New Era for Payday Lending: Regulation, Innovation and the Road Ahead

With the creation of the Consumer Financial Protection Bureau (CFPB) under the Dodd–Frank Act in 2010, lenders who offer payday loan products fall under the direct supervision of a federal regulatory authority. As we move forward into this era of federal oversight of payday loans and other small-dollar loan products, there is a critical need for creative collaboration between the private, not-for-profit and financial technology (fintech) sectors in order to effectively serve the financial needs of low- and moderate-income (LMI) individuals. While each of these industry sectors has seen success in the past, data indicate that it is only through meaningful cooperation and innovation that we will be able to address the issue of LMI individuals’ lack of access to affordable small-dollar credit products with customer protections.

What Is a Payday Loan?

A payday loan is a short-term loan, generally $500 or less, that is normally due on the borrower’s next payday.[1] Most payday loans, regardless of the lender, share certain key features:

- Are for small amounts,

- Are due within two weeks or on the consumer’s next payday,

- Require the borrower to give the lender access to their checking account or provide a check in advance for the full balance that the lender can deposit when the loan becomes due; and

- Are usually offered without a true verification of the borrower’s ability to repay or a credit check.

Payday loans can also be installment based and have rollover and/or renewal options. Annual percentage rates (APRs) on these loans can range from double-digit, near-prime rates to as high as 800 percent. In Texas, APRs average over 600 percent for these types of loans.[2]

For many consumers, payday loans have served as a source of added means during times of financial hardship. While these high-cost loans do provide individuals with a temporary source of immediate funds, they also trap many people in a debt cycle. Borrowers usually qualify easily and are approved for these loans, then are later surprised by the unexpected financial burdens that result from their decision to access this form of credit.

Why Are Payday Loans Used?

Many borrowers see payday loan products as their only means of survival during periods of financial hardship. According to the Center for Financial Services Innovation (CFSI), most people use payday loans to cover unexpected expenses, misaligned cash flow, planned purchases or periods where they have exceeded their income. In a CFSI survey, 67 percent of borrowers cited one of these reasons as the primary driver for their payday loan usage, while the remaining one-third of borrowers cited two or more reasons. Most survey respondents identified unexpected expenses and exceeding their income as the leading causes for their use of this type of credit.[3]

The Cycle of Debt

Payday loans are characterized by their high fees. For most borrowers, the loan amount itself does not pose a challenge to repayment; rather, it is the fees charged by the lender that so often consume them in an unending cycle of debt. When consumers are unable to pay off their loan, they are usually forced to pay outstanding fees and interest to keep the loan out of default status. With limited access to other sources of capital, these individuals find themselves stuck in a cycle of paying fees and interest while never actually paying down the principal balance on the loan.

