Review, Reflect and Deflect

September 23, 2013 San Antonio

Thank you, Chris [Williston]. I am honored and delighted to speak to you all today. I understand that Danny King's daughter, Amy, arranged quite a songwriters' show for you last night. I heard it was so good that Ann Worthy, my head regulator at the Dallas Fed, stayed up past midnight … for the first time in 40 years.

I am going to start today by reviewing current banking trends for the nation and for the Eleventh Federal Reserve District.

Then, as there has been a great deal of reflection in the press and blogosphere on the occasion of the fifth anniversary of Lehman Brothers’ bankruptcy and the ensuing global financial crisis, I want to briefly provide you an overview of what the crisis cost us as a nation and the work remaining to prevent a reoccurrence of a crisis, a subject I will be addressing in a more fulsome manner in a speech and a public debate in New York in mid-October.

Last, I will comment briefly on last week’s FOMC meeting and what some have referred to as “the taper caper,” doing my utmost to deflect your criticism.

Texas’ Superior Bank Performance

First, let’s discuss how banks in the Eleventh Federal Reserve District are performing in the context of national trends. Recall that the district includes some 27 million people sprawled across approximately 360,000 square miles in southern New Mexico, Texas and the wooded north of Louisiana. Over 96 percent of the economic output and the district’s banking assets are in Texas, so you might reasonably say I am speaking of the performance of Texas banks versus banks in the U.S. as a whole.

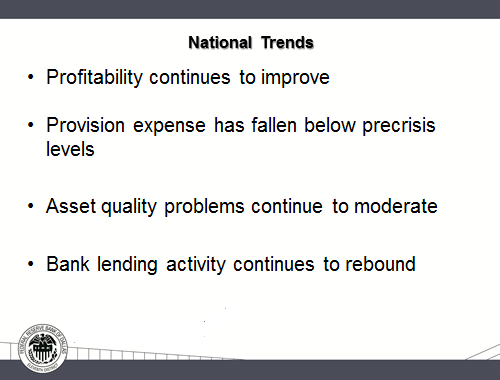

Profitability is fairly strong across the nation, helped in part by a continued decline in provision expense. Asset quality continues to improve, and lending activity continues to grow nationally. These national trends are consistent with what we have seen over the last several quarters.

You should take pride in knowing that Eleventh District and Texas banks are outperforming the rest of the nation’s banks.

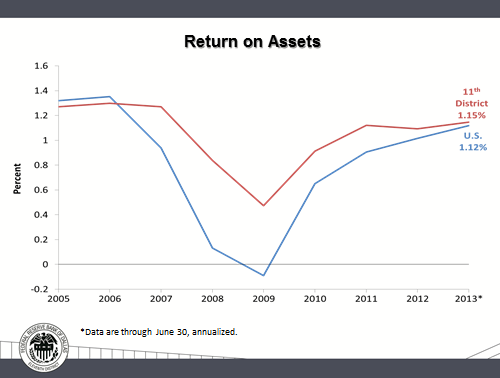

Let’s look at comparative return on assets (ROA):

Profitability trends over the last several years as measured by ROA show that district banks continue to outperform banks nationwide, with an ROA of 1.15 percent versus 1.12 percent for all U.S. banks.

While moving in the right direction, banks still have a little more work to do before their profitability reaches precrisis levels.

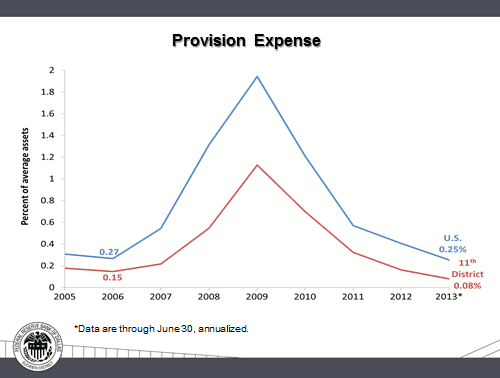

Provision expense is worth noting:

Falling provision expense has contributed to improved earnings trends for both U.S. and district banks. Declines in the amount banks set aside to cover bad loans have importantly contributed to improved profitability over the last several years. This, however, is not likely to be the case moving forward.

Banks nationwide and in the district are now reporting provisions below precrisis levels. In the case of our district banks, provision expense as a percentage of average assets is almost half of what was reported in 2006.

