Janet Yellen Is No Mae West!

March 9, 2015 Houston Speech in PDF

Thank you, Mr. Ambassador (Ed Djerejian), for hosting me this evening. I am honored to have been chosen to give my last speech as a Federal Reserve official to the Baker Institute’s Founding Director’s Lecture Series.

Jim Baker is, himself, an institution; I admire him greatly. Few individuals in the history of this country—I think the only others may be George Shultz and the late Elliot Richardson—have held as many cabinet posts as Jim. And few are as loyal a friend.

Jim and I were cabin mates on an elk hunting trip on the high plains of Utah last fall. As you may know, he is a crack shot and a skilled hunter. We spent the first few hours after arrival at our campsite practicing at the range. While I missed every single shot, Jim effortlessly placed every one of his squarely in the bull’s-eye, at every distance. And yet the next day, within an hour of our setting out in a light snow and bitter cold, on my very first shot, I dropped a big bull that had long evaded his ultimate fate. That bull’s nickname was Hugh Hefner—he was old and always had a dozen or so cows with him. Hugh Hefner the elk had an impressive, wide-spread six by six point rack; he was a true trophy. I was proud of my little accomplishment and told Jim about it immediately and repeatedly through the day.

The next two days, Jim returned without firing a single shot. He said he “just couldn’t find anything worth shooting.” But I suspect that he held himself back simply to allow me to have my bragging rights for the trip. That’s the kind of gentleman Jim Baker is. (Though I feel compelled to tell you he did not hold himself back in loudly winning the snoring contest we had in our cabin: In addition to all his accomplishments, including his kindness to neophyte hunters like me, Jim Baker should be on the list of the world’s great snorers!)

It Ain’t Brag if It’s True

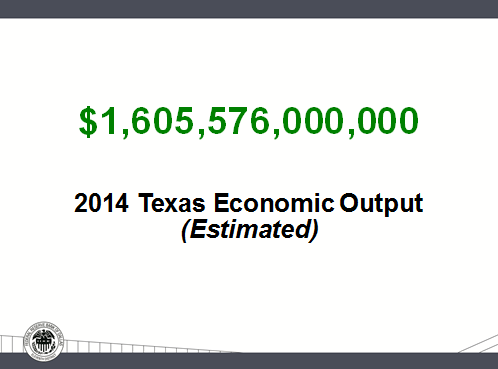

On the bragging rights front, I have thoroughly enjoyed using my perch at the Fed to spread the story of Texas’ economic success. Last Friday, I shared some statistics about our state with an audience in Dallas.[1] Like this one: 1,605,576,000,000. Do you know what that represents? No, it is not the number of “likes” or followers that Houston native Beyoncé has on social media, although that number might be up there. If you place a dollar sign before it, $1,605,576,000,000 is the estimated gross state product of Texas for 2014. One trillion, six hundred and five billion, five hundred and seventy-six million dollars. That is the amount of output Houstonians and their fellow Texans produced last year—roughly equivalent to the output of Canada, our great neighbor to the north.

There has been strong momentum building up to that number. Just since I came to the Dallas Fed in 2005, my staff estimates that the real Texas economy has grown by $382 billion, or 36 percent. That increment equates to adding more than the entire output of Norway, my mother’s homeland and now one of the world’s richest nations measured on a per capita basis.

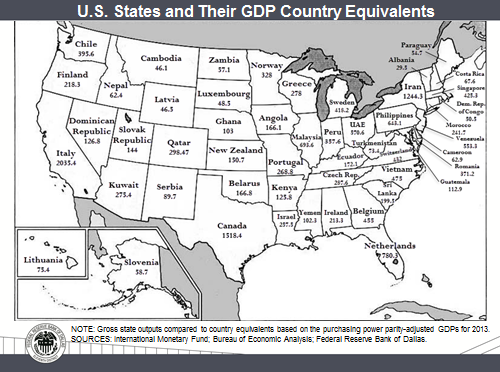

To put Texas in global perspective, my staff put together this tongue-in-cheek map of the United States that compares the output of each state of the union with an international counterpart.

I am not sure my friends in Rhode Island—whose wonderful Bryant University awarded me an honorary doctorate last June—will much appreciate their output being compared to that of the Democratic Republic of the Congo. Or that another cabinet member named Richardson—Bill Richardson, who went on to become governor of New Mexico—will like seeing that New Mexico produces the economic equivalent of Serbia. Or that my colleagues in New York will cotton to having the same output level as Iran. But there you are: Texas is the second-largest economic engine in the country, behind only California. But I rather like pointing out that California can be compared to Italy, for unless it corrects its course of over-taxation and regulation, it will surely end up with an economy very much like that of the Repubblica Italiana.

