State of the Texas Economy: An Annual Update

December 19, 2013 Dallas, Texas

Thank you, Margaret [Keliher].

Today I am going to talk about one subject only: the Texas economy. As you know, just yesterday I was in Washington for the meeting of the Federal Open Market Committee (FOMC). At the end of the meeting, a statement was issued as to what that committee consisting of the 12 Federal Reserve Bank presidents and six members of the Fed’s Board of Governors decided regarding the course of monetary policy; Chairman Bernanke followed with a press conference. In keeping with our tradition, this morning I will refrain from commenting on the decisions made. We are under a self-imposed “communication blackout” regarding our views about macroeconomic developments or monetary policy issues until after midnight tonight. So if you wish, call me at home at 12:01 tomorrow morning and … incur the eternal wrath of my wife, Nancy!

Some of you have undoubtedly heard Gen. Philip Sheridan’s notable expression, “If I owned Texas and hell, I would rent out Texas and live in hell.” Although he reportedly recanted his statement, even a man as renowned for his cruelty as Gen. Sheridan would certainly have changed his opinion if he were around today. It wouldn’t have taken him long after crossing the river Styx to realize that rather than renting out Texas he would have been better off purchasing every bit of it. His return on investment would have been astronomical. My hunch is that Sheridan would want to live in Texas with you and me and would seek to rent out hell—perhaps to the U.S. Congress, though it would have to be free of charge given their fiscal predicament!

The Success of the Lone Star State

Here’s why I believe Texas is attractive to even the Gen. Sheridans of the world. The state’s total output—the equivalent of gross domestic product—is approximately $1.4 trillion, in the neighborhood of countries like Australia and Spain. We produce more oil than Venezuela or Norway and more natural gas than Canada or all 28 countries of the European Union combined. And we produce jobs like gee-whiz. A job is the source of income and the root of security and wealth for a productive people. Without income a person cannot consume and invest, engaging the engines of economic growth. Most importantly, a job is the route to dignity as we have historically defined it in America.

Jobs, Jobs, Jobs

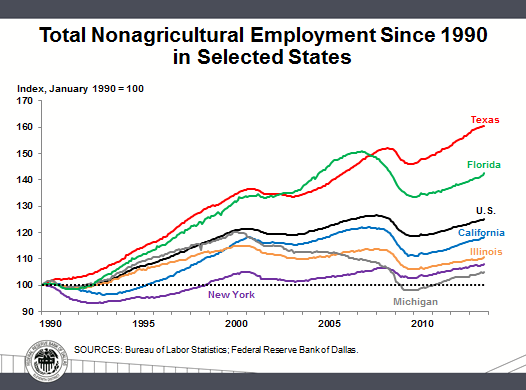

For the past 23 years, Texas has outpaced the country in job creation by a factor of more than 2-to-1. Here is a slide that shows the percentage increase in jobs created by several large states and for the U.S. as a whole since 1990:

Note the dotted black line drawn from the base of 100 in 1990. For the residents of the home of Motown or the Empire State or the Land of Lincoln, this graph does not present a happy picture. Since 1990, total employment growth in Michigan has been 5 percent, a compound annual growth rate of 0.17 percent, a pace that is one-twelfth that of Texas over the same period. New York and Illinois have not fared much better.

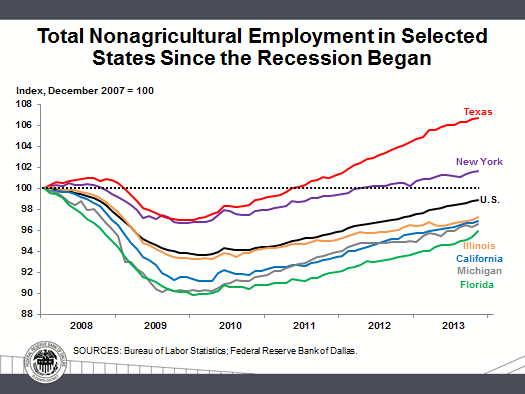

If you zoom in on the period since the onset of the financial crisis, you can see an even greater disparity in employment growth trends for Texas vis-à-vis the other large U.S. states:

In terms of jobs, Texas was one of the last states to lose ground during the recession and then led the pack in punching through employment levels that prevailed at the end of 2007. Fortunately, all of the selected states shown in the chart appear to be recovering, albeit rather slowly, from licks taken during the crisis. However, even the Empire State can’t compare, despite its devotees of the perspective captured by Saul Steinberg’s iconic 1976 cover of New Yorker, “View of the World from Ninth Avenue,” depicting everything west of the Hudson River as a vast wasteland. Compared to the view in 1976, Texas stands tall above all the rest. Why is that?

