R.I.P. QE3 ... Or Will It?

November 3, 2014 New York City

Thank you, Mickey [Levy], for that colorful introduction.

Unless you have been living under a rock (and no one in this audience looks like a cave dweller), you know that on Wednesday of last week, the Federal Reserve’s Federal Open Market Committee (FOMC) ended its program of purchasing Treasury bonds and mortgage-backed securities (MBS). Thus endeth QE3.

May it rest in peace.

Effects and Efficacy of QE3

Under QE3, the FOMC directed the New York Fed’s trading desk to purchase a total of $1.7 trillion in longer-term Treasuries and mortgage-backed securities, on top of the $2 trillion invested in the first two rounds of quantitative easing. When we started the first tranche of asset purchases in late 2008, our balance sheet had footings of around $900 billion; as the third and final round of quantitative easing ends, our balance sheet has reached $4.5 trillion.

The initial impetus for MBS purchases was a wide gap between MBS and Treasury yields, symptomatic of a dysfunctional mortgage-finance market. The Federal Reserve responded by purchasing $1.3 trillion in MBS and agency debt as part of QE1, the program of balance-sheet expansion that ran from late 2008 through the spring of 2010. Holdings of MBS and agency debt were then allowed to run off and by September 2011 had fallen to a little under $1 trillion. Holdings were stabilized at that level when proceeds from maturing agency securities and MBS began to be reinvested in MBS, starting October 2011.

The renewed expansion of MBS holdings that began in October 2012 as part of QE3 was motivated less by any sense that the mortgage-finance market was dysfunctional than by the notion that normal frictions in that market potentially provided monetary policy with leverage to stimulate the housing sector—and thus the economy as a whole—at a time when more-traditional policy tools had been exhausted. The FOMC majority pushed aside concerns that providing targeted support to housing is more properly the province of fiscal policy, and voted to proceed. From the start of QE3 to its conclusion, the Fed’s portfolio of agency securities and MBS expanded by about $850 billion. In the latest version of its normalization principles, released this September, the FOMC indicated that it expects to reduce its holdings in future years primarily through attrition.

What of the expansion of the Federal Reserve’s holdings of longer-term Treasury securities under QE3? Fed purchases of longer-term Treasuries amount to nothing more than the transformation of long-term Treasury obligations into short-term obligations of the Federal Reserve. Essentially, long-term government obligations are transformed into short-term government obligations. The government benefits from lower interest costs in the near term, but its future net revenues become more sensitive to future interest-rate increases. Government finance problems are reduced today, at a cost of potential future problems. The larger bank reserves become, the greater is the government’s future interest-rate exposure.

Chairman Ben Bernanke famously said that “the problem with QE is that it works in practice, but it doesn’t work in theory”—QE3 seemed to succeed in pushing interest rates lower out along the yield curve, energizing the bond market and lowering the hurdle rate for discounting cash flows and earnings of companies whose shares traded in stock markets.[1] This came, of course, at the expense of savers who kept their money in the most basic of short-term investments. But this was a cost that the committee felt was exceeded by the expected wealth effect.

Well before last week’s FOMC meeting, it seemed to me that QE3’s effectiveness had waned while its current and potential future costs were mounting. I was thus an enthusiastic supporter of killing the program.

Indeed, I would rather we had never had QE3 in the first place. To this day, I feel that the costs of accumulating another $1.7 trillion of Treasuries and MBS will be shown to exceed the benefits. And yet, as I have said on countless occasions, drawing on former Dallas Fed board Chairman Herb Kelleher’s love for bourbon, once we had QE3 in place, I considered it unwise to go directly from Wild Turkey to cold turkey for fear of getting the financial equivalent of delirium tremens; indeed, we saw that with the “taper tantrum” the markets threw in May of 2013. So I was an eager proponent of the tapering program the FOMC initiated in January of this year.

I want to be clear here. Especially at the beginning of QE3, when the nonsense term “QE infinity” was being broadcast by otherwise responsible analysts, journalists and pundits, rates dipped to lows that helped creditworthy businesses bolster their balance sheets and strengthen their wherewithal for future expansion. Again, even if you were living under a rock, you know that this gift of near-cost-free debt as measured in inflation- and tax-adjusted terms has thus far been used primarily to finance stock buybacks, increase dividends and fatten cash reserves, and recently, finance mergers by the most creditworthy companies. For those with access to capital, it was a gift of free money to speculate with. (One wag—I believe it was me—quipped that there was, indeed, a “positive wealth effect… the wealthy were affected most positively.”)

