Excerpts From "A Conversation About Longhorns, Longnecks and Liquidity: The Economy and the Course of Monetary Policy"

February 21, 2014 Austin, Texas

This is a major theme of my remarks here today. No, not longnecks or other free-flowing libations specifically, but the concept that too much liquidity can be a very dangerous thing. William McChesney Martin, the longest-serving Fed chairman in our institution’s 100-year history, famously said that the Fed’s job is to take away the punchbowl just as the party gets going.

… In the remainder of my time with you here today, I will speak briefly about the operations of the Dallas Fed and of the other 11 Federal Reserve Banks. Then I am going to comment on the Texas economic recovery and speak extemporaneously on recent policy decisions taken by the Federal Open Market Committee (FOMC). Finally, I am going to make a brief comment on the depth of the punchbowl of liquidity the Fed has created, the reason I have advocated removing it, and the sobering reality of the fiscal folly of our lawmakers in Washington, D.C.

… For far too long, the greatest obstacle to the nation’s economic prosperity has resided here:

A straight-talker with a little salt on his tongue might be tempted to say: “It is fiscal policy that is leading to the Californication of our national economy rather than its Texification.” But I would not say anything so crude, so I am not going to say it. Instead, I’ll invoke an editorial in a recent Financial Times that said it more politely: “Fiscal policy is still not an ally of U.S. growth.”

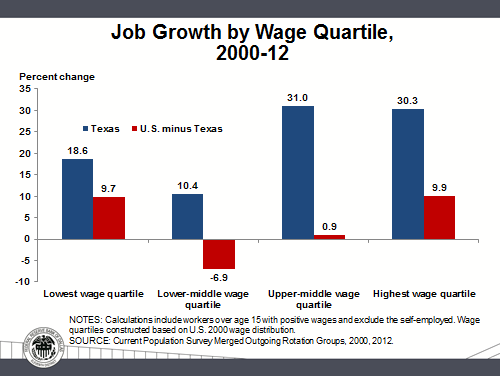

This is a picture of the gaping hole in the heart of our nation’s prosperity: If you remove the job-creating machine of Texas from the U.S. economy, the nation has experienced job destruction that has occurred over the past 12 years in the middle-income quartiles.

I never refer to “classes”; I do not believe status in a democracy should be defined by the hidebound concept of “classes.” But no matter: The most vital organ of our nation’s economy—the middle-income worker—is being eviscerated.

This is the pathology I worry most about. So I ask: Can my colleagues and I at the Fed cure this with monetary policy? Obviously, businesses cannot create jobs without the means for investing in job-creating expansion, so, yes, monetary policy is necessary to propel job creation.

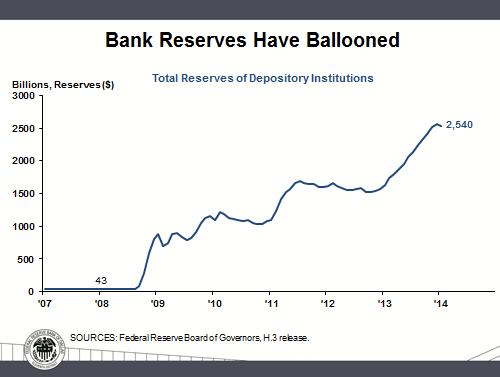

But as I have shown this afternoon, the store of bank reserves awaiting discharge into the economy through our banking system is vast, yet it lies fallow. Take a look at this chart of total reserves of depository institutions: They have ballooned from a precrisis level of $43 billion to more than $2.5 trillion.

Here is the point: There is plenty of money available for businesses to work with. Consider this: In fourth quarter 2007 the nation’s gross domestic product (GDP) was $14.7 trillion; at year-end 2013 it was estimated to be $17.1 trillion. Had we continued on the path we were on before the crisis, GDP would currently be roughly $20 trillion in size. That’s a third larger than it was in 2007. Yet the amount of money lying fallow in the banking system is 60 times greater now than it was at year-end 2007. One is hard pressed to argue that there is insufficient money available for businesses to put people back to work.

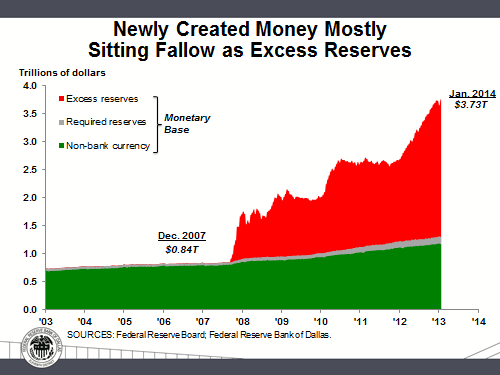

Now, bear in mind that we at the Fed only control the monetary base (cash plus bank reserves), not the velocity with which money is used. Again, consider this graph:

Over the past six years, the monetary base has increased 340 percent, 10 times the rate at which the economy would have expanded in nominal terms had we not suffered the recent recession. One is hard pressed to argue that there is much efficacy derived from additional expansion of the Fed’s balance sheet. This is why I’ve been such a strong proponent of dialing back our large-scale asset purchases and will continue advocating that we do so.

It is my firm belief that the fault in our economy lies not in monetary policy but in a reckless and feckless federal government that simply cannot get its fiscal and regulatory policy geared so as to encourage business to take the copious amount of money we at the Fed have created and put it to work creating jobs and growing our economy. Fiscal policy is not only “not an ally of U.S. growth,” it is its enemy. If the fiscal and regulatory authorities that you elect and put into office to craft taxes, spending and regulations do not focus their efforts on providing incentives for businesses to expand job-creating capital investment rather than bicker with each other for partisan purposes, our economy will continue to fall short and the middle-income worker will continue being victimized, no matter how much money the Fed puts into the system.

I don’t want to ruin your lunch after such pleasant talk of longnecks and liquidity, but if you wish to know who is at fault for hollowing out the welfare of middle-income workers and the American economy, kindly do not look at me or my colleagues at the Fed. When you go home or take a break during today’s conference, look at yourself in the mirror, for you elect our fiscal and regulatory policymakers. Many of you give money to finance the campaigns of candidates from out-of-state: Texas is a treasure trove of campaign finance for both Republicans and Democrats running for national office. We at the Fed are providing more than enough monetary accommodation. It is time for fiscal policymakers to do their job, to ally themselves with us to achieve a fully employed, prosperous America.

In addition to being proud Longhorns and prosperous Texans, be bold Americans. Only you, as voters, have the power to insist that our lawmakers craft policies that are needed to restore American prosperity. Please do so.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- See “Report: Texans Drink a Lot of Beer—34.4 Gallons per Person in 2012,” by Tiney Ricciardi, Dallas Morning News, July 9, 2013.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.