Consumer Credit Trends for Texas

October 2019

Overview

The extents to which individuals are accessing credit and making timely payments on debt are important measures of financial inclusion and economic health in the United States, as well as in states and local communities. This paper uses a nationally representative loan-level dataset from Equifax to study consumer use and timely payment of four major loan types in Texas: mortgage, credit card, auto and student. It also looks at trends in balances, delinquent payments and credit scores over the past 15 years. Analysis finds that although there has been a decline in overall serious delinquencies since the Great Recession, recent years have seen increases in significantly late payments for car and student loans in the state. The portion of Texas’ student debt that is currently at least 90 days past due is about 13.3 percent, while the total balance carried by Texas borrowers has almost tripled since 2006, adjusting for inflation. Car loans experienced increases in serious delinquency rates over the past four years, particularly in El Paso County, where the rate has nearly doubled since 2014. This report also notes that much of the improvement in the mortgage and credit card markets may come from restricted loan access for those with less-than-prime credit. Although the number of people in the Texas mortgage market overall increased, the numbers of those with near-prime or subprime credit decreased by more than 445,000 people. Further research is needed to understand how well the credit markets are striking a balance between keeping serious delinquencies low and ensuring that all consumers have an equal opportunity for inclusion in the credit economy.

Introduction

Credit access and loan delinquencies are important indicators of financial health in the United States—both for an individual’s economic prosperity and for the nation as a whole. On an individual level, loans increase access to large-scale purchases such as cars, houses and higher education. They also help people meet everyday expenses or serve as a necessary buffer for unexpected costs or emergencies. An inability to access mainstream, affordable credit can lock people out of asset-building opportunities or increase their likelihood of using high-cost alternative lenders.

In the aggregate, measuring credit availability can be used as a proxy for economic inclusion—the ability of individuals, regardless of background, to participate fully in the economic life of their community and country, typically through mainstream financial institutions. The percentage of people with a credit history can provide insight into how many people have access to loans, how many do not, and how this has changed over time, such as before the Great Recession versus after it. Measuring credit availability can also shed light on macroeconomic trends. Tighter credit restrictions can limit consumer spending, which in turn can have a negative impact on growth of the country’s gross domestic product (GDP).[1]

On the other hand, there can be dire consequences for debt performance when credit standards are too loose and consumers do not have the information they need to understand the risks they are taking. At a household level, borrowers can become trapped in a cycle of debt, defaulting on loans or depleting savings. On a larger scale, such situations can have drastic ramifications for the national economy, with the 2007–10 subprime mortgage crisis serving as the most recent example.[2] Studying the balance of these two concepts—credit access and debt performance—can help researchers and community leaders gauge the health and inclusivity of an important facet of the American economy.

This report provides a look at these important debt trends and debt performance across the state of Texas. A 5 percent nationally representative sample of consumer-level and loan-level data from the New York Federal Reserve Bank’s Consumer Credit Panel and Equifax—one of the country’s three main credit bureaus—were used for this report. This report is a follow-up to a 2018 Dallas Fed report on Dallas County and a precursor to three additional publications on credit in the Texas counties of Bexar, El Paso and Travis.[3] This series aims to provide a comprehensive view of credit access, loan volumes and delinquencies across the state.

The Credit Economy in Texas

Personal credit history, contained in a credit report, is essentially a factor that allows lenders to underwrite debt based on perceived risk. Aspects such as previous payment history (making on-time payments on other loans), credit utilization (how much debt is carried) and length of credit history all impact a lender’s prediction of the likelihood of a consumer’s timely repayment. Credit bureaus—Equifax, Experian, Transunion—use these factors to calculate a credit score for an individual, which lenders can use to make decisions about extending credit: to whom, at what cost and how much.

In Texas, 86.6 percent of adults age 18 and older had a credit file and credit score in the Equifax dataset as of 2017, the most recent year calculations are available.[4] This is down from 92 percent in 2006. This means that while 8 percent of adults in Texas were credit-invisible, i.e., without a scorable credit history, prior to the Great Recession in 2006, the rate climbed to nearly 13.5 percent 11 years later. Not having a credit score with one of the three credit bureaus can mean being excluded from credit access and from full participation in the mainstream economy. Across the nation, low-income consumers, as well as black and Latino consumers, are more likely to be credit-invisible, as are residents in southern states.[5] Texas has a higher rate of credit invisibility than the national average, likely due to its comparatively young and racially diverse demographics, large immigrant population, relatively high poverty rate and southern geographic location.[6],[7]

This report uses Equifax data to analyze four major types of consumer loans: credit card, auto, student and mortgage. These four types of loans make up about 95 percent of the loan volume in the state. Equifax calculates risk scores, typically known as credit scores, and groups them into four different categories: prime, near prime, subprime and deep subprime (Table 1). The majority of Texans with a credit report are prime borrowers, considered the least-risky type of borrower. Just under 30 percent of Texans with credit have scores below 620, considered riskier consumers.

