Ending 'Too Big to Fail': A Proposal for Reform Before It's Too Late (With Reference to Patrick Henry, Complexity and Reality)

January 16, 2013 Washington, D.C.

It is an honor to be introduced by my college classmate, John Henry. John is a descendant of the iconic patriot, Patrick Henry. Most of John’s ancestors were prominent colonial Virginians and many were anti-crown. Patrick, however, was the most outspoken. Ask John why this was so, and he will answer: “Patrick was poor.”

However poor he may have been, Patrick Henry was a rich orator. In one of his greatest speeches, he said: “Different men often see the same subject in different lights; and therefore, I hope that it will not be thought disrespectful to those gentlemen if, entertaining as I do, opinions of a character very opposite to theirs, I shall speak forth my sentiments freely, and without reserve. This is no time for ceremony … [it] is one of awful moment to this country.”

Patrick Henry was addressing the repression of the American colonies by the British crown. Tonight, I wish to speak to a different kind of repression—the injustice of being held hostage to large financial institutions considered “too big to fail,” or TBTF for short.

I submit that these institutions, as a result of their privileged status, exact an unfair tax upon the American people. Moreover, they interfere with the transmission of monetary policy and inhibit the advancement of our nation’s economic prosperity.

I have spoken of this for several years, beginning with a speech on the “Pathology of Too-Big-to-Fail” in July 2009.[1] My colleague, Harvey Rosenblum—a highly respected economist and the Dallas Fed’s director of research—and I and our staff have written about it extensively. Tomorrow, we will issue a special report that further elucidates our proposal for dealing with the pathology of TBTF. It also addresses the superior relative performance of community banks during the recent crisis and how they are being victimized by excessive regulation that stems from responses to the sins of their behemoth counterparts. I urge all of you to read that report.[2]

Now, Federal Reserve convention requires that I issue a disclaimer here: I speak only for the Federal Reserve Bank of Dallas, not for others associated with our central bank. That is usually abundantly clear. In many matters, my staff and I entertain opinions that are very different from those of many of our esteemed colleagues elsewhere in the Federal Reserve System. Today, I “speak forth my sentiments freely and without reserve” on the issue of TBTF, while meaning no disrespect to others who may hold different views.

The Problem of TBTF

Everyone and their sister knows that financial institutions deemed too big to fail were at the epicenter of the 2007–09 financial crisis. Previously thought of as islands of safety in a sea of risk, they became the enablers of a financial tsunami. Now that the storm has subsided, we submit that they are a key reason accommodative monetary policy and government policies have failed to adequately affect the economic recovery. Harvey Rosenblum and I first wrote about this in an article published in the Wall Street Journal in September 2009, “The Blob That Ate Monetary Policy.”[3] Put simply, sick banks don’t lend. Sick—seriously undercapitalized—megabanks stopped their lending and capital market activities during the crisis and economic recovery. They brought economic growth to a standstill and spread their sickness to the rest of the banking system.

Congress thought it would address the issue of TBTF through the Dodd–Frank Wall Street Reform and Consumer Protection Act. Preventing TBTF from ever occurring again is in the very preamble of the act. We contend that Dodd–Frank has not done enough to corral TBTF banks and that, on balance, the act has made things worse, not better. We submit that, in the short run, parts of Dodd–Frank have exacerbated weak economic growth by increasing regulatory uncertainty in key sectors of the U.S. economy. It has clearly benefited many lawyers and created new layers of bureaucracy. Despite its good intention, it has been counterproductive, working against solving the core problem it seeks to address.

Defining TBTF

Let me define what we mean when we speak of TBTF. The Dallas Fed’s definition is financial firms whose owners, managers and customers believe themselves to be exempt from the processes of bankruptcy and creative destruction. Such firms capture the financial upside of their actions but largely avoid payment—bankruptcy and closure—for actions gone wrong, in violation of one of the basic tenets of market capitalism (at least as it is supposed to be practiced in the United States). Such firms enjoy subsidies relative to their non-TBTF competitors. They are thus more likely to take greater risks in search of profits, protected by the presumption that bankruptcy is a highly unlikely outcome.