Payday Lending in Texas

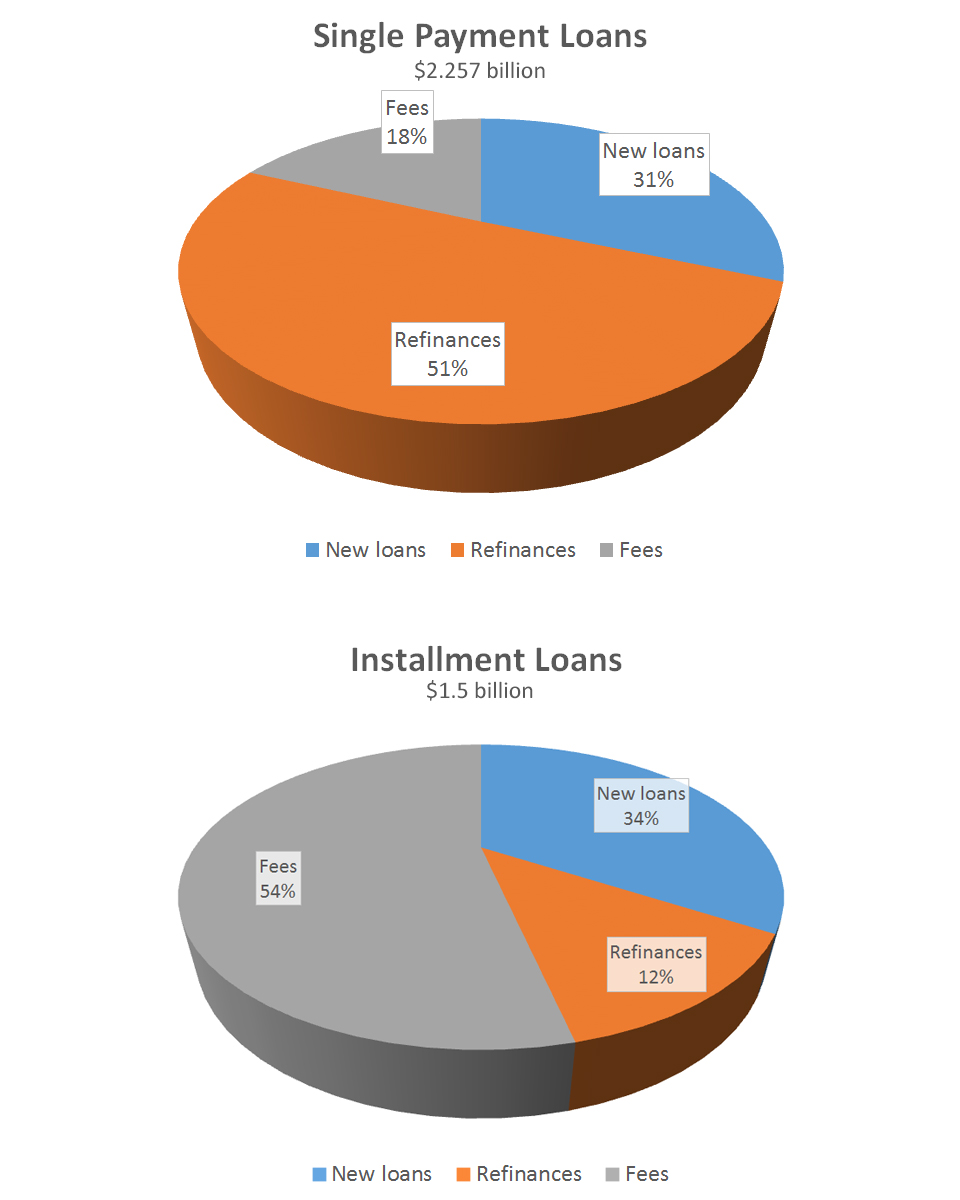

For both single-payment and installment loans, fees and refinances account for two-thirds of the revenue of the payday lending industry in 2015 (Chart 1). Single-payment loan borrowers typically had greater difficulty repaying their loans, which resulted in more than half of this category’s revenue stemming from refinances. Conversely, due to the high costs associated with installment loans in Texas, the majority of the revenue in this loan classification was from fees charged by lenders. This distribution reflects what national studies have also found in other markets across the U.S—that for each borrower, the loan principal accounted for only a small fraction of the total loan balance, compared to the loan fees charged. During 2015, the overwhelming majority of payday loans were for principal amounts between $250 and $500.[4]

Chart 1

Refinances and Fees Generate Most Revenue for Texas Payday Lenders in 2015

SOURCE: Credit Access Business (CAB) Annual Report 2015, Texas Office of Consumer Credit Commissioner.

Further review of the 2015 data shows that, of the 3,153 payday lenders reported as doing business in Texas, 50 were out-of-state entities. Refinancing data indicated most borrowers refinanced their loan between two to four times before paying it off. More than 61,000 borrowers were recorded as refinancing their loan more than ten times before reaching “paid in full” status.[5]

Local Ordinances: An Indicator of Changing Sentiment

In Texas, while there are disclosure requirements governing the issuance of payday loans, there is a system outlet that allows lenders who operate as credit services organizations (CSOs) to bypass state usury laws that regulate the amounts that lenders can charge in fees and interest for a given loan. Through the CSO provisions, instead of operating as consumer lenders, payday lenders register as credit repair businesses, pay a $100 annual registration fee and act as third party brokers to facilitate loans with no caps on the amounts they can charge in fees.[6] Absent this legislative technicality, payday and auto title lenders would be subject to Texas consumer lending laws which require licensing fees, compliance exams and include extensive lending guidelines.