Why Are Things Bigger (or Better) in Texas?

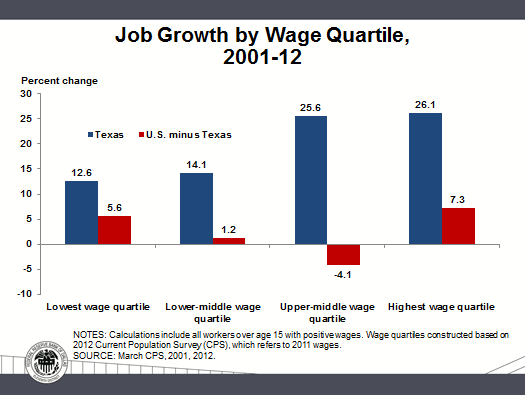

My friends in New York and other foreign places often criticize the relative success of the Lone Star State. They like to argue that Texas may well be creating more employment, but it is just low-wage jobs—the kind nobody wants. Well, truth be told, while low-wage jobs grow faster in Texas than elsewhere, so do all other jobs. As this next slide makes very clear, Texas also leads the rest of the nation in creating middle-income and high-wage jobs:

The U.S. ex-Texas has seen net job destruction for middle wage earners over the past decade. Meanwhile, Texas has experienced robust job creation for these important middle-income workers. Texas has not been immune to growing income inequality or the larger issue of labor market polarization, but the notion that Texas only creates minimum wage jobs is a myth.

Diversification Helps

Another Texas-growth-miracle fable I enjoy debunking goes like this: All of our state’s job and wealth creation comes from the booming energy industry. At the Dallas Fed, we account for the influence of oil and gas on our state’s welfare: Oil and gas extraction and mining directly employ 2.5 percent of our workforce—two-point-five percent. And the energy sector’s total contribution to our state’s total output is roughly 11 percent. So, yes, it is true: We have a strong energy sector in Texas. We are the No. 1 producer of oil and gas in the nation. I already mentioned that we produce more oil than Venezuela and more natural gas than Canada.

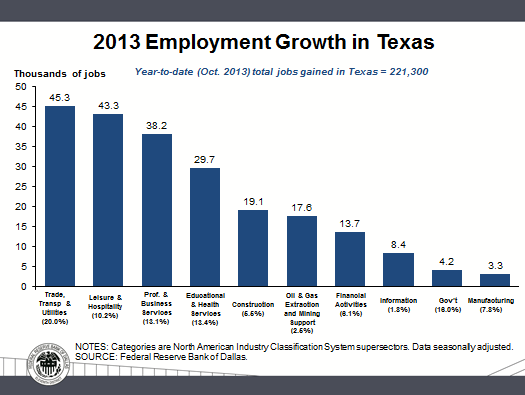

On net, high energy prices do, indeed, benefit Texans. But look at this slide of the number and diversity of jobs created by sector thus far in 2013. The vertical axis is the number of jobs created in thousands; the horizontal axis denotes the various job categories and, in parentheses, the share of total jobs represented by each category:

Oil and gas and mining and their support services accounted for 17,600 jobs, or 8 percent, of the 221,300 positions created in Texas in January through October of this year. Of course, the oil and gas sector has large multipliers, so the overall economic impact is greater than just these 17,600 jobs. For example, a University of Texas at San Antonio study estimates that the Eagle Ford Shale generated over $61 billion in economic impact and supported 116,000 jobs in 2012. And this is just one of four important oil and natural gas producing regions in the Eleventh Federal Reserve District that the shale boom has significantly affected. In 2012, the Permian Basin, Barnett, Haynesville and Eagle Ford accounted for 25 percent of U.S. oil supply and 28 percent of U.S. natural gas supply.[1]

Obviously, the oil patch has been a boon to Texas growth. But in 2013, trade, transportation and utilities accounted for 45,300 jobs; leisure and hospitality, 43,300; professional and business services, 38,200; educational and health services, 29,700; and construction, 19,100. As this chart shows, oil and gas is but the sixth strongest source of job creation. Ours is a diversified economy, creating jobs across the spectrum and in all income categories.

