrow year-over-year range of 1.5 to 2.8 percent. It is noteworthy that the fraternity of U.S. professional economic forecasters has been consistently disappointed: Forecasts made at the beginning of 2010, 2011 and 2012 all overpredicted growth. At the onset of this year, the median projection of professional forecasters called for 2.4 percent GDP growth for all of 2013, and that, too, has been challenged by first-quarter data that came in below expectations, raising fears of “déjà vu all over again.”

However, the April jobs report, revisions of previous jobs data, and reports concerning consumer behavior in May have put some spring back in economists’ steps despite the malaise in manufacturing that has persisted for some time (long before yesterday’s Institute for Supply Management manufacturing numbers were released). Initial claims for unemployment insurance are now back on a downward trend, retreating toward prerecession levels, and recent retail sales numbers and indicators of consumer activity have surprised to the upside. This would appear to indicate that consumers may have digested delayed tax rebates and the increase in payroll taxes, and are relishing the benefits of lower gasoline, food and other prices. So the recovery presently appears to be strong enough to propel hopes that consumption will help employment growth gradually improve over the long term.

I know audiences like this always want to be given some forecast of economic growth, especially by someone who they assume has some inside knowledge. I’ll stick my neck out in a moment, after a brief discourse on where we are on the inflation front. But I ask that you treat any forecast from any source with what I like to call “Arrow’s Caveat.”

During World War II, future Nobel laureate Ken Arrow served as a weather officer in the Army Air Corps. He and his team were charged with producing month-ahead weather forecasts. Being a disciplined analyst, Arrow reviewed the record of his predictions and, sure enough, confirmed statistically that the corps’ forecasts were no more accurate than random rolls of dice. He asked to be relieved of this futile duty. Arrow’s recollection of the response from on high was priceless: “The commanding general is well aware that the forecasts are no good. However, he needs them for planning purposes.”

… and the Outlook for Price Stability

The Fed’s most sacred duty is to see to the maintenance of price stability. Today, inflation is benign. With a jobless rate still well north of 7 percent, a high rate of underemployment, labor compensation rising at less than 2 percent per year, an outlook for abundant food crops and expanding energy resources, and near-record profit margins among operating businesses, there is little likelihood of cost–push pressures in 2013. Slower growth around the globe is putting the damper on demand–pull inflation. Provided the public remains confident in the Fed’s commitment to price stability, anchored by the stated 2 percent long-term target of the Federal Open Market Committee (FOMC), the chances of inflation rearing its ugly head in 2013 are presently extremely low. I am sticking my neck out for the next six months!

Indeed, the latest Trimmed Mean PCE inflation calculation done by the Dallas Fed for April posted a negative reading—minus 0.1 percent—for the first time since the raw data became available in 1977, with 44 percent of the basket of 178 components measured declining in price.[3] This is all subject to revision, but the drift is that the underlying inflation rate as we see it at the Dallas Fed, as mentioned, is running at a pace of 1.3 percent.

The Efficacy of Current Monetary Policy

As a hawk in the aviary of policymakers, I have for some years now said that the issue of the moment is not a meaningful threat to price stability. The issue is job creation. And the questions I keep raising at FOMC meetings regard our limited ability to affect it with our über-accommodative monetary policy.

With the Arrow Caveat in mind, my staff and I think there is a better-than-even chance that the present GDP growth consensus forecast of 2.4 percent by professional economists may be underestimating the underlying pace of growth. The housing market is in resurgence, contributing significant impetus to the economy. The Fed’s senior loan officer survey indicates that commercial banks are becoming more accommodative lenders, albeit remaining cautious. The snapback in housing and the harnessing of cheap and abundant money by the business sector have made for more manageable financial obligations. State and local governments, not just in my home power-state of Texas but elsewhere in the nation, are on a better financial footing and no longer appear to be a major drag on growth. New technologies are providing for cheaper and more abundant energy. Consumers continue consuming, an important component that represents 71 percent of the U.S. economy (compared with Canadian consumption accounting for 54 percent of national output). Monetary policy has helped drive interest rates to historic lows and equity markets to historic highs; if anything, as noted, it may be giving rise to excessive speculation and risk taking. In addition to the pricing of CCC debt and the surge in low-covenant lending, margin debt is climbing rapidly.

Even if we at the Dallas Fed are right and the overall outlook for the economy is better than the current dashboard or the conventional prognostications of economists, there exists a formidable brake on growth. It was referred to point-blank in the last statement issued by the FOMC: “…fiscal policy is restraining economic growth.”[4]

Fiscal policy is inhibiting the transmission of monetary policy into robust job creation.