The phenomenon of TBTF is the result of an implicit but widely taken-for-granted government-sanctioned policy of coming to the aid of the owners, managers and creditors of a financial institution deemed to be so large, interconnected and/or complex that its failure could substantially damage the financial system. By reducing a TBTF firm’s exposure to losses from excessive risk taking, such policies undermine the discipline that market forces normally assert on management decisionmaking.

The reduction of market discipline has been further eroded by implicit extensions of the federal safety net beyond commercial banks to their nonbank affiliates. Moreover, industry consolidation, fostered by subsidized growth (and during the crisis, encouraged by the federal government in the acquisitions of Merrill Lynch, Bear Stearns, Washington Mutual and Wachovia), has perpetuated and enlarged the weight of financial firms deemed TBTF. This reduces competition in lending.

Dodd–Frank does not do enough to constrain the behemoth banks’ advantages. Indeed, given its complexity, it unwittingly exacerbates them.

Complexity Bites

Andrew Haldane, the highly respected member of the Financial Policy Committee of the Bank of England, addressed this at last summer’s Jackson Hole, Wyo., policymakers’ meeting in witty remarks titled, “The Dog and the Frisbee.”[4] Here are some choice passages from that noteworthy speech.

Haldane notes that regulators’ “… efforts to catch the crisis Frisbee have continued to escalate. Casual empiricism reveals an ever-growing number of regulators … Ever-larger litters have not, however, obviously improved the watchdogs’ Frisbee-catching abilities. [After all,] no regulator had the foresight to predict the financial crisis, although some have since exhibited supernatural powers of hindsight.

“So what is the secret of the watchdogs’ failure? The answer is simple. Or rather, it is complexity … complex regulation … might not just be costly and cumbersome but sub-optimal. … In financial regulation, less may be more.”

One is reminded of the comment French Prime Minister Clemenceau made about President Wilson’s 14 points: “Why 14?” he asked. “God did it in 10.”

Were that we only had 14 points of financial regulation to contend with today. Haldane notes that Dodd–Frank comes against a background of ever-greater escalation of financial regulation. He points out that nationally chartered banks began to file the antecedents of “call reports” after the formation of the Office of the Comptroller of the Currency in 1863. The Federal Reserve Act of 1913 required state-chartered member banks to do the same, having them submitted to the Federal Reserve starting in 1917. They were short forms; in 1930, Haldane noted, these reports numbered 80 entries. “In 1986, [the ‘call reports’ submitted by bank holding companies] covered 547 columns in Excel, by 1999, 1,208 columns. By 2011 … 2,271 columns.” “Fortunately,” he adds wryly, “Excel had expanded sufficiently to capture the increase.”

Though this growingly complex reporting failed to prevent detection of the seeds of the debacle of 2007–09, Dodd–Frank has layered on copious amounts of new complexity. The legislation has 16 titles and runs 848 pages. It spawns litter upon litter of regulations: More than 8,800 pages of regulations have already been proposed, and the process is not yet done. In his speech, Haldane noted—conservatively, in my view—that a survey of the Federal Register showed that complying with these new rules would require 2,260,631 labor hours each year. He added: “Of course, the costs of this regulatory edifice would be considered small if they delivered even modest improvements to regulators’ ability to avert future crises.” He then goes on to argue the wick is not worth the candle. And he concludes: “Modern finance is complex, perhaps too complex. Regulation of modern finance is complex, almost certainly too complex. That configuration spells trouble. As you do not fight fire with fire, you do not fight complexity with complexity. [The situation] requires a regulatory response grounded in simplicity, not complexity. Delivering that would require an about-turn.”

The Dallas Fed’s Proposal: A Reasonable ‘About-Turn’

The Dallas Fed’s proposal offers an “about-turn” and a way to mend the flaws in Dodd–Frank. It fights unnecessary complexity with simplicity where appropriate. It eliminates much of the mumbo-jumbo, ineffective, costly complexity of Dodd–Frank. Of note, it would be especially helpful to non-TBTF banks that do not pose systemic or broad risk to the economy or the financial system. Our proposal would relieve small banks of some unnecessary burdens arising from Dodd–Frank that unfairly penalize them. Our proposal would effectively level the playing field for all banking organizations in the country and provide the best protection for taxpaying citizens.