Blessed to Be in Texas

Here are some other facts and figures that help round out the economic picture of our state.

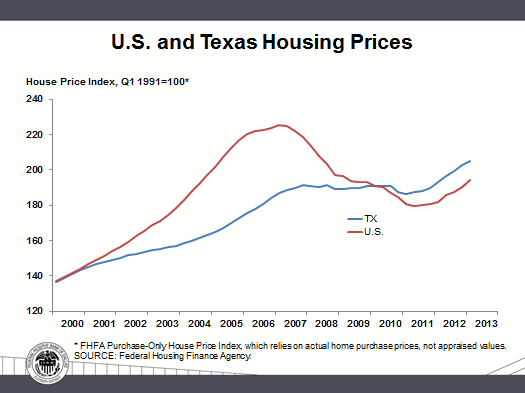

In the housing sector, Texas largely avoided the housing boom and bust that struck most of the nation. We did not experience a housing bubble:

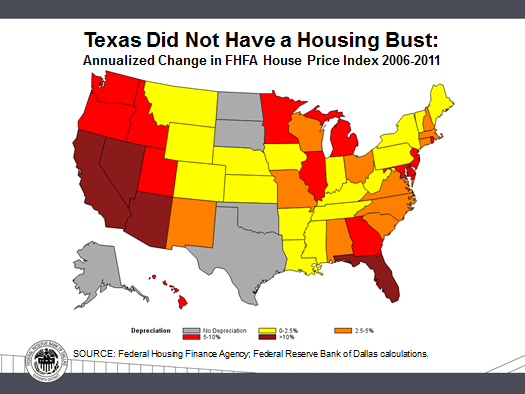

Nor did we suffer a housing bust:

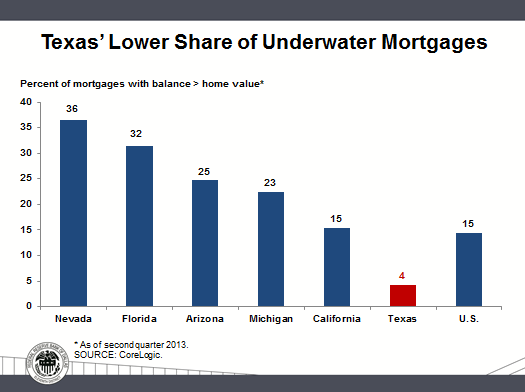

It helped that a 1997 amendment to the Texas Constitution allowed home equity loans and cash-out refinancing for the first time in the state’s history, but limited the amount of total debt (new loan plus the first mortgage) to no more than 80 percent of a home’s value. Combined with other factors such as ample land availability and fewer development and zoning restrictions, Texas housing stock increased during the last decade’s national boom without the rapidly rising home prices experienced elsewhere. With borrowing under control and house prices relatively stable, the state escaped the brunt of the housing sector fallout and experienced relatively few underwater mortgages:

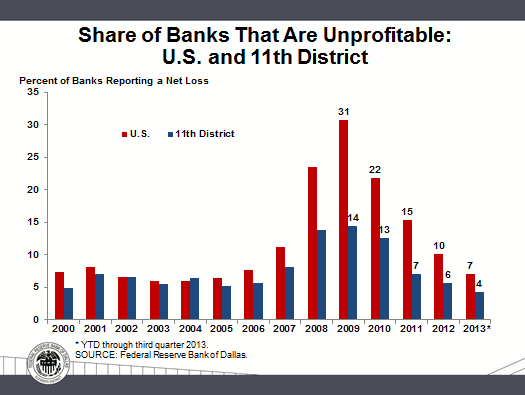

As to the sector we at the Dallas Fed supervise directly, fewer Texas banks have suffered net losses than in the rest of the nation:

¡Viva México!

Last, Texas is blessed to have a great neighbor to the immediate south. The Mexican economy has a significant impact on our state; a fortunate development for us, given that its economy is being transformed to a greater degree than most people here in El Norte realize. Admittedly, Mexico hit a rough patch in the first half of this year, but the Dallas Fed sees this as largely due to transitory factors.

