Opportunity Zones: How will we know if communities reap the benefits?

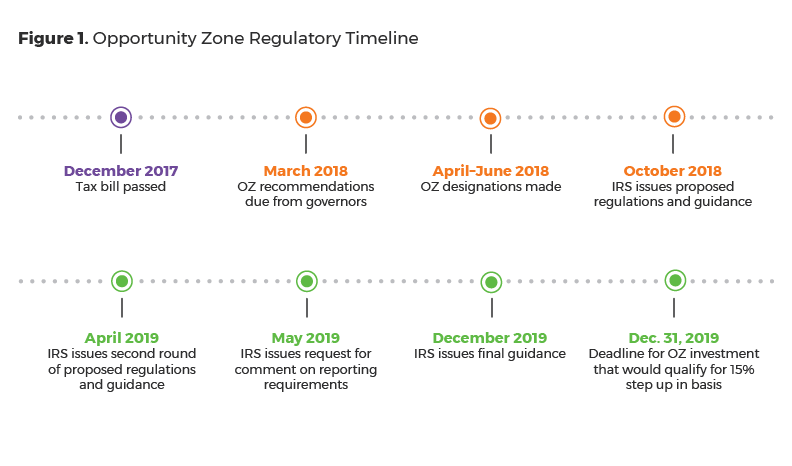

Much has happened since the Dallas Fed released its first article on Opportunity Zones (OZs), a tax-incentive tool built into the Tax Cuts and Jobs Act of 2017 to spur investment in low-income communities. In the past 15 months, the IRS has released three rounds of guidance (Figure 1), while the Treasury Department and other federal entities have solicited requests for comment on how best to implement OZs.

While we know a lot more than we did, some aspects of OZs remain unclear. High on the list of ongoing concerns are questions about reporting requirements. Community organizations, researchers and investors are all asking: Will Opportunity Zone investments be tracked? Will information about OZ projects, whether real estate or business focused, be shared with the public? Ten years from now, will we have the metrics available to understand the outcomes of OZ investments in our communities?

Guidance: What more do we know?

Here is what has happened over the past 15 months:

First round

The IRS released the first set of proposed regulations on OZs in October 2018. This guidance clarified some basic information on investments, including:

- Taxes on the original capital gain are due no later than Dec. 31, 2026.

- There is a 180-day grace period, starting from the day on which the gain is required to be recognized (if not deferred), for a gain to be transferred to a Qualified Opportunity Fund (QOF).

- If an investment is made in a QOF by June 29, 2027, and held for at least 10 years, investors can get the full OZ benefit through the end of 2047.

This first round of proposed regulations clarified some important concepts, but many questions remained, particularly regarding business investment. Start-up business investment and job creation were two ideas at the heart of OZs, as conceptualized by the Economic Innovation Group (EIG), a Washington, D.C.-based research and advocacy organization.

According to Rachel Reilly, EIG’s director of impact strategy, a central purpose of OZs was equity for new businesses, which are responsible for the majority of net job creation in the country. “For early-stage entrepreneurs, sources of capital are very weak and especially absent from distressed communities, many of which are now designated Opportunity Zones,” she says. Reilly says this capital infusion in turn could “provide an economic base for distressed communities that feels more self-sufficient.”

However, the emphasis of the October guidance did not provide specifics regarding business investment, which meant that most of the conversation among investors and developers focused on real estate. “Real estate was better positioned to react to the original guidance and participate in those discussions,” she says. “However, Treasury and the IRS made significant improvements in the final regulations to facilitate increased levels of business investment.”

Second round

The second round of regulations, released in April 2019, shed light on how business investment can qualify:

An investment qualifies if the business meets any of the following requirements:

- At least half of all employees’ work time is spent in an OZ.

- At least half of all employees’ compensation occurs in an OZ.

- Management and operations are based in an OZ.

- At least half of gross income is derived from business conducted in an OZ.

These clarifications have opened up multiple avenues for businesses to benefit from OZs.

For example, in the case of a start-up firm manufacturing children’s toys: If the headquarters (management and operations) were located in an OZ, an equity investment in this business would qualify. If the headquarters were outside an OZ, an investment could qualify if the factory producing the toys were in an OZ, provided at least half of all hours worked took place in the factory. If the factory were outside an OZ, but the highest-paid staff members had offices in an OZ, an investment would still qualify if compensation in the OZ accounted for at least half of total compensation.

These clarifications have made it easier for businesses to take advantage of the tool. After these rules were released, multiple federal agencies entered the arena. The Small Business Administration and the Economic Development Administration offered competitive grants and prioritization of work that focuses on OZs.

Third round

A final update came on Dec. 19. These regulations clarified some time horizons, doubled the working-capital safe harbor window for start-up businesses, and made it a lot easier to invest in the cleanup of brownfields, areas where environmental contamination is a concern.

Reporting and tracking: an outstanding issue

Among the issues flagged in our 2018 article was a lack of OZ reporting requirements. At that time, there had been no discussion at a federal level about tracking QOF investments. When Congress empowered the Treasury to create QOF regulations, it did not indicate the need for data collection on the size, type or outcome of any such investment. In fact, the IRS initially required only that a taxpayer (organized as a corporation or partnership) self-certify on a one-and-a-half page form (8996) to operate as a QOF.

In May 2019, the Treasury issued a request for information, soliciting feedback on how best to collect data on OZ investments. Seven months later, the IRS released a new draft of its form, extending the process by collecting an additional two pages of information, specifically on location and value of investments in business properties in OZs.

Some feel the form will not go far enough. The EIG’s Reilly suggests that the modest IRS reporting standards will likely not be sufficient to evaluate the program’s impact, adding that the IRS and Treasury may not be able to go further with data collection under current law. She says that EIG continues to “urge Congress to take a bipartisan approach to developing a framework.”

Tighter reporting and tracking standards may indeed be gaining traction in Congress with the introduction of multiple bills in the House and Senate. A November 2019 bill, S. 2787, goes the furthest in terms of required reporting and transparency; it mandates public disclosure of all QOFs, asset sizes, and types and locations of investments, and revisits original tract designation criteria. This particular bill was introduced amid accusations that certain OZ projects were benefiting wealthy, politically connected investors rather than low-income communities.

S. 2787 does not presently show the bipartisan support that the original OZ legislation enjoyed. “From our perspective, a reporting framework will have to balance a few things,” Reilly says. “First, the need to provide transparency and evaluation of impact is important. Second, we need to be cautious in transferring onerous reporting requirements to businesses to the extent that it impedes their ability to grow.”

She says that having transparent reports on investment activities is necessary for states and communities to be responsive to the market and to ensure there are guardrails against abuse. But some proposed bills could burden operating businesses with day-to-day reporting. Reilly is hopeful that a balance can be achieved: “There is bipartisan agreement that reporting requirements need to be in place. It’s just how to get there, and what it includes, that is the discussion of the day.”

About the author

Emily Ryder Perlmeter is a policy analyst in the Integrated Policy Department at the Federal Reserve Bank of Dallas. She was formerly a senior advisor in the Community Engagement and Development Department.