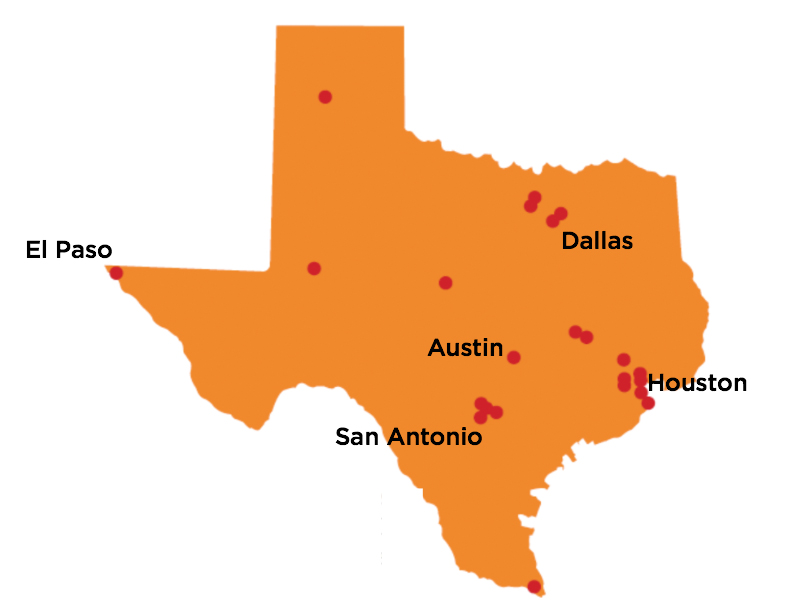

With limited state regulations in place, many cities in Texas began tackling the problem of payday lending by adopting local ordinances that regulate the practices of payday lenders. Chart 2 shows the 35 Texas cities that have adopted the Texas Fair Lending Alliance’s Unified Payday Lending Ordinance, which now provides coverage to over 9.3 million individuals.[7]

Chart 2

Texas Cities Adopt Payday Lending Ordinances

SOURCES: Texas Fair Lending Alliance; Texas Appleseed.

Lessons from Houston

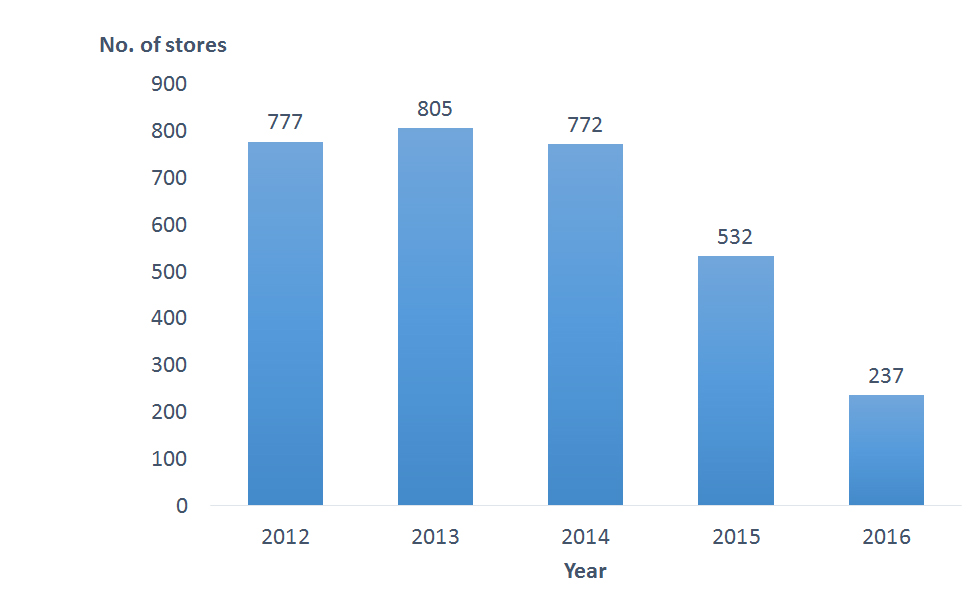

In Houston, Texas’ largest city, a payday lending ordinance was passed by the city council in 2013. After one year of enforcement, the number of payday loan stores operating within the city declined noticeably.[8] Chart 3 shows the number of payday loan stores in Houston over the past 5 years.

Chart 3

Payday Lending Stores in Houston Decline After Ordinance Enacted

SOURCES: Texas Office of Consumer Credit Commissioner; Texas Appleseed.

However, while the number of payday loan storefronts in Houston has declined significantly since passage of the ordinance, the number of individuals seeking access to this form of credit has continued to increase. Consumers still must find ways to cope with rising monthly expenditures and stagnant income levels [9]—so they have been forced to use these credit products simply to make ends meet.

Recent data from fintech giant Intuit, reported at CFSI’s 2016 Emerge Conference, illustrate the scope of this problem: 33 percent of Americans have missed at least one bill in the last 12 months and 47 percent of American consumers would struggle to pay a $400 unexpected expense. When asked why they used payday loan products, consumers cited affordable payments and convenience of access as the primary drivers.