In a nutshell, we recommend that TBTF financial institutions be restructured into multiple business entities. Only the resulting downsized commercial banking operations—and not shadow banking affiliates or the parent company—would benefit from the safety net of federal deposit insurance and access to the Federal Reserve’s discount window.

Defining the Landscape

It is important to have an accurate view of the landscape of banking today in order to understand the impact of this proposal.

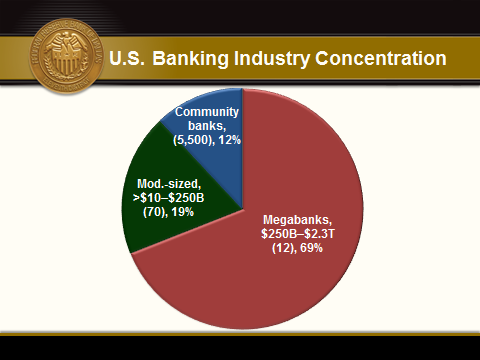

As of third quarter 2012, there were approximately 5,600 commercial banking organizations in the U.S. The bulk of these—roughly 5,500—were community banks with assets of less than $10 billion. These community-focused organizations accounted for 98.6 percent of all banks but only 12 percent of total industry assets. Another group numbering nearly 70 banking organizations—with assets of between $10 billion and $250 billion—accounted for 1.2 percent of banks, while controlling 19 percent of industry assets. The remaining group, the megabanks—with assets of between $250 billion and $2.3 trillion—was made up of a mere 12 institutions. These dozen behemoths accounted for roughly 0.2 percent of all banks, but they held 69 percent of industry assets.

SOURCES: Call reports (Federal Financial Institutions Examination Council); FR Y-9C filers (National Information Center, Federal Reserve System).

The 12 institutions that presently account for 69 percent of total industry assets are candidates to be considered TBTF because of the threat they could pose to the financial system and the economy should one or more of them get into trouble. By contrast, should any of the other 99.8 percent of banking institutions get into trouble, the matter most likely would be settled with private-sector ownership changes and minimal governmental intervention.

How and why does this work for 99.8 percent but not the other 0.2 percent?

To answer this question, it helps to consider the sources of regulatory and market discipline imposed on each of the three groups of banks.

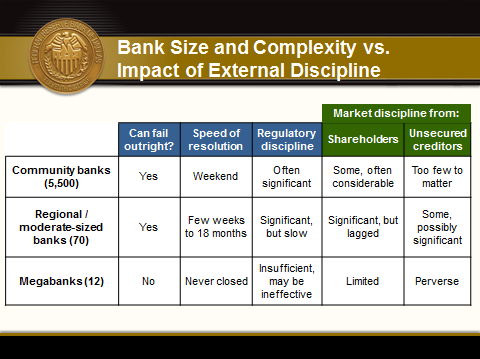

Let’s look at two dimensions of regulatory discipline: Potential closure of the institution and the effectiveness of supervisory pressure on bank management practices.

Do the owners and managers of a banking institution operate with the belief that their institution is subject to a bankruptcy process that works reasonably quickly to transfer ownership and control to another banking entity or entities? Is there a group of interested and involved shareholders that can exert a restraining force on franchise-threatening risk taking by the bank’s top management team? Can management be replaced and ownership value wiped out? Is the firm controlled de facto by its owners, or instead effectively management-controlled?[5] In addition, we ask: To what extent do uninsured creditors of the banking entity impose risk-management discipline on management?

This analytical framework is summarized in the following slide:

SOURCE: Federal Reserve Bank of Dallas.

Looking across line 1, it is clear that community banks are subject to considerable regulatory and shareholder discipline. They can and do fail. In the last few years, the Federal Deposit Insurance Corp. (FDIC) has built a reputation for regulators carrying out Joseph Schumpeter’s concept of “creative destruction” by taking over small banks on a Friday evening and reopening them on Monday morning under new ownership. “In on Friday, out by Monday” is the mantra of this process.

Knowing the power of banking supervisors to close the institution, owners and managers of community banks heed supervisory suggestions to limit risk. Community banks often have a few significant shareholders who have a considerable portion of their wealth tied to the fate of the bank. Consequently, they exert substantial control over the behavior of management because risk and potential closure matter to them. Since community banks derive the bulk of their funding from federally insured deposits, they are simple rather than complex in their capital structure and rarely have uninsured and unsecured creditors. “Market discipline” over management practices is primarily exerted through shareholders.

