'Oil and Gas, Blondes and Over-Accessorized Brunettes, and Ruthless, Hard-Drinking Cowboys' (With Reference to Sheikh Zayed, Diana Natalicio, My Nephew Charles and President Peña Nieto)

April 10, 2013El Paso, TX

I so appreciate being here at the University of Texas at El Paso (UTEP), my first outing since returning from a trip to the United Arab Emirates. The founder of the Emirates—a collection of former “Trucial States” along the lower coast of the Arabian Sea—was Sheikh Zayed bin Sultan Al Nahyan, a wise man who had no formal education but knew of its enormous value. He said, “Education is a lantern which lights the dark alleys of ignorance.”[1]

I mention this because I cannot think of an educator who embodies this practical dictum better than Diana Natalicio. President Natalicio is a bright, shining lantern in the world of education. Actually, that’s an understatement: She is a klieg light! We are blessed to have her lead UTEP and move Texas and the nation forward on the frontiers of higher education. I am tremendously honored to be introduced by her. Thank you, Diana.

I am going to depart from my usual format today and rely heavily on slides—slides that provide a factual basis for what is going to be a dose of “Texas brag.” With its branches in El Paso, San Antonio and Houston, the Federal Reserve Bank of Dallas—the Federal Reserve’s Eleventh District—covers about 27 million people over 360,000 square miles stretching from northern Louisiana to southern New Mexico. Over 96 percent of the economic output of the district comes from Texas.

I find that when I speak about my district in foreign lands—say, in New York or Washington, D.C.—there is a stereotypical reaction not unlike the image projected by the TV show Dallas. “Of course you are doing well,” they say. “You are rich in oil and gas, blondes and over-accessorized brunettes, and ruthless, hard-drinking cowboys.” Today, I want to set the record straight.

Prices Are Presently Stable; Employment Is Far From Optimal; the Efficacy of Quantitative Easing Is as Yet Unclear

The road to dignity is through work: Jobs provide the means for economic advancement. As the nation’s central bank, the Federal Reserve is tasked with maintaining price stability—a common monetary policy goal of all responsible central banks. But under the laws created by Congress that govern our franchise and allow it to operate independently, the Fed works under a dual mandate—to conduct monetary policy that keeps prices from inflating or deflating and to achieve full employment.

At the moment, and for the foreseeable future, neither inflation nor deflation appears on the forecast horizon. However, the longer-term inflationary consequences of the massive quantitative easing programs we have undertaken—programs I have opposed in our Federal Open Market Committee (FOMC) meetings but that have been approved by the majority of the committee—are as yet unclear. Those aftereffects will depend on how artful the committee will be in unwinding that accommodation on a timely basis. Indeed, one of the signal achievements of Federal Reserve policy under Ben Bernanke’s leadership is to have formalized a long-term inflation target of 2 percent, something the FOMC had never before distinctly declared.

Presently, the 12-month inflation rate is 1.6 percent, according to our calculation at the Dallas Fed, where we do a “trimmed mean” analysis of 178 items consumers use, including guns and beer (hopefully not enjoyed simultaneously) and the cost of gasoline, food, getting your hair cut or your shoes repaired, or buying an electronic device. Given that the trimmed mean analysis has proven to be an excellent rule-of-thumb predictor of headline inflation one year forward, we can say with some degree of confidence that, at present, we are keeping inflation at or below our 2 percent target.

Employment, however, is not at a comfortable level. Pick up any newspaper or go to any news website or broadcast medium and you will read or hear of the still-too-high unemployment rate that bedevils our economy. Monetary policy acts with a lag, including unorthodox monetary policy as it is now being conducted. It would appear from some studies and from anecdotal evidence that companies are starting to use the copious cheap money they have access to for investing in capital projects and employing increasing amounts of workers.[2] But it is not yet clear that we will achieve a justifiable bang for the trillions of bucks the Fed has flooded the economy with. Only time will tell if the efficacy of quantitative easing we have undertaken was justifiable in regard to job creation and delivering on the second component of our dual mandate.

