Small business hardships highlight relationship with lenders in COVID-19 era

The COVID–19 outbreak has drastically disrupted small businesses and their lenders. Millions of small enterprises are simultaneously confronting health risks, reduced demand and supply chain issues. Many were ordered closed or told they could only partially operate, creating additional financial strain.

The most vulnerable—restaurants, nonessential retailers and personal services—are in sectors that typically maintain low cash buffers.[1] Within days of public health officials calling for social distancing, less than two-thirds of American businesses remained open.[2]

Small businesses have struggled to arrange short-term funding to meet expenses, while their lenders have responded cautiously. Federal government stimulus programs have offered a measure of relief.

Some lenders, attempting to navigate an uncertain environment, tightened underwriting criteria.[3] Still others paused making loans not backed by the federal government.

Recessions over the past two decades provide some guidance on the funding challenges small businesses face.

Economic Activity Generators

Small businesses—those with fewer than 500 employees, according to the Small Business Administration (SBA)—accounted for 99.9 percent of U.S. firms and 99.8 percent of Texas firms in 2017.[4] Texas small businesses boast a larger share of exporters and minority-owned-business employees than their counterparts in the nation as a whole.[5]

As a vital part of the economy, these small businesses generate almost two-thirds of net new jobs nationally, account for nearly half of private sector employees and produce one-third of exports. These companies tend to be more productive than big businesses in terms of contribution to gross domestic product (GDP) per payroll dollar.[6]

More than 90 percent of small businesses have fewer than five employees. Nonemployer firms—often the self-employed—account for about four-fifths of small businesses. Although most are profitable, their margins aren’t necessarily predictive of survival.[7] Businesses with sufficient cash or liquidity, regular cash flow and access to affordable loans are more likely to survive volatile times.

Loan Program Lifeline

Reacting to the COVID–19 crisis, the federal government and the Federal Reserve collectively responded with fiscal stimulus, lending programs and monetary policy to bring relief, including programs to support employee retention through guaranteed loans or grants.[8]

In addition to payment waivers for existing SBA borrowers and direct Economic Injury Disaster Loans with a forgivable loan advance of $10,000, the Coronavirus Aid, Relief, and Economic Security (CARES) Act provided $349 billion in aid (with another $310 billion on April 24) and authorized the SBA to create a platform for the Paycheck Protection Program (PPP).

The program provides small businesses low-interest, partially forgivable, two-year loans to maintain payrolls and pay other expenses.[9] PPP funding is largely distributed through banks and other private channels and aims to quickly inject hundreds of billions of dollars in liquidity into small businesses.

To protect lenders against liquidity risk, the Federal Reserve established a lending facility to depository institutions on April 9. The Fed expanded eligibility to all PPP lenders, taking PPP loans as collateral on April 30. The Federal Reserve also established the Main Street Expanded Loan Facility to offer more liquidity to small and medium-sized enterprises as a supplement to the PPP program.[10] These measures were intended to provide more assurance to lenders and boost available funds.