U.S. Economic Landscape

Now enough of the Texas braggadocio, even though it happens to be true. This is my final speech at the Fed and I want to address some of the more pressing issues facing my counterparts on the Federal Open Market Committee (FOMC) in the months ahead.

First, it helps to put the size of the U.S. economy in perspective. In 2014, the U.S. produced $17.4 trillion in goods and services. Just since I arrived at the Dallas Fed 10 years ago, the U.S. has increased its total level of real output approximately $2.2 trillion. In sum, the U.S. is a huge, muscular economy.

What is the muscle tone of our economy? Where are we presently in terms of growth and from the perspective of the Federal Reserve’s dual mandate of maintaining price stability and providing the monetary conditions to underwrite full employment?

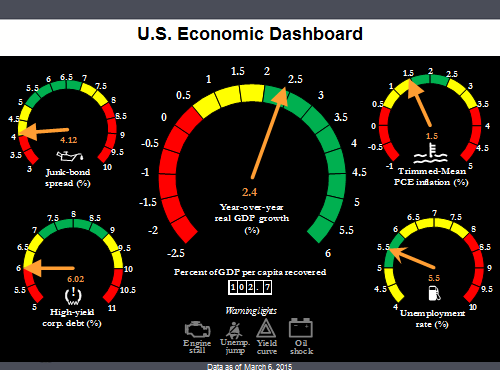

Here is a simple “dashboard” we use at the Dallas Fed to encapsulate the economy’s current condition:

The bottom line: At present, inflation is contained, unemployment is declining and approaching the level most economists feel is sustainable without creating inflationary pressures, and the overall economy is steaming along at a growth rate of 2.4 percent.

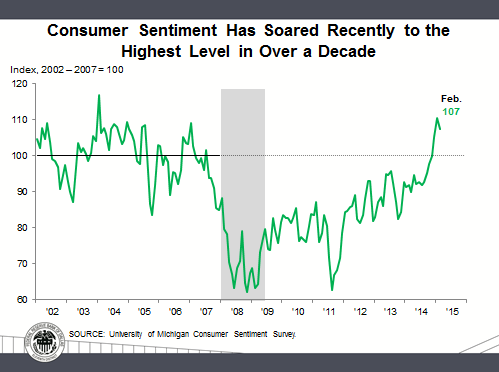

Importantly, our fellow citizens are once again feeling more confident about the economy. In an economy propelled by household and business spending, it is helpful to get a grasp of the feelings of the average American consumer. The University of Michigan Consumer Sentiment Survey does just that, and right now it is telling us that consumers feel better than they did on average from 2002 to 2007. It had been a long time since hope sprang eternal, but 2014 was a huge year for rebuilding consumer confidence.

Enter Prince: ‘Gonna Party Like It’s 1999’?

Despite increased consumer sentiment,

the U.S. experienced very uneven gross domestic product (GDP) growth during 2014. This was partly a result of severe winter weather and partly a result of the Affordable Care Act rollout, which disrupted the pattern of household health care expenditures. For the year as a whole, growth looks to have averaged out to around 2½ percent. That may not sound like much at first blush, but it was enough to give us a 1.1 percentage-point drop in the unemployment rate and the largest job gains since 1999.[2] You might not have expected that at the beginning of the year if you had listened to the gloom-and-doomers. The musician Prince (or should I call him by one of his other names: “the artist formerly known as Prince,” Joey Coco, Alexander Nevermind or that ![]() symbol?) must have foreseen this when he sang “gonna party like it’s 1999.”

symbol?) must have foreseen this when he sang “gonna party like it’s 1999.”

So, are we going to rock on? Should we look for more of the same in 2015? Or should we be reminded of another lyric from Prince: “… parties weren’t meant to last”? Again, we need to put things in perspective.

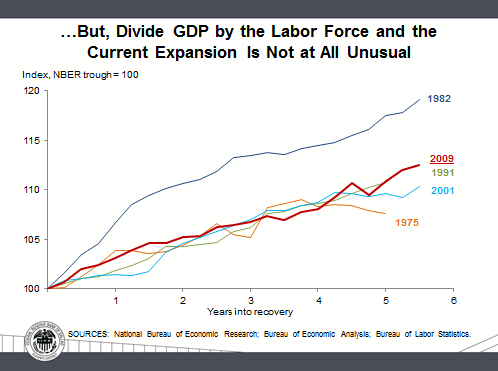

The Wall Street Journal recently published an article that included a chart comparing the level of real GDP in the current expansion with that of four prior expansions. In that chart, the current expansion finished dead last, with output well behind what one might have expected based on the economy’s performance during the late 1970s and the 1980s, 1990s and 2000s.