Of the three groups, the 70 regional and moderate-sized banking organizations depicted in line 2 are subject to a broader range of market discipline. Like community banks, these institutions are not exempt from the bankruptcy process; they can and do fail. But given their size, complexity and generally larger geographic footprint, the failure resolution and ownership transfer processes cannot always be accomplished over a weekend. In practice, owners and managers of mid-sized institutions are nonetheless aware of the downside consequences of the risks taken by the institution. Uninsured depositors and unsecured creditors are also aware of their unprotected status in the event the institution experiences financial difficulties. Mid-sized banking institutions receive a good dose of external discipline from both supervisors and market-based signals.

TBTF megabanks, depicted in line 3, receive far too little regulatory and market discipline. This is unfortunate because their failure, if it were allowed, could disrupt financial markets and the economy. For all intents and purposes, we believe that TBTF banks have not been allowed to fail outright.[6] Knowing this, the management of TBTF banks can, to a large extent, choose to resist the advice and guidance of their bank supervisors’ efforts to impose regulatory discipline. And for TBTF banks, the forces of market discipline from shareholders and unsecured creditors are limited.

Let’s first consider discipline from shareholders. Having millions of stockholders has diluted shareholders’ ability to prevent the management of TBTF banks from pursuing corporate strategies that are profitable for management, though not necessarily for shareholders.

As we learned during the crisis, adverse information on poor financial performance often is available too late for shareholder reaction or credit default swap (CDS) spreads to have any impact on management behavior. For example, during the financial crisis, shares in two of the largest bank holding companies (BHCs) declined more than 95 percent from their prior peak prices and their CDS spreads went haywire.[7] The ratings agencies eventually reacted, in keeping with their tendency to be reactive rather than proactive. But the damage from excessive risk taking had already been done. And after the crisis? Judging from the behavior of many of the largest BHCs, with limited exception, efforts by shareholders of these institutions to meaningfully influence management compensation practices have been slow in coming. So much for shareholder discipline as a check on TBTF banks.

Unfortunately, TBTF banks also do not face much external discipline from unsecured creditors. An important facet of TBTF is that the funding sources for megabanks extend far beyond insured deposits, as referenced by my mention of CDS spreads. The largest banks, not just the TBTF banks, fund themselves with a wide range of liabilities. These include large, negotiable CDs, which often exceed the FDIC insurance limit; federal funds purchased from other banks, all of which are uninsured, and subordinated notes and bonds, generally unsecured. It is not unusual for such uninsured/unsecured liabilities to account for well over half the liabilities of TBTF institutions. If market discipline were to be imposed on TBTF institutions, one would expect it to come from uninsured/unsecured depositors, creditors and debt holders. But TBTF status exerts perverse market discipline on the risk-taking activities of these banks. Unsecured creditors recognize the implicit government guarantee of TBTF banks’ liabilities. As a result, unsecured depositors and creditors offer their funds at a lower cost to TBTF banks than to mid-sized and regional banks that face the risk of failure.

This TBTF subsidy is quite large and has risen following the financial crisis. Recent estimates by the Bank for International Settlements, for example, suggest that the implicit government guarantee provides the largest U.S. BHCs with an average credit rating uplift of more than two notches, thereby lowering average funding costs a full percentage point relative to their smaller competitors.[8] Our aforementioned friend from the Bank of England, Andrew Haldane, estimates the current implicit TBTF global subsidy to be roughly $300 billion per year for the 29 global institutions identified by the Financial Stability Board (2011) as “systemically important.”[9] To put that $300 billion estimated annual subsidy in perspective, all the U.S. BHCs summed together reported 2011 earnings of $108 billion.