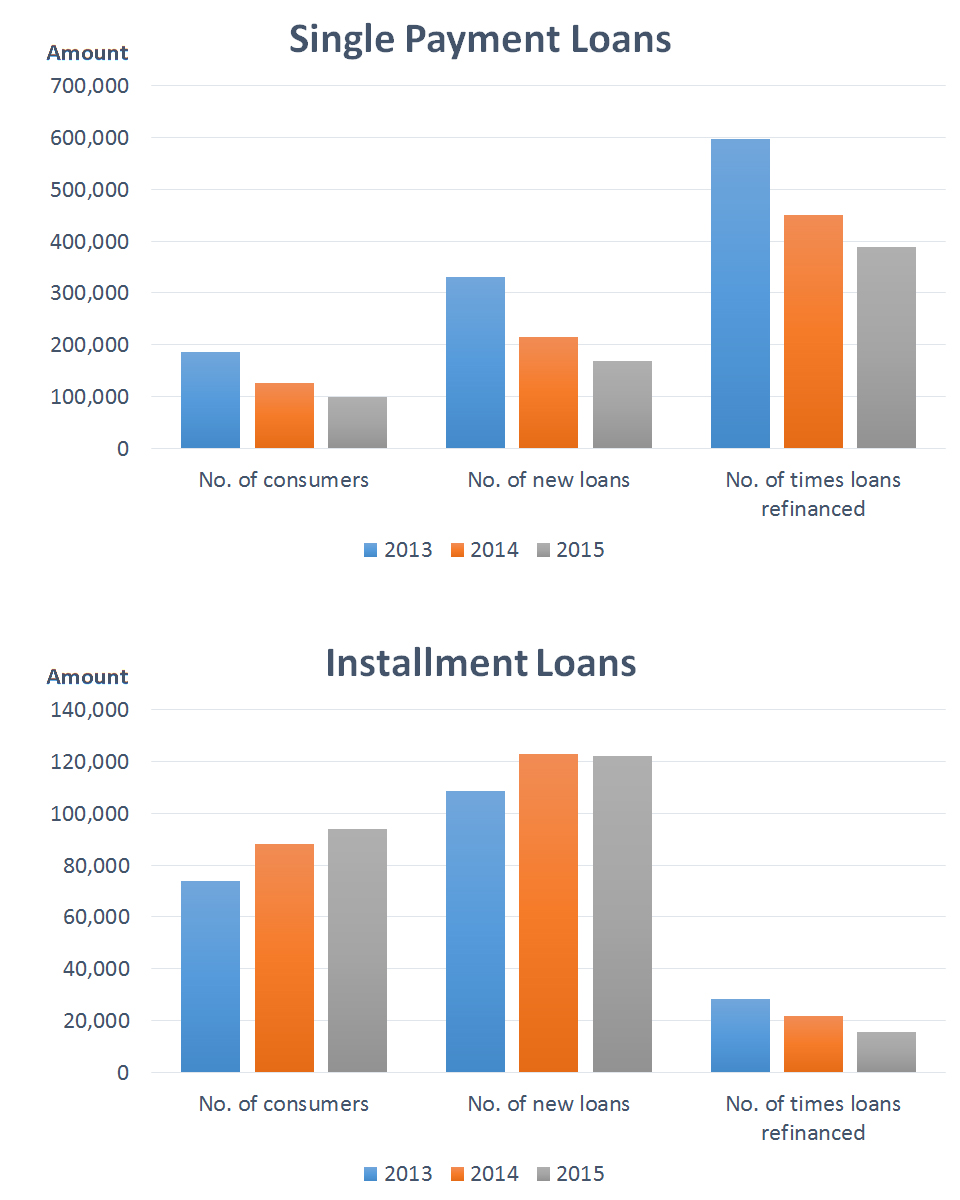

The search for affordable payments has resulted in a noteworthy shift among users of payday loan products. While installment loans, with their high costs and fees, would seem to be an unattractive solution for most, in a market of limited options, borrowers have now began to move from the single-payment structure of payday loans to longer-term installment products—as they appear to offer lower scheduled payments, which borrowers find more comfortable.

These patterns can be seen in Houston. Chart 4 provides an overview of payday lending market trends in the city from 2013 to 2015. Over the three-year period, the number of consumers seeking single payment loans has steadily decreased, while the number using installment loans has increased. This same trend can be seen in new loans issued, and there has been a steady decline in the number of times a loan is refinanced as well.

Chart 4

Houston Consumers Switch to Installment Loans

Refinances of single payment loans in Houston have remained the largest source of revenue overall, and fees, while slightly declining, have remained the largest revenue generator for longer-term loan products.

The Call for Federal Regulation and Supervision

While the problems associated with payday lending are recognized across the nation, oversight and supervision of payday lenders has been fragmented. Some states have sought to protect consumers, while other states have remained laissez-faire in regulating this multibillion dollar industry. Innovation and technology advancements have also made regulation more difficult, as new online platforms have eliminated the need for lenders to maintain the local, physical presence that was once necessary for them to conduct day-to-day business operations in various communities. Numerous lenders now utilize models that are entirely online—enabling borrowers to go from application to approval without ever stepping foot into a storefront location.

