Community Banks Play Important Role for Rural Eleventh District Communities

Many of the Eleventh District’s rural counties rely on community bank branches, particularly in Texas and Louisiana. These rural areas are important to the production and support of the cattle, agricultural and energy industries for the district, the U.S. and the world.

Texas’ rural population of 4.7 million exceeds that of any other U.S. state, according to research nonprofit Texas 2036. Rural small businesses make up 24 percent of all businesses in Texas, contributing more than 20 percent of the state’s economic output. That’s not insignificant, considering Texas’ GDP would make it the eighth largest economy in the world.

Community banks are lifelines for these businesses and rural populations. Nearly half of the brick-and-mortar bank branches in the Eleventh District are community banks, and of the 298 counties in the district, 106 are solely served by community banks. Access to banking is important for saving, building wealth and supporting career mobility, which community banks help to facilitate by serving these rural populations.

Community banks account for largest share of Eleventh District bank branches

According to Federal Deposit Insurance Corp. Summary of Deposits data for 2025, there are a total of 6,503 full-service bank branches in the Eleventh District. Of these branches, 12 are cyber offices without any physical presence, and 507 are retail office branches within grocery or big-box stores. The remaining 5,984 are physical brick-and-mortar branches.

While large banks hold more than 50 percent of the $1.2 trillion in deposits at bank branches in the district, they represent just 31 percent of the brick-and-mortar branches (Table 1). Community banks, with about a quarter of the value of branch deposits, operate the largest share of branches.

| Number of Eleventh District branches | Share of Eleventh District branches (%) | Eleventh District branch deposits ($billion) | Share of Eleventh District branch deposits (%) | |||

| Community banks | 2,800 | 47 | 314 | 26 | ||

| Regional banks | 1,347 | 22 | 256 | 21 | ||

| Large banks | 1,837 | 31 | 623 | 52 | ||

| NOTE: Figures are for brick-and-mortar branches as of June 30, 2025. Community banks have assets less than $10 billion, regional banks have assets between $10 billion and $100 billion, and large banks have assets greater than $100 billion. SOURCE: Federal Deposit Insurance Corporation, Summary of Deposits. |