This picture changes markedly, though, if you divide GDP by the available labor force. Then the current expansion is tied with that of the 1990s and edges out those of the 1970s and 2000s. Really, all four of those expansions lie almost on top of one another, as the following chart shows. Only the recovery from the 1981–82 recession stands out. The implication is that the weak GDP growth we’ve seen during the current expansion is entirely explained by weak labor force growth.

So why has labor force growth been weak? Demographics have played a big role. Population growth has slowed from 2¼ percent per year in the mid-1970s to 1 percent per year today, and more and more baby boomers—old codgers like me and Ambassador Djerejian—are pushing retirement age. The combined effect of these trends is that growth in the working-age (16 to 64) population has slowed to just 0.5 percent per year.[3] In addition, a higher proportion of young people are attending college than in the past, and the huge flow of women from the home to the workplace has largely run its course.[4] The recession of 2008–09 undoubtedly pushed many people into premature retirement. It’s doubtful, though, whether enough of them can be brought back into the job market at this point to move the participation rate appreciably higher.

In sum, labor force growth has been anemic because of slow growth in the working-age population and because, for reasons that have nothing to do with monetary policy, the labor force participation rate for those of working age has stopped rising and started trending downward. Labor force growth is likely to remain anemic over at least the next couple of years. With the working-age population growing at only 0.5 percent per year, the dividing line between a rising and a falling unemployment rate is less than 100,000 jobs per month for any realistic assumption about labor force participation.

The point is that economic growth at the pace we saw in 2014 will very quickly drive us to and past the 5 to 5.5 percent unemployment range regarded as sustainable by most policymakers and private analysts. A repeat of 2014’s performance would put us around 4.5 percent unemployment by year-end.

The sustainable—or in Fedspeak, the “natural” rate of unemployment—varies over time with changes in educational attainment and the demographic composition of the labor force. At any point in time, estimates are subject to considerable uncertainty. We have to be constantly alert to the possibility that current estimates are mistaken. Still, given the dangers associated with overshooting full employment, I believe it behooves monetary policymakers to be cautious. With all the benefits of hindsight, the Congressional Budget Office estimates that the natural rate of unemployment has averaged 5.6 percent and has never fallen below 5 percent in the United States going all the way back to 1948.

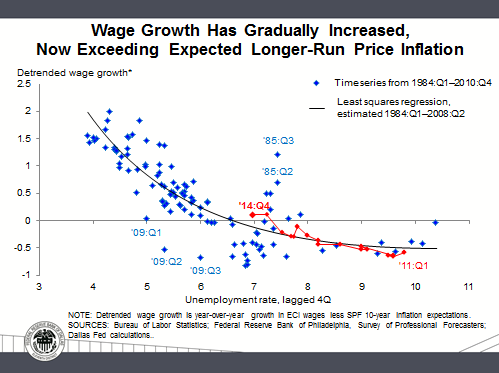

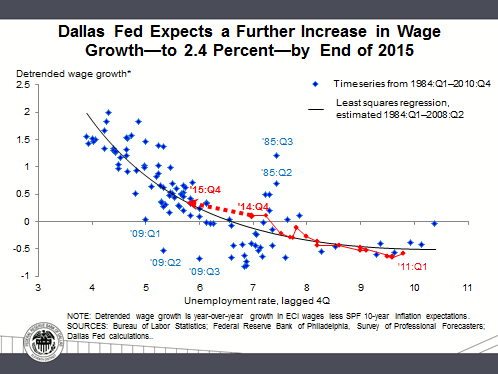

Some commentators point to subdued wage growth as evidence that substantial labor market slack remains. Taking policy cues from present wage growth, though, would move us into dangerous territory indeed. Slack responds to monetary policy with a lag, and wage growth responds with a lag to slack, so current wage growth is a very backward-looking measure of policy’s stance. Moreover, research conducted at the Dallas Fed has demonstrated that wage growth’s response to labor market slack is highly nonlinear: The response gets stronger and stronger as slack diminishes.[5] The gradual increase in wage growth that we’ve seen to date is entirely consistent with historical experience once lags and nonlinearity are taken into account. The red lines in these two graphs will show you how we tracked from the beginning of 2011 to the end of 2014 in terms of wage growth detrended by inflation expectations (the vertical axis) relative to the declining unemployment rate (the horizontal axis), and then where we at the Dallas Fed expect to be at the end of 2015.