We know that monetary policy acts with long and variable lags. That characterization applies, in spades, to the unorthodox policy we have pursued at the zero bound, in terms of achieving full employment and hitting our 2 percent inflation target.

Together with the healthy rejuvenation of the balance sheets and equity prices of investment grade companies, we have seen what I consider to be a manifestation of an indiscriminate reach for yield, a revival of covenant-free lending, and an explosion of collateralized loan obligations (CLOs), pathologies that have proved harbingers of eventual financial turbulence.

Noticeably affected by QE3 have been the nominal yield levels of subpar credits and their spreads relative to investment-grade issues. Some 40 percent of newly issued CCC credits have negative cash flows.[2] And yet “junk” bonds have been trading at or near record historic low yields both in absolute terms and as measured by spreads over investment-grade credits. I worry about this as a risk that has been propagated by QE3, though I do not believe it is the Fed’s job to rescue reckless investors from the errors of their ways.

The stock market bottomed in March 2009 and had already more than doubled by the time we initiated QE3. It has since risen by another 40 percent; equities have, all-in, tripled in price since the lows of 2009. Only time will tell if stocks have risen to unsustainable heights and, if so, how deep a correction might be needed to bring them back to sustainable valuations.

The Last FOMC

I believe that the Fed should, in most circumstances, not directly concern itself with fluctuations in financial-asset prices. If the economy is strong, the securities markets will be propelled by that strength. If the real economy is hearty, it can withstand reversions to the mean of junk bond or any other trading market and stock market corrections: It did so during the prolonged correction of 1962 and again in 1987. For this reason, as we approached our deliberations at last week’s FOMC, I saw no reason for the Fed to react to the heightened volatility that occurred in mid-October and strongly advised my colleagues that we should be wary of any action we might take at the FOMC that would lead investors to assume there is a “Yellen Put” hidden in our pocket. For this would only encourage continued indiscriminate investing.

I view the economy as becoming stronger. My colleagues and I at the Dallas Fed realize that the current unemployment rate, at 5.9 percent as of September, is still somewhat above most estimates of the “natural,” or minimum-sustainable, rate of unemployment. But the gap between actual and “natural” unemployment has been rapidly shrinking and is now less than 1 percentage point.

Some commentators argue that the unemployment rate hasn’t been a reliable indicator of labor-market slack during the last five years. As evidence, these commentators point to subdued wage growth. We at the Dallas Fed have investigated the links between wage inflation and the unemployment rate using the aggregate data that are available for the U.S., and also using state-level data. These investigations have led us to three main conclusions. First, wage growth responds to the unemployment rate with a lag. That’s no mystery: Many employers adjust wage and salaries just once each year. Second, wage growth becomes increasingly sensitive to the unemployment rate as the unemployment rate reaches lower and lower levels. A drop in the unemployment rate from 9 percent to 8 percent may not do much for the negotiating leverage of the typical worker. But the story is different when the unemployment rate drops from 6 percent to 5 percent or below, for example.

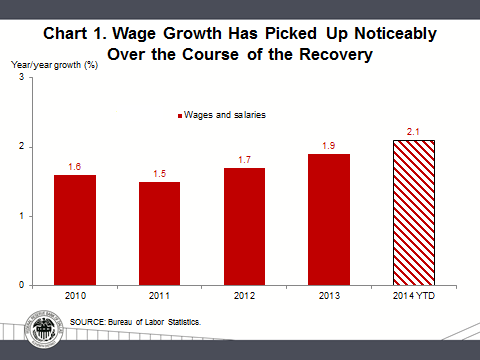

Finally, taking these two factors into account, there’s been nothing at all unusual about the behavior of wage growth over the period since the national unemployment rate peaked nearly five years ago. We went through a deep recession. Coming out of a deep recession, it takes time for the unemployment rate to reach levels where wage growth picks up noticeably. Wage growth was about 1½ percent in both 2010 and 2011—not too surprising, given that the unemployment rate was 9.9 percent in the final quarter of 2009 and, at 9.6 percent, nearly as high in the final quarter of 2010. Since then, the unemployment rate has fallen by a little less than 1 percentage point each year, and wage growth has picked up by 0.2 percentage points each year. Three quarters into 2014, wage growth is already up another two-tenths, to 2.1 percent at an annual rate.