||||||

Eleventh District community banks are more active in rural areas

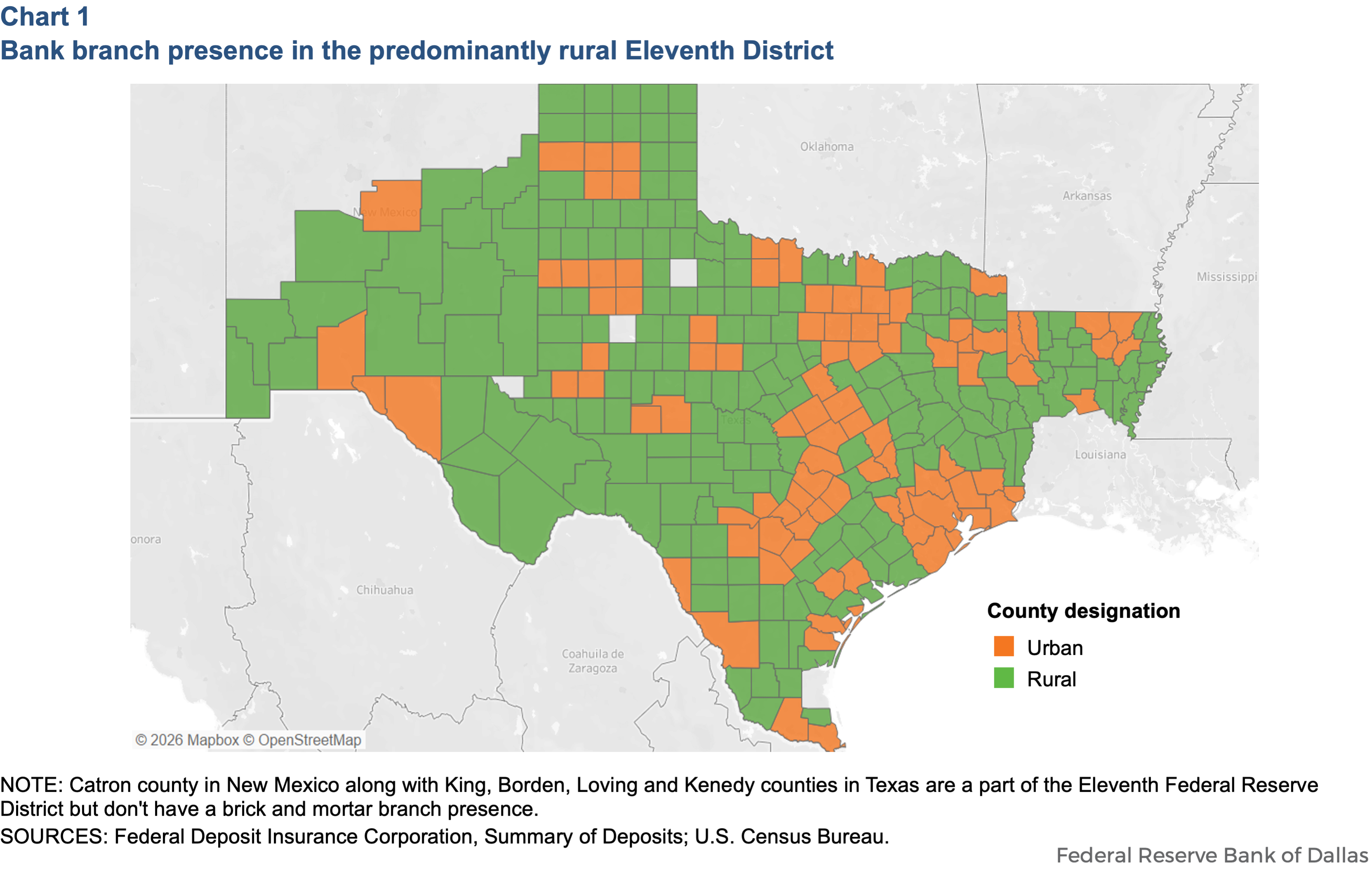

Of the 202 rural counties in the Eleventh District, all but five have at least one brick-and-mortar banking office, and all of the 96 urban counties have banking offices (Chart 1). Compared with their regional and large bank counterparts, community banks have a larger share of branches and branch deposits in the Eleventh District’s rural counties. According to 2025 SOD data, 33 percent of community bank branches holding 26 percent of community bank deposits are in Eleventh District rural counties, compared with 13 percent of regional bank branches holding 6 percent of regional bank deposits and 4 percent of large bank branch deposits.

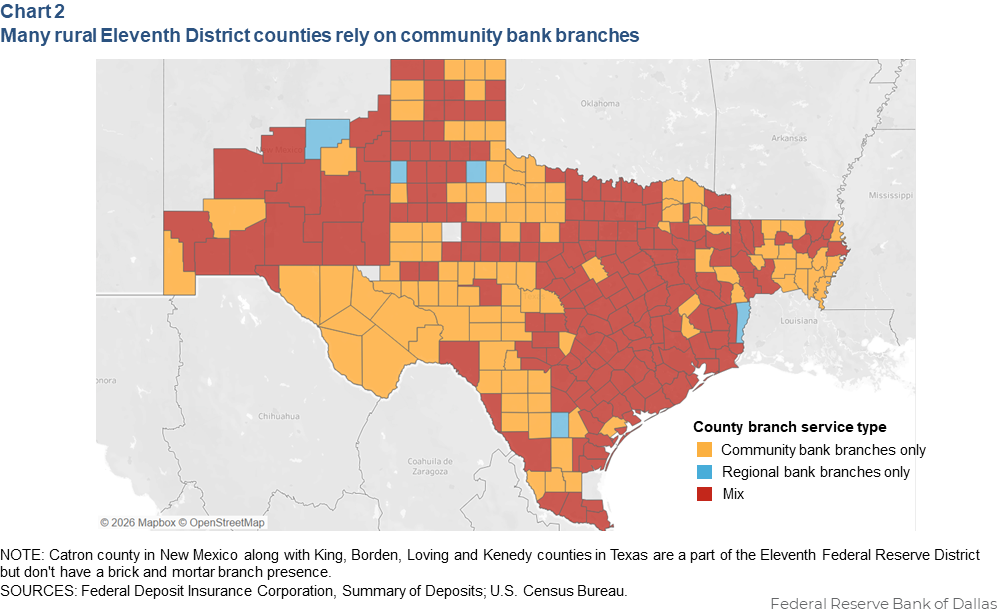

Many rural Eleventh District counties only have community bank branches. Of the 197 rural Eleventh District counties with at least one bank branch, 91 are only served by a community bank, and five are served by only a regional bank, while none is served by only a large bank (Chart 2).

Community banks serve an important role in rural counties in the Eleventh District, play an outsized role in supporting small businesses and have a deep commitment to the communities they serve Fostering a strong community banking ecosystem is a priority of the Dallas Fed to support access to banking across the district.

About the author

JR Garcia is a data scientist in the supervisory risk, policy and surveillance division of the Banking Supervision Department at the Federal Reserve Bank of Dallas.

Lorenzo Garza is a vice president in Banking Supervision at the Federal Reserve Bank of Dallas, where he oversees teams responsible for supervisory risk, policy and bank surveillance.

Kelly Klemme is a lead data scientist in the supervisory risk, policy and surveillance division of the Banking Supervision Department at the Federal Reserve Bank of Dallas.