Banking Conditions Survey

Strong Increases Seen in Loan Volume Growth, Though Future Expectations Fall

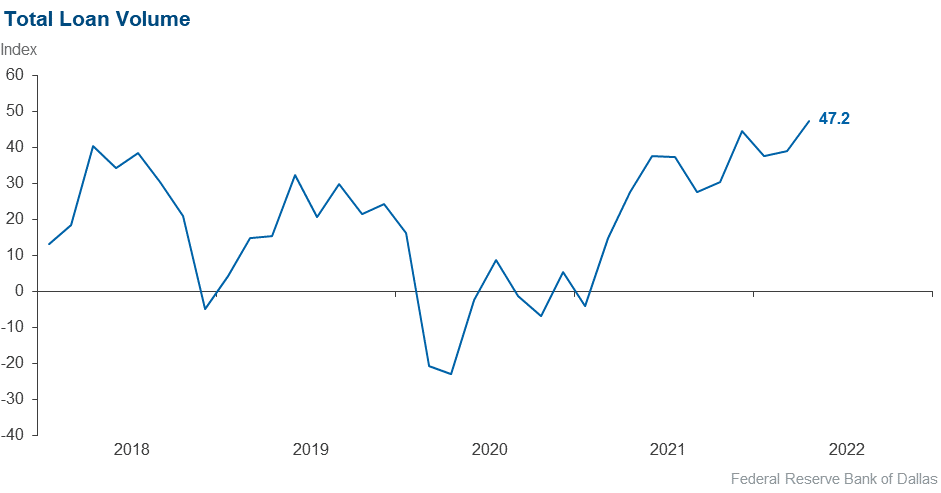

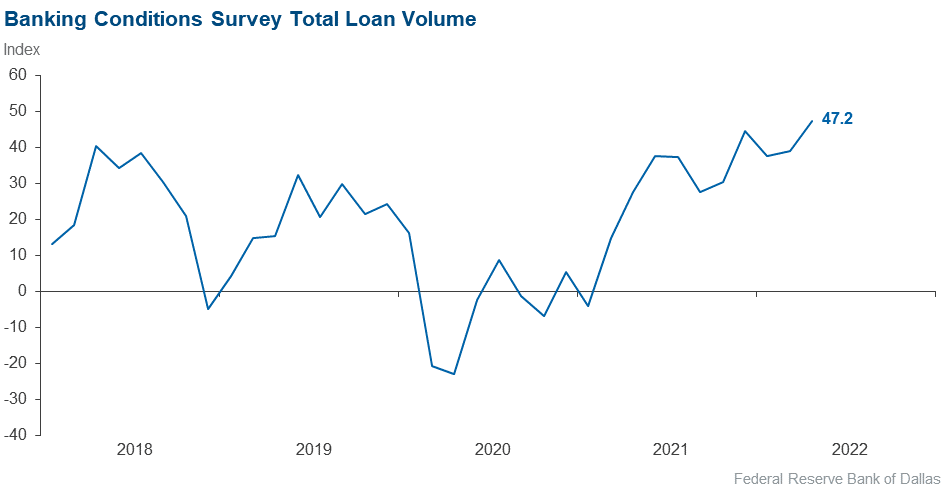

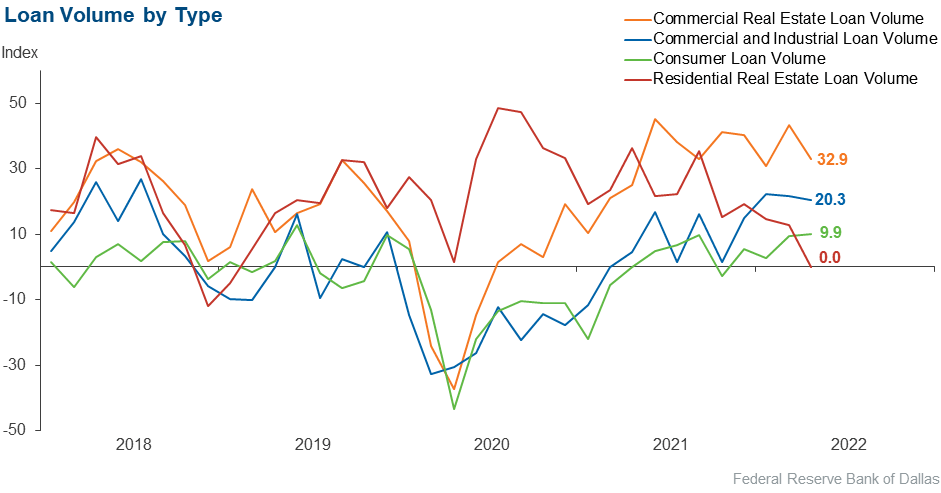

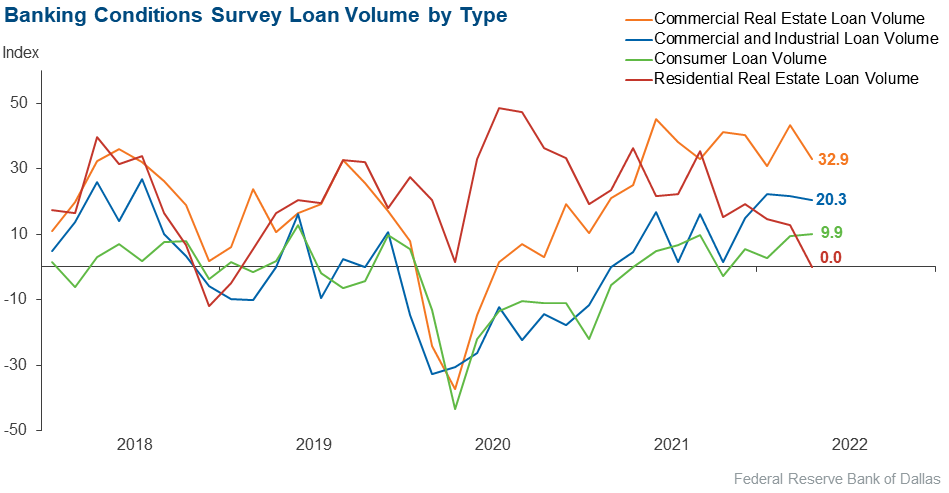

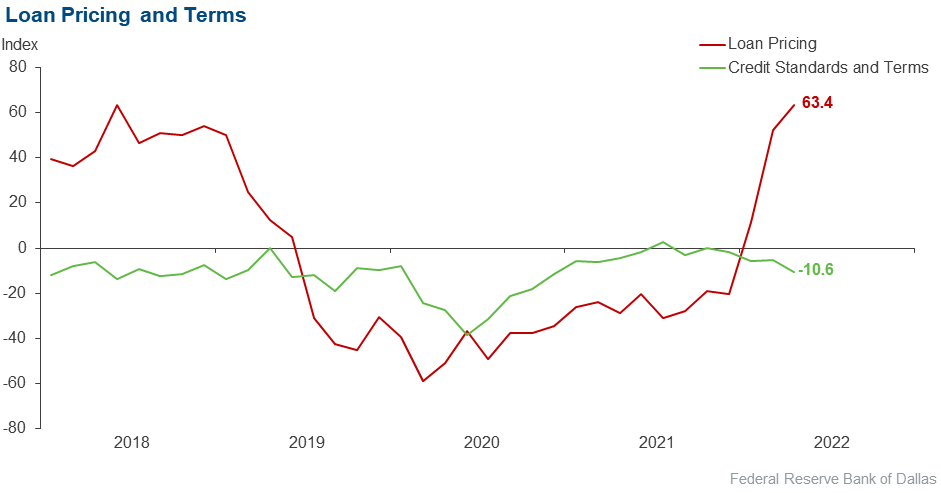

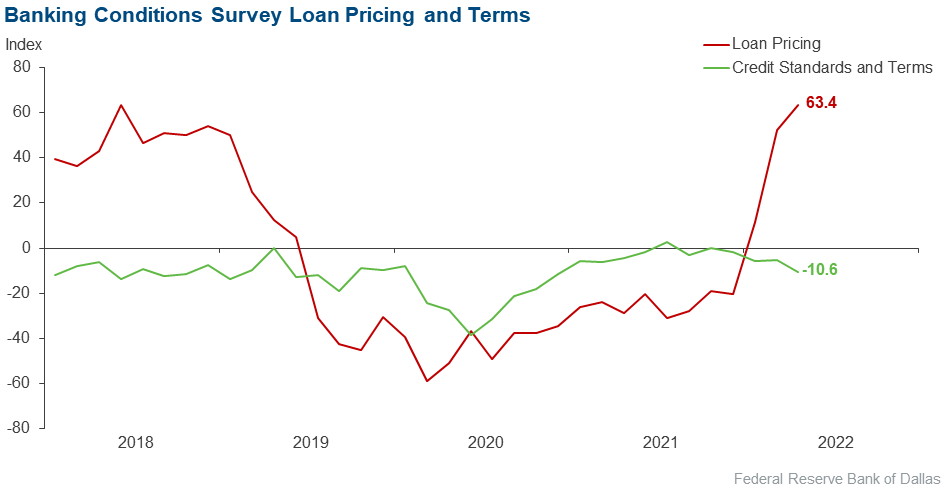

Loan volume grew over the past six weeks amid broad increases in loan pricing. This growth was the fastest since the survey began in 2017. Loan volume growth spanned lending types with the exception of residential real estate, which saw no change in loan volumes over the last six weeks. Nonperforming loans continued to decrease, and credit standards and terms tightened further. Looking six months ahead, contacts expect that general business activity and loan demand will decrease, and nonperforming loans will increase.

Next release: June 27, 2022

Data were collected May 3–11, and 72 financial institutions responded to the survey. The Federal Reserve Bank of Dallas conducts the Banking Conditions Survey twice each quarter to obtain a timely assessment of activity at banks and credit unions headquartered in the Eleventh Federal Reserve District. CEOs or senior loan officers of financial institutions report on how conditions have changed for indicators such as loan volume, nonperforming loans and loan pricing. Respondents are also asked to report on their banking outlook and their evaluation of general business activity.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease (or tightening) from the percentage reporting an increase (or easing). When the share of respondents reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior reporting period. If the share of respondents reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior reporting period. An index will be zero when the number of respondents reporting an increase is equal to the number reporting a decrease.

Results Summary

Historical data are available from March 2017.

| Total Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 47.2 | 39.1 | 63.9 | 19.4 | 16.7 |