Innovation has created new challenges in promoting safer access to credit, but it can also be an integral part of the solution. Financial innovation has been a driving force moving banking and lending into a technologically-advanced reality. For many consumers, fintech innovation has increased their ability to access credit—and without it, some would have no means to acquire the credit they need during difficult times.

CFSI has conducted numerous studies of innovative lending models and has found that many of them represent promising alternatives to the various high-cost loan products commonly in use. Yet without regulation alongside innovation which tend to bring costs down, these alternatives are not consistently available nationwide. Often, the same lenders offer affordable loan products in markets where state laws limit their ability to charge excessive fees or usury interest rates, while extending drastically different products in states where there is little or no regulatory oversight.

The Texas market, with its limited statewide regulations, illustrates this problem. Lenders offer options such as flexible terms, online platforms or monthly-payment selector tools to better serve their borrowers. While, at first glance, they might appear to provide credible payday loan alternatives, further review of their lending disclosures reveals that, on a state-by-state basis, many of these innovators continue to offer products that can be classified as predatory. It is important to note, that while there is no universally recognized definition for the term predatory, the FDIC provides insight into loans, products and practices that can be classified as predatory and has identified elements which appear to indicate the presence of predatory lending. These elements include:

- Making unaffordable loans based on the assets of the borrower rather than on the borrower's ability to repay an obligation;

- Inducing a borrower to refinance a loan repeatedly in order to charge high points and fees each time the loan is refinanced ("loan flipping"); or

- Engaging in fraud or deception to conceal the true nature of the loan obligation, or ancillary products, from an unsuspecting or unsophisticated borrower.”[10]

In the absence of national lending guidelines, consumers in certain states are granted greater financial protections than others who reside in states where their respective legislatures have not acted. CFPB under its regulatory authority has now taken its first steps to formally address this issue.

CFPB-Proposed Regulations

Lenders who offer small-dollar loans are subject to this jurisdiction whether they operate online or from physical storefront locations. In June 2016, the CFPB proposed new rules that will govern certain payday, high-cost installment, open-end credit and auto title loan products. These rules include income and “ability to pay” verifications, loan structure and rollover limitations, as well as caps on the number of loans borrowers can have during a given time period or in succession. The CFPB also presented its recommendations on account drafting, advance notice requirements and the new “debit attempt cut-off rule” which requires the lender to obtain a new authorization after two unsuccessful attempts to draft a borrower’s account. The written comment period is currently underway and slated to close on Oct. 7, 2016.

The CFPB-proposed rules divide covered loans into two categories: short-term and longer-term loans. Short-term loans include products that are typically due on the borrower’s next payday as well as single-payment auto title loans. For these loans, lenders have the option of conducting a full-payment test or structuring the loan in a way that prevents the borrower from becoming trapped in debt.

The full-payment test requires the lender to verify the borrower’s income (after taxes), borrowing history (credit report check), and certain other key obligations the borrower may have (including basic living expenses such as food, rent and medical costs). The lender must determine whether the borrower will have the ability to repay the loan in full and satisfy their other major financial obligations without re-borrowing. This ability-to-pay review extends for the term of the loan and for 30 days after the loan has been paid off.

Lenders can use an alternative method—the principal payoff option—when they do not want to conduct income verification and the loan meets certain requirements. These requirements include a loan limit of $500, a loan structure that is designed to keep the consumer from getting trapped and the elimination of auto-title collateral or open-end credit lines. For this option, the borrower cannot have any other outstanding short-term or balloon-payment loans or cannot have been in debt on a short-term loan for 90 days or more over the preceding 12 months.

When extending installment loans, lenders can either conduct the same full-payment test required for short-term loans, or they have two other options available. One option is to offer loan products that meet the National Credit Union Administration’s (NCUA’s) “payday alternative loans” (PAL) guidelines. Alternatively, lenders can extend loans that are repayable in roughly equal installment payments for a term not to exceed two years and that have an all-in APR of 36 percent or less not including a reasonable origination fee. Lenders that offer this second option are also required to maintain an annual default rate under 5 percent on these types of loans and are subject to an origination fee repayment penalty for any year in which they exceed the 5-percent rule.

For more information on the proposed rules, visit the Consumer Financial Protection Bureau at www.consumerfinance.gov.

Payday Loan Alternatives: An Expanding Marketplace

While federal regulation of payday lending and other small-dollar loan products will provide much-needed oversight and protection for consumers, the CFPB rules alone cannot address all the challenges facing LMI individuals in obtaining access to credit. Their need for small-dollar loans will continue, so developing effective, less predatory alternatives to traditional payday loans is imperative.

There has already been a significant amount of work done in this area by various sectors—including private, not-for-profit and fintech. A review of existing products is helpful in identifying avenues for innovation and creative collaboration moving forward.

