Placing Manufacturing in Context

August 22, 2013 Orlando, Florida

Every morning there is a quote of the day on the ubiquitous Bloomberg screens. Monday’s was especially apt for today’s conference. It was from Frank Sinatra: “The best revenge is massive success.”

Bill Simon asked me to provide context for your discussion of a manufacturing revival in the U.S.A. I am delighted to do so. It is well-nigh time for us to once again become a “massive success” in manufacturing. But there are obstacles to doing so. If our manufacturing sector is to experience a lasting renaissance, significant changes in fiscal policy and regulation that emanate from Washington are sorely needed.

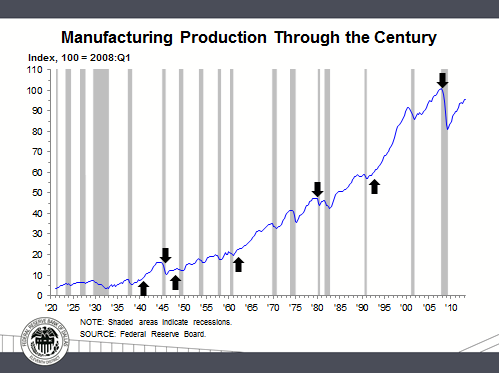

First, some historical context. Look at this chart:

U.S. manufacturing production was ramped up to fight the Second World War and, as you can see, declined precipitously after the war’s end. Then starting in 1947 or thereabouts, manufacturing output in America picked up slowly at first, adjusting to a post-WWII world, before accelerating to an expansion rate of 4.6 percent per annum from the time of the election of President Kennedy until Paul Volcker’s Fed broke the back of inflation and engineered a recession at the end of the 1970s. During the high-tech revolution of the 1990s, manufacturing production took off at a torrid pace, then bounced back from the tech wreck of the early 2000s until hitting the brick wall of the financial panic of 2007 and the severe recession that ensued.

The downturn in U.S. manufacturing output during the 2007–09 recession was on the order of 20 percent, the worst setback but for the defense-related decline following WWII and the 54 percent decline experienced during the Great Depression. Manufacturing output today is still about 5 percent below its December 2007 business-cycle peak.[1]

As for employment, manufacturing payrolls fell 16.6 percent between December 2007 and January 2010. They are still 12.9 percent below where they stood 5 ½ years ago.

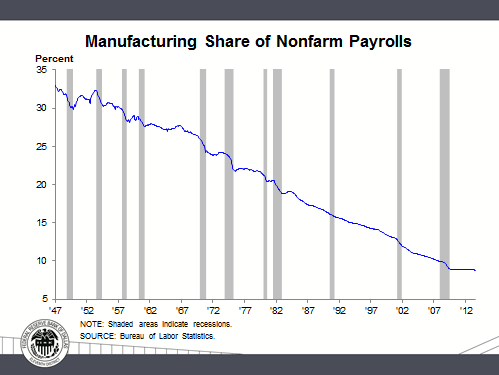

This raises the issue of productivity enhancement. Look at this chart:

Since the end of the post-WWII recession, manufacturers’ share of the nation’s payrolls has been in continual decline. Whereas at war’s end they represented 33 percent of nonfarm payrolls, today they account for less than 10 percent. To be sure, this reflects a rise in our nation’s prosperity: As nations grow richer, they produce and consume more services. Today, manufacturing accounts for only about 12 percent of gross domestic product. The divergence between trends in job and output shares is largely accounted for by a relentless drive by manufacturers to increase productivity. Workers today are dramatically more productive than the workers of our parents’ and grandparents’ generations because technology has enabled them to produce more with fewer hours worked and at less cost.

This is not going to change. The iconic economist, Joseph Schumpeter, coined the phrase “creative destruction.” In plain English, this means “out with the old, in with the new.” Americans are masters of replacing outdated methods with new ones. And it is by mastering new technology, new methodologies, and new techniques that we have the hope of revitalizing and bringing back to our shores a greater amount of the world’s manufacturing, regaining what was lost since the recession and—perhaps—bending upward the long-term manufacturing employment curve.

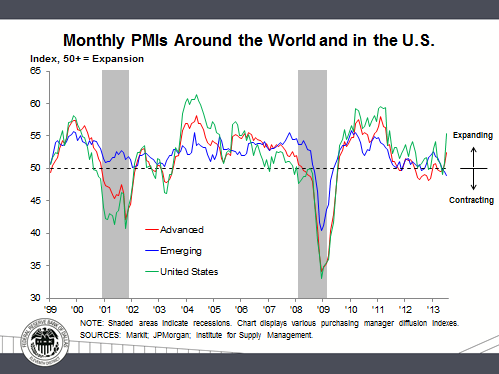

Now here is more recent history:

I have been saying for the past few years that the United States is the “best-looking horse in the glue factory.” This is certainly true in manufacturing. We have actually been outperforming the rest of the world on the manufacturing front as the recovery from the Great Recession has gained traction.