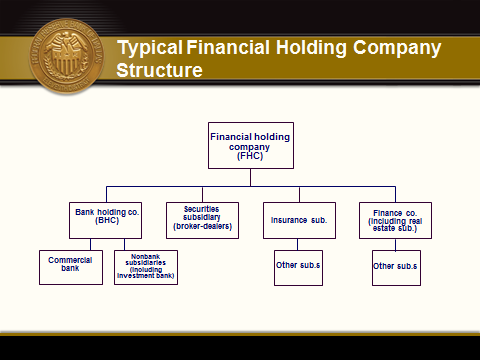

Add to that the burdens stemming from the complexity of TBTF banks. Here is the basic organization diagram for a typical complex financial holding company:

SOURCE: Federal Reserve Bank of Dallas.

To simplify a complex issue, one might consider all the operations other than the commercial banking operation as shadow banking affiliates, including any special investment vehicles—or SIVs—of the commercial bank [10].

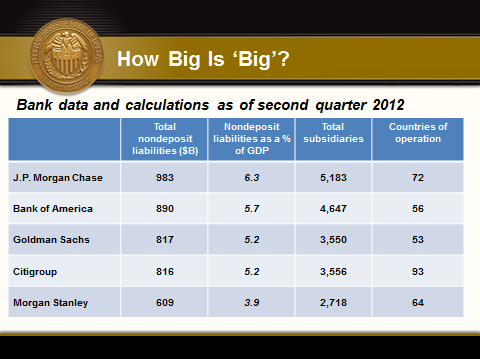

Now, consider this table. It gives you a sense of the size and scope of some of the five largest BHCs, noting their nondeposit liabilities in billions of dollars and their number of total subsidiaries and countries of operation (according to the Financial Stability Oversight Council):

SOURCES: "Which Banks Could Face Cap on Size?" by Victoria McGrane, Wall Street Journal, Oct. 11, 2012; Financial Stability Oversight Council.

For perspective, consider the sad case of Lehman Brothers. More than four years later, the Lehman bankruptcy is still not completely resolved. As of its 10-K regulatory filing in 2007, Lehman operated a mere 209 subsidiaries across only 21 countries and had total liabilities of $619 billion. By these metrics, Lehman was a small player compared with any of the Big Five. If Lehman Brothers was too big for a private-sector solution while still a going concern, what can we infer about the Big Five in the table?

Correcting for the Drawbacks of Dodd–Frank

Dodd–Frank addresses this concern. Under the Orderly Liquidation Authority provisions of Dodd–Frank, a systemically important financial institution would receive debtor-in-possession financing from the U.S. Treasury over the period its operations needed to be stabilized. This is quasi-nationalization, just in a new, and untested, format. In Dallas, we consider government ownership of our financial institutions, even on a “temporary” basis, to be a clear distortion of our capitalist principles. Of course, an alternative would be to have another systemically important financial institution acquire the failing institution. We have been down that road already. All it does is compound the problem, expanding the risk posed by the even larger surviving behemoth organizations. In addition, perpetuating the practice of arranging shotgun marriages between giants at taxpayer expense worsens the funding disadvantage faced by the 99.8 percent remaining—small and regional banks. Merging large institutions is a form of discrimination that favors the unwieldy and dangerous TBTF banks over more focused, fit and disciplined banks.

The approach of the Dallas Fed neither expands the reach of government nor further handicaps the 99.8 percent of community and regional banks. Nor does it fight complexity with complexity.

It calls for reshaping TBTF banking institutions into smaller, less-complex institutions that are: economically viable; profitable; competitively able to attract financial capital and talent; and of a size, complexity and scope that allows both regulatory and market discipline to restrain excessive risk taking.

Our proposal is simple and easy to understand. It can be accomplished with minimal statutory modification and implemented with as little government intervention as possible. It calls first for rolling back the federal safety net to apply only to basic, traditional commercial banking. Second, it calls for clarifying, through simple, understandable disclosures, that the federal safety net applies only to the commercial bank and its customers and never ever to the customers of any other affiliated subsidiary or the holding company. The shadow banking activities of financial institutions must not receive taxpayer support.

We recognize that undoing customer inertia and management habits at TBTF banking institutions may take many years. During such a period, TBTF banks could possibly sow the seeds for another financial crisis. For these reasons, additional action may be necessary. The TBTF BHCs may need to be downsized and restructured so that the safety-net-supported commercial banking part of the holding company can be effectively disciplined by regulators and market forces. And there will likely have to be additional restrictions (or possibly prohibitions) on the ability to move assets or liabilities from a shadow banking affiliate to a banking affiliate within the holding company.[11]

To illustrate how the first two points in our plan would work, I come back to the hypothetical structure of a complex financial holding company. Recall that this type of holding company has a commercial bank subsidiary and several subsidiaries that are not traditional commercial banks: insurance, securities underwriting and brokerage, finance company and others, many with a vast geographic reach.