Existing Alternative Products

Credit Union PAL Products

Many credit unions already offer affordable small-dollar loan products to their members. Using the PAL guidelines created by the NCUA, credit unions have worked to provide payday loan alternatives to consumers. These lending guidelines include a maximum loan amount limit of $1000 and application fee of $20, as well as a maximum 28 percent APR, six-month amortization and membership requirements.[11] These small-dollar loan options have not entirely eliminated credit unions members’ use of payday loan products, but they have provided a viable alternative and a means by which many consumers are able to lift themselves out of payday loan debt.

Table 1 shows the structure, requirements and results of the Greater El Paso Credit Union’s (GECU’s) Fast Cash program. After determining that many of its members were using payday loans as a means to supplement their monthly income, GECU created Fast Cash as a payday loan alternative that their members could easily access to receive a small-dollar loan within minutes. The program has achieved overwhelming success and enabled many credit union members to eliminate their payday loan debt and improve their overall credit profiles.

Greater El Paso Credit Union (GECU) Fast Cash Program Provides Consumers Small-Dollar Alternative

| Structure | Qualification | Accessibility | Results (07/14-3/16) |

| Loan amount: $200–$1000 | Credit union membership | Online | 80% of users were already credit union members |

| 6 month repayment term | 2 current paystubs | Mobile devices | 17,377 loans |

| 27.9% APR (all interest, no fees) | 6 months employment | Any credit union branch | $10,794,138 lent |

| No early repayment penalty | Average term: 85 days | ||

| Reports monthly to credit bureaus | |||

| SOURCE: “Small Loan Credit Union Lending in El Paso” presentation by Larry Garcia of NALCAB board, May 11, 2016, at the 2016 RAISE Texas Summit in Dallas, Texas. | |||

Kinecta Federal Credit Union in California, through its subsidiary, Nix Lending, has created several small-dollar loan products that provide payday loan alternatives. Through its 30-plus lending centers across the greater Los Angeles area, Nix Lending is working to help consumers with debt consolidation, cash flow shortages, unexpected expenses and other financial hardships.

Nix offers a Payday Advance Cash loan where borrowers can receive up to $400 at a cost of $34.25 for fees and interest for a two-week time period. With a 15 percent APR, this payday loan alternative provides borrowers with access to the short-term loan they need at a fraction of the cost that most payday lenders charge.[12] In addition to its NCUA-compliant Payday Advance Cash loan, Nix Lending offers other products to help members with their small-dollar credit needs.

Borrow to Save Programs

Borrow to Save (BTS) programs, another popular credit union alternative to payday loan products, give borrowers access to capital through a loan while encouraging saving and budgeting at the same time—generally by directing a portion of either the loan principal or the repayment fees into the borrower’s savings account. Nationally, BTS programs vary dramatically in their terms, fees and loan limits, but available data indicate that they can see meaningful success.

In 2014, the Filene Institute conducted an 18-month pilot of BTS programs with 14 credit unions across the nation. Twelve credit unions completed the pilot and reported completing 3,100 loans, loaning $2.9 million, and producing more than $900,000 in savings for their borrowers. The average loan amount was $944, and the average savings for each borrower was $290. The average borrower served was 41 years old, with an average credit score of 523 and average annual income of $33,268. Of the credit unions that participated, 75 percent continued to offer their BTS product after completion of the study.[13]

Other Credit Union Products

To assist consumers with credit deficiencies who pose a greater risk to lenders, credit unions have created additional credit lines to serve this type of borrower. Secured loan products that link lines of credit to savings/checking accounts have become increasingly popular. CoVantage Credit Union offers a shared secured loan that allows its members to borrow up to the balance amount in their savings, charges an interest rate of 2 percent above what the savings account or certificate earns and allows borrower to earn dividends on the full amount in their savings account during the loan period.[14] Other credit union small-dollar loan products include lifeline loans, credit builder loans and various unsecured microloan products.

For-Profit Alternatives

Private companies also operate successfully within the small-dollar loan market—and while many for-profit companies have terms that might be classified as high-cost, some have created alternative products that effectively serve LMI individuals and communities. Issues with profitability have prompted most for-profit organizations and banks to exit this lending space, but numerous institutions have recognized the importance of providing banking solutions for all consumers and moved forward with innovating and modifying their programs to meet this need.