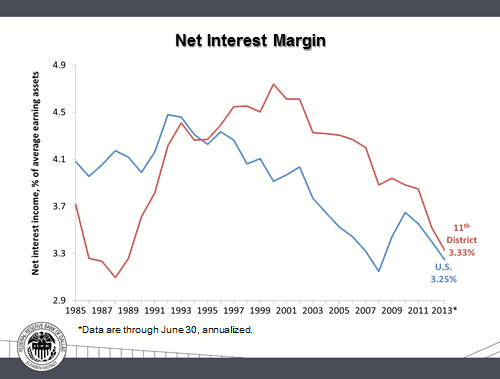

It doesn’t look like profitability is going to be bolstered much by net interest margin (NIM), either.

The NIM for banks across the U.S. has continued to trend lower over the past two decades; in the district, the trend has been observed over the past decade. It is noteworthy that the most recent decline in NIM is certainly affected by the zero lower bound on short-term interest rates.[1]

As you can see in this chart, district banks continue to report a slightly higher margin at 3.33 percent versus 3.25 percent for banks nationwide.

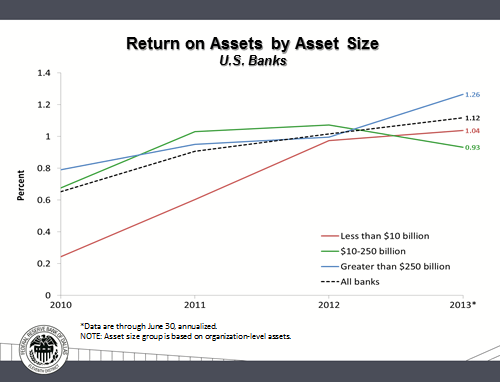

Now let’s look at how profitability differs nationally by bank asset size:

ROA has considerably improved in all size classes—banks with asset sizes of less than $10 billion and between $10 billion and $250 billion, and the largest banks, those with assets greater than $250 billion.

The upward trend in ROA tapers off by 2013 for community and midsize banks, while profitability for the dozen or so big banks—the cohort that includes banks considered “too big to fail” (TBTF)—shoots up rather dramatically. The Big Guys earned a ROA of 1.26 percent versus 1.04 percent for the community banks.

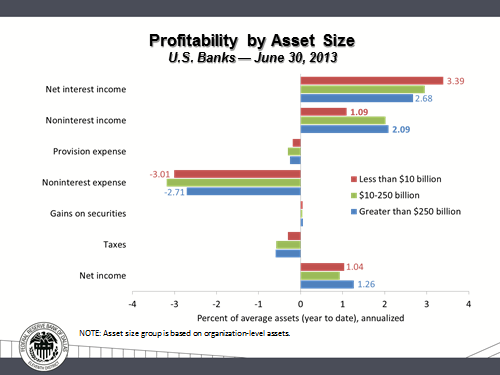

This chart shows the major profitability components for the asset size classes we just discussed:

Starting from the bottom up, you can see that the ROA for the biggest banks is 22 basis points above that for community banks. Recall that Eleventh District banks earned 1.15 percent ROA; thus, the Big Guys outpace even the relatively stronger performance of our healthy banks in and around Texas.

This gap is being driven by a couple of things: The largest banks have lower noninterest expense; some would say this is due to economies of scale. These Big Guys also recorded much higher noninterest income—a full 100 basis points higher. These two items were more than enough to offset the lower net interest income reported by the biggest banks.

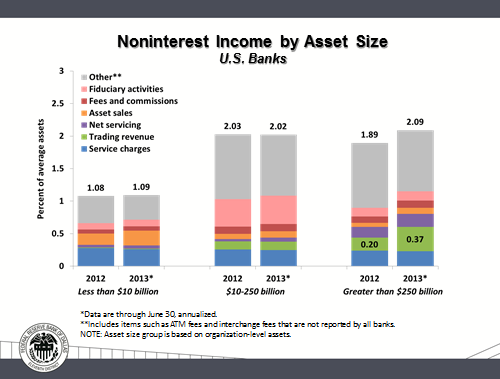

Having noted that big gap, let’s focus on the noninterest-income component for a minute and look at how it has impacted earnings trends for the Big Guys.

