Eleventh District banks hold fewer loans to non-banking firms compared with peers

Since 2009, loans by banks to non-banking financial institutions (NBFIs) have grown faster than any other loan type, at a compound annual growth rate of 21.9 percent nationally according to FDIC research.[1]

Concurrently, the private credit market has grown and could soon make up 15 percent of the fixed-income investment market, according to a Bloomberg Intelligence survey.[2]

Recent high-profile bankruptcies of firms relying on private credit financing, including auto parts manufacturer First Brands, and subprime auto lender Tricolor Auto, have raised concerns that relatively opaque and riskier credit could hide broader systemic risk. Several banks, including some headquartered in the Dallas Fed Eleventh District, announced asset write-downs from exposure to these bankruptcies. As a result of these bankruptcies, share prices of many regional banks fell in October 2025 by about 5 percent to 15 percent.

Motivated by the impact of these recent bankruptcies on our district, as well as the rapid growth of NBFI loans, we sought to examine NBFI loan trends among Eleventh District state-member banks (SMBs), that is, state-chartered banks that are Federal Reserve members. Recent changes in the Call Report, the Fed’s quarterly assessment of financial institutions, allow analysts to examine bank loans to NBFIs in greater detail.

NBFIs are companies that provide financial services without full banking licenses. Common examples of NBFIs include insurance companies, pension funds and mortgage companies. NBFI loans are not exclusively made to private credit firms, but loans to private credit firms are included in the broader NBFI loan category in the Call Report.

Without examining much detail on the quality of these loans, we find that Eleventh District SMBs hold fewer NBFI loans than their peers in other Federal Reserve districts.