Yet many things do emerge when you examine the entrails of employment data from across the country. One thing is that you learn a lot about Texas, which is the focus of my remarks today.

‘If You Pull Texas Out of the Puzzle, the Country Falls Down’

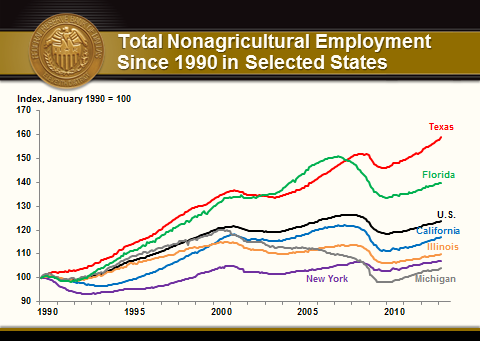

For the past 22 years, Texas has outgrown the country by a factor of more than 2-to-1. Here is a slide that shows the percentage increase in jobs created by several large states and for the U.S. as a whole since 1990:

SOURCES: Bureau of Labor Statistics; Federal Reserve Bank of Dallas.

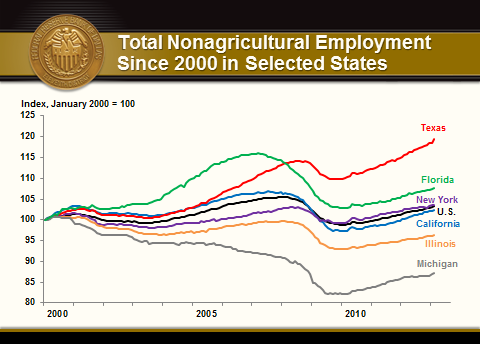

And here is a look at the rate of job creation for those same states and the U.S. as a whole since 2000:

SOURCES: Bureau of Labor Statistics; Federal Reserve Bank of Dallas.

We were one of the last states to go into the recent recession and one of the first to come out. In terms of jobs, as of now, 10 states have come back to or have exceeded employment levels that prevailed before the crisis: Alaska, Louisiana, Massachusetts, New York, North Dakota, Oklahoma, South Dakota, Texas, Utah and West Virginia.

The Federal Reserve has no index that measures the number of blondes or ruthless cowboys in Texas, but we can account for the influence of oil and gas on our state’s welfare: Oil and gas extraction and mining support directly accounts for 2.4 percent of our workforce—two-point-four percent. And the energy sector’s total contribution to our state’s gross domestic product (GDP) is roughly 10 percent. So yes, the foreigners are correct: We have a strong energy sector in Texas. We are the No. 1 producer of oil and gas in the nation. We produce more oil than Venezuela and more natural gas than Canada. On net, high energy prices do, indeed, benefit Texans.

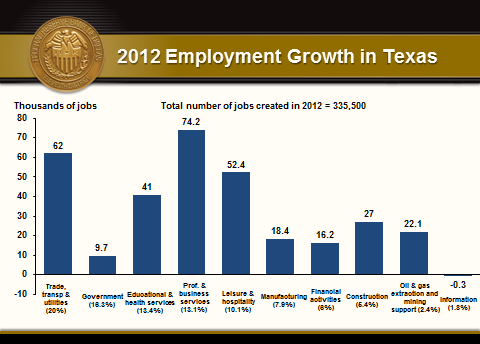

But look at this slide of the number of jobs created by sector in 2012:

SOURCES: Bureau of Labor Statistics; Federal Reserve Bank of Dallas.

Oil and gas and mining and their support services accounted for 22,100, or less than 7 percent, of the 335,500 jobs created in Texas last year. Professional and business services accounted for 74,200; trade, transportation and utilities 62,000; leisure and hospitality 52,400; educational and health services 41,000; and construction 27,000. Each of these sectors created more jobs than the energy sector. Of course, the oil and gas sector has large multipliers, so the overall economic impact is greater than just these 22,100 jobs. The University of Texas at San Antonio—your sister organization—estimates that the Eagle Ford Shale generated over $61 billion in economic impact in 2012. As this chart shows, however, ours is a diversified economy, creating jobs across the spectrum.