It is surprising to many that Mexico recovered more quickly from the Great Recession than the United States. Inflation in Mexico has reached record lows after trending down for two decades following important reforms: central bank independence in 1994 and adoption of inflation targeting in 2001. Relatively low inflation, together with a stable peso, has protected the purchasing power of the Mexican consumer and allowed income and savings to grow. Further, after its horrific banking crisis in 1994–95 and an ensuing decade of stagnant lending, Mexico’s banking industry is well capitalized and growing again, and financial access, while still limited, is expanding quickly.

Mexico has also remained a staunch proponent of free trade. Exports and imports now make up 62 percent of Mexican economic output versus 17.5 percent as recently as 1980. Since Mexico joined the General Agreement on Tariffs and Trade (the forerunner of the World Trade Organization) in 1986 and ratified the North American Free Trade Agreement in 1994, it has forged 12 trade pacts with 44 nations.

On the fiscal front, Mexico’s 2012 budget deficit was a respectable 2.6 percent of GDP, which compares with 7 percent here. For all their differences, Mexican lawmakers have a commitment to fiscal discipline. They adopted a balanced-budget rule in 2006 and have chosen to abide by it rather than take the “kick-the-can-down-the-road” approach.

With all the progress in the macroeconomy, banking, finance and trade, structural reforms are what Mexico now needs to catapult to a leadership role among emerging-market economies. President Peña Nieto appears to be doing just that, pushing forward with structural modernization. Mexico might best be described, in economic parlance, as an “emerged country.”

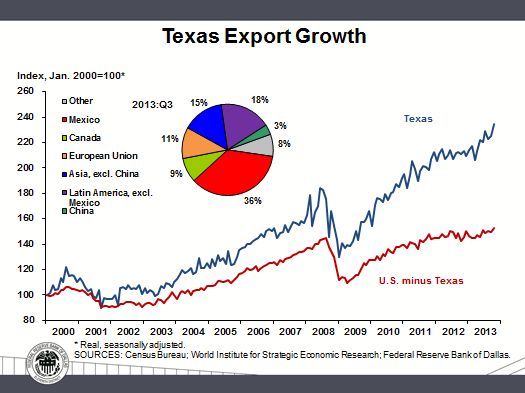

Exports, Exports, Exports

Texas benefits from a stronger Mexico in many ways, including on the export front. Here is a picture of the export growth from our trade relationships with our increasingly successful southern neighbor, as well as our other major trading partners:

One noticeable takeaway from this Texas export chart is the difference in the trajectory of the red and blue lines. Since the beginning of 2009, Texas exports have grown more than 70 percent while the nation’s exports, sans Texas, have increased at half that pace and are only now back to prerecession levels.

A Great Place for Immigrants

Of course, not every facet of the Texas economy is as supportive of the economic narrative expressed by the previous charts. Texas lags most other states in social services. We are the antithesis of the welfare state. And yet, if you believe people vote with their feet and put their money where their mouth is, the balance Texas has struck between job creation and social services seems appropriate enough to attract the diaspora from the other mega-states. We draw massive inflows of business investment, and we attract significant numbers of newcomers. In recent years, Texas has consistently welcomed more migrants—foreign and domestic—than any other state.[2]

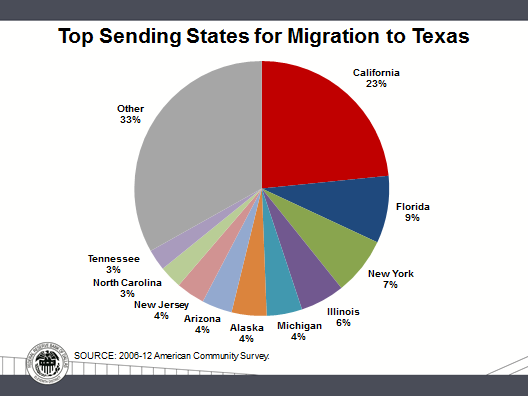

Domestic migration is a brain and human-resource gain for Texas and corresponding drain from sending states. Texas transplants have higher levels of education than native Texans and fill key niches in the high-skilled labor force. Since 2004, California has been the largest sending state by far—nearly one-quarter of net domestic migration to Texas between 2006 and 2012 came from California. In fact, so many Californians have been moving to Texas in recent years that the price of a one-way, 26-foot U-Haul rental truck from San Francisco to San Antonio is over twice the price for the same truck traveling in the opposite direction.