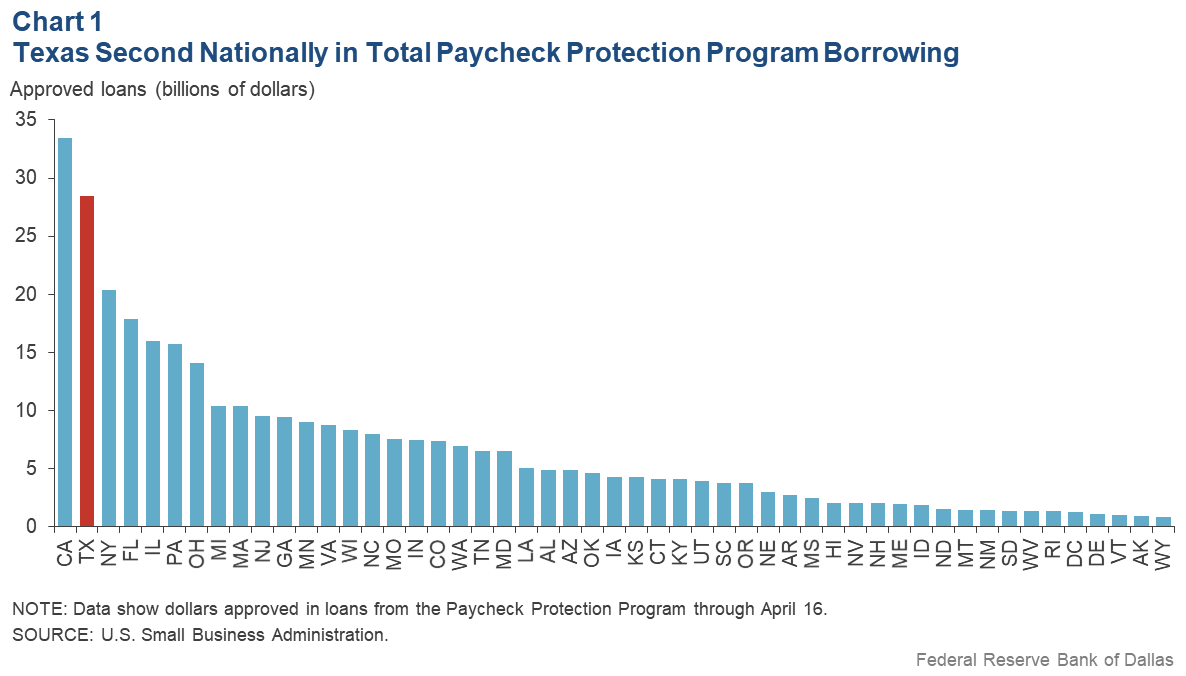

Take-up of the PPP was rapid. The program ran through its initial $349 billion in two weeks. In this first wave, the SBA made 1.7 million loans totaling about $342 billion through 4,975 lenders. Seventy-four percent of loans were for $150,000 or less. Texas was No. 2 among the states in PPP dollars borrowed ($28 billion) through April 16, behind only California, according to the SBA (Chart 1).

However, the amount borrowed relative to state GDP placed Texas 40th among states (1.5 percent of state GDP), with less-populous states such as Maine, Vermont and Montana in the lead at close to 3 percent.

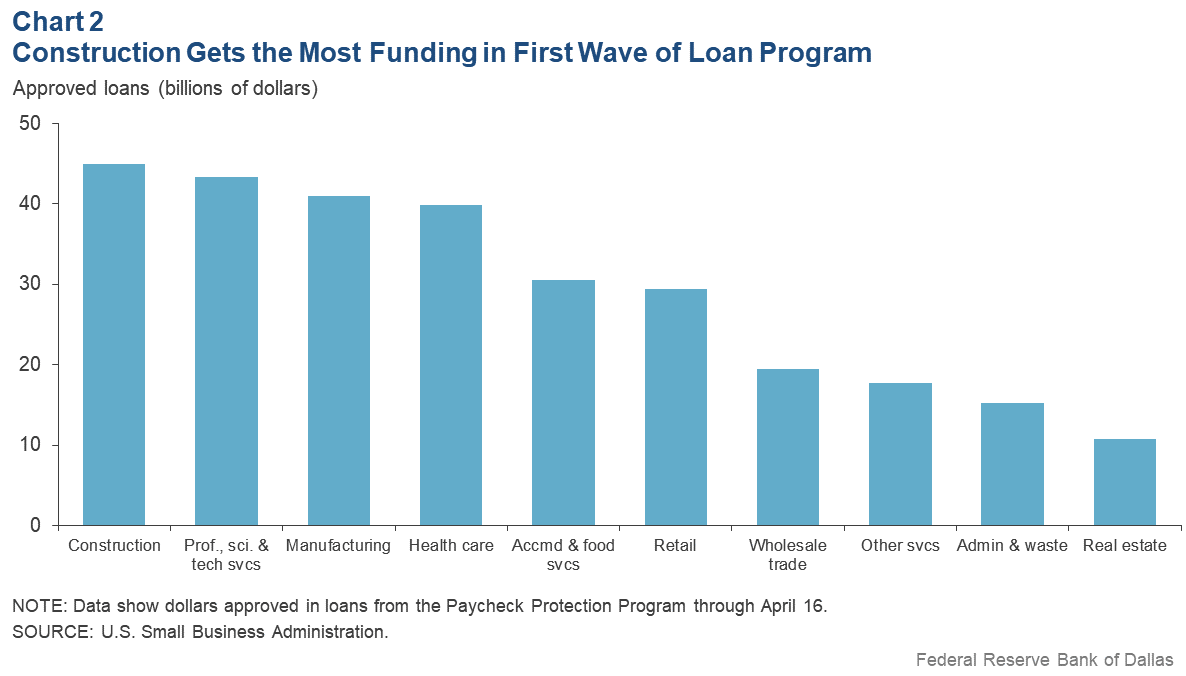

By industry, construction borrowed the most nationally, followed by professional, scientific and technical services; manufacturing; and health care and social assistance (Chart 2). Accommodation and food services was in fifth place, and retail trade was sixth.