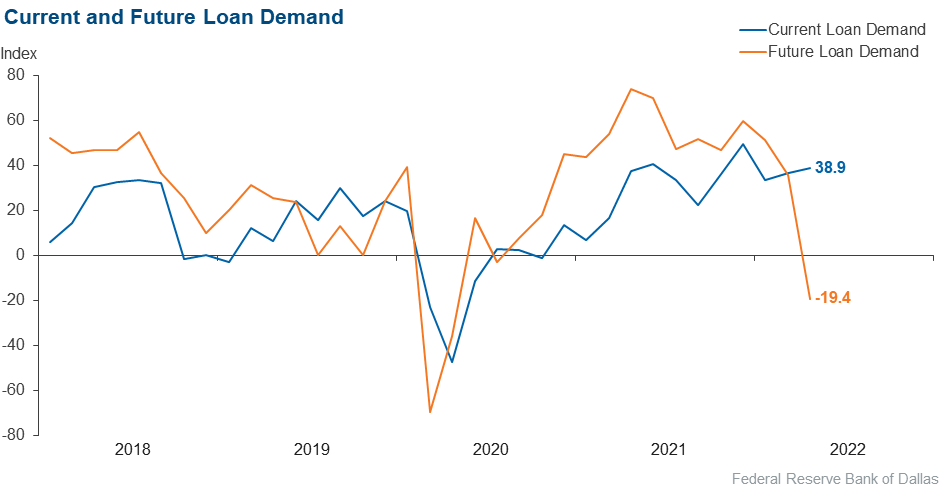

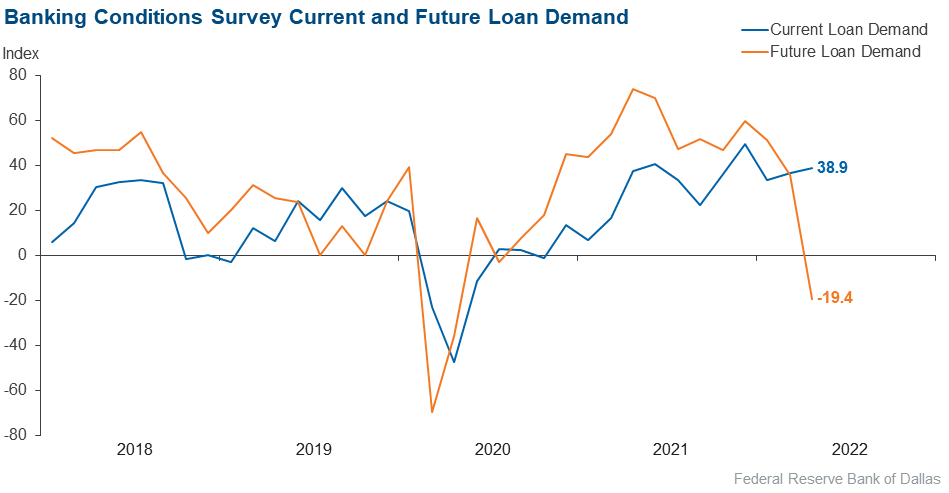

Loan demand | 38.9 | 36.5 | 52.8 | 33.3 | 13.9 |

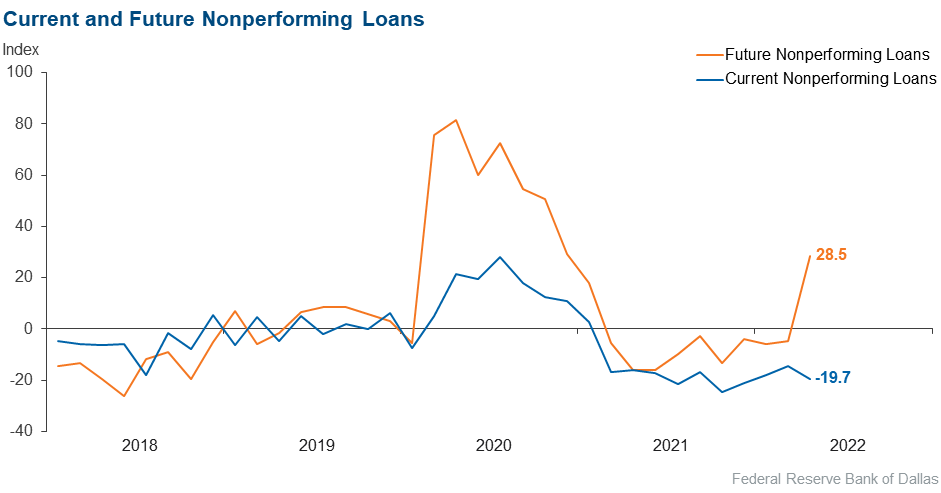

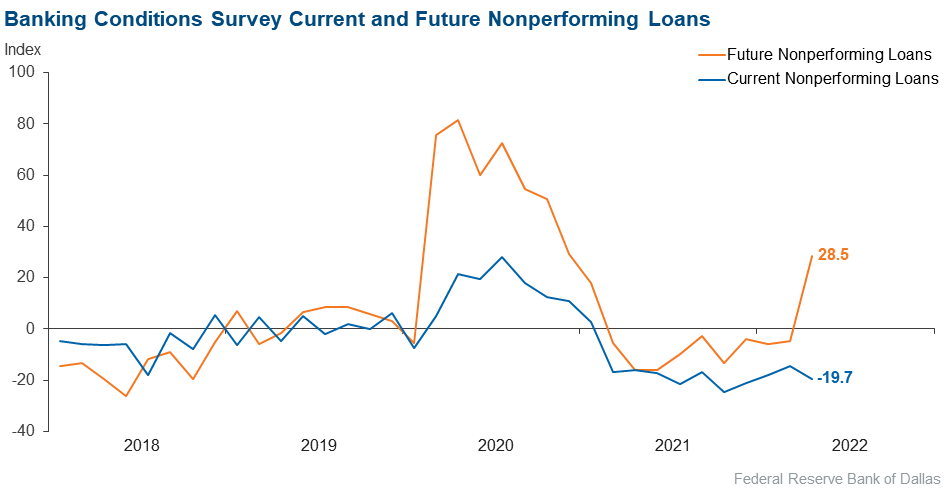

Nonperforming loans | –19.7 | –14.3 | 4.2 | 71.8 | 23.9 |

Loan pricing | 63.4 | 52.4 | 69.0 | 25.4 | 5.6 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –10.6 | –5.1 | 3.0 | 83.3 | 13.6 |

| Commercial and Industrial Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 20.3 | 21.7 | 30.4 | 59.4 | 10.1 |

