Federal and local resources help small businesses strive for new normal

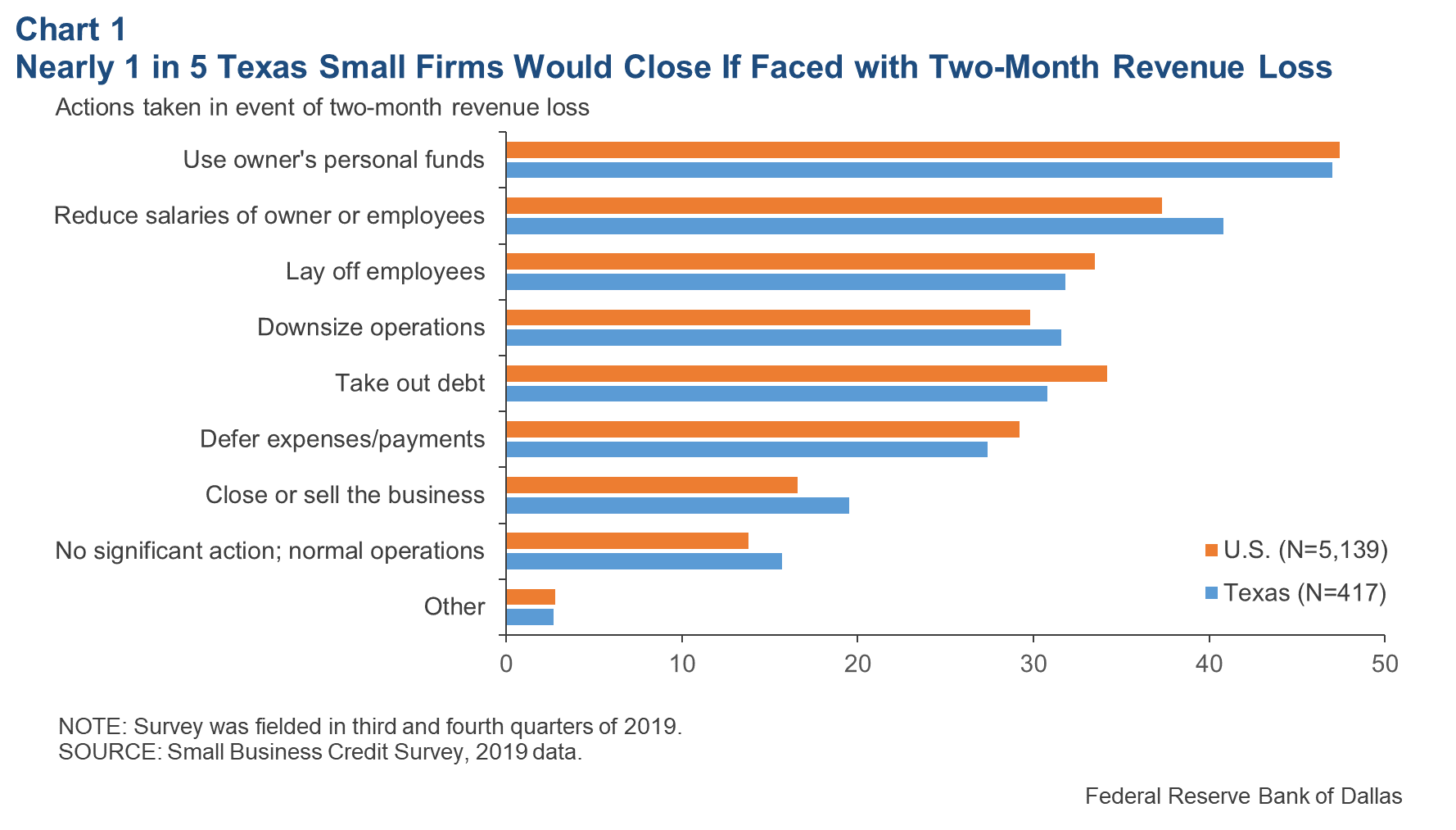

Despite the fact that local economies have partially reopened, small businesses across the country continue to reel from the impact of COVID-19. Revenue losses continue across communities and industries. Even before the crisis, many small firms were in a vulnerable position. In fact, according to the Federal Reserve’s Small Business Credit Survey, just 14 percent of U.S. firms in 2019 reported they had sufficient cash reserves to continue operating normally if faced with a two-month revenue loss. Texas small businesses fared a bit better with 16 percent reporting they had sufficient cash reserves in that scenario; but they also reported they were more likely to need to sell or close their business in that situation (Chart 1). At the time this survey was fielded, few could have predicted the severe and universal nature of the economic crisis that would hit just four months later.

In May, we released an in-depth look at the experiences of small business owners across Texas in the first month of the crisis. In the subsequent months, there have been updates to existing resources, and more initiatives have launched to support small firms across the country and state.