Liftoff!

Some highly respected observers would have the Fed wait until we “see the whites of full-employment’s eyes” before it starts raising interest rates or shrinking its $2.5 trillion bond portfolio. Would pushing past full employment really be so bad? So what if inflation rises, temporarily, above target? Can’t we do an after-the-fact course correction if it should turn out that policy has been too accommodative?

There’s certainly something to the argument that it’s okay to go off your diet from time to time, especially if your weight has been running below target. But you can’t consistently binge without getting into trouble. Sooner or later, you have to bring your caloric intake back to normal, lest your weight and your waistline balloon and your health deteriorate. In the monetary policy sphere, unfortunately, cutting back has proven to be even more difficult than it is in personal weight control. In the real world, one never sees the smooth, moderately sized unemployment increases that our simple mathematical models so readily generate. A recessionary dynamic kicks in whenever the unemployment rate rises by more than a few tenths of a percentage point. The problem with overshooting full employment to any significant degree is that it has always set the stage for a new recession. Gaining weight (reducing the unemployment rate) is easy. Attempts to lose weight (to stem overheating of the economy) seem always to get out of control and land us in the hospital. Every time the Fed has tightened policy after achieving full employment, it has driven the economy into recession.

It’s because of this dynamic, and my desire to prolong the current expansion, that I have argued that we should begin reducing policy accommodation earlier than many of my colleagues on the FOMC appear to prefer.

There’s every indication that solid, above-potential growth in employment and output is going to continue through the summer of 2015. The unemployment rate is likely to reach the bottom of the range of natural-rate estimates within that time frame. So if we are serious about limiting full-employment overshoot, I posit that prompt action to scale back policy accommodation is likely to prove imperative. The idea that we can substitute a steeper future funds-rate path for an early liftoff seems risky to me. I would rather the FOMC raise rates early and gradually than late and steeply.

The credibility of a “later and steep” policy strategy is suspect, it seems to me. Isn’t it possible—even likely—that the public will interpret a decision to defer liftoff as a signal that the committee is generally “dovish” and generally disinclined to raise rates? In other words, mightn’t the public see the choice as between “earlier and gradual” and “later and gradual” rather than between “earlier and gradual” and “later and steep”?

I have felt that were we to begin liftoff—I have been eager to use this term in this town for some time, especially with Ellen Ochoa, the director of Johnson Space Center and the chair of the Houston Branch board of directors sitting right here in front of me!—earlier in 2015, markets would have more confidence about the “gradual” in “earlier and gradual.” Otherwise, as some of my colleagues have stated publicly, if we were to defer liftoff until, say, December 2015 but plan to raise rates quickly thereafter, people have to wait until January 2016 to determine whether the FOMC is serious. Early and gradual is quickly verified. Later and steep requires a high level of trust. It is certainly no stretch to think that the public might not completely buy into the “steep” in “later and steep.”

And what about the incentive to renege? January 2016 arrives. Suppose that the public has, in fact, not bought into the FOMC’s promises of a steeper funds rate path. What if the Fed’s surveys of market operators and dealers reveal that financial bets and commitments have been made such that a move to raise rates appears likely to incite financial market turbulence? Might future policymakers then be strongly tempted to back down?

Inflation Outlook

In the aviary of central bankers, I am known as a “hawk,” even though I have not spoken of the threat of immediate inflation since 2008, when we had an inflationary scare before having the legs pulled out from the table of the economy with the implosion of Lehman Brothers and the financial superstructure. You may wonder how I view the minimal inflation, or even deflationary pressure, some commentators seem to be worrying about.

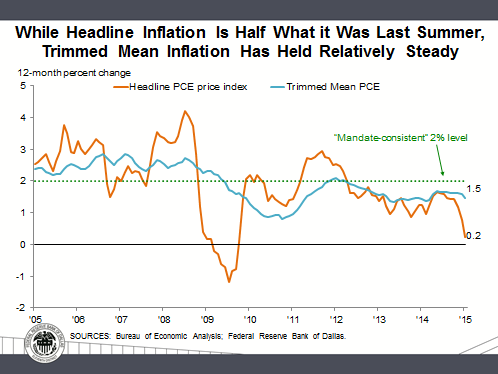

The FOMC is trying its level best to understand the dynamics of inflation. We have declared a 2 percent intermediate target for inflation, which seems to be standard for most central banks. Headline inflation measures show a significant shortfall from that target. The headline personal consumption expenditures (PCE) price index fell 0.5 percent in January. Its 12-month increase was just 0.2 percent, down from 1.6 percent in June. Should this low, and still falling, rate of price inflation retard the date of the liftoff from the zero-interest-rate policy we have been operating for more than six years?