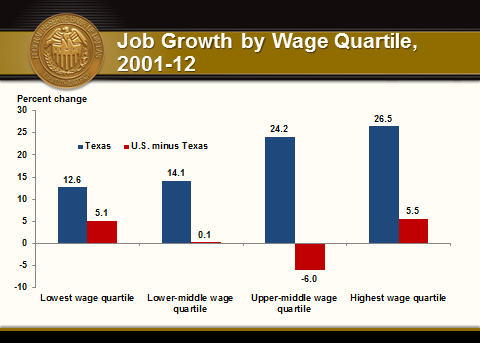

“But these jobs are all low paying,” our uninformed friends say. And to that I respond: “You are right. We create more low-paying jobs in Texas than anybody else. Yet look at this breakdown of job creation by income quartile for Texas versus the United States minus Texas for the past 10-plus years”:

SOURCE: March CPS, 2001, 2012.

We created a lot of low-paying jobs. But we also created far more high-paying jobs. Most importantly, while the United States has seen job destruction in the two middle-income quartiles, Texas has created jobs for those vital middle-income workers, too.

The bottom line—we have experienced growth across all sectors and in all income categories. And it continues: In February, job growth in Texas was an annualized 6.9 percent. Year to date, construction, trade and transportation, and professional and business services have led the pack in what we believe will be another year of employment growth that, knock on wood, will approach 3 percent.

Here are some other facts that help round out the economic picture of our state.

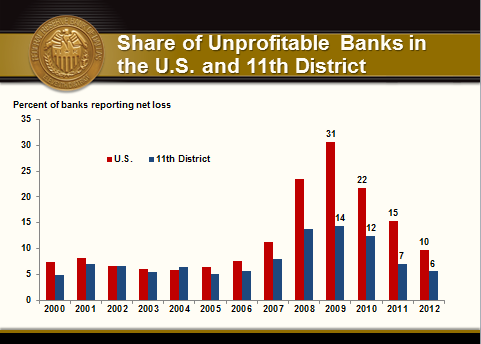

Our banks are more profitable than those in the rest of the nation …

SOURCES: Bureau of Labor Statistics; Federal Reserve Bank of Dallas.

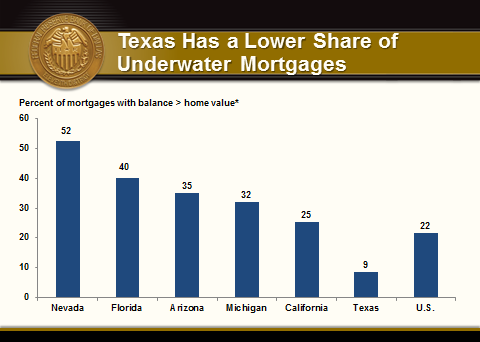

In the housing sector, we have fewer underwater mortgages …

SOURCE: CoreLogic.

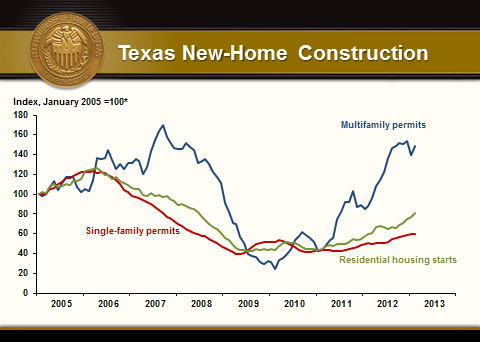

Robust new-home construction …

SOURCES: U.S. Census Bureau; Bank of Tokyo-Mitsubishi UFJ.