Paycheck Protection Program updates

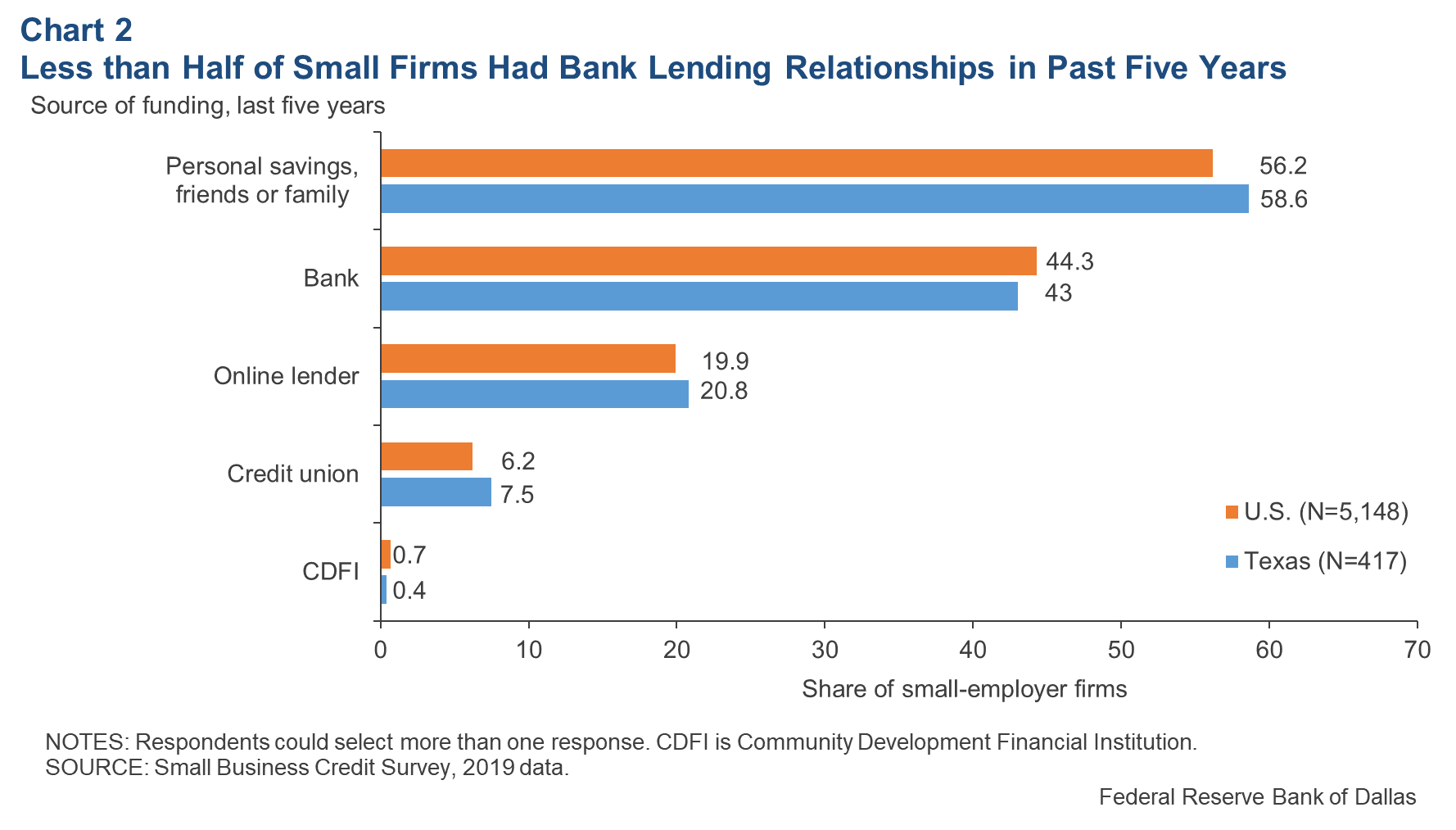

The $349 billion initial rollout of Paycheck Protection Program (PPP) funding in early April suffered some technical glitches and concerns regarding the types of firms reaping the benefits. Given that banks are typically required to undertake a firm vetting process when making loans but faced a tight timeline for disbursing PPP funds, a prior lending relationship appeared critical to receiving round one of PPP loans. This matters because prior bank lending relationships (beyond a traditional savings or checking account) are less prevalent for many small firms than one might expect—particularly among certain subsets like minority-owned businesses or microfirms. According to 2019 data from the Fed’s Small Business Credit Survey, just 44 percent of small-employer firms in the U.S. used a bank lender within the prior five years. At 43 percent, the Texas share was slightly smaller (Chart 2). Firms that did have such a bank relationship tended to be larger and were more likely to be white-owned.

Recognizing the need for both additional funds and a more-inclusive process, Congress passed an extra $310 billion in second-round PPP funding, including:

- A specific $30 billion set-aside for Community Development Financial Institutions (CDFIs), minority depository institutions, credit unions and community banks with assets less than $10 billion.

- An additional $30 billion reserved for banks with asset sizes between $10 billion and $50 billion.