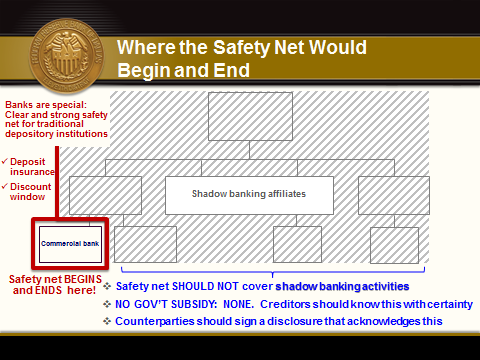

Where the Government Safety Net Would Begin and End

Under our proposal, only the commercial bank would have access to deposit insurance provided by the FDIC and discount window loans provided by the Federal Reserve. These two features of the safety net would explicitly, by statute, become unavailable to any shadow banking affiliate, special investment vehicle of the commercial bank or any obligations of the parent holding company. This is largely the current case—but in theory, not in practice. And consistent enforcement is viewed as unlikely.

SOURCE: Federal Reserve Bank of Dallas.

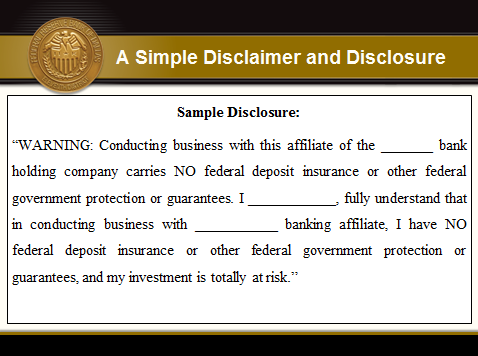

Reinforced by a New Covenant

To reinforce the statute and its credibility, every customer, creditor and counterparty of every shadow banking affiliate and of the senior holding company would be required to agree to and sign a new covenant, a simple disclosure statement that acknowledges their unprotected status. A sample disclosure need be no more complex than this:

This two-part step should begin to remove the implicit TBTF subsidy provided to BHCs and their shadow banking operations. Entities other than commercial banks have inappropriately benefited from an implicit safety net. Our proposal promotes competition in light of market and regulatory discipline, replacing the status quo of subsidized and perverse incentives to take excessive risk.

As indicated earlier, some government intervention may be necessary to accelerate the imposition of effective market discipline. We believe that market forces should be relied upon as much as practicable. However, entrenched oligopoly forces, in combination with customer inertia, will likely only be overcome through government-sanctioned reorganization and restructuring of the TBTF BHCs. A subsidy once given is nearly impossible to take away. Thus, it appears we may need a push, using as little government intervention as possible to realign incentives, reestablish a competitive landscape and level the playing field.

Why Protect the 0.2 Percent?

My team at the Dallas Fed and I are confident this simple treatment to the complex problem and risks posed by TBTF institutions would be the most effective treatment. Think about it this way: At present, 99.8 percent of the banking organizations in America are subject to sufficient regulatory or shareholder/market discipline to contain the risk of misbehavior that could threaten the stability of the financial system. Zero-point-two percent are not. Their very existence threatens both economic and financial stability. Furthermore, to contain that risk, regulators and many small banks are tied up in regulatory and legal knots at an enormous direct cost to them and a large indirect cost to our economy. Zero-point-two percent. If the administration and the Congress could agree as recently as two weeks ago on legislation that affects 1 percent of taxpayers, surely it can process a solution that affects 0.2 percent of the nation’s banks and is less complex and far more effective than Dodd–Frank.