This chart shows noninterest income and its components for each of the three size classes of banks for 2012 and 2013.[2] As you can see, noninterest income was virtually unchanged for the community and midsize banks, while noninterest income has increased for the largest banks, from 1.89 percent of average assets in 2012 to 2.09 percent in 2013. Looking at the components of noninterest income, you can see that the growth has been driven by an increase in trading revenue.

Trading revenue is a noncore/nontraditional income source that is typically not available to community and the smaller midsize banks. It is thus more difficult for these smaller institutions to return to their historical norms or even compete in traditional lending with the Big Guys, whose lending activities, in a sense, are subsidized by their trading activities. We are receiving numerous reports from community and regional banks in the Eleventh District that the lending terms and standards of big banks are becoming increasingly lax.

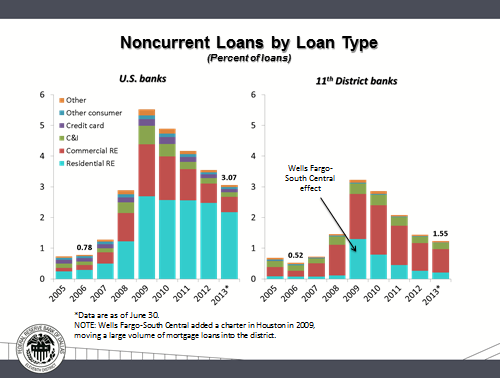

As you know, a common measure of asset quality is the noncurrent loan ratio, the percentage of a bank’s loans 90 or more days past due or on nonaccrual status. Here’s a comparison of noncurrent loans for U.S. versus district banks:

We’ve seen fairly dramatic improvement in asset quality over the last several years, with the noncurrent ratio declining to 3.07 percent for banks nationwide and 1.55 percent for those in the district. You can see from this chart that banks in Texas and the district continue to outperform banks nationwide.

Most of you remember the legendary Bob Hankins, who retired last year after 20 years as head of Banking Supervision at the Federal Reserve Bank of Dallas. Bob received an award last year at this very luncheon. He had a saying that Texas banks were “twice as good and half as bad” as banks nationwide. That remains the case, though banks around the U.S. are slowly catching up with Texas, and you can also see from the chart that banks here and in the U.S. still have some work to do to get noncurrent loans down to precrisis levels.

How about the so-called Texas ratio—a measure of noncurrent loans plus other real estate owned expressed as a percentage of equity plus loan loss reserves?[3] This became a scarlet letter in the late 1980s when 20 percent of Texas banks had a Texas ratio exceeding 100 percent. However, in 2013 only 0.7 percent of Texas banks had a Texas ratio greater than 100 percent, compared with 2.5 percent nationwide—and that nationwide number is down from a 5.7 percent peak in fourth quarter 2010.

Note what is labeled on the center right side of the chart as the “Wells Fargo-South Central effect.” Wells Fargo relocated a charter to Houston in 2009 and moved a large volume of mortgage loans into the district, triggering the increase in nonperforming residential real estate. (If the Wells Fargo-South Central effect is excluded from the 2009 data, the noncurrent loan ratio falls by 71 basis points for the district.)

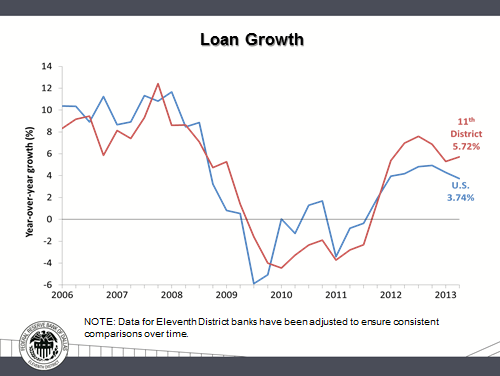

Now here is something I consider particularly noteworthy about our district: our loan growth and its composition.

Loan growth on a year-over-year basis remains good, but it decelerated a bit for the nation in the second quarter to 3.74 percent. In contrast, loan growth for district banks ticked up slightly to 5.72 percent, almost 200 basis points above the nationwide average.

Of interest, you can see from this multiyear chart that loan growth for banks nationwide hooks downward in the first half of 2013, while in the district, it turns upward.