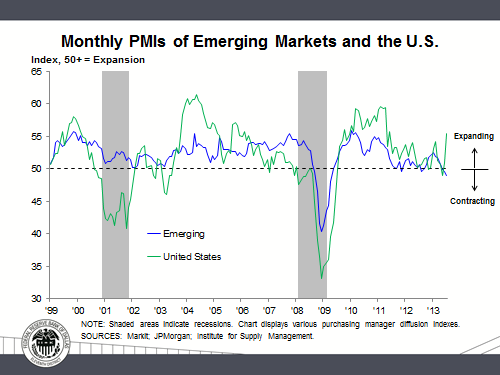

For the past three years, we have outperformed the “emerging” countries:

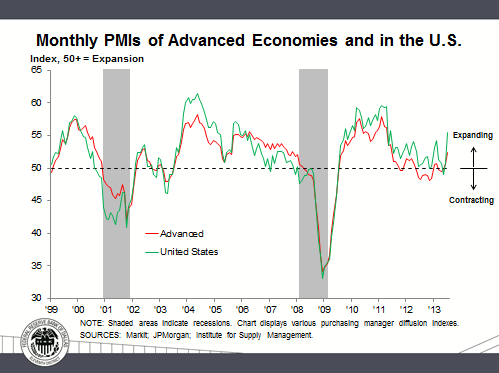

And we have outperformed the “advanced” countries:

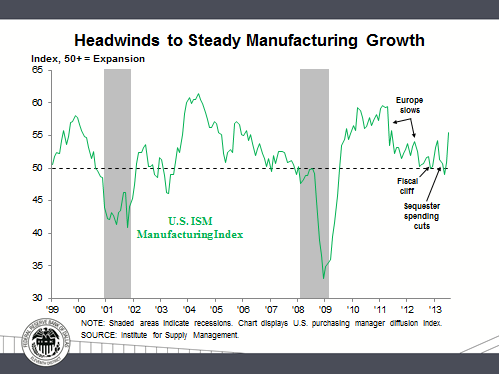

But in the last two years gains have been choppy. Notice how manufacturing growth slowed not only when Europe’s woes began to crimp confidence, but also when fiscal infighting dominated behavior in Washington.

So, two questions: How do we continue to outperform other nations? How do we reignite and sustain the manufacturing renaissance?

Monday’s front-page article of the Wall Street Journal pointed to some of the sources of strength in U.S. manufacturing, citing my old friend Ernie Preeg (who used to supervise me in writing economic policy decision memoranda for President Carter—which means Ernie must be 110 years old by now, a miracle of science!) and the work done by Hal Sirkin and his colleagues at the Boston Consulting Group.

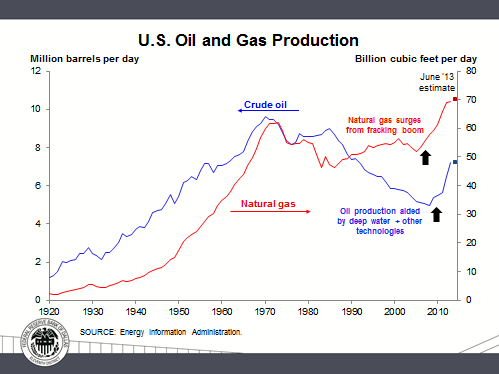

The article cited a critical factor influencing our destiny: the revolution occurring in oil and gas production. Thanks to a Houstonian named George Mitchell and other Schumpeterian practitioners who defied conventional wisdom and threw out the old and embraced the new, we have developed an abundance of natural gas and liquids production that are the stuff of production and the enablers of consumption. This is captured graphically here:

The Journal article also cited better relationships with unions and with workers in crafting flexible and innovative labor contracts, the rising cost of labor relative to productivity in China and the “world is our oyster” capacity for sales of exported U.S. manufactured goods, noting as examples the overseas sales of Hypertherm and Graco.