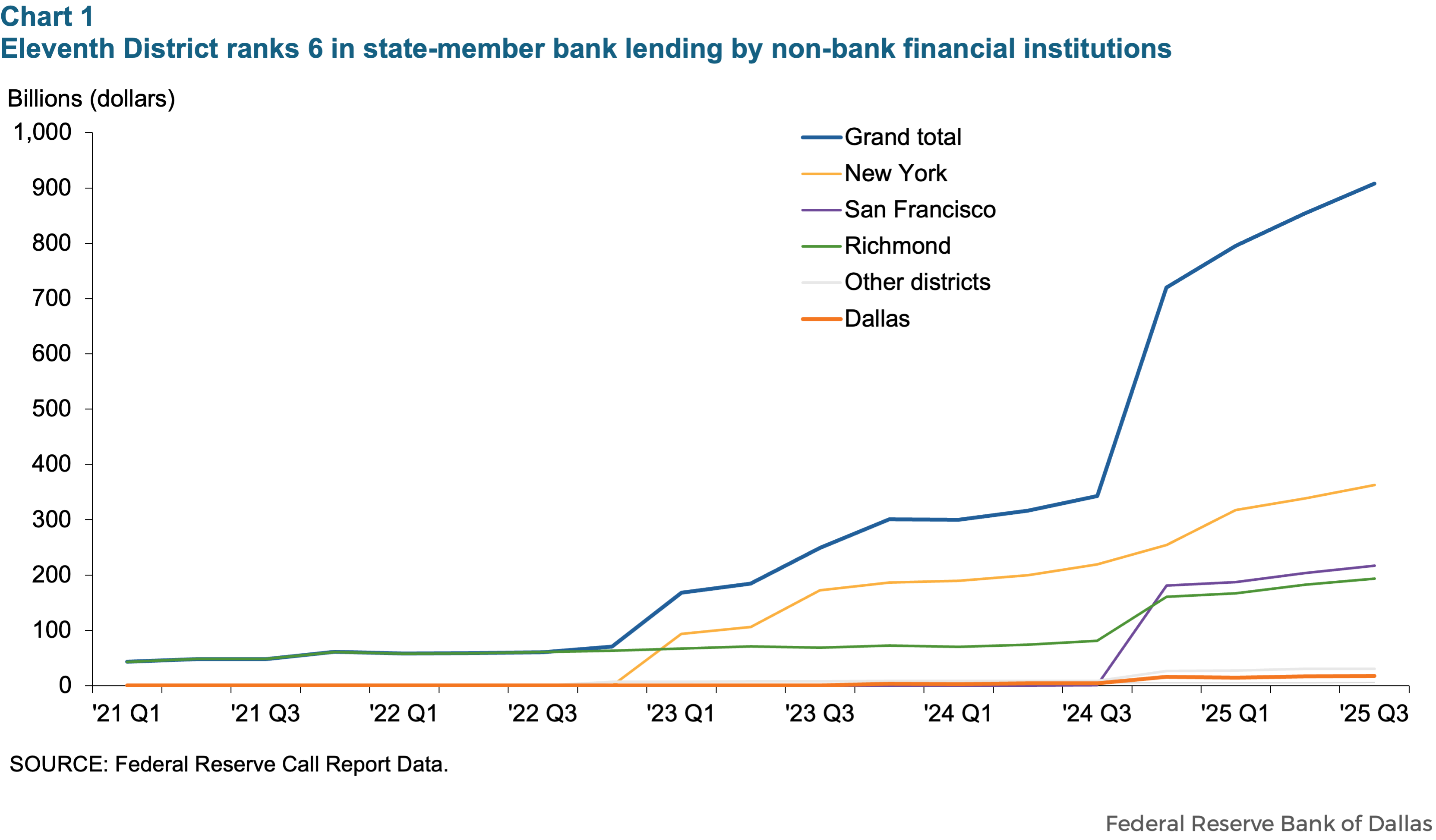

Eleventh District state member banks hold fewer NBFI loans than banks in other districts

National state-member bank holdings of NBFI loans increased 26 percent in the four quarters ending in third quarter 2025, from $720 to $908 billion. In comparison, Eleventh District SMB NBFI loan growth was mild, increasing about 12 percent in that period from $15.6 to $17.5 billion. This means the Eleventh District comprised about 2 percent of total national SMB lending to NBFIs, ranking sixth out of the 12 Federal Reserve districts (Chart 1).

