Fiscal Policy. Oy! (With Reference to Ben Bernanke, Ken Arrow, Thomas Jefferson, William Shakespeare and the Oracle of Omaha)

May 16, 2013 Houston, TX

Thank you, Ken (Simonson). I am delighted that the National Association for Business Economics (NABE) has chosen the Dallas Fed’s Houston Branch as the venue for this meeting on the oil and gas boom as a possible engine for “Reigniting the Economy.” As you will shortly hear from my Dallas Fed colleague, Mine Yücel; my wise old colleague from my days at Treasury in the 1970s, Phil Verleger; the incoming chairman of our San Antonio Branch, Curt Anastasio; and others, this is an intriguing proposition. The technical and entrepreneurial genius of Houston and Texas is playing a key role in unlocking our nation’s energy potential. Indeed, there are many here in Texas and abroad—in places as distant as Illinois, Michigan and New York—who argue that reigniting their local economies and the nation’s economy calls for more “Texification,” above and beyond the frontiers of energy.

But I am not here today to discuss oil and gas or engage in “Texas brag.” I have been asked to provide a broader perspective on the nation’s economic and monetary policy.

Current Predicament of Monetary Policy: A Grand Experiment

I’ll begin with a summary of the current predicament of monetary policy.

The Federal Reserve has undertaken a grand experiment to reignite the economy through unprecedented monetary accommodation. We cut to zero the base rate that anchors the yield curve and have pursued a policy aimed at driving rates throughout the curve to historic lows by buying Treasuries and mortgage-backed securities (MBS). Our portfolio totals about $3 trillion, which we have recently been expanding at a rate of $85 billion per month.

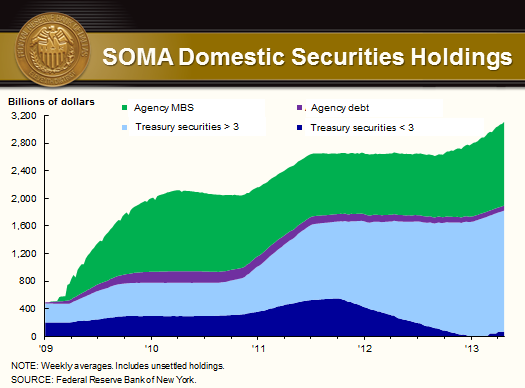

Here is a picture of the domestic securities of the current System Open Market Account (SOMA) portfolio. [1]

The sea change in the balance sheet in recent years is immediately visible: In sharp contrast to the past, we now hold almost no Treasury notes of less than three years’ duration—the dark blue space. We have purchased in the secondary markets some $1.7 trillion in longer-term Treasuries—the light blue area—and, as denoted by the green, more than $1.1 trillion of securities backed by the Federal National Mortgage Association (commonly known as Fannie Mae), the Federal Home Loan Mortgage Corp. (Freddie Mac) and the Government National Mortgage Association (Ginnie Mae). We live in an age of big numbers when I can say, “Ignore the purple space, for it is only $70 billion in remaining Fannie and Freddie debentures, aka ‘agency debt.’” Before the crisis, when we didn’t have any agency debt, $70 billion would have represented 8 percent of our balance sheet.

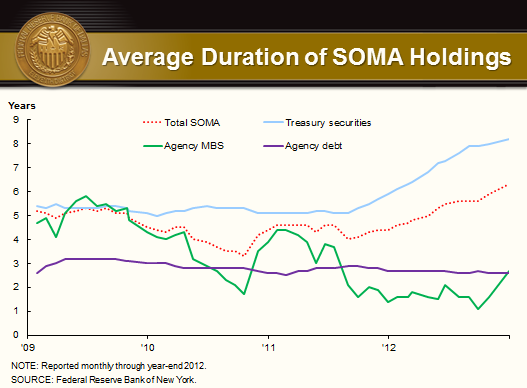

As to the duration of these purchases, here is a picture from year-end 2012:

Including securities purchased since then, the total SOMA portfolio has an average duration of seven years, with Treasury securities at eight years and MBS having risen to four years.

