Current Banking Risks

This summary is drawn from the Dallas Fed’s quarterly assessment of the risk landscape for banking institutions in the Eleventh District. It is not an all-inclusive list of banking risks.

Current risks facing the banking industry are defined as key issues in the present environment that could impact a bank’s ability to operate its business model. These risks are considered the most significant exposures based on a forward-looking evaluation of the inherent risks and effectiveness of risk management activities.

The risks highlighted in this report are identified by their perceived impact, as well as the potential for data gaps that may present a supervisory challenge.

While vacancies are improving, rent growth continues to lag, and ongoing economic uncertainty may keep certain sectors of the market in a risk-averse mode. High interest rates continue to affect refinancing, and capitalization rates are not declining. There is some dispersion in how much different banks with high concentration in commercial real estate are provisioning for potential credit losses, but noncurrent loan rates remain historically low.

Uncertainty about inflation and labor market fragility have created an unclear interest rate path, but firms have reduced their interest rate sensitivity following the regional banking turmoil in 2023. Unrealized losses in bank portfolios persist but are declining.

Cybersecurity risk remains elevated in the Eleventh District due to geopolitical factors and the use of new technologies by banks that introduce cybersecurity risks that banks must manage. Successful cyber attacks could create a range of outcomes involving financial losses or potential liquidity issues at an affected firm.

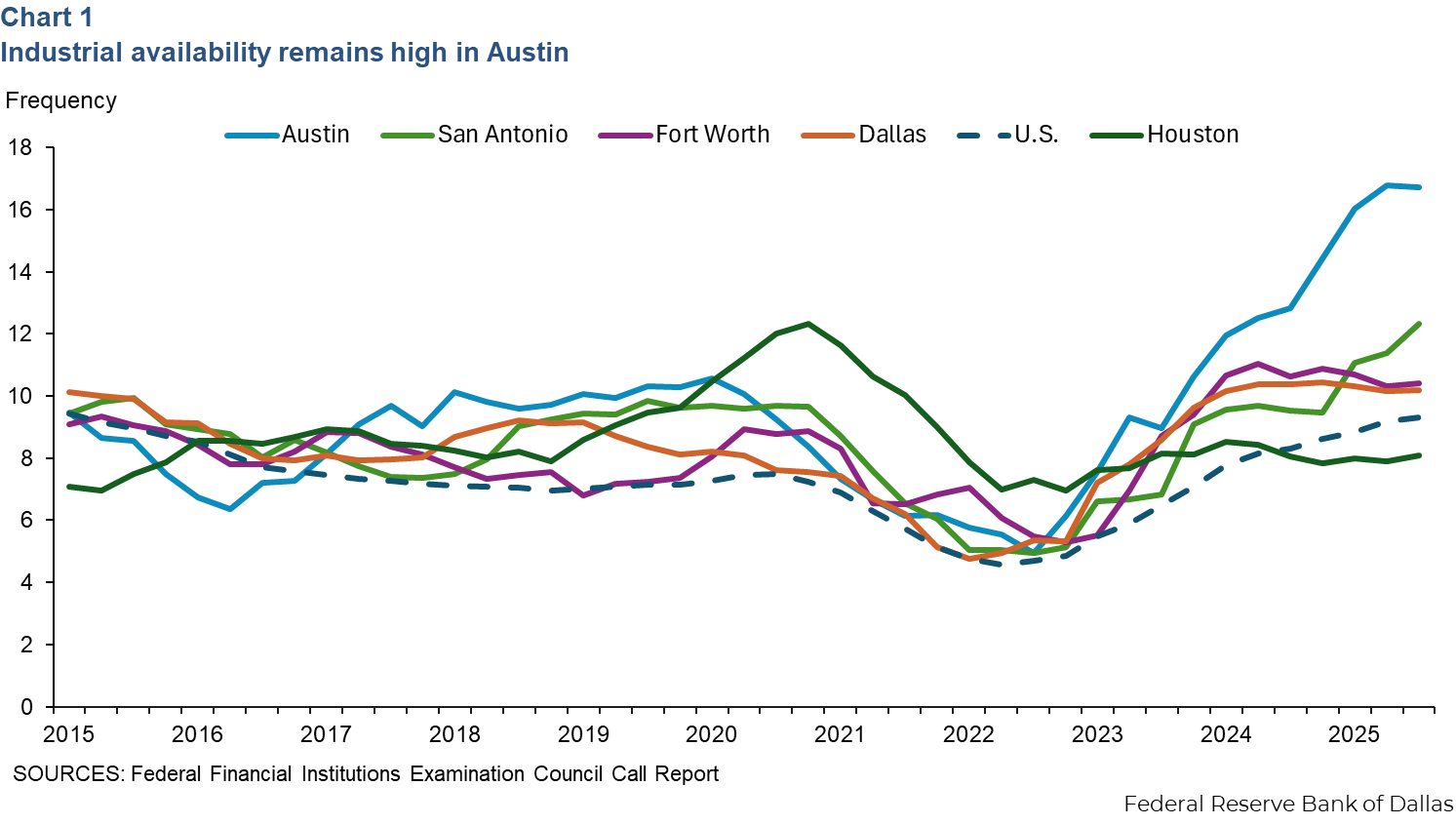

Industrial completions continue to outpace net absorption in 2025, both nationwide and in all major Texas metro areas except Dallas and Fort Worth. The Austin industrial availability rate remains high, and the rate for San Antonio is on the rise (Chart 1). At the same time, Austin industrial rents continue to decline, and rent growth in San Antonio has slowed. As of third quarter 2025, Austin had the second-highest industrial availability rate (17 percent) and the third steepest year-over-year rent decline (-5.7 percent) among the 76 metros tracked by CBRE.