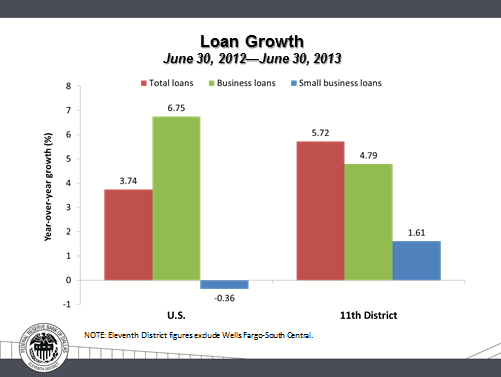

Here’s a closer look at loan growth between June of 2012 and 2013:

You can see in this chart how business loans contributed to total loan growth nationwide and in the district. Business loans grew 6.8 percent for banks nationwide and 4.8 percent for those in the district.

We do, however, continue to see pockets of weakness. Small-business lending was down 36 basis points year over year for banks in the U.S., while it increased only 1.6 percent districtwide.[4]

So let me summarize all of this:

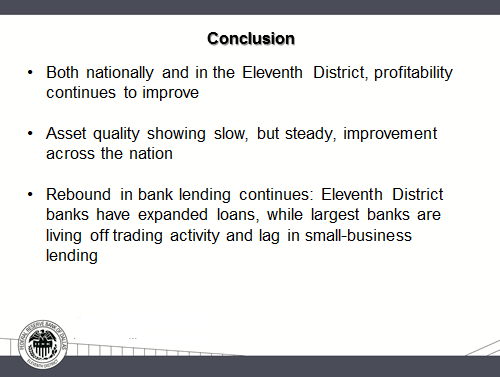

Profitability continues to trend upward, although when we will make it back to precrisis levels remains to be seen. Asset quality is improving, but there is more work to be done. Lending continues to rebound: We’ve seen seven consecutive quarters of growth nationwide. However, areas of weakness remain, particularly small-business lending.

The issue of small-business lending and the difference between the drivers of income for the largest banks and those with less than $250 billion in assets is a reminder of a lingering problem: The coddling, whether intentionally or otherwise, of the biggest of the big banks—those considered too big to fail.

Five Years After Lehman, We Still Have a Big Problem

Working with Harvey Rosenblum and my colleagues at the Dallas Fed, I have been a constant burr under the saddle of the too big to fails. In a nutshell, I believe that the megabanks are inherently handicapped by their size and scale in practicing the basic principle of banking: Know your customer. Extreme size and complexity have proven to be the enemy of prudence and the source of costly mistakes. Mathematically based risk-management models, while theoretically comforting, have their deficiencies. We learned during the recent crisis just how perilous those deficiencies can be.

We at the Dallas Fed believe, based on the experience of the last five years, that the largest financial institutions are a dagger pointed at the heart of our economy. We are not alone. Even the local paper in the denizen of the megabanks, the New York Times, recently editorialized regarding the controversies surrounding JPMorgan Chase: “The underlying problem is not only this or that violation, but the fact that the sheer size and scope and complexity of the banking behemoths defy controls, encouraging speculation and bad behavior.”[5]

We at the Dallas Fed would add that they undermine free-market capitalism and jeopardize our economic welfare. But we would note that it is unfair to single out JPMorgan Chase as a culprit. It is only one of a set of megabanks that remain a threat to financial stability. Indeed, Bob Diamond, the former head of the megabank Barclays, recently warned in a Financial Times op-ed that additional steps are needed “if we are to avoid the kind of capital regulatory arbitrage that weakened the financial system.”[6]

And on Friday, the Wall Street Journal’s lead editorial said: “The policy of too big to fail has been codified and expanded. Dodd–Frank lets Washington’s wise men define ‘systemically important’ institutions subject to stricter regulation … [But] Dodd–Frank’s … great conceit is that in a crisis these firms will be wound down without a rescue. They even have to provide ‘living wills’ that are supposed to plan the funeral. But the law also gives regulators the freedom to protect creditors as they see fit, which they will surely do in a panic. The difference next time will be that more firms will be deemed too big to fail.” The Journal’s editorial highlighted this in bold print: “The financial system is more regulated than ever, but also no safer.”[7]

It would appear that the editors of these three great newspapers have been reading my speeches and Congressional testimony! They seem to agree with me and Harvey that TBTFs or “systemically important financial institutions” (SIFIs) might easily again play the nefarious role they did five years ago in bringing down our economic and financial system. (The acronym SIFI sounds like some kind of communicable disease transmitted through reckless behavior. In the event of another crisis brought on by the behavior that SIFIs still appear to have leeway to engage in, my guess is the acronym would come to stand for “Save If Failure Impending”).