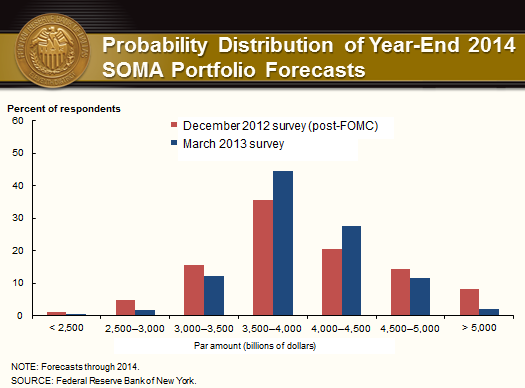

According to dealers’ forecasts at year-end and as of March, the probability distribution of the expected size of the SOMA portfolio is as follows:

So, you now have a snapshot of where we are. The Federal Open Market Committee (FOMC) has cut the short-term rate to zero. Being “zero bound,” we instructed our traders to embark on a buying spree of Treasuries and MBS, and they have done so, ballooning our balance sheet from its precrisis level of less than $900 billion to about $3.3 trillion. Presently, the committee is adding to its holdings at a rate of $85 billion in longer-term securities each month, in addition to reinvesting principal payments from holdings of agency MBS and agency debt securities into agency MBS. And the predominant sentiment of the “market,” as measured by our dealer surveys, presently posits that we will build our holdings further, to between $3.5 trillion and possibly $5 trillion by the end of 2014.

The Economy’s Dashboard

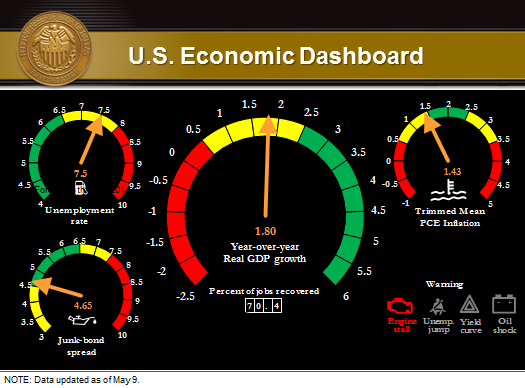

As to the status of the economy, here is the dashboard our Research Director (and former NABE President) Harvey Rosenblum uses as a simple graphic to describe the current economic predicament:

You will note that the data compiled at the end of the first quarter on real gross domestic product (GDP) growth and inflation—as measured by the Trimmed Mean Personal Consumption Expenditure (PCE) Index, the Dallas Fed’s preferred indicator—show that both increased less than 2 percent year over year. The dashboard also indicates that at quarter’s end, we were cruising along at near stall speed—note the “Engine stall” red warning light. The unemployment-rate gauge is not red because it declined to 7.5 percent in April. And, as indicated by the odometer box, we have traveled some distance in job creation, even though we have not seen the job creation we might have hoped for in a typical recovery: 70.4 percent of jobs lost in the recent recession have been recovered, up from about 50 percent only a year ago. The indicator for the yield curve, if anything, is robust. Junk-bond spreads are below 5 percent; nominal yields for even the lowest-grade bonds (CCC-rated credit that is one notch above default) have fallen to below 7 percent from double digits only a year ago. Further, covenant-light lending is on a tear. The “oil gauge” indicates the Fed has supplied plenty of lubrication for the engine of job creation.

Professional Forecasters Have Been Disappointed Thus Far…

Over the four years since the recession ended in June 2009, GDP growth has averaged just 2.1 percent, hewing to a narrow year-over-year range of 1.5 to 2.8 percent. It is noteworthy that the fraternity of professional economic forecasters has been consistently disappointed: Forecasts made at the beginning of 2010, 2011 and 2012 all overpredicted growth. At the onset of this year, the median forecast for 2013 called for 2.4 percent GDP growth, and that, too, has been challenged by first-quarter data that came in below expectations, raising fears of “déjà vu all over again.”

…But April Could Signal Improvement

However, the April jobs report and revisions of previous jobs data have put some spring back in economists’ steps. Initial claims for unemployment insurance are now back on a downward trend, retreating to prerecession levels, and Monday’s retail sales numbers were a nice upside surprise. This indicates that consumers may have digested delayed tax rebates and the increase in payroll taxes, and are reaping the benefits of lower gasoline and food prices. So the recovery presently appears to be strong enough to propel hopes that employment growth will continue improving over the near term.