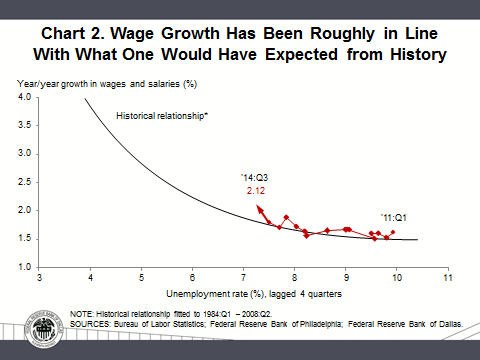

This pattern of rising wage growth is roughly what one would have expected judging by prerecession data.[3] If anything, wage growth has been running a bit above what we should have expected. This contradicts the view that the unemployment rate has understated labor-market slack.

Of course, the Federal Reserve has a target for price inflation, not wage inflation. The rate of wage inflation consistent with our 2 percent price-inflation target depends on secular trends in labor productivity growth and in labor’s bargaining power—trends over which the Federal Reserve has no control and about which it can only make informed guesses. Nevertheless, the Dallas Fed’s study of the Phillips curve has an important lesson for Fed policymakers: If we keep pushing on the accelerator pedal until wage growth matches the rate that we believe to be sustainable, we will likely have pushed too far and missed our exit. Because wage growth reacts to slack with a lag, it will continue to increase even after policy stimulus is removed. Because wage growth rises at an increasing rate the farther the unemployment rate declines, the overshoot is likely to be large.

I liken monetary policy to duck hunting. If you want to bag a mallard, you don’t aim where the bird is at present, you aim ahead of its flight pattern. To me, the flight pattern of the economy is clearly toward increasing employment and inflation that is approaching our 2-percent target.

Thus, I was encouraged by the wording we negotiated at the last FOMC meeting. I was pleased that we dropped the reference to “significant” in describing the remaining labor-market slack and that wording was included indicating we might well move to raise rates sooner than thus far assumed, should the economy proceed along the trajectory I think we are on. To me, this neutered the adjective “considerable” in stating the time frame under which we might act. This is why this particular hawk voted “yes” in support of the statement we released on Wednesday.

Now to the Exit...

Of course, I am concerned with what will happen to all the liquidity that remains in the system in the aftermath of our QE programs. The depository institutions we transact with have put back to the 12 Federal Reserve Banks some $2.7 trillion in excess reserves. “Excess” means they cannot find better uses for that money than earning the 25 basis points (25/100ths of one percent per annum) we pay them until they can find creditworthy borrowers to lend to at significant multiples of that amount. And considering that this $2.7 trillion represents perhaps as little as one-fifth of the amount of ready liquidity in the U.S. financial system—that being held not just on deposit at the Fed Banks but also by nonfinancial corporations, private equity funds, other investors and households—there is a lot of inflationary tinder available should the Fed mismanage its exit from the hyper-accommodative policy we have pursued and augmented with QE3.

Thus, only time will reveal the efficacy of the policy we have pursued and whether the risks that I and other observers (among them my mentor, Paul Volcker) fret over are as substantial, or whether we have made much ado about nothing.

My former colleague, the wonderful ex-banker and much-admired Fed Governor Betsy Duke, was quoted on Oct. 28 in The Washington Post as saying this about QE3: “It’s still important to see what the ultimate costs are going to be. You can’t really judge those until it’s completely unwound.”[4] Betsy is spot on.

Channeling Shakespeare

In June of last year, I gave a speech in Toronto in which I likened the post-zero-bound monetary policy to a Shakespearean drama with five acts, suggesting we were then in the last scene of the third act of a play titled “The Grand Experiment in Modern Monetarism.”[5] I posited we will not know until the final act whether the play will end felicitously or otherwise.

I thought I would update that analogy here today. Here is the CliffsNotes summary: The play opened with the great financial tempest of 2008–09, during which it appeared the ship of the mighty American economy would founder. A humble, once unassuming but suddenly daring captain named Ben Bernanke took firm control of the nation’s monetary helm in Act II, working with his officers—the FOMC—to contrive innovative ways to keep the economy afloat by jury-rigging monetary policy and adopting radical tactical maneuvers. These efforts succeeded in steering the ship of the economy away from the shoals of depression and deflation and into more tranquil waters.

Act III began with a recovering economy heading on a more promising course. But the headway being made was substandard, hindered by the flotsam and jetsam of fiscal incompetence and rising fears of a new storm brewing in Europe. In an effort to propel the economy forward at a better clip, the FOMC commanded that unprecedented amounts of monetary fuel be provisioned for the financial system through large-scale asset purchases, the proceeds of which were pumped into the stores of banks.