Table 1: Credit Score Categories and Texas Borrowers, 2018

| Category | Credit score range | Share of Texas borrowers (percent) |

| Prime | 680 and above | 55.4 |

| Near prime | 620–679 | 16.0 |

| Subprime | 550–619 | 15.1 |

| Deep subprime | Below 550 | 13.4 |

| NOTE: Credit scores are based on Equifax Risk Score 3.0. Percentages may not add to 100 due to rounding. SOURCES: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; author’s calculations. | ||

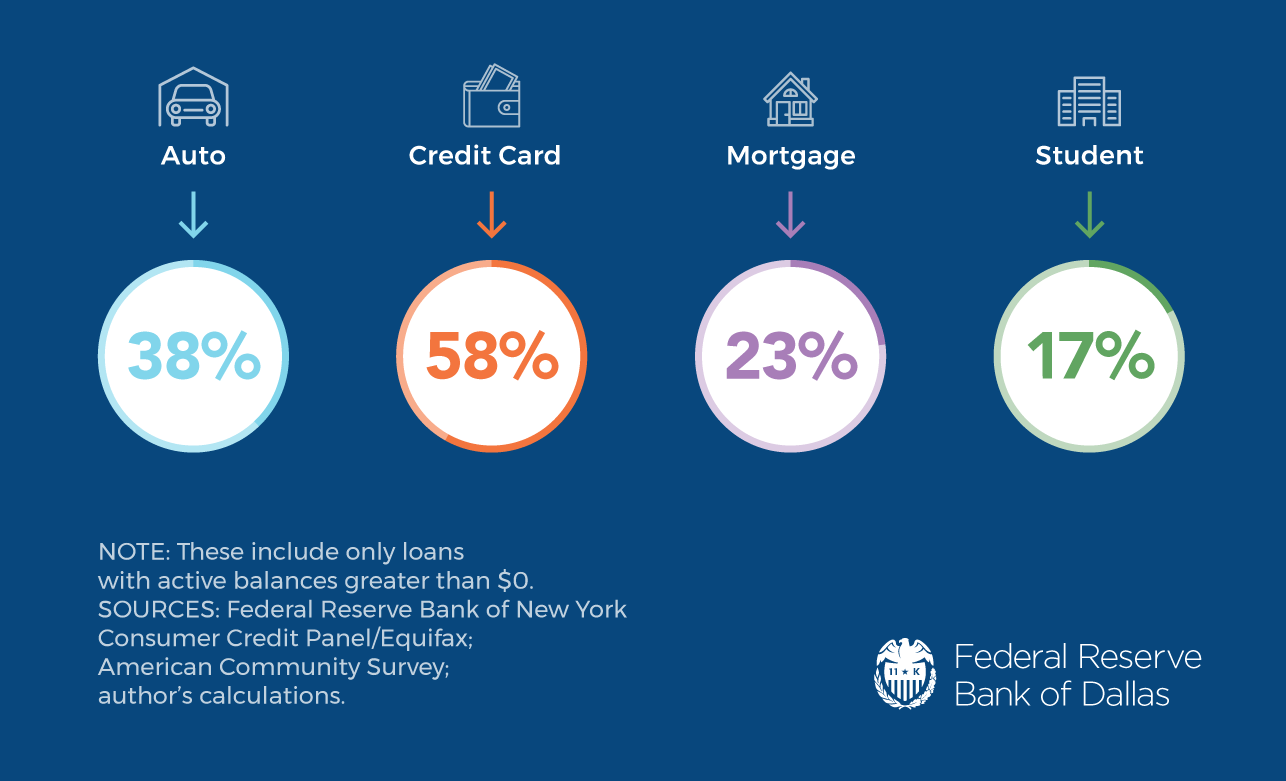

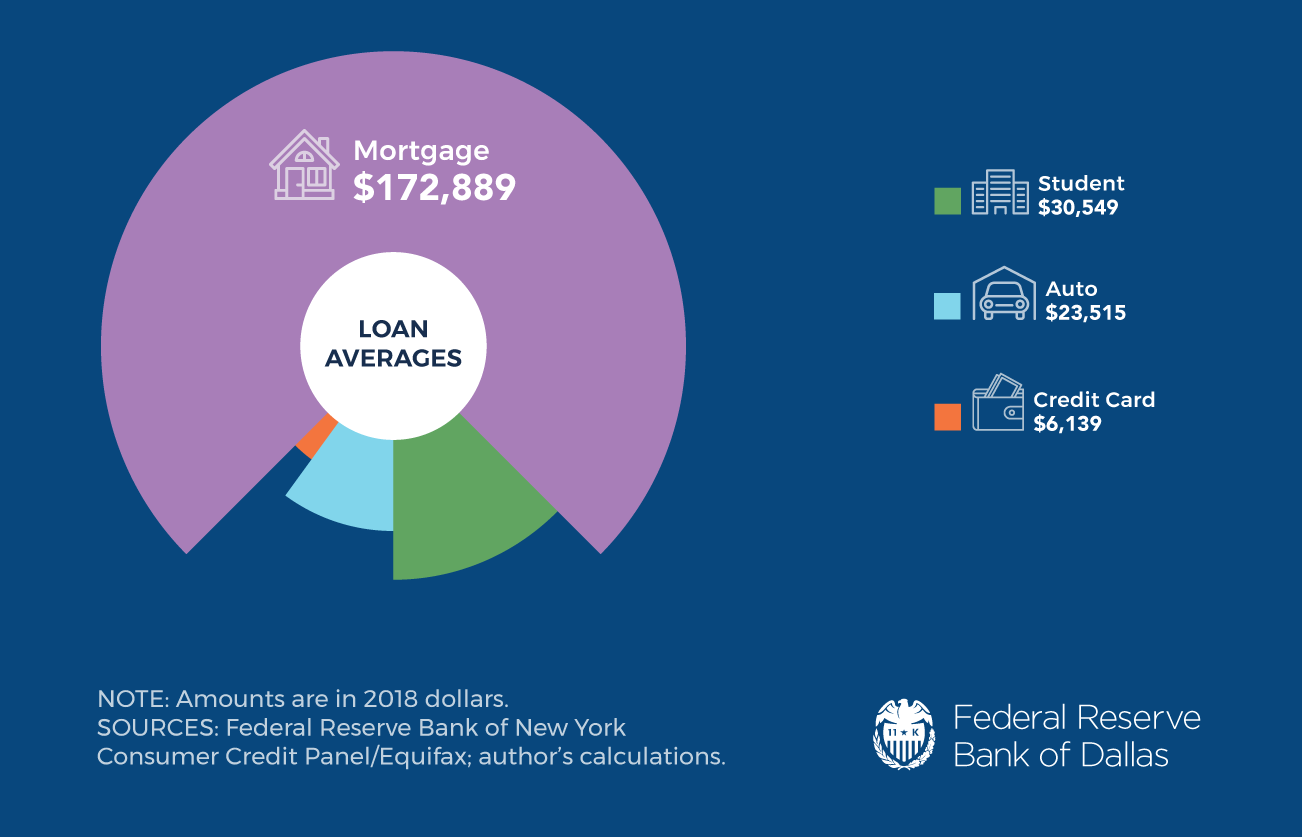

Among the four types of loans studied in this report, credit card debt is by far the most common type of loan in Texas, with nearly 60 percent of the state’s adult population carrying an active credit card balance (Figure 1). Nearly 40 percent have a car loan, and about a quarter of the state’s adults have mortgage debt. Relatively fewer adult Texans have student loans (17 percent), but this population is growing, with less than 11 percent of adults in 2006 holding student debt. The average loan amount is on the rise too, from $21,672 in 2006 to $30,549 in 2018, adjusting for inflation (Figure 2).

Figure 1: Most Texans Have Credit Card Balances*

*Adult population, 2017.[8]

Figure 2: For Texans with Student Debt, Average Amount Exceeds $30,000

This average student loan amount is more than the average car loan, which sits at about $23,515. The average balance carried for credit card holders is $6,139, and unsurprisingly, mortgage debt is the highest at $172,889 on average.