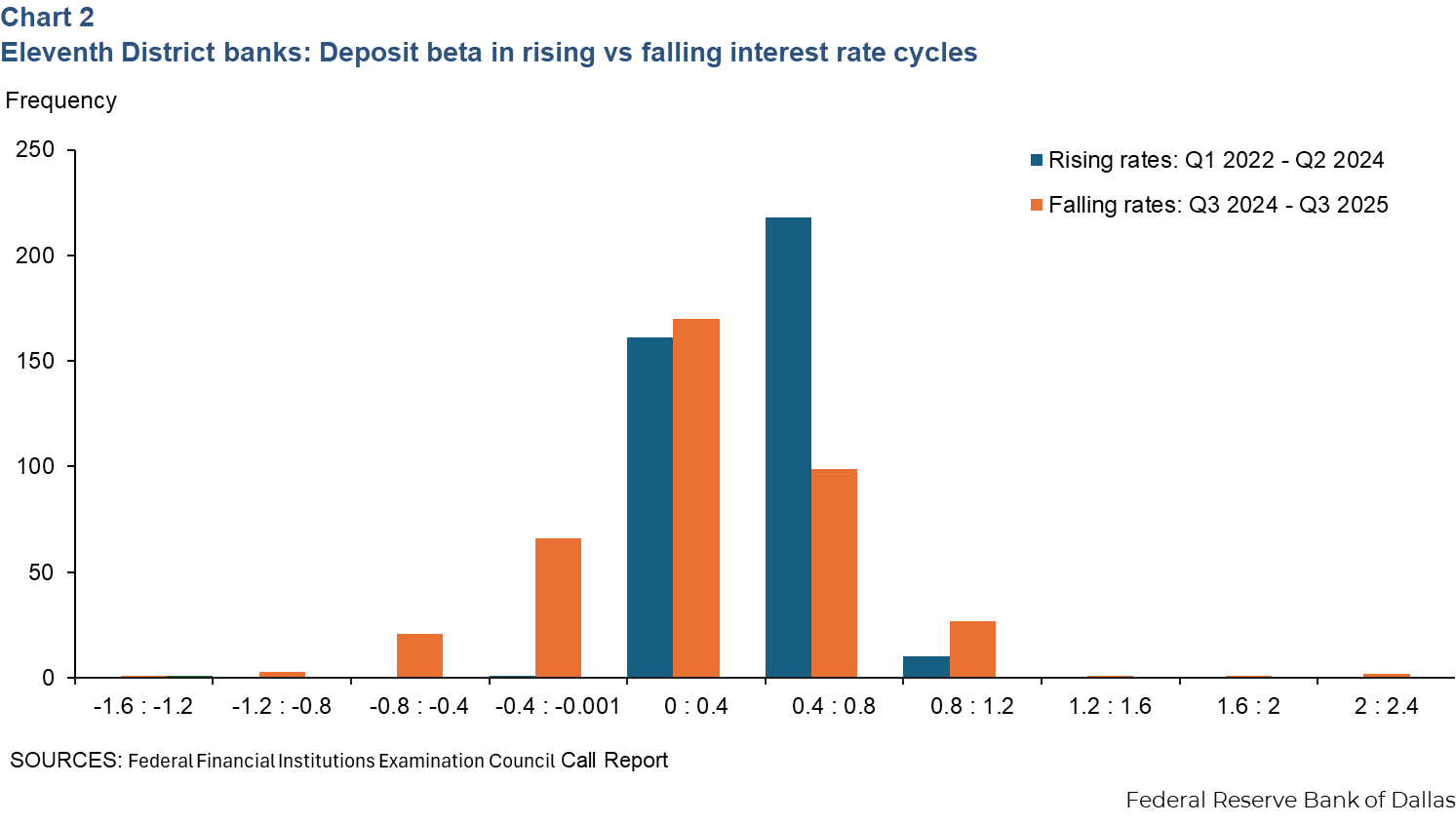

Deposit betas measure how much bank deposit rates move with changes in the federal funds rate. Among Eleventh District banks, deposit betas were largely concentrated between 0 and 1 during the uprate cycle between first quarter 2022 and second quarter 2024 (Chart 2, blue bars). They have shown much greater dispersion through the most recent downrate cycle, with several instances of deposit funding costs moving upward while the effective federal funds rate has declined (Chart 2, orange bars).

NOTE: Analysis for this release is based on data as of Sept. 30, 2025.

About Current Banking Risks

For more information about this report, contact Emily Greenwald