Granular data are necessary to understand how well this second, more-targeted round of funding has reached all communities. Taking a significant step toward this goal, on July 6, the Small Business Administration (SBA) and the Treasury Department released loan-level data on the 4.9 million PPP loans made thus far.[1]

According to early analysis, Texas issued the second-largest aggregate loan amount, which at $41.1 billion, is only surpassed by California’s $68.2 billion. However, as a share of small business payroll, Texas falls squarely in the middle of the 50 states. PPP funds went to firms representing about 82 percent of small business payrolls in Texas—about halfway between Florida’s and Hawaii’s 96 percent and Virginia’s 72 percent. There are businesses in approximately 157 cities in Texas listed as receiving some amount of PPP funds. Determining the reach of dollars to minority-owned and/or woman-owned firms is much more challenging, given the significant number of PPP recipients who did not disclose firm ownership demographics.

Finally, a few additional regulatory shifts took place in June, loosening restrictions for small business borrowers:

- The coverage period was extended from just eight weeks to 24 weeks, which takes the program to the end of 2020.

- The requirement that 75 percent of funds be allocated for payroll, rents or utility costs was dropped to just 60 percent, making it easier for firms to qualify for loan forgiveness.

- The loan repayment period was extended to five years, as opposed to just two.

These first two changes retroactively apply to March 27, 2020, the date the Coronavirus Aid, Relief and Economic Security (CARES) Act was originally passed. The third change related to loan maturity only applies to loans made on or after June 5, 2020.

Additional national resources

Beyond the PPP, other resources exist at the federal level. Two important updates since publishing our May 12 article on small businesses and COVID include:

- Main Street Lending Program (MSLP): In April, the Federal Reserve announced a new lending program to help fill the needs of businesses that may be too large to qualify for the PPP, yet too small to access some of the financial relief options offered to large corporations, like the purchase of corporate bonds. Eligible businesses are considered either small or mid-sized, with up to 15,000 employees or revenues of $5 billion or less. Lender registration for the MSLP opened on June 15, and the Fed expects to purchase 95 percent of each issued loan, providing lender liquidity and sharing the risk. Unlike the PPP, MSLP loans are not forgivable. Principal payments are deferred two years, and interest payments are deferred for one year. Loan sizes are between $250,000 and $300 million.

- Economic Injury Disaster Loans (EIDL): Unlike the resources discussed above, EIDL has been a longstanding SBA program, normally intended to assist business owners in the aftermath of a natural disaster such as hurricanes or tornadoes. In March, Congress expanded eligibility by designating COVID as a national disaster. The maximum loan size is $2 million, and interest rates are 3.75 percent for small businesses and 2.75 percent for nonprofits. After being flooded with requests the first month, the SBA paused new applications but resumed them as of June 15. As of June 21, just under 1.8 million loans—representing over $113 billion—have been approved nationally.

Targeted local programs

Beyond resources at a national level, many cities across Texas have recognized the need for additional support in their small business communities. In Dallas, for instance, a multisector approach led to the development of the Revive Dallas Small Business Relief Fund. Private businesses, the Communities Foundation of Texas (CFT), LiftFund and the Dallas Entrepreneur Center Network all play a role in the fund. The fund specifically targets businesses in Dallas that employ a maximum of 15 employees and that have experienced at least a 15 percent loss of revenue since the onset of the COVID crisis. A majority of loans are dedicated to women-owned or minority-owned firms. With 0 percent interest, they are fully forgivable if participants meet certain requirements, including participating in a mentorship program and creating a 2021 budget.

Sejal Desai, business engagement director for CFT, the fund’s fiscal sponsor, notes the goal of the collaborative was to provide small businesses not solely with funding but also “wrap-around, full-service support.” She says, “Many businesses can use not only the money but also mentoring from business leaders who are successfully managing to pivot during these unprecedented and challenging times.” The Revive Dallas fund plans to total $5 million, nearly half of which has already been raised.

Various other local resources exist across the state. Some of these include:

- Travis County Thrive

- Support Lubbock Fund

- Wood County Coronavirus Relief Fund

- Amarillo Is Open

Looking to the past and the future

A June 2020 Dallas Fed analysis highlights the particular challenges small businesses face, including the fact that in normal economic times, only about half of startups survive more than five years. Small firms tend to struggle more with credit access than larger firms, a phenomenon that is amplified in times of economic crisis. In fact, the analysis points out that small businesses suffered greater job losses than larger ones during the two recessions of the 2000s, and small business lending fell during the Great Recession and stayed below prerecession levels.

It’s clear that small firms—and the overall economy—are once again facing a very significant challenge. What remains to be seen is how effective the historic federal economic relief packages will be at stemming the widespread revenue losses for small firms throughout the U.S. and Texas and how equal the recovery may be among communities.

Notes

- For loan amounts $150,000 and above, exact amounts are not disclosed; ranges are listed in lieu of precise dollar amounts. For loans under $150,000, business names and addresses are not listed. Regardless of the lack of complete and precise loan-level information, this data release will help approximate the reach of the PPP across various communities, including cities, counties and ZIP codes.

About the author

Emily Ryder Perlmeter is a policy analyst in the Integrated Policy Department at the Federal Reserve Bank of Dallas. She was formerly a senior advisor in the Community Engagement and Development Department.