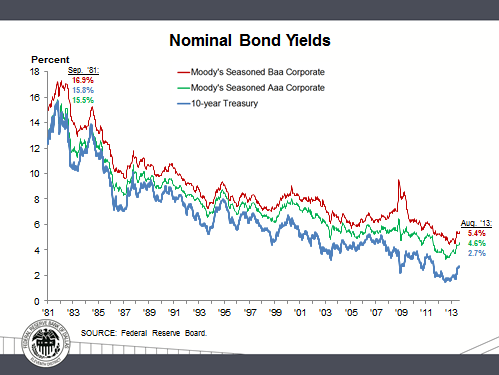

What the Journal article failed to cite is a historically profound enabler: Cheap and abundant money made possible by the Federal Reserve. I promised Bill Simon I would not venture into monetary policy today, and I won’t. But I will say this: While there are many risks in the policy that the Fed has been pursuing (and God and anyone who has suffered through my speeches the past few years knows I fret about those risks), every manufacturer of goods in America has been given a great gift by your central bank—the lowest cost of money in 237 years, an extension of the roaring bond market rally that has now run 32 years, and a broad stock market rally that began in March of 2009 and has gone on to bust through all previous record highs.[2]

Look at this chart of the three-decade-old bond market rally:

Our manufacturers, like all businesses public and private—large, medium and small—have also been given more than abundant natural gas and other sources of energy for their operations: They have been given abundant, super-cheap monetary fuel needed to stoke up their production engines and expand their businesses.

So what is holding us back from bending the curve of historical manufacturing production that I first showed you and extending our recent superior performance on the manufacturing front?

The Journal article I just mentioned noted inhibiting factors such as a shortage of skilled workers and the draw of growing markets like China, India and Brazil for plant location. And of course there’s the slowdown in Europe and in some emerging markets. But the article skirted the most vexing and self-inflicted inhibitor of all: fiscal and regulatory policy of the gang that can’t shoot straight in Washington.

I have spoken of this for years.

The Constitution unambiguously gives the Congress of the United States control of the fiscal purse strings. Yet all they have done under both Republican and Democrat presidents and the leadership of both parties in the upper and lower houses is spend and regulate with abandon.

Let’s cut to the chase: The remaining obstacle to being the absolute best economy for manufacturers and other businesses, bar none, has been fiscal and regulatory policy that seems incapable of providing job-creating manufacturers and other businesses with tax, spending and regulatory incentives to take advantage of the cheap and abundant fuel the Fed has provided.

After recovering most of the losses from the Great Recession, manufacturing growth has, on net, decelerated in the last two years. Ask any manufacturer what holds him or her back and they will tell you that they can’t operate in a fog of total uncertainty concerning how they will be taxed or how government spending will impact them or their customers directly. And as to asking their opinion of the impact of regulation on their businesses—from the Affordable Care Act to the thousands of other regulations enumerated in the Federal Register—don’t even go there, unless you delight in hearing profanities. I thought my college classmate Tom Stemberg, the founder of Staples, was remarkably constrained in his Wall Street Journal op-ed piece today as he pointed out that the 50,000 jobs he created from scratch might never have occurred under what he called today’s “blizzard of bureaucratic red tape.”[3]

We needn’t be condemned to the glue factory. American companies publicly held and private—large, medium and small—have taken advantage of the cheap and abundant money made available by the Fed’s very-accommodative monetary policy to create lean and muscular balance sheets. In response to the deep recession and the challenges of fiscal and regulatory uncertainty, they have rationalized their cost structures and ramped up productivity, leveraging IT, just-in-time inventory management and new production structures to the max. Their workers are more productive than ever.

I believe American manufacturers today have the potential, far and away, to be the most efficient operators in the world. We have countless manufacturers in every sector of goods production and assembly that are the equivalent of the Secretariats, Man o’ Wars, Citations, Seabiscuits or any great thoroughbred that has ever graced the track. They just need to be let out of the starting gate.

That gate is controlled by Congress, working with the president. If they would just let ’em rip, we would have an economy that would take off. Instead of settling for being the “best-looking horse in the glue factory,” we can become the wonder-horse that outpaces the rest of the world, putting the American people back to work and renewing the unparalleled magnificence of American prosperity.

Here is an image I want engraved in your minds. It is of Secretariat winning the Belmont Stakes by 31 lengths in 1973, leaving his competitors in the dust.

I want our manufacturers to be Secretariats, beating out the rest of the world by a stunning margin. We can do it. We must do it. We must insist that Congress practice a little Schumpeterianism of its own: throwing out old, counterproductive fiscal and regulatory policies and ushering in new ones that unleash job creators from the starting gates. Then we will experience a “massive success.” And as Old Blue Eyes said, that massive success will be “the best revenge”—sweet revenge, indeed, on those who say that a true renaissance of American manufacturing is beyond our reach.

Thank you.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- An alternate measure of output, called the value-added production series, shows that manufacturing output has nearly recovered its prerecession level.

- See remarks before the Ninth Annual Redefining Investment Strategy Education Forum, Dayton, Ohio, March 26, 2009, www.dallasfed.org/en/news/speeches/fisher/2009/fs090326.aspx.

- “A New Law to Liberate American Business,” by Thomas G. Stemberg, Wall Street Journal, Aug. 22, 2013, p. A15.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.