Oportun, a Community Development Financial Institution (CDFI) based in California, provides unsecured credit to individuals in need of an alternative to payday loans. With more than 190 locations in California, Utah, Nevada, Illinois and Texas (30 plus Texas), Oportun reports that 90 percent of its clients live in LMI communities, and it has provided loans for many individuals within Hispanic and immigrant communities. Through an in-person lending process, Oportun has completed more than 1.4 million loans worth more than $2.4 billion. Maximum loan amounts have reached over $7,000 with an average APR for each loan of 32.60 percent. The Oportun loan program features underwriting for every loan, no prepayment penalties or balloons and credit reporting with two of the major credit bureaus.[15]

Bank Alternatives

Liberty National Bank in Paris, Texas, provides small-dollar loans to its customers across the Lamar County area. A participant in the FDIC’s 2008 Small-Dollar Loan Pilot Program, this community bank in northeast Texas has continuously offered a small-dollar loan program since its inception in 1931. With a default rate around 7 percent, the program, which is available to both customers and non-customers, features a $500 minimum loan amount and no credit score requirement. Indicative of the overwhelming need for small-dollar credit, the bank remains inundated by persons seeking assistance from as far as several hundred miles away in neighboring counties.

Sunrise Banks, a CDFI headquartered in St. Paul, Minnesota, offers a small-dollar, employer-based installment loan alternative for consumers. Through its True Connect program, borrowers access an online lending platform to take out loans against their future paycheck earnings. Loans typically range between $1,000 and $2,000, depending on the employee’s salary, and have a 25 percent interest rate during a one-year term. According to Sunrise, loans can be disbursed within 24 hours, providing borrowers with quick access to the cash they need.[16]

Not-for-Profit Models

Community-based organizations have also recognized the need to provide individuals within LMI communities with access to affordable small-dollar loan products. Working with philanthropic organizations, banks and other funding sources, many mission-driven organizations have created innovative programs that offer potential alternatives to payday loans.

St. Vincent de Paul-Dallas Mini Loan Program. The Society of St. Vincent de Paul–Dallas recently began offering small-dollar loans to LMI individuals living in the Dallas area. The Mini Loan Program (MLP) was launched in January 2015 and reached its one-year mark of lending in July. Using $135,000 in collateral, St. Vincent de Paul–Dallas has successfully co-signed and extended credit for 47 new small-dollar loans and 56 predatory loan conversions ranging from $200 to $3,500. The average loan amount for the program to date is $1240, with a monthly payment of $144. For predatory loans that were converted, the average APR for borrowers in this program had been 347 percent prior to conversion. The Society estimates that 80 percent of its borrowers would not qualify for a loan at a bank if they applied alone.

Providing 12-month installment loans at a fixed low-interest rate, MLP combines small-dollar credit with savings and financial management education. MLP reports to credit bureaus, and volunteers trained as financial coaches work very closely with borrowers on their budget. The program tracks and provides borrowers with connection to intensive support services from the moment they sign for their loan at the bank until they pay the loan in full.

Only four MLP applicants have been declined to date, and the program boasts a zero percent default rate and 6.7 percent delinquency rate. The Society works with delinquent borrowers to identify and address issues the borrower may be facing as well as the reason the borrower is not paying the loan. Leveraging the Society’s relationships with other social service agencies, borrowers are connected to the wraparound services they need to get back on track.

While the MLP program has seen some success to date, it is facing some headwinds. Developing the sustainability of this model has been a challenge, as the program is currently funded entirely by donations. Operating costs for personnel also limit the reach of the program. St. Vincent de Paul–Dallas is currently working to address these issues. Plans for future expansion include incorporating borrow-and-save components as well as loan models that include use of income tax refunds.

Community Loan Center (CLC). The Community Loan Center (CLC) is an employer-based loan model that originated in Texas and uses payroll deduction as a means of repayment. Created in 2011 by the Rio Grande Valley Multibank (RGVMB), a CDFI in Texas’ Rio Grande Valley, this loan alternative provides low-interest, low-cost personal loans. The CLC is an online lending model administered by not-for-profit organizations that serve as local loan centers. Currently, CLC operates in Indiana as well as several Texas markets, including Houston, Dallas and Austin. There are plans to expand to San Antonio, El Paso and Lubbock in the near future.

Offered at no cost to the employer and marketed as an employee benefit, this loan is coupled with financial education and credit bureau reporting to help borrowers establish or rebuild their credit. Loan terms include a $1,000 loan maximum, 12-month installment plan, 18 percent interest rate (21.83% all-in APR) and $20 origination fee. Every loan is underwritten and there are no prepayment penalties, balloon payments or collateral requirements.[17]

Since its inception, CLC has completed over 12,600 loans worth more than $9 million. With a loan loss rate of 2.5 percent, this small-dollar loan alternative is estimated to have saved borrowers more than $8 million.[18]

Other Not-for-Profit Alternatives

Technology has spurred increased innovation in the small-dollar lending market. The inability of many consumers to access credit directly from banks and other traditional lenders has led some to create peer-to-peer lending alternatives to fulfill their credit needs. In 2008, San Francisco-based Mission Asset Fund (MAF) started Lending Circles, a loan alternative that provides zero-interest loans to help participants build credit and access affordable, small-dollar credit.