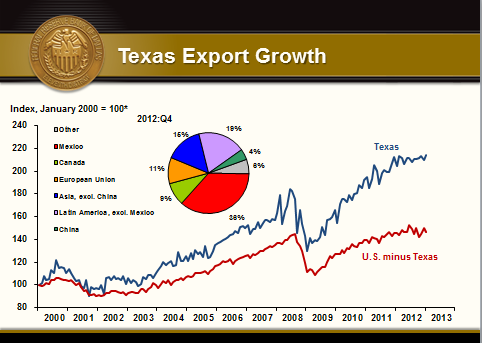

And an export sector that has come out of the recession like gee-whiz. In, fact, you can see from this graph that without Texas, the top blue line, exports from the rest of the United States, indicated by the red line, are hovering around the peak level of 2008:

SOURCES: Census Bureau; World Institute for Strategic Economic Research; Federal Reserve Bank of Dallas

My little nephew, Charles, was playing with a three-dimensional wooden puzzle map of the United States in his preschool class the other day. He came home with the piece that was Texas and a smirk on his face: “Mom,” he said, “guess what? If you pull Texas out of the puzzle of the United States, the rest of the country falls down!”

Although little Charles lives in Massachusetts, he gets the picture. It came as no surprise when a recent study by the highly respected Brookings Institution, as reported in the Wall Street Journal last week, revealed that only 14 of the nation’s 100 biggest metropolitan areas have more people employed than they did before the 2007–09 recession and that six of them are in Texas: Austin, San Antonio, McAllen, Dallas, Houston and … El Paso. “Robust employment in the oil and gas industries helped the Texas cities,” the article read, “although data from the Texas Workforce Commission suggests the job recovery has come from a variety of industries.”[3] Amen to that.

El Paso at a Crossroads

You’ll note that El Paso was mentioned in the Brookings study. Let’s talk a little about this unique city.

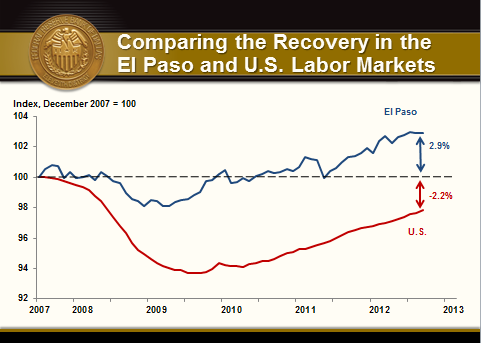

It’s no small wonder that of the 23,000 students enrolled at UTEP, 77 percent are Mexican–Americans and another 6 percent commute from Ciudad Juárez, across the border. El Paso is at the very nexus of the cultures and economies of two countries. As Roberto Coronado, our economist and assistant vice president in charge at our El Paso Branch, likes to point out, “Given its unique geographic position, El Paso is very good at importing recessions both from the north and from the south of the Rio Grande.” I would add that it’s also good at drawing from the best of both countries in recoveries. The El Paso labor market has outperformed that of the U.S. for several years. Here is a graph that shows how the El Paso employment picture has changed relative to the U.S. since the onset of the Great Recession:

SOURCES: Bureau of Labor Statistics; HAVER Analytics.

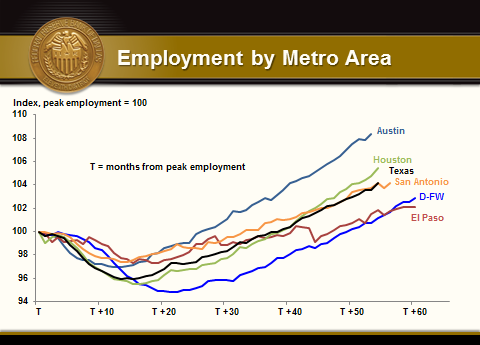

Now, as the following chart demonstrates, it remains a fact that the local employment picture is less bright in El Paso than in Texas’s other major metro areas.

SOURCES: Bureau of Labor Statistics; HAVER Analytics.

The unemployment rate here is hovering around 9 percent. El Paso’s unemployment rate has historically been 2 percentage points higher than the U.S. rate and 3.2 percentage points above the Texas rate. In part, this is due to population growth. El Paso had more than 21 million border crossings in 2011 alone. Most of these visitors came to shop, but many stayed and looked for jobs. These visitors increase the number of job seekers in the unemployment equation, driving the rate upward.