As this is an after-dinner speech and a little levity is always helpful in making a point at this time of night, here is my favorite spoof on the historical behavior of fiscal policy makers in Washington, D.C.:

This would be funny if it were not so sad. The propensity of members of Congress has been to spend in excess of revenues to give pleasure to their constituents and garner their affection. They just didn’t get the memo that Jefferson wrote to Madison over two centuries ago: “We are ruined, Sir, if we do not overrule the principles that ‘the more we owe, the more prosperous we shall be,’ [and] ‘that a public debt furnishes the means of enterprise.’”[5] The good news is that, some 200-plus years later, the memo seems to have finally been received; there are numerous plans to rein in Congress’ spendthrift ways, and there have been improvements that have brightened the short-term outlook for the level of federal debt.[6] But, as yet, there has been little more than passive action.

Until the Congress and the president provide a clear road map to restoring fiscal rectitude, economic growth will continue to be impeded by undue uncertainty about future tax rates, future government purchases, future retiree benefits and all manner of factors that prevent the U.S. from achieving its long-run potential. Meanwhile, the divisive nature and petty posturing of those who must determine the fiscal path of the nation are further undermining confidence, hindering the upward momentum needed for a full recovery and limiting the effectiveness of monetary policy.

Here is the rub: Even if the arguments of those who wish for greater fiscal stimulus prevail, expansion in government purchases will have reduced effectiveness if it is thought that those purchases will be financed with higher future marginal tax rates, or the broadest tax of all, higher inflation. If you are an operating business, you have to discount this risk before adding significantly to payrolls and before undertaking capital expansion. In a similar vein, you need to consider how the opposite approach of cutting government expenditures might impact your top line if the cuts are in areas that affect the markets you sell into. Add to that the enormous uncertainty about how health care reform will impact your cost structure. And add to that the fact that community bankers—providers of the lifeblood of loans to small businesses, which are the impetus for new job creation and economic rejuvenation—are hamstrung by burdensome regulations and fees imposed in response to the misbehavior of their too-big-to-fail brethren. If you consider the economy from this perspective, you can see where brakes of the government’s own making are being applied, impeding the realization of our growth potential.

Decision-making under conditions of uncertainty is always a challenge for businesses; decision-making in a thick fog of uncertainty is well-nigh impossible. It negates the power of hyperaccommodative monetary policy to propel our economic vessel forward. The restraining influence of rudderless fiscal policy is readily seen in the piling up of excess reserves on the balance sheets of banks and in the coffers of operating businesses.

I argue that the Fed has no hope of moving the economy to full employment, despite having pulled out all the stops on the monetary front, unless our fiscal authorities get their act together. Those economic agents with the wherewithal to expand payrolls and put the American people back to work must have confidence that our fiscal authorities and regulation makers—the legislative and the executive—will reorganize the tax code, spending habits and the regulatory regime so that the cheap and abundant money we at the Fed have made available to invest in job-creating capital expansion in the United States is put to use. Until then, I argue that the Fed is, at best, pushing on a string and, at worst, building up kindling for speculation and, eventually, a massive shipboard fire of inflation.

I note that in his speech of last Wednesday to the Economic Club of New York, former Fed Chairman Paul Volcker highlighted that managing the supply of money and liquidity “to accommodate misguided fiscal policies, to deal with structural imbalances, [or] to square continuously the hypothetical circles of stability, growth and full employment” was a risky proposition for the Federal Reserve and warned that in attempting to do so, the Fed “will inevitably fall short.” He even referenced “pushing on a string.” And he added that, “The risks of encouraging speculative distortions and the inflationary potential—[note the word “potential,” not “present instance”]—of the current approach plainly deserve attention.” I am in complete agreement with Mr. Volcker. I urge you to read his speech if you wish to understand my personal concerns about the present course of monetary policy.[7]

A Shakespearean Scenario

Only time will reveal the efficacy of current policy and whether the risks that I and more experienced observers like Paul Volcker fret over are as substantial as we surmise, or whether we have made much ado about nothing.

If the Fed’s monetary policy were the stuff of Shakespearean drama with a prototypical five acts, one might say we are in the last scene of the third act of a play titled “The Grand Experiment in Modern Monetarism.” We will not know until the next two acts whether the play will end felicitously or otherwise.