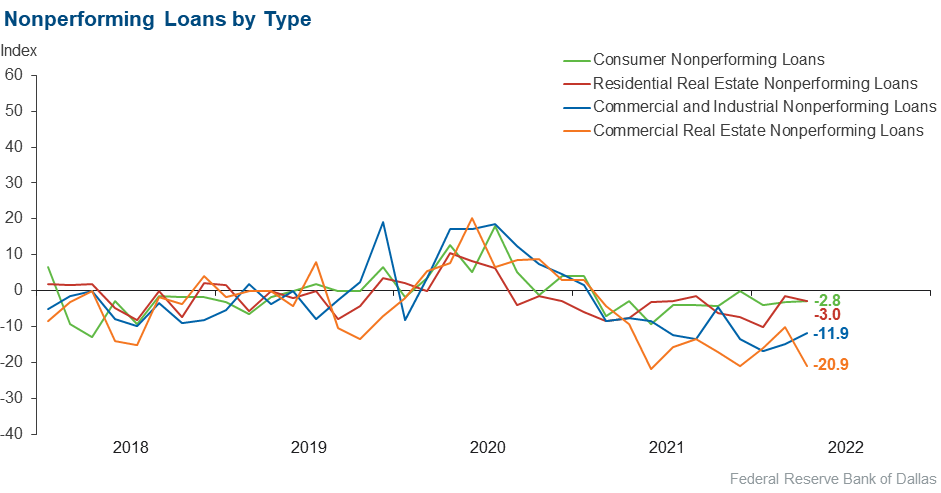

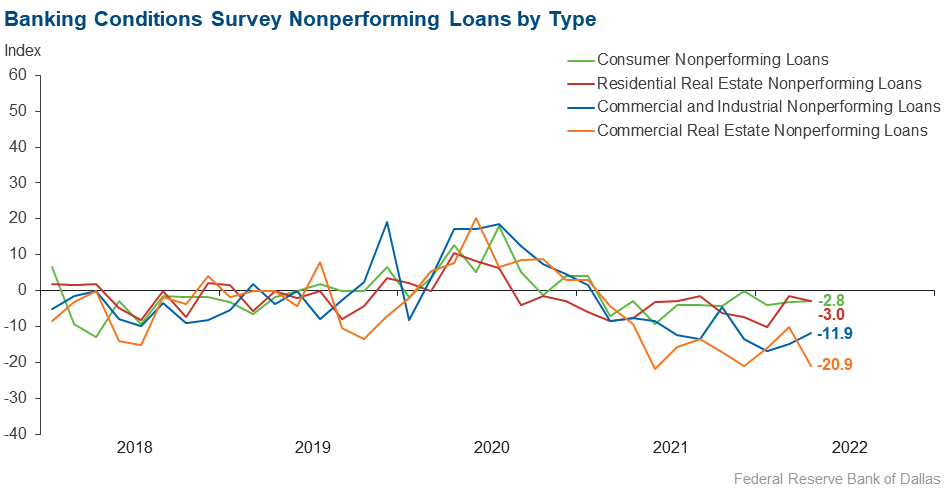

Nonperforming loans | –11.9 | –15.0 | 3.0 | 82.1 | 14.9 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –7.7 | –5.0 | 1.5 | 89.2 | 9.2 |

| Commercial Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 32.9 | 43.4 | 44.8 | 43.3 | 11.9 |

Nonperforming loans | –20.9 | –10.2 | 1.5 | 76.1 | 22.4 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –5.9 | –1.7 | 4.5 | 85.1 | 10.4 |

| Residential Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 0.0 | 12.9 | 34.3 | 31.3 | 34.3 |

Nonperforming loans | –3.0 | –1.6 | 6.0 | 85.1 | 9.0 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –4.5 | 0.0 | 0.0 | 95.5 | 4.5 |

| Consumer Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 9.9 | 9.5 | 28.2 | 53.5 | 18.3 |

Nonperforming loans | –2.8 | –3.3 | 4.3 | 88.6 | 7.1 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –2.9 | 1.6 | 1.4 | 94.3 | 4.3 |

| Banking Outlook: What is your expectation for the following items six months from now? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Total loan demand | –19.4 | 35.9 | 26.4 | 27.8 | 45.8 |

Nonperforming loans | 28.5 | –4.8 | 31.4 | 65.7 | 2.9 |

| General Business Activity: What is your evaluation of the level of activity? | |||||

| Indicator | Current Index | Previous Index | % Reporting Better | % Reporting No Change | % Reporting Worse |