Of additional concern is that El Paso is more dependent on federal government employment than any other Texas city, with 5 percent of your workforce coming from the public sector. And that is before accounting for the payroll of Fort Bliss itself and the impact it has on private-sector employment and consumption. Clearly, El Paso is quite vulnerable to constriction in the growth of federal spending. This will ultimately present serious challenges as the federal government struggles to right its fiscal imbalances.

The Good News

But there is good news that offsets that risk:

Thanks to the North American Free Trade Agreement, or NAFTA—an agreement that, as Diana mentioned, I played a role in implementing as deputy U.S. trade representative—El Paso is no longer at the edge of the United States but, instead, at a strategic location in the vast North American market.

In this context, the maquiladoras of Ciudad Juárez become an important factor determining El Paso’s economic fate. The relationship exists via a ricochet effect that begins with U.S. industrial activity picking up, say in auto manufacturing, followed by new production orders being sent to Ciudad Juárez maquiladora plants and then economic benefits flowing back to El Paso. The flowback to El Paso comes from firms on this side of the border providing logistical support, insurance and other services to the maquiladoras—as well as in the aforementioned form of maquiladora employees shopping and consuming more on this side of the border. And, as this table shows, it results in an increase of high-value-added sales of El Paso-based services into Ciudad Juárez, making up for reductions in manufacturing jobs on this side of the border:

Ciudad Juárez Maquiladoras’ Impact on El Paso |

|

Percent increase per every 10 percent increase in maquiladora output |

|

Total employment |

2.8 |

Transportation employment |

5.3 |

Retail trade employment |

1.3 |

Finance, insurance, real estate employment |

2.1 |

Services employment |

1.8 |

Manufacturing employment |

-1.3 |

SOURCE: “The Impact of Maquiladoras on U.S. Border Cities,” by Jesus Cañas, Roberto Coronado, Robert W. Gilmer and Eduardo Saucedo, Growth and Change, forthcoming. |

|

¡Sigue México!

As the maquiladora example illustrates, Mexico has a significant impact on the fate of the El Paso economy.

This is fortunate because the Mexican economy is being transformed to a greater degree than most people here in El Norte understand.

On Sunday, the Dallas Morning News kindly ran an op-ed piece I wrote based on the work of our Dallas Fed economists, titled “Mexico Outdoes the U.S. on Fiscal Discipline.”[4] The article outlines the great progress Mexico has made in transforming its economy and the significant steps taken by President Enrique Peña Nieto in the footsteps of his predecessors, from President Calderon back to President Salinas.

Here are the facts:

Mexico recovered more quickly from the recession than the United States.

Mexico’s 3.3 percent GDP growth in 2012 compares with the U.S.’s 1.7 percent.

Mexico, home to 1980s hyperinflation and a poster child of that decade’s Latin American debt crisis, has recorded a core consumer price index annual inflation rate below 3 percent for the last three months. In fact, inflation in Mexico has trended down for two decades following two important reforms: central bank independence in 1994 and adoption of inflation targeting in 2001.

Meanwhile, the peso, floating since late 1994, held its own through the global financial crisis. And year to date, the peso has gained 6.9 percent against the dollar.

Low and stable inflation, together with a steady peso, has protected the purchasing power of the Mexican consumer and allowed nest eggs to grow. Those nest eggs can now be safely deposited in banks. After a horrific banking crisis in 1994–95 and an ensuing decade of stagnant lending, Mexico’s banking industry is growing again and financial access, while still limited, is expanding quickly. The number of Mexican banks increased 14.3 percent in 2012; in the U.S., the number of institutions contracted 3.1 percent. It may be surprising to you that Mexican banks are also better capitalized than U.S. banks. As of Dec. 31, 2012, equity-to-asset ratios were 11.1 percent at U.S. banks and 15.9 percent at Mexican banks.

On the fiscal front, Mexico’s 2012 budget deficit was a respectable 2.6 percent of GDP, which compares with 7 percent here. For all their differences, Mexican lawmakers on the right and the left have a commitment to fiscal discipline. They adopted a balanced-budget rule in 2006 and have chosen to abide by it rather than take the “kick the can down the road” approach of the U.S. Congress. As a result, Mexico’s national debt is stable at 28 percent of GDP, while here it raced past $16 trillion in 2012, about 105 percent of GDP.