As to Inflation…

Of course, the Fed’s most sacred duty is to see to the maintenance of price stability. Today, inflation is benign. With a jobless rate still well north of 7 percent, labor compensation rising at less than 2 percent per year, an outlook for abundant food crops and expanding energy sources, and near-record profit margins among operating businesses, there appears to be little risk that we will see significant cost-push pressures in 2013. In addition, slower growth around the globe is putting the damper on demand-pull inflation. Provided that the public remains confident in the Fed’s commitment to long-run price stability, anchored by the FOMC’s stated commitment to a target of 2 percent, my reading of the entrails of the Trimmed Mean PCE inflation rate currently indicates we will likely end this year somewhere between 1.5 percent and our 2 percent long-run goal. [2]

As a hawk in the aviary of policymakers, I have for some years now said that the issue at present is not a meaningful threat to price stability in the immediate future. The issue is job creation. And the questions I keep raising at FOMC meetings regard our ability to affect it.

Time to Reset the Fed’s Sails?

Having spent the happiest of my formative years preparing for and attending the U.S. Naval Academy, then paying my way through Harvard sailing oceangoing yachts as a hired hand, I am given to seafaring analogies. Here is how I would summarize our most recent journey:

The current chairman, Ben Bernanke, took the wheel at the Fed just as we sailed into a tempest that nearly capsized our economy. He and his able crew kept the ship of the economy from floundering and navigated it past the rocks of depression and deflation. The Bernanke-led FOMC steered clear of the shoals of economic collapse by jury-rigging the vessel of monetary policy in an unconventional and unprecedented manner. Now the ship of the Fed is in more benign waters and is sailing forward. The question before us is this: Are we moving forward at sufficient speed to allow the Fed to reset our rigging and our sails, eventually going back to a more conventional configuration?

The answer lies in the economic outlook. I am wary of giving pinpoint forecasts of economic growth. As I mentioned earlier, professional forecasters, including the very capable staff of the Federal Reserve, have fallen short on this front, time and again, during the recovery and on numerous occasions before that. I am always mindful of the memorable comments of Ken Arrow. You may recall them:

During World War II, Arrow served as a weather officer in the Army Air Corps. He and his team were charged with producing month-ahead weather forecasts. Being a disciplined analyst, Arrow reviewed the record of his predictions and, sure enough, confirmed statistically that the corps’ forecasts were no more accurate than random rolls of dice. He asked to be relieved of this futile duty. Arrow’s recollection of the response from on high was priceless: “The commanding general is well aware that the forecasts are no good. However, he needs them for planning purposes.”

With that caveat in mind, my staff and I think there is a better-than-even chance that the present GDP growth consensus forecast of 2.4 percent by professional economists may be underestimating the underlying pace of growth. The housing market is in resurgence, contributing significant impetus to the economy. The Fed’s senior loan officer surveys indicate that commercial banks are becoming more accommodative lenders, albeit remaining cautious. [3] The snapback in housing and the harnessing of cheap and abundant money by the business sector have made for more manageable financial obligations. State and local governments, not just in Texas but elsewhere in the nation, are on a better financial footing and no longer appear to be a major drag on growth. As this audience knows better than anybody, new technologies are providing for cheaper and more abundant energy. Consumers continue consuming. Monetary policy is hyper-accommodative, driving interest rates to historic lows and equity markets to historic highs; if anything, it may be giving rise to excessive speculation and risk taking. (In addition to the pricing of CCC debt and the surge in low-covenant lending, margin debt is climbing rapidly.)

I have advocated that we begin to reef in the sails, beginning with our MBS purchase program. In my view, the housing market is on a self-sustaining path and does not need the same impetus we have been giving it. In recent months, under its balance-sheet expansion program, the Fed has bought about 50 percent of gross issuance of agency MBS, partly to replace prepayments of our MBS holdings. When refinancing activity eventually shifts down, the Fed could soon be buying up to 100 percent of MBS issuance if the current purchase program continues. I believe buying such a high share of gross issuance in any security is not only excessive, but also potentially disruptive to the proper functioning of the MBS market. I have never been comfortable with our investing in anything but Treasuries, being wary of a central bank engaging in credit allocation and favoring specific sectors of the economy. It brings to mind the fears Thomas Jefferson and James Madison had about the slippery slope of Alexander Hamilton’s First Bank of the United States, recently recalled in Jon Meacham’s brilliant book on Jefferson: “They feared that the Hamiltonian program would enable financial speculators to benefit from commercial transactions made possible by government funds.”[4]