Many of the high-skilled migrants coming to our state are drawn to the high-tech, health care, professional and business services, and energy sectors in the fast-growing “Texas Triangle” cities—Austin, Houston and Dallas–Fort Worth. Internal Revenue Service tax records suggest that over 80 percent of taxpayers who moved into Texas during 2000–10 flowed into these three metropolitan areas, which also experienced significant inflows from other parts of Texas.

Thus, it comes as no surprise that these major metros have been huge contributors to the state’s strong overall employment growth. Year-to-date through October, Dallas–Fort Worth has added 87,400 jobs. The DFW metro area has maintained a year-over-year annual growth rate greater than 2 percent since January 2011 (34 months and counting). Due south, down Interstate 45, there’s a new Houstonian every four minutes, given current in-migration and net population growth trends. Houstonians are also on a homebuying tear; this year the pace has averaged one home sale every six minutes. In summary, Texas is attracting bright minds and eager workers from across the nation, and we are all better off for it.

And You Can’t Fault the Fed

There are many reasons that Texas is outpacing the nation in terms of economic growth. But one thing I can tell you with absolute certainty is that the underperformance of other large states, like California, relative to Texas has nothing to do with Federal Reserve policy. After all, Texas is subject to the same monetary policy as California and the other states of the union. Texans pay similar interest rates on mortgages and on commercial and industrial and consumer loans. We operate under the same federal regulatory regime governing banks and financial institutions and compete in the same financial markets as the rest of the nation.

So what gives? If my charts did not impress you, then perhaps the economic miracle of Texas can be best explained by John Steinbeck’s account of his travels across America with his poodle, Charley, in 1960:

I have said that Texas is a state of mind, but I think it is more than that. It is a mystique closely approximating a religion. And this is true to the extent that people either passionately love Texas or passionately hate it and, as in other religions, few people dare to inspect it for fear of losing their bearings in mystery or paradox. But I think there will be little quarrel with my feeling that Texas is one thing. For all its enormous range of space, climate, and physical appearance, and for all the internal squabbles, contentions, and strivings, Texas has a tight cohesiveness perhaps stronger than any other section of America. Rich, poor, Panhandle, Gulf, city, country, Texas is the obsession, the proper study, and the passionate possession of all Texans. [3]

Steinbeck nailed it. Above all, Texas is a state of mind where people are ready to work and get things done for the betterment of their families, communities, cities and beyond. We should be proud, indeed, to call the Lone Star State our home.[4]

I usually end my speeches by saying “In the great tradition of central bankers, I would now be happy to avoid answering your questions.” But given that monetary policy is off limits this morning, and I am never shy on Texas brag, I’d be glad to answer any and all of the questions you might have.

Thank you.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- For more information on the shale boom in the Eleventh District, see www.dallasfed.org/research/econdata/energy.cfm.

- For an excellent report on how immigration affects the Texas economy, see “Gone to Texas: Immigration and the Transformation of the Texas Economy,” by Pia M. Orrenius, Madeline Zavodny and Melissa LoPalo, Federal Reserve Bank of Dallas Special Report, November 2013, www.dallasfed.org/~/media/Documents/research/pubs/gonetx.ashx.

- Travels with Charley: In Search of America, by John Steinbeck, New York: Viking, 1962.

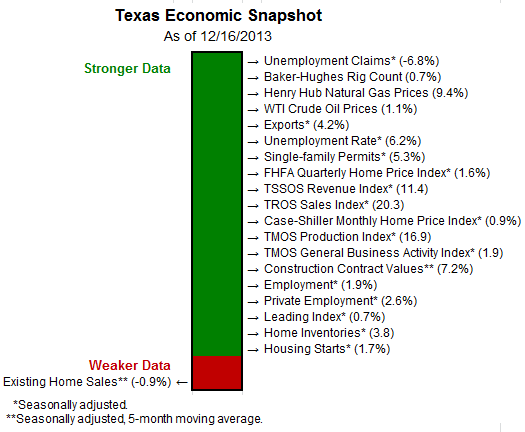

- A personal favorite snapshot of the regional economy I receive weekly from my staff shows how the tide of economic data has been in our favor recently. One could not have asked for a better Christmas present:

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.