The PPP loan effort drew on the infrastructure of the SBA’s flagship 7(a) loan program, which provides partial guarantees to small businesses annually during normal times. The program typically accounts for less than 5 percent of the total small business lending market. PPP loans are 100 percent guaranteed by the SBA and 20 times larger than SBA 7(a) funding. Eligibility is broadened from for-profit businesses to include all businesses with 500 or fewer employees.[11] Compared with the usual underwriting criteria for SBA 7(a) loans, PPP loans waived the collateral requirements and only asked lenders to conduct a minimal credit check.

To quickly disburse funds, the PPP program worked with more institutions. Usually, only certified lenders—typically banks and a small number of nonbanks and credit unions—can make SBA 7(a) loans. Under PPP, all federally insured depository institutions and credit unions, and Farm Credit System institutions can participate.[12]

The Treasury, seeking to further boost the number of outlets disbursing funds, released a new application for nonbank program lenders on April 9.

Many smaller banks moved faster than some large banks to process applications. Moreover, a substantial number of initial loans occurred between borrowers and lenders with an existing relationship.[13]

The first-wave PPP did not entirely align with the areas most affected by COVID–19. Lender participation played an important role. The 21 largest banks made 14.4 percent of initial PPP loans, a much smaller share of small business lending than prior to COVID–19 (59 percent).[14] Small banks filled the gap by making about 41 percent of PPP loans, as of May 16.[15]

Small Business Funding

Running a small business involves substantial uncertainty. Hundreds of thousands of small businesses fail each year. Only about half of startups survive more than five years, and just one-third last beyond 10 years.[16] The median small business has enough cash on hand to cover 27 days of cash outflows, and retained earnings are usually insufficient to operate or expand.[17]

Small business lenders are generally cautious, often charging relatively high interest rates to offset credit risk. Thus, many business owners draw on personal funds, borrow from friends and families, take out home equity, use a personal or business credit card, or borrow from business partners before seeking commercial loans.

The Federal Reserve Banks’ 2019 Small Business Credit Surveys showed that in more-normal times, while the majority of small firms experienced financing shortfalls, only 26 percent of nonemployer firms (usually the self-employed) and 43 percent of employer firms applied for external credit (Table 1).[18]

Table 1: Small Businesses Generally Credit Constrained

| Nonemployer firms (percent) |

Employer firms (percent) |

|

| Have financial shortfalls | 61 | 54 |

| Applied for external credit | 26 | 43 |

| Received some/all if applied | 62 | 47 |

| Have outstanding debt | 46 | 70 |

| Debt averse | 23 | 14 |

| Discouraged to apply | 13 | 9 |

| NOTES: Nonemployer firms have no paid employees and are usually self-employed individuals. The survey had 6,614 responses from small employer firms and 5,841 responses from nonemployer firms. SOURCE: Federal Reserve Banks’ Small Business Credit Surveys, 2019. |

||

Many cited debt aversion or being discouraged to apply as reasons for not seeking loans. Among those that applied, many failed to receive funding. According to employer firms that attempted to get credit, about 57 percent sought $100,000 or less, 35 percent applied for $100,000 to $1 million and 8 percent asked for $1 million or more.

Among all loan-seeking businesses—which often look to borrow at several institutions—about 49 percent applied to large banks (assets exceeding $10 billion), 44 percent to small banks, 35 percent to online nonbanks and 14 percent to credit unions or community development financial institutions. Small banks were more likely than large banks to approve loans.

Challenges for Lenders

Two main factors contribute to small businesses’ unmet credit needs. Small business loans aren’t as profitable to lenders as other types of loans. Origination and servicing costs for small loans are comparable to larger loans, but interest revenue is much less.