Yet I admit that given the crucial role housing plays in our economy and the dire straits the housing market was in at the time, I did hold my nose and vote for the first tranche of MBS purchases. I believe that initiative was helpful in jump-starting the housing market. But now I believe the efficacy of continued purchases is questionable. And I consider holding $1.1 trillion and counting of MBS as a possible impairment to our ability to maneuver our balance sheet with the nimbleness and alacrity we might need. I think we can rightly declare victory on the housing front and reef in (or dial back) our purchases, with the aim of eliminating them entirely as the year wears on.

Enter Fiscal Policy. Oy!

Even if we at the Dallas Fed are right and the overall outlook for the economy is better than the current dashboard or the conventional prognostications of economists, there exists a formidable brake on growth. It was referred to point-blank in the last statement issued by the FOMC: “…fiscal policy is restraining economic growth.”[5]

Fiscal policy is inhibiting the transmission of monetary policy into robust job creation.

As it is early in the morning and a little levity is always helpful in making a point, here is my favorite spoof on the historical behavior of fiscal policy makers:

This would be funny if it were not so sad. The propensity of members of Congress has been to spend in excess of revenues to give pleasure to their constituents and garner their affection. They just didn’t get the memo that Jefferson wrote to Madison:“We are ruined, Sir, if we do not overrule the principles that ‘the more we owe, the more prosperous we shall be,’ [and] ‘that a public debt furnishes the means of enterprise.’” [6] The good news is that, some 200-plus years later, the memo seems to have finally been received; there are numerous plans to rein in Congress’ spendthrift ways and there have been improvements that have brightened the short-term outlook for the level of federal debt. [7] But, as yet, there has been little more than passive action. Until the Congress and the president provide a clear road map as to how fiscal rectitude will be implemented, this lack of credible details for limiting the debt-to-GDP ratio and reengineering fiscal policy to stimulate rather than constrain growth is creating undue uncertainty about future tax rates, future government purchases, future retiree benefits and all manner of factors that impact employment and economic growth. Meanwhile, the divisive nature and petty posturing of those who must determine the fiscal path of the nation is further undermining confidence and limiting the effectiveness of monetary policy.

Here is the rub: Even if the arguments of those who wish for greater fiscal stimulus prevail, expansion in government purchases will have reduced effectiveness if it is thought that those purchases will be financed with higher future marginal tax rates. If you are an operating business, you have to discount this risk before adding significantly to payrolls and before undertaking capital expansion. In a similar vein, you need to consider how the opposite approach of cutting government expenditures might impact your top line if the cuts are in areas that affect the markets you sell into. Add to that the enormous uncertainty about how health care reform will impact your cost structure. And add to that the fact that community bankers—providers of the lifeblood of loans to small businesses, which are the impetus for new job creation and economic rejuvenation—are hamstrung by burdensome regulations and fees imposed in response to the misbehavior of their too-big-to-fail brethren. If you consider the economy from this perspective, you can see where brakes of our own government’s making are being applied to a realization of our growth potential.

Decisionmaking under conditions of uncertainty is always a challenge for businesses; decisionmaking in a thick fog of uncertainty is well-nigh impossible. It negates the power of hyper-accommodative monetary policy to propel our economic vessel forward. The restraining influence of rudderless fiscal policy is readily seen in the piling up of excess reserves on the balance sheets of banks and in the coffers of operating businesses.

I argue that the Fed has no hope of moving the economy to full employment unless our fiscal authorities get their act together. Those economic agents with the wherewithal to expand payrolls and put the American people back to work must have confidence that our fiscal authorities and regulation makers—the legislative and the executive—will reorganize the tax code, spending habits and the regulatory regime so that the cheap and abundant money we at the Fed have made available to invest in job-creating capital expansion in the United States is put to use. Until then, I argue that the Fed is, at best, pushing on a string and, at worst, building up kindling for a massive shipboard fire of eventual inflation.