Here is the CliffsNotes summary of the play thus far: The play opened with the great financial tempest of 2008–09, during which it appeared the ship of the mighty American economy would founder. A humble, once unassuming but suddenly daring captain named Ben Bernanke took firm control of the nation’s monetary helm in Act II, contriving innovative ways to keep the economy afloat by jury-rigging monetary policy and adopting radical maneuvers. These efforts succeeded in steering the ship of the economy away from the shoals of depression and deflation and into more tranquil waters.[8]

Act III began with a recovering economy heading on a more promising course. But the headway being made was substandard, hindered by the flotsam and jetsam of fiscal incompetence and rising fears of a new storm brewing in Europe. In an effort to propel the economy forward at a better clip, the FOMC commanded that unprecedented amounts of monetary fuel be provisioned for the financial system through large-scale asset purchases, colloquially known as QE2 and 3. These purchases pumped almost $1 trillion into the stores of reserves of banks. As yet, however, the banks have for the most part not shoveled that fuel into their boilers, lending only a small fraction of it to job-creating businesses and hoarding the remainder. Other members of the financial fleet, however, have been heartened by the turn of events, especially those who finance themselves through the issuance of stocks and bonds rather than through bank loans. Yet they, too, have been reluctant to transform their renewed means into robust job creation. Thus, the economy remains weaker than desired, and the ship of the economy is making less-than-desired headway.

The plot now thickens. Act IV, just beginning, will involve the drama of introspection, with the FOMC evaluating the utility of its navigational tactics, and, perhaps, fine-tuning them, if not altering the course.

Not until the final act will we know whether we have achieved the felicitous outcome of arriving at the desired port of an economy that grows sufficiently to bring about full employment without giving rise to inflation. With Shakespeare, the most pleasant plays typically end in marriage. The happy outcome to our economic predicament would entail a coupling of sensible fiscal policy with prudent monetary policy, carrying the American economy to new horizons, allowing the Fed to emerge a hero.

One can envision less-pleasant outcomes, however, some of them tragic. If the fiscal authorities—Congress and the president—are unable to provide tax, spending and regulatory incentives for job creators to use the cheap and abundant capital the FOMC has made available, the economy might remain endlessly becalmed. Should the FOMC try to compensate for fiscal authorities’ inability to act by provisioning still more monetary fuel, it may risk an explosion of speculative excess, or worse: an eventual inflationary conflagration, the debasement of money and the ruination of our economy and lifestyle. Should this prove the outcome, the Fed will be transmogrified from hero to villain.

To thicken the plot further, there is the uncertainty about whether command of the Fed will change hands during Act IV or V—whether the skipper who set us on the present course will stay (which I have personally advocated in other speeches) or be replaced by someone who wishes to remain on the course he set or change it. And whether in commissioning a new captain of the Fed’s fleet, if that is what the playwright decides, the Congress will introduce new dramatic themes that might steer the plot in new directions. Even now, the chorus is chanting about a Sound Dollar Act and other initiatives from behind the curtain.

All of which means that despite the mighty efforts of Captain Bernanke and his crew, present company included, we do not know how this play will end. Will “The Grand Experiment” prove an inspiring history, a tragedy or simply a comedy of errors? We will not know for some time. We will not know until the curtain drops on Act V.

I am tempted to end with a slightly adapted, trite reminder that “All the world’s economy is a stage and we policymakers are merely players upon it,” but I shan’t. Instead I’ll end by thanking you for listening to me and, again, expressing my gratitude for the solidarity you and your fellow Canadians have shown the United States through thick and thin.

And now, Hugh, time and patience permitting, I would be happy to avoid answering any questions you and your colleagues might have.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- As deputy U.S. trade representative, I was dispatched to Ottawa by President Clinton to negotiate away the legislation Minister Copps was proposing that would make it a criminal offense for U.S. companies to advertise in Canadian magazines, a clear violation of the North American Free Trade Agreement.

- See “Bond Investors Break Pattern, Dump ‘Junk,’” by Katy Burne, Wall Street Journal, May 31, 2013.

- For the latest reading of the Dallas Fed’s alternative measure of core inflation, see www.dallasfed.org/research/pce/index.cfm.

- The latest statement by the Federal Open Market Committee and the Board of Governors on the stance of monetary policy can be found at www.federalreserve.gov/newsevents/press/monetary/20130501a.htm.

- See Thomas Jefferson: The Art of Power, by Jon Meacham, New York: Random House, 2012, p. 251.

- See “Our Debt Problems Are Still Far from Solved,” Committee for a Responsible Federal Budget, May 15, 2013.

- If you wish to view a measure of this good man, read “The Ten Suggestions,” speech by Ben S. Bernanke at the Baccalaureate Ceremony at Princeton University, Princeton, N.J., June 2, 2013, www.federalreserve.gov/newsevents/speech/bernanke20130602a.htm.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.