Making a Time of ‘Awful Moment’ a Time of Promise

The time has come to change the decisionmaking paradigm. There should be more than the present two solutions: bailout or the end-of-the-economic-world-as-we-have-known-it. Both choices are unacceptable. The next financial crisis could cost more than two years of economic output, borne by millions of U.S. taxpayers. That horrendous cost must be weighed against the supposed benefits of maintaining the TBTF status quo. To us, the remedy is obvious: end TBTF now. End TBTF by reintroducing market forces instead of complex rules, and in so doing, level the playing field for all banking institutions.

I return to Patrick Henry. He noted that “it is natural to man to indulge in the illusions of hope. We are apt to shut our eyes against a painful truth, and listen to the song of that siren till she transforms us.” We labor under the siren song of Dodd–Frank and the recent run-up in the pricing of TBTF bank stocks and credit, indulging in the illusion of hope that this complex legislation will end too big to fail and right the banking system. We shut our eyes to the painful truth that TBTF represents an ongoing danger not just to financial stability, but also to fair competition.

The Dallas Fed offers a modest but, we believe, far more effective fix to Dodd–Frank. This plan is not without its costs. But it is less costly than all the alternatives put forward and it seriously reduces the likelihood of another horrendous and costly financial crisis.

This need not be a time of “awful moment.” It should instead be a time of promise. Treating the pathology of TBTF now would be a big step toward a more stable and prosperous economic system, one that relies on fundamental principles of capitalism rather than regulatory complexity and increasing government intervention.

Thank you.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- See “Two Areas of Present Concern: the Economic Outlook and the Pathology of Too-Big-to-Fail (With Reference to Errol Flynn, Johnny Mercer, Gary Stern and Voltaire),” speech by Richard W. Fisher, July 23, 2009, and “Paradise Lost: Addressing ‘Too Big to Fail’ (With Reference to John Milton and Irving Kristol), speech by Richard W. Fisher, Nov. 19, 2009.

- See “Financial Stability: Traditional Banks Pave the Way,” Federal Reserve Bank of Dallas Special Report, January 2013, www.dallasfed.org (note: the report will be available online at 9 a.m. Eastern time on Jan. 17).

- See “The Blob That Ate Monetary Policy,” by Richard W. Fisher and Harvey Rosenblum, Wall Street Journal, Sept. 27, 2009.

- See “The Dog and the Frisbee,” by Andrew G. Haldane and Vasileios Madouros, Bank of England, paper presented at “The Changing Policy Landscape” symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyo., Aug. 30–Sept. 1, 2012.

- For a distinction between owner-controlled and management-controlled firms, see The Modern Corporation and Private Property, by Adolf A. Berle and Gardiner C. Means, New York: Macmillan, 1932.

- Several of the nation’s largest banking companies received massive and extraordinary government assistance in 2008–09 but were never listed as failures in the FDIC database nor included on the list of “problem banks.” Discipline without teeth probably leads the management of such institutions to “turn a deaf ear” to their supervisors. Rod Stewart said it well in his song “Young Turks”: “But there ain’t no point in talking, when there’s nobody listening.”

- See “Regulatory and Monetary Policies Meet ‘Too Big to Fail’,” by Harvey Rosenblum, Jessica J. Renier and Richard Alm, Federal Reserve Bank of Dallas Economic Letter, vol. 5, no. 3, 2010, Chart 1, p. 6. More specifically, Citigroup and BankAmerica Corp. experienced peak-to-trough declines in their common stock prices of over 96 percent.

- Bank for International Settlements 2011/2012 Annual Report, June 24, 2012, pp. 75–6.

- See “On Being the Right Size,” speech by Andrew Haldane, Bank of England, at the 2012 Beesley Lectures, Institute of Economic Affairs’ 22nd Annual Series, London, Oct. 25, 2012.

- For a review of shadow banking, see “Understanding the Risks Inherent in Shadow Banking: A Primer and Practical Lessons Learned,” by David Luttrell, Harvey Rosenblum and Jackson Thies, Federal Reserve Bank of Dallas Staff Papers, no. 18, 2012.

- As an example, Sen. David Vitter and Sen. Sherrod Brown cite in their letter to the Government Accountability Office on Jan. 1, 2013, that “Bank of America moved $15 trillion in derivatives contracts from its broker-dealer, Merrill Lynch, to its insured depository institution affiliate in response to a credit downgrade. ... This move reportedly saved the bank $3.3 billion in additional collateral payments.”

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.