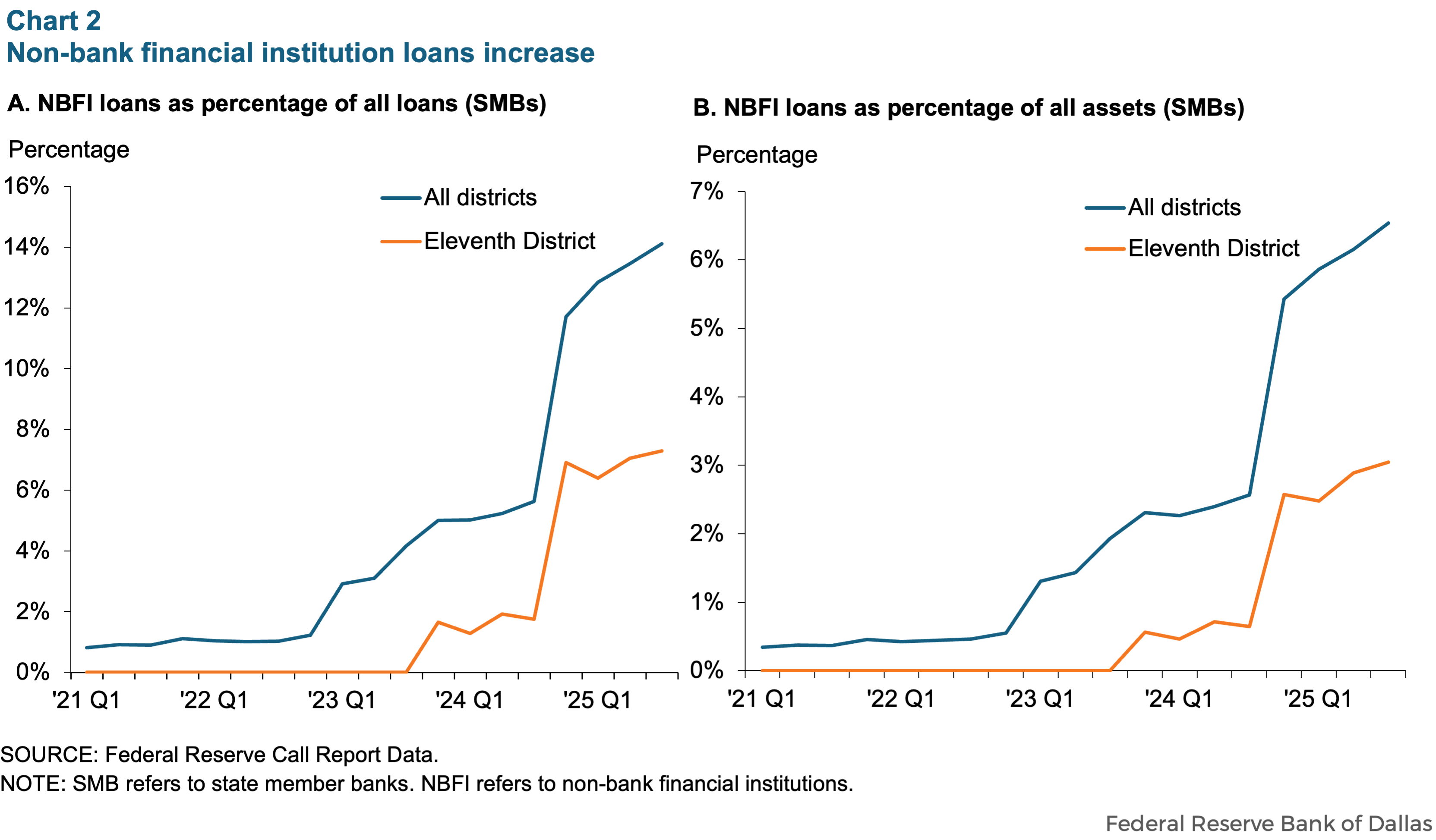

Similarly, Eleventh District SMBs tend to hold fewer NBFI loans in terms of both total loans held and total assets compared with the national average (Chart 2).