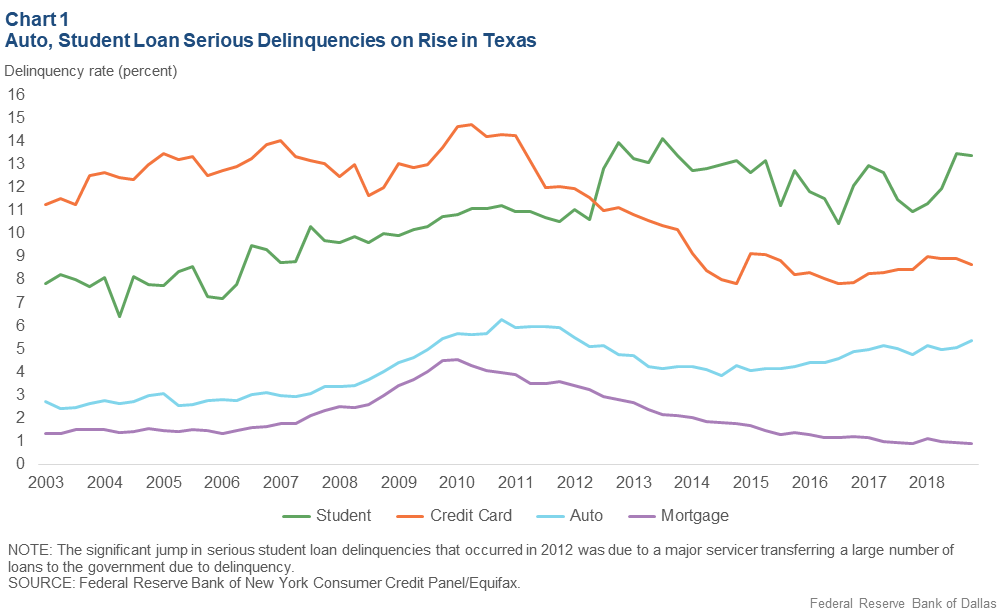

Chart 1 shows the statewide serious delinquency rate for the four types of loans starting in 2003. Loans are considered “seriously delinquent” if the debt holder is 90 or more days late on a payment. Credit cards had the highest serious delinquency rate before the Great Recession. Since then, the rate has dropped significantly, likely due in part to federal legislation passed in 2009 (see “Credit Card Debt”). Median credit card debt fell 14 percent in the past decade, while the average fell 23 percent, indicating a significant drop in large debt burdens.

The opposite is true for student loans. Student loan serious delinquency rates have been creeping steadily upward for over a decade, and median loan amounts per borrower increased 43 percent between 2006 and 2018, after adjusting for inflation. Recently, serious delinquency rates for student loans have remained high, much higher than any of the other three types of loans. Taken together, these trends have been a cause of concern for economists, community groups, borrowers and lenders. Given that a postsecondary credential generally leads to higher-paying jobs, striking a balance between access to student loans and low delinquency rates is important to preserving economic mobility in this country.[9],[10]

Serious delinquency rates for mortgage loans in Texas have always been lowest of the four, even during the Great Recession’s housing crisis. For a variety of reasons, Texas fared better in the mortgage crisis relative to other states.[11] Recently, the serious delinquency rate has fallen even lower than it was before the recession. Still, the shifts between loosening and tightening lending standards that have characterized the past 16 years have had ramifications for lower-income borrowers and should be monitored (see “Mortgage Debt”).

Since about 2015, the serious delinquency rate for car loans in Texas has slowly risen. Historically, the serious delinquency rate has also been relatively low in the state, with a bit of a rise during the recession before dipping back down. As of fourth quarter 2018, rates are nearing their recession peaks. Consumers often prioritize making a car loan payment above other loans, which gives cause for concern when car loan delinquencies increase.[12] In particular, this trend implies that some consumers are still struggling despite an otherwise strong economic climate.

Authors

- Emily Ryder Perlmeter

Community Development Advisor, Federal Reserve Bank of Dallas - Anna Crockett

Community Development Outreach Analyst, Federal Reserve Bank of Dallas - Garrett Groves

Vice President of Business & Industry Partnerships, Austin Community College

The information and views expressed in this report are the author’s and do not necessarily reflect official positions of the Federal Reserve Bank of Dallas or Federal Reserve System; nor do they constitute an endorsement of any organization or program.

Full report is available online: https://www.dallasfed.org/cd/cct/19ccttx.

Federal Reserve Bank of Dallas 2200 N. Pearl St., Dallas, Texas 75201 | 214.922.6000 or 800.333.4460