Am I exaggerating when I say that the TBTFs are a dagger pointed at the heart of the economy?

To be sure, there were many causes and tripwires for the financial debacle from which we are still struggling to recover—a debacle that we at the Dallas Fed estimate cost more than an entire year’s worth of U.S. economic output, or more than $120,000 per American household.[8] Among those causes and tripwires were the unbridled advent of toxic forms of structured finance, complicity by the ratings agencies, and even the Fed’s own role: keeping interest rates too low for too long, rebuffing Fed Governor [Edward] Gramlich’s attempts to regulate subprime lending, and blessing the increased consolidation of banking.

As my Dallas Fed colleague, John Duca, gently reminds me, there was more than a little “we have met the enemy and he is us” that contributed to the perfect storm of forces that led our economy into that frightful and costly tailspin.[9]

But still, the TBTF behemoths were indisputably what the Bank of England’s Andy Haldane called “super-spreaders” of the virus that brought our financial system and economy to its knees.[10] They retain that potential today. For in the aftermath of the crisis and the passage of Dodd–Frank, the giants have gotten bigger, and the profitability of the community and regional banks that might pose meaningful, healthy competition has been undermined by the legislation’s complexity.

Dodd–Frank claims to end TBTF. Instead, as the Wall Street Journal editorialized, it entrenches the TBTF pathology. The megabanks remain a potential lethal force. As mentioned, I will be speaking at length on this subject in New York in October.

A Deliberate Deflection

As I said at the beginning of my remarks, I am going to try to avoid answering questions you might have about last week’s FOMC meeting and what some in the press have now labeled “the taper caper.” Nearly every Federal Reserve Bank president and his or her sister will be speaking to this topic this week, so you will be getting an earful of cacophonous comments on this subject.

Today, I will simply say that I disagreed with the decision of the committee and argued against it. Here is a direct quote from the summation of my intervention at the table during the policy “go round” when Chairman [Ben] Bernanke called on me to speak on whether or not to taper: “Doing nothing at this meeting would increase uncertainty about the future conduct of policy and call the credibility of our communications into question.” I believe that is exactly what has occurred, though I take no pleasure in saying so.

Enough said. Thank you for what you do for the business and citizens of Texas. And thank you for listening.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- Since banks borrow short-term funds from depositors and lend for longer terms, the gap between interest earned on loans and interest paid to depositors typically benefits from a steep yield curve, or the difference between the yields on the 10-year Treasury bond and the three-month Treasury bill.

- “Trading revenue” represents the net gains/losses from trading cash instruments and derivative contracts.

- The “Texas ratio” is defined as the ratio of loans past-due 90 days or more, nonaccrual loans, and other real estate owned relative to equity capital, plus loan loss reserves, less intangibles.

- “Small-business loans” are commercial and industrial loans and loans secured by nonfarm nonresidential property, with original amounts of $1 million or less.

- “Chasing JPMorgan Chase,” New York Times, Sept. 2, 2013, p. A16.

- “Bob Diamond Calls for Bank Rules Shake-up,” by Tom Braithwaite and Patrick Jenkins, Financial Times, Sept. 16, 2013, p. 1.

- “The Government Won on Financial Reform,” Wall Street Journal, Sept. 20, 2013, p. A14.

- “Assessing the Costs and Consequences of the 2007–09 Financial Crisis and Its Aftermath,” by David Luttrell, Tyler Atkinson and Harvey Rosenblum, Federal Reserve Bank of Dallas Economic Letter, vol. 8, no. 7, 2013, www.dallasfed.org/research/eclett/2013/el1307.cfm.

- Cartoonist Walt Kelly’s satire cartoon Pogo coined this phrase as a parody of a message sent from U.S. Navy Commodore Oliver Hazard Perry to Army General William Henry Harrison after the 1813 Battle of Lake Erie: “We have met the enemy, and they are ours.”

- See “The Birds and the Bees, and the Big Banks,” by Andrew Haldane and Robert May, Financial Times, op-ed, Feb. 20, 2011.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.