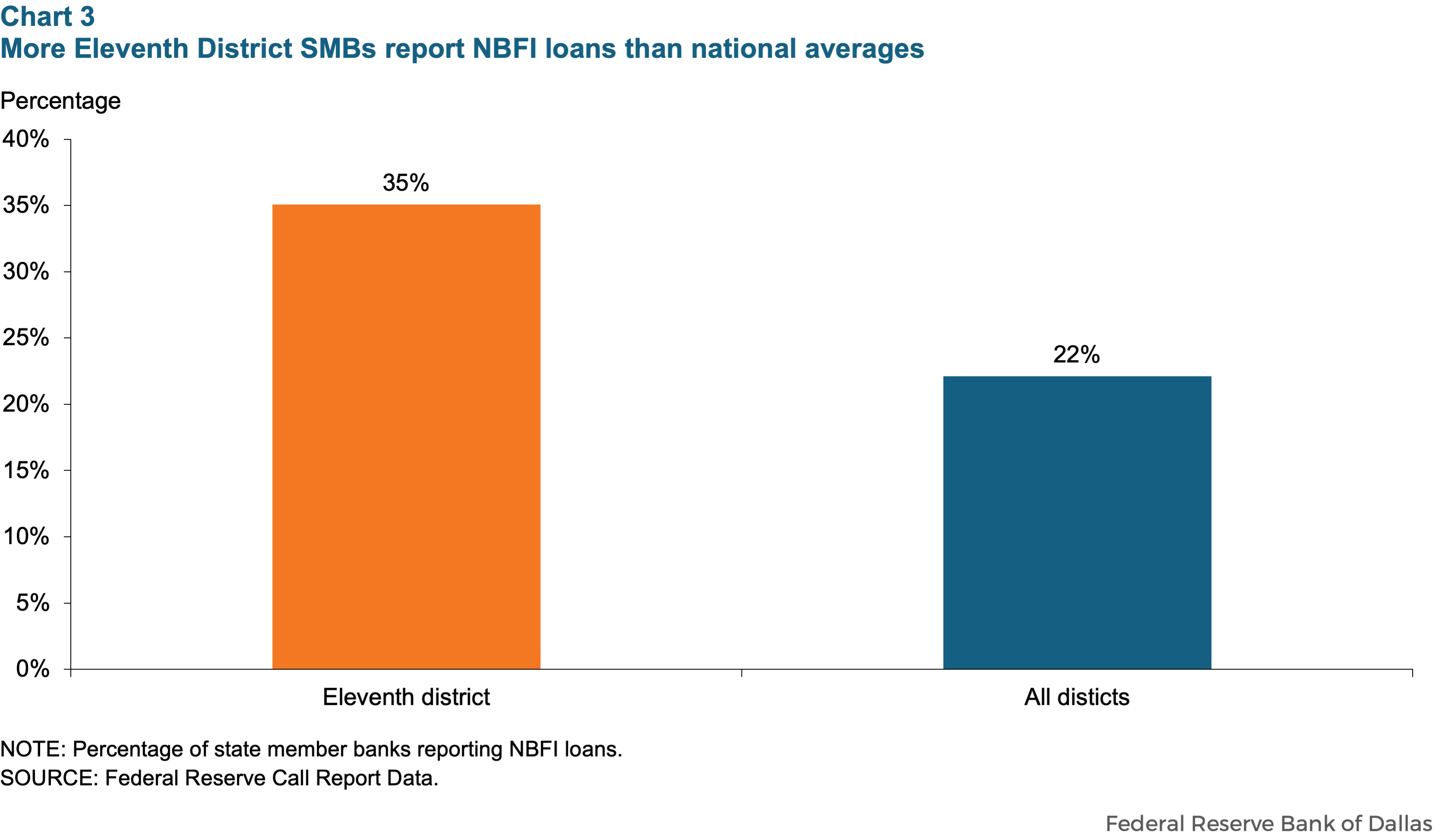

While Eleventh District SMBs in aggregate do not hold as many NBFI loans as other districts, it is worth noting that the district has a relatively high proportion of SMBs that make at least some NBFI loans, as seen below in Chart 3. In fact, the district has the third highest percentage of SMBs with record non-zero NBFI loan amounts across all Federal Reserve districts. However, the average NBFI loan portfolio per bank is relatively small in the Eleventh District.