But as Act IV began, the banks lingered in the wings rather than taking center stage. Rather than shovel their abundant means into their loan boilers, they were parsimonious and hoarded their fuel. Other members of the financial fleet, however, were heartened by the turn of events, especially those who finance themselves through the issuance of stocks and bonds rather than through bank loans. They danced a happy jig while they decorated their balance sheets with cheaper debt and improved their margins and earnings per share through share buybacks. Slowly they began to hire new workers, and the ship of the economy started gathering momentum to steam along at an improved clip.

As Act IV came to an end, the FOMC evaluated the utility of its navigational tactics, and having tentatively decided that it was on course to its desired destination, began cutting back on the amount of fuel it was pumping into the financial system. Initially, it fumbled the dialogue, but eventually the articulation of its intention was accepted, if not applauded, by its audience.

Now we have entered Act V. Not until the final scene will we know whether we have achieved the auspicious outcome of arriving at the desired port of an economy that grows sufficiently to bring about full employment without giving rise to inflation. With Shakespeare, the most pleasant plays typically end in marriage. The happy outcome to our economic predicament would entail the marriage of sensible fiscal policy with prudent monetary policy, carrying the American economy to new horizons, allowing the Fed to emerge a hero.

One can envision less-pleasant outcomes, however, some of them tragic. If, even after the mid-term elections tomorrow, the fiscal authorities—Congress and the president—are unable to provide tax, spending and regulatory incentives for job creators to use the cheap and abundant capital the FOMC and other creditors have made available, the economy might once again find itself becalmed. In the speech I gave nearly four years ago to your sponsor, the Manhattan Institute, I specifically said of the then new Congress: “For all the hoopla (surrounding it), it will prove to be nothing more than a case of putting old, rancid wine in new bottles.”[6] Pray this does not happen again. Should the FOMC then try to compensate for fiscal authorities’ inability to act by provisioning still more monetary fuel, it may risk an explosion of speculative excess, or worse: an eventual inflationary conflagration, the debasement of money and the ruination of our economy and lifestyle. Should this prove the outcome, the Fed will be transmogrified from hero to villain.

To thicken the plot, as Act V began, Captain Bernanke exited stage right and a new skipper entered stage left. I should say here that I advocated for this particular skipper. Janet Yellen, when she was just another member of the crew as a Fed governor, was pigeonholed as a “dove” (forgive the double-entendre; doves are, ornithologically speaking, part of the pigeon family) but has proven herself in her role at the helm of the FOMC to be neither dove nor hawk. Rather, she is impressively balanced and fully aware, at least in my opinion, that her legacy will be whether she can successfully complete Act V by realizing the Fed’s mandate to maintain price stability while providing the monetary means to achieve full employment.

All of which means that despite the mighty efforts of Captains Bernanke and Yellen and their officers and crew, present company included, we do not know how “The Grand Experiment” drama will end. We certainly all hope it proves an inspiring history, not a tragedy. But, we will not know for some time. We will not know until the curtain drops on Act V.

R.I.P?

Betsy Duke had it right: Only when we have normalized monetary policy—only when the play is done—will we know if QE3 rests in peace or comes back to haunt us. Only when it is done will we know if “The Grand Experiment in Modern Monetarism” is a smash hit or a bomb or something in between.

As Yogi Berra said and Lenny Kravitz sang: “It ain’t over till it’s over.” But one thing I know for sure: This speech is over. Thank you for listening.

And now, Mickey, time and patience permitting, I would be happy to avoid answering any questions you and your colleagues might have.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- “A Conversation: The Fed Yesterday, Today and Tomorrow,” a discussion with Federal Reserve Chairman Ben Bernanke on the Fed’s 100th anniversary, Brookings Institution, Washington, D.C., Jan. 16, 2014.

- See “The Next Default Wave: Slow and Low,” in The HY Wire, Bank of America Merrill Lynch, Sept. 24, 2014.

- The following charts illustrate the recent acceleration in wage growth (Chart 1) and the relationship between rising wage growth and falling unemployment (Chart 2). For more information, see the Dallas Fed Economic Letter titled“Are We There Yet? Assessing Progress Toward Full Employment and Price Stability,” available at www.dallasfed.org/assets/documents/research/eclett/2014/el1413.pdf.

- See “The Federal Reserve’s Experiment in Quantitative Easing Is Coming to an End,” by Ylan Q. Mui, The Washington Post, WonkBlog, Oct. 28, 2014.

- If you wish to read that speech in its entirety, it can be found at www.dallasfed.org/news/speeches/fisher/2013/fs130604.cfm.

- See “The Limits of Monetary Policy: ‘Monetary Policy Responsibility Cannot Substitute for Government Irresponsibility’,” remarks by Richard W. Fisher, Jan. 12, 2011.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.