Mexico has also remained a staunch proponent of free trade. Exports and imports now make up 62 percent of Mexican economic output versus 17.5 percent as recently as 1980. Since Mexico joined the General Agreement on Tariffs and Trade (the forerunner of the World Trade Organization) in 1986 and ratified NAFTA in 1994, it has forged 12 trade pacts with 44 nations.

With all the progress in the macro economy, banking, finance and trade, structural reforms are what Mexico now needs to catapult it to a leadership role among emerging-market economies. If President Peña Nieto’s first 100 days in office are any indication, this critical next step is underway. He has engineered the Pacto por México (Pact for Mexico) with the other political parties; arrested Elba Esther Gordillo, the corrupt leader of the massive national teachers’ union; brought a class-action suit against Carlos Slim’s growth-retarding telecommunications empire; and begun a national conversation about reforming the country’s woefully underperforming, yet potentially rich energy sector.

If this effort at structural modernization continues, Mexico’s growth will increase significantly.

All of this will be good for El Paso. Just as El Paso suffers when recession afflicts both sides of the border, it will prosper as expansion takes hold here in the U.S. and in Mexico.

The Good, the Bad and the Comical

Let me give you a pictorial summary of this lecture:

We are blessed by a force of nature named Diana Natalicio (a Texas blonde, by the way!) …

By UTEP as a symbol of El Paso’s critical place at the crossroads of North America…

By having the good fortune to live in Texas …

And by sharing a border with an increasingly successful neighbor to our south.

But we also have challenges. It would be unbecoming of a central banker to be entirely optimistic—we are a pretty sober species. So here is the bad news. Here’s what is holding back the economic progress of El Paso, Texas, Mexico and America:

Yup—Washington. The Federal Reserve has provided plenty of, if not too much, high-octane fuel in the form of cheap and abundant money to propel the economy forward. Our southern neighbor, Mexico, is responsibly managing its fiscal affairs and structural reforms (as is our northern neighbor, Canada).

Texas is showing the nation the way to create jobs and encourage prosperity with a highly diversified economy. And yet Congress and executive branch cannot agree on a budget, or on a path forward for taxes and spending, or on a regulatory structure that incentivizes business to put people back to work.

This is the subject of an entire separate lecture. But to summarize the root fiscal problem of past Congresses and administrations, Democrat- or Republican-led, my staff found a clip on YouTube that sums it up better than words:

That sketch says it all. We must all pray that our president and our congressional representatives will find a way to reverse their spendthrift ways and do what is right by putting us back on the path of fiscal probity.

El Paso and Texas have done well despite the disorderly behavior of our nation’s fiscal authorities. Imagine how well we would do if they actually managed to get their act together!

As we eagerly await that day, let us be thankful for the exceptional nature of this great state, this great city and this wonderful university. ¡Ándale Pues!

Gracias.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- As quoted by Sheikh Nahayan Mabarak Al Nahayan, Minister of Culture, Youth and Community Development and Chancellor, Higher Colleges of Technology, in his speech at Sharjah Women’s College, United Arab Emirates, March 27, 2013.

- See “Easy Money: Fed Policies Spur Corporate Spending,” by Victoria McGrane, Wall Street Journal, April 9, 2013.

- See “Hiring Spreads, but Only 14 Cities Top Prerecession Level,” by Amy Schatz, Wall Street Journal, March 31, 2013.

- See “Mexico Outdoes the U.S. on Fiscal Discipline,” by Richard W. Fisher, Dallas Morning News, April 7, 2013. This article was based on the excellent work of Federal Reserve Bank of Dallas economists Pia Orrenius, Jesus Cañas, Roberto Coronado and Ed Skelton. For information on inflation in Mexico, see “The Conquest of Mexican Inflation,” by Mark Wynne and Edward C. Skelton, in the Globalization and Monetary Policy Institute 2011 Annual Report, Federal Reserve Bank of Dallas.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.