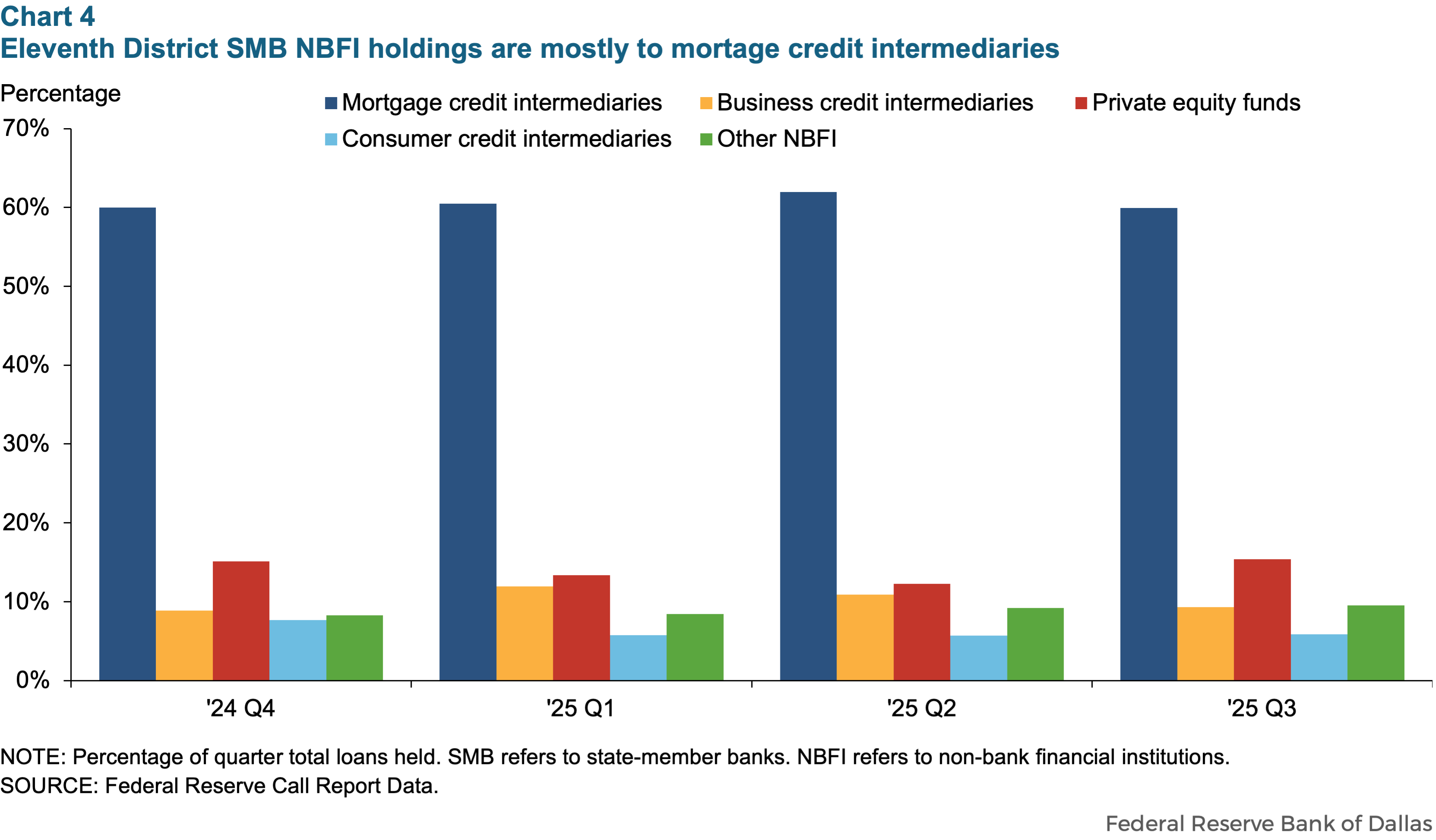

Eleventh district NBFI loans tend to be concentrated in the mortgage credit sector

Changes to the Call Report that took effect in fourth quarter 2024 also allow us to examine NBFI loans by sub-type. As shown in Chart 4 below, from fourth quarter 2024 to third quarter 2025, the majority (roughly 60 percent) of Eleventh District state member bank NBFI loans were made to mortgage credit intermediaries. Mortgage credit intermediaries are also the largest sub-type at a national level, albeit at a much lower rate (typically around 25 percent). Many mortgage credit intermediaries originate home mortgages to distribute through government agencies such as Fannie Mae and Freddie Mac and typically do not present a significant credit risk when banks lend to them.

All other sub-types tend to be much smaller, with each sub-type comprising less than 15 percent of the total share of NBFI loans in the Eleventh District. Of note, the business credit intermediaries sub-type is likely the best direct link to the private credit loans associated with recent bankruptcy news and typically makes up 10-15 percent of NBFI loans in the Eleventh District. Nationally, loans to business credit intermediaries tend to comprise around 20 percent of NBFI loans.