Under the Lending Circles program, a group of individuals (usually six to ten) join together to form a lending circle. As a prerequisite, program participants are required to complete an online financial training class before joining a circle. They meet in person to decide on an amount for their group loan and began making a monthly payment, usually ranging from $50 to $200, which is reported to credit bureaus monthly by MAF. Members of the lending circle take turns receiving the loan each month until everyone in the group has a chance to use the group loan capital.

To date, MAF has worked through its 50 program providers located across 17 states to complete over 5,669 social loans totaling more than $5.05 million. The program boasts a 99.3 percent repayment rate, with borrowers increasing their credit score by over 168 points on average.[19]

The Path Forward

In analyzing alternative lending products, a great deal of activity and innovation within these various sectors of the industry has occurred. Moving forward, it may become increasingly difficult for organizations to address the challenge of providing affordable small-dollar credit while working alone. We must look to cross-sector collaboration, where diverse partners work together to form effective solutions that provide successful payday loan alternatives.

This form of cooperation is seen in the greater Kansas City area, local banks including Central Bank, Missouri Bank and United Missouri Bancshares (UMB) Financial Corp. have partnered with Next Step KC, a United Way community-based nonprofit agency, to provide financial education and small-dollar loan products to LMI families. Loans range between $300 and $500, have terms of four-to-nine months and allow borrowers to build or improve their credit while forming a relationship with a mainstream financial institution. Next Step KC does not make loans, but focuses on what it does best to facilitate loans by using a referral process and its relationships with other community partners to create a pipeline of consumers in need who potentially qualify for the loan program.[20]

In Virginia, the Jubilee Assistance Fund established by the Virginia United Methodist Credit Union (VUMCU) provides evidence of the success that is possible through thoughtful collaboration and cross-sector partnerships. Working with a network of United Methodist churches across Virginia, VUMCU uses the Jubilee Assistance Fund to offer small-dollar loans at an interest rate of about 6 percent. This collaborative loan program allows local churches to establish an account with the credit union and provide collateralized, short-term, small-dollar loans to members who ordinarily would not qualify for a loan elsewhere. Borrowers are required to receive financial counseling and agree to payroll deduction as well as loan monitoring. While currently limited to Virginia, plans to expand the program to other United Methodist church conferences across the nation are underway.[21]

Working independently, credit unions, banks, CDFIs and community-based organizations have all seen various degrees of success—but issues of profitability, scale, and adequate financing present impediments to moving forward as a collective. Financial institutions with access to funding struggle to find models and platforms that are profitable. Similarly, community-based organizations and nonprofits with successful programs struggle to find sufficient capital.

With new federal regulations on the horizon that create certainty and even the playing field when compared to the payday lending market, an opportunity now exists to explore new ways to expand this market. As outlined, the most creative alternative solutions are those that are collaborative, scalable and primed for a new and emerging market place.

Notes

- Consumer Financial Protection Bureau

- Texas Appleseed

- Know Your Borrower: The Four Need Cases of Small-Dollar Credit Consumers, by Nicholas Bianchi and Rob Levy, Center for Financial Services Innovation, December 2013.

- Texas Office of Consumer Credit Commissioner, Credit Access Businesses (CAB) Annual Report 2015.

- See note 4.

- Texas Secretary of State

- Texas Fair Lending Alliance and Texas Appleseed.

- See note 2.

- Economic Policy Institute.

- Federal Deposit Insurance Corp.

- National Credit Union Administration (NCUA).

- Nix Lending.

- Filene Research Institute.

- CoVantage Credit Union.

- Presentation by Sarah Livnat, Senior Director of Community Relations at Oportun, May, 11, 2016 at the 2016 RAISE Texas Summit in Dallas, Texas.

- TrueConnect.

- Rio Grande Valley Multibank.

- Presentation by Howard Porter, Program Manager at Community Loan Center of Texas, July, 12, 2016 at the 2016 RAISE Texas Webinar on Workplace Financial Wellness.

- Presentation by Jose Quinonez, Chief Executive Officer at Mission Asset Fund, June, 14, 2016 at the Federal Reserve System Connecting Communities What It’s Worth: Strengthening the Financial Future of Families, Communities and the Nation Webinar.

- Next Step KC.

- Virginia United Methodist Credit Union.

About the Author

Kevin Dancy is a community development specialist at the Houston Branch of the Federal Reserve Bank of Dallas.