I think not. Especially here in Houston, folks know that headline inflation is being held down by the big decline in energy prices that began in the second half of 2014. But we should also know that once energy prices stabilize, headline inflation is likely to bounce right back up. Policy needs to take past inflation into account, but it needs to take future inflation into account, too. For policy purposes, it is inflation’s medium-term trend that matters. That’s why, in evaluating progress toward our price-stability objective, I pay close to zero attention to realized headline inflation. I pay nearly as little attention to conventional core inflation, which excludes food and energy prices. I prefer the Dallas Fed’s Trimmed Mean PCE core inflation measure, which each month excludes the most extreme upward and downward price movements, regardless of their source. Here’s a graph of the current trend of both headline and Trimmed Mean PCE inflation:

A good core inflation measure strips the noise out of headline inflation and leaves the signal. The trimmed mean inflation rate has, so far, held pretty steady in the face of the drop in energy prices and the appreciation of the dollar. It would not surprise me to see some decline in the trimmed mean run rate, as we did last month, in the near term; but I think that the decline will likely be temporary. The inflation trend should reverse later this year, assuming that energy prices don’t fall further and that the dollar stabilizes.

If you go to the Dallas Fed website, you will see our most recent posting: The 12-month trimmed mean rate slipped slightly to 1.5 percent, just below the range of 1.6 to 1.7 percent it’s occupied every month since April 2014.[6] While 1.5 percent is lower than the FOMC is shooting for, it’s a whole lot less discouraging than a headline inflation reading of almost nil. At the end of the year, trimmed mean inflation is more likely to be above its current 1.5 percent rate than below.

Janet Yellen Is No Mae West!

That’s probably about all the interpreted Fedspeak you can handle in an evening, so perhaps I can leave you with a few simple takeaways. The U.S. economy is improving. We are approaching any sensible measure of full employment. And even though the numeric inflation target for the intermediate term has not been reached, we have reasonable price dynamics that are unlikely to threaten further economic growth and continued job creation as long as the FOMC doesn’t flinch from beginning to normalize policy on a timely basis.

We will see. In a recent speech to the Economic Club of New York, I quoted Mae West: “I generally avoid temptation,” she said, “unless I can’t resist it.”

I think I am safe in saying that Janet Yellen is no Mae West. I leave the Fed with the high expectation that she will ably lead the FOMC down the path of normalizing monetary policy and resist any temptation to delay for too long that path-changing task.

Ed, thank you for letting me speak here tonight. I thank the people of Houston and all of Texas for allowing me the privilege of serving for a decade as president and CEO of the Eleventh District’s Federal Reserve Bank. The past 10 years have been challenging but immensely rewarding. Indeed, in my farewell letter to my staff, I suggested that given the crisis we went through, the life of a Fed president should be measured in dog years. So I thank you all for letting me lead your Federal Reserve Bank for the past 70 years.

Goodnight, God bless you, and God bless Texas.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- See “Homage to Texas, the Great People of Dallas and the Staff of the Dallas Fed,” speech by Richard W. Fisher, March 6, 2015, www.dallasfed.org/news/speeches/fisher/2015/fs150306.cfm

- Nonfarm employment rose 2.27 percent in 2014, the highest December-over-December growth rate since 1999’s 2.49 percent.

- Of note, the 0.5 percent growth rate for the working-age population, defined here as those ages 16 to 64, isn’t very sensitive to changing the age limits. The working population age 20 to 64, for example, has also been growing at 0.5 percent per year, while the working population age 16 to 69 has been increasing at about 0.6 percent per year.

- The labor force participation rate of those age 16 to 19 has dropped from over 58 percent in the late 1970s to just 34 percent today, and the gap between the age 20-plus men’s and women’s labor force participation rates has shrunk from 57 percentage points in 1948 to 13 percentage points today. The most rapid shrinkage—more than 1.3 percentage points per year—occurred in the 1970s. Over the past five years, in contrast, the male–female participation gap has shrunk only 0.1 percentage points per year.

- See “Are We There Yet? Assessing Progress Toward Full Employment and Price Stability,” by Richard W. Fisher and Evan Koenig, Federal Reserve Bank of Dallas Economic Letter, vol. 9, no. 13, 2014, www.dallasfed.org/media/Documents/research/eclett/2014/el1413.pdf.

- See www.dallasfed.org/research/pce/ for monthly updates by Jim Dolmas, senior research economist and advisor at the Dallas Fed.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.