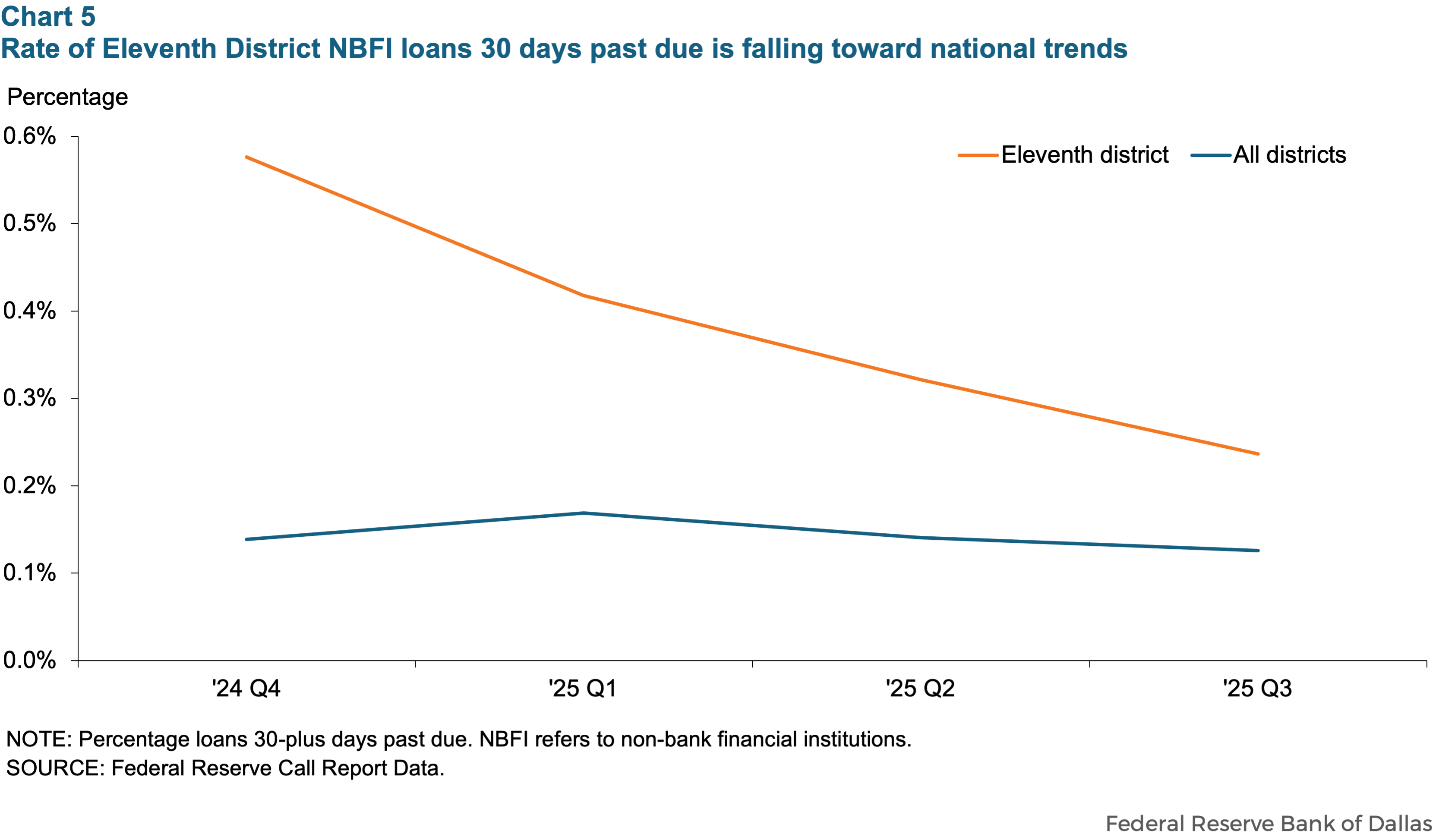

Eleventh district NBFI past-due rates typically higher than national averages, but trending down

Lastly, we examine the past-due rates of NBFI loans in the Eleventh District. The chart below shows that since fourth quarter 2024, the percentage of Eleventh District NBFI loans that are at least 30 days past due has been higher than the national trend. However, this percentage has trended down in the district, from about 0.6 percent in fourth quarter 2024 to about 0.3 percent in third quarter 2025.

These delinquency rates tend to be dominated by a small handful of banks, both at a national level and in the Eleventh District. For example, in third quarter 2025 two state member banks (not in the Eleventh District) held more than 45 percent of the 30-days-past-due loans (Chart 5). Within the Eleventh District, two SMBs held over 90 percent of the 30-days-past-due loans above.

Both the Eleventh District and national past-due rates on NBFI loans seem to be relatively low. According to Federal Reserve Economic Data (FRED) database, for example, the national delinquency rate on business loans from commercial banks in third quarter 2025 was roughly 1.3 percent, about five times higher than the Eleventh District NBFI loan past-due rate.[3]

It is worth noting that a few valuable data points are still not available despite the Call Report changes that allow for this analysis. First, we cannot examine past-due or delinquency rates by loan sub-type. Second, bank call reports still do not offer a way to examine the profitability of NBFI loans compared to other loan types. Third, we cannot view the individual NBFI loans issued by a bank, meaning it is impossible to tell from public financial data if an institution may have outsized exposure with a single or small group of borrowers. Regulators can try to approximate some of this information from the Federal Reserve Y-14 report on bank holding companies or Shared National Credit data, but it remains incomplete. Finally, we cannot tell exactly how many NBFI loans are made to private credit firms, an industry currently receiving extra attention from the media and financial analysts.

While private credit and NBFI lending have received increased national scrutiny, Eleventh District state-member banks maintain a limited exposure to these sectors. Eleventh District SMBs hold a smaller percentage of NBFI loans relative to assets compared to national averages, and past-due rates for these loans are higher but falling in the district. As always, banks should continue to monitor their private credit lending and maintain high underwriting standards to avoid potential NBFI losses.

Notes and related fed research:

- “Bank Lending to Nondepository Financial Institutions”, by Kate Fritzdixon and Joycelyn Lu from the FDIC

- “Private Credit Set to Win More Deals From Rivals, Survey Shows”, by Francesca Veronesi from Bloomberg on 10/15/25

- Board of Governors of the Federal Reserve System (US), Delinquency Rate on Business Loans, All Commercial Banks [DRBLACBS], retrieved from FRED, Federal Reserve Bank of St. Louis, January 6, 2026

- Bank Lending to Private Equity and Private Credit Funds: Insights from Regulatory Data

- Banks and Private Credit: Competitors or Partners?

- Banking Trends: Why Banks Finance Their Nonbank Competitors

About the author

Michael Troxell is a data scientist in the supervisory risk, policy and surveillance division of the Banking Supervision Department at the Federal Reserve Bank of Dallas.