All the World’s a Stage (and All the Policymakers Merely Players)

It is thus as-yet unclear whether the benefits of the strategy the Fed has taken outweigh its costs. Only time will tell. The Federal Open Market Committee will have to wait for the verdict of history. Scholars know that Shakespearian plays all have five acts. I would suggest that we are but in the third act of a play—we had the tempest in Act 1; the jury-rigging of monetary policy and radical maneuvers by the Fed to save the ship in Act 2; and in the present act, we are back on course but somewhat becalmed, sailing at less-than-desired cruising speed even as we have cranked up an auxiliary motor of large-scale asset purchases. Act 4 will involve the travails and challenges of adjusting our policy course, fine-tuning the motor and rearranging the rigging. And not until the final act will we know whether we have achieved the felicitous outcome that is the hallmark of most romantic plays, or whether the melancholy that defines a tragedy awaits us.

The romantic outcome ends, as most all Shakespearian comedies do, in a marriage—in this case, a marriage of sensible fiscal and monetary policy that lifts employment and carries the American economy to new heights.

The tragic outcome is one in which the fiscal authorities—the Congress and the president—are unable to provide incentives for risk takers to make use of the cheap and abundant capital the Fed has made available, and the play ends in a debasement of the central bank and the ruination of our economy and lifestyle.

The former outcome is that envisioned by the theoreticians that lead the Fed: According to this plot, by driving rates to historical lows along the entire length of the yield curve, investors will rebalance their portfolios and reach out to riskier assets, providing the financial wherewithal for businesses to increase capital expenditures and reengage workers, expand payrolls and regenerate consumption. Rising prices of bonds, stocks and other financial instruments will bolster consumer confidence. The CliffsNotes account of this play has the widely heralded “wealth effect” paving the way for economic expansion, thus saving the day.

The latter outcome posits that the wealth effect is limited, for two possible reasons. One is that our continued purchases of Treasuries are having decreasing effects on private borrowing costs, given how low long-term Treasury rates already are. Another is that the uncertainty resulting from fiscal tomfoolery is a serious obstacle to restoring full employment. Until job creators are properly incentivized by fiscal and regulatory policy to harness the cheap and abundant money we at the Fed have engineered, these funds will predominantly benefit those with the means to speculate, tilling the fields of finance for returns that are enabled by historically low rates but do not readily result in job expansion. Cheap capital inures to the benefit of the Warren Buffetts, who can discount lower hurdle rates to achieve their investors’ expectations, accumulating holdings without necessarily expanding employment or the wealth of the overall economy.

I hold no vendetta against the Buffetts of the world, having once been a junior member of that class—I made a nice living during the 1980s and ’90s buying operating assets for nickels and dimes and turning them into dollars by rationalizing and downsizing them. And like legions of others, I have for countless years read the Oracle of Omaha’s annual statement with admiration for his prowess as an investor and profit-seeker. But my role as a policymaker is different from my previous role as an investor: I have sworn fealty to a dual mandate of conducting monetary policy so as to maintain price stability AND create the monetary conditions for full employment and prosperity for all, not just for the rich and the quick. This, I fear, we will fail to do unless Congress and the president develop and deliver on a strategy that complements ours at the Fed.

This may be a sour ending to a somber song, but, after all, economics is not called “the dismal science” for nothing. Have a nice day!

Now, in the best tradition of central bankers, I would be happy to avoid answering your questions.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- For more information, see the New York Fed’s website at www.newyorkfed.org/markets/soma/sysopen_accholdings.html

- For the latest reading of the Dallas Fed’s alternative measure of core inflation, see www.dallasfed.org/research/pce/index.cfm.

- For more information regarding the Senior Loan Officer Opinion Survey, see www.federalreserve.gov/boarddocs/SnLoanSurvey/201305/default.htm.

- See Thomas Jefferson: The Art of Power, by Jon Meacham, New York: Random House, 2012, p. 248.

- The latest statement by the Federal Open Market Committee and the Board of Governors on the stance of monetary policy can be found at www.federalreserve.gov/newsevents/press/monetary/20130501a.htm.

- See note 4, p. 241.

- See “Our Debt Problems Are Still Far from Solved,” Committee for a Responsible Federal Budget, May 15, 2013.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.