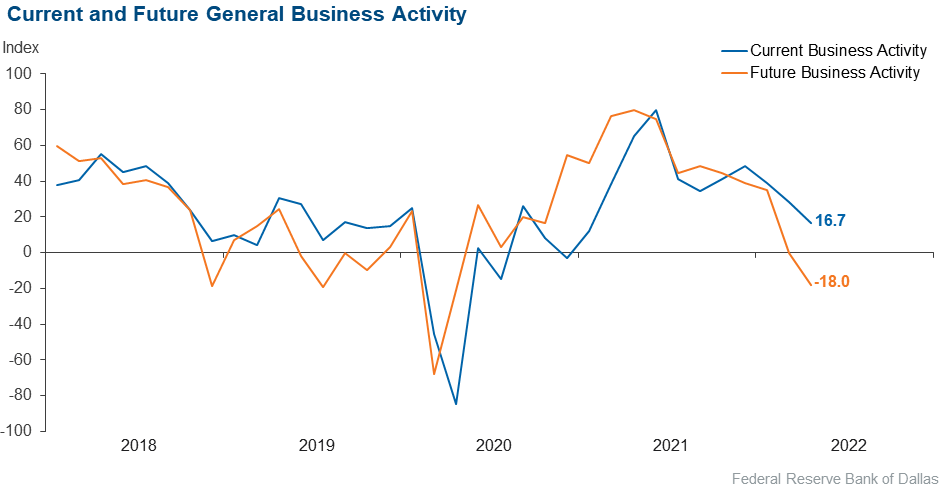

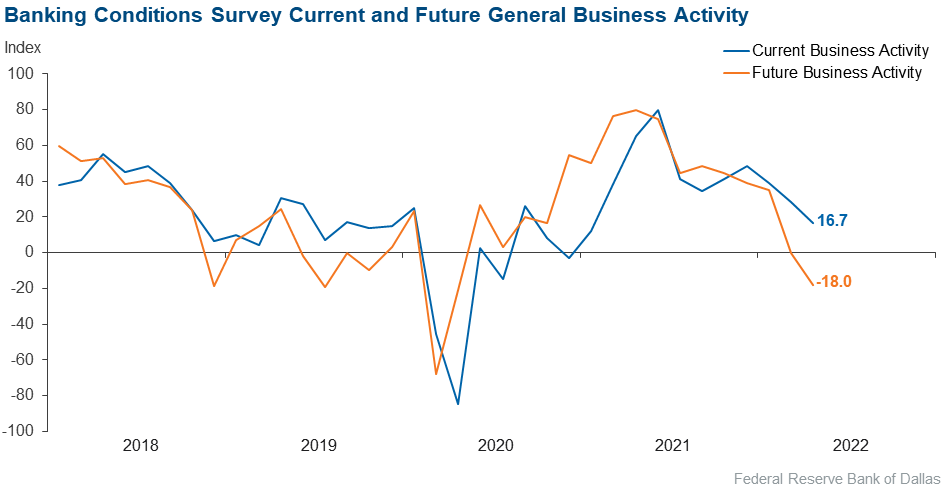

Over the past six weeks | 16.7 | 28.1 | 37.5 | 41.7 | 20.8 |

Six months from now | –18.0 | 0.0 | 27.8 | 26.4 | 45.8 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Comments from Survey Respondents

Respondents were given an opportunity to comment on any issues that may be affecting their business.

These comments are from respondents’ completed surveys and have been edited for publication.

- There is still strong commercial real estate activity in the face of rising interest rates and higher costs. Projects will require increasing (trended) rents to make economic sense.

- We have had an increase in farm/ranchland and residential loans. We expect a decrease in demand due to rising rates.

- We believe we will be in a recession in the second half of 2022.

- Inflation appears to be affecting businesses and consumers. Businesses still report some supply-chain constraints. We are watching the Fed [Federal Reserve] to see what actions are going to be taken and how those affect the economy.

- We have seen an uptick in loan demand, while our deposit levels have declined, and most bonds in our portfolio are carried at unrealized losses. As such, we have increased our attention and consideration to our secondary liquidity sources to fund the rising loan demand.

- Rising input costs including labor are pressuring commercial and industrial clients along with ongoing supply-chain issues. The Wall Street Journal ran a recent article on how even Amish furniture makers are experiencing supply-chain issues and volatile lumber prices. Commercial real estate borrowers are rushing to try and lock in rates. Interchange and card transactions indicate changing consumer behavior as well.

- South Texas could enjoy an economic boom due to several factors. First, the Biden administration has made a commitment to Europe to expand our LNG [liquefied natural gas] shipments to them. South Texas is in a position to provide the extra gas needed to replace Russian gas. Secondly, South Texas is seeing an increase in drilling for natural gas, which puts a lot of people back to work. The one headwind is a lack of employees who want to go back into oil and gas.

- We are beginning to see some trending, possibly indicating the impact of rising rates and volatility in markets impacting members/business activity. When combined with forecasts for interest rates, increasing complexity/burden of regulations and continued supply/demand imbalances for purchasing homes, autos, etc., a collective increase in uncertainty of the economic and business path forward exists.

- We are seeing high inflation, high oil and gas prices, Ukraine–Russia war, high real estate prices and rising interest rates.

- Continued inflation, expected interest rate increases from the FOMC [Federal Open Market Committee], supply-chain issues and a reduction in the money supply are creating very uncertain times and making it difficult to plan long term.

- The current administration's view on the economy, inflation and governmental spending is concerning.

Historical Data

Historical data can be downloaded dating back to March 2017. For the definitions, see data definitions.

NOTE: The following series were discontinued in May 2020: volume of core deposits, cost of funds, non-interest income and net interest margin.

Questions regarding the Banking Conditions Survey can be addressed to Emily Kerr at emily.kerr@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Banking Conditions Survey is released on the web.