The other challenge is accurately assessing small businesses’ credit risk. While traditional credit scoring models can effectively predict repayment patterns for consumer loans—mortgages, auto loans and credit cards—these models less ably assess business prospects and the repayment capacity of small firms, especially newer enterprises.

Historically, community banks have specialized in small business lending because lenders in physical proximity can conveniently learn more about prospective borrowers through personal relationships and face-to-face interactions and collect more “soft” information to assist underwriting. Loans made from distant locations tend to be riskier.

These challenges nevertheless provide opportunities for lending innovations. “Fintechs,” a class of banks and nonbanks that use new technologies to make loans, have developed rapidly in the past decade. Advanced data integration technology and analytical tools allow lenders to efficiently process a broad range of borrower information. Data once gathered informally through personal contact have become quantifiable and easily transferrable for automated, online underwriting.

Fintech lending is in an early stage of development and hasn’t been rigorously tested, leaving the majority of small business loans still locally originated. Nonbank fintech companies accounted for $6.5 billion in loans with a small business focus in 2017.[19] This represented less than 2 percent of the small business lending market, although it was the fastest-growing segment in fintech lending relative to student loan refinance and personal loans.

Lending During Downturns

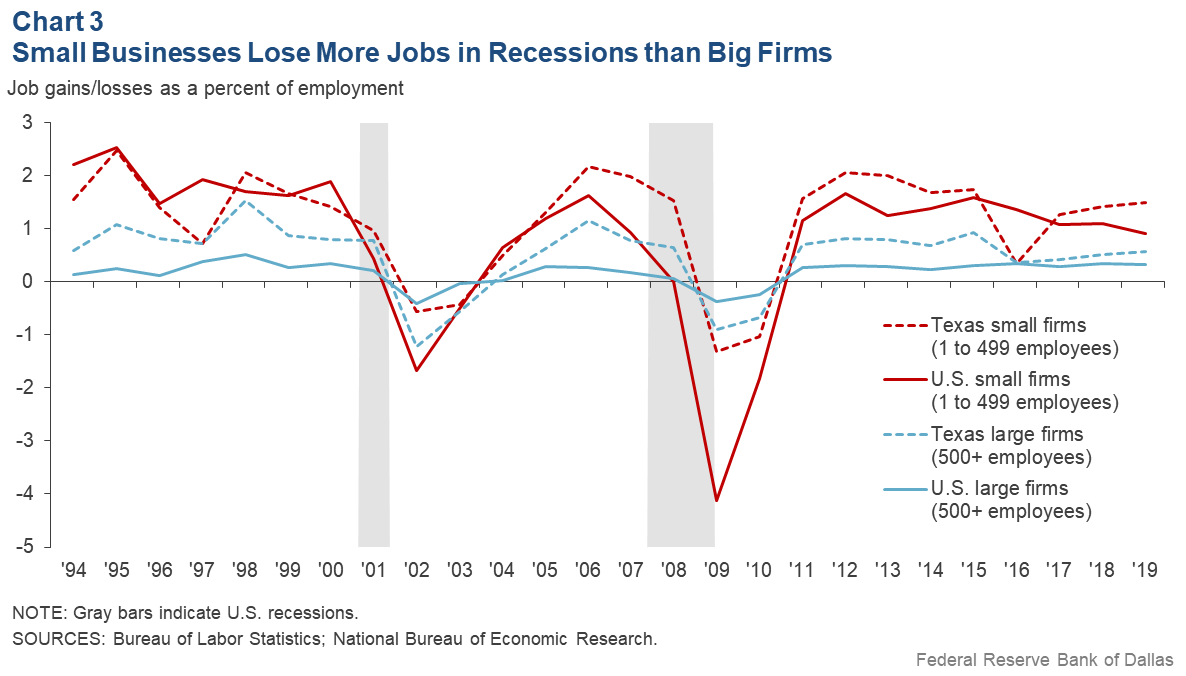

Small businesses are less resilient in economic downturns and suffered more job losses than larger companies the previous two recessions in the 2000s (Chart 3). Small businesses also subsequently rebounded with greater job gains.

Small businesses in Texas contracted more than larger firms during the Great Recession, a pattern that repeated itself nationwide. They were not as affected following the earlier dot-com bust. State and national trends suggest that small businesses may experience greater weakness during a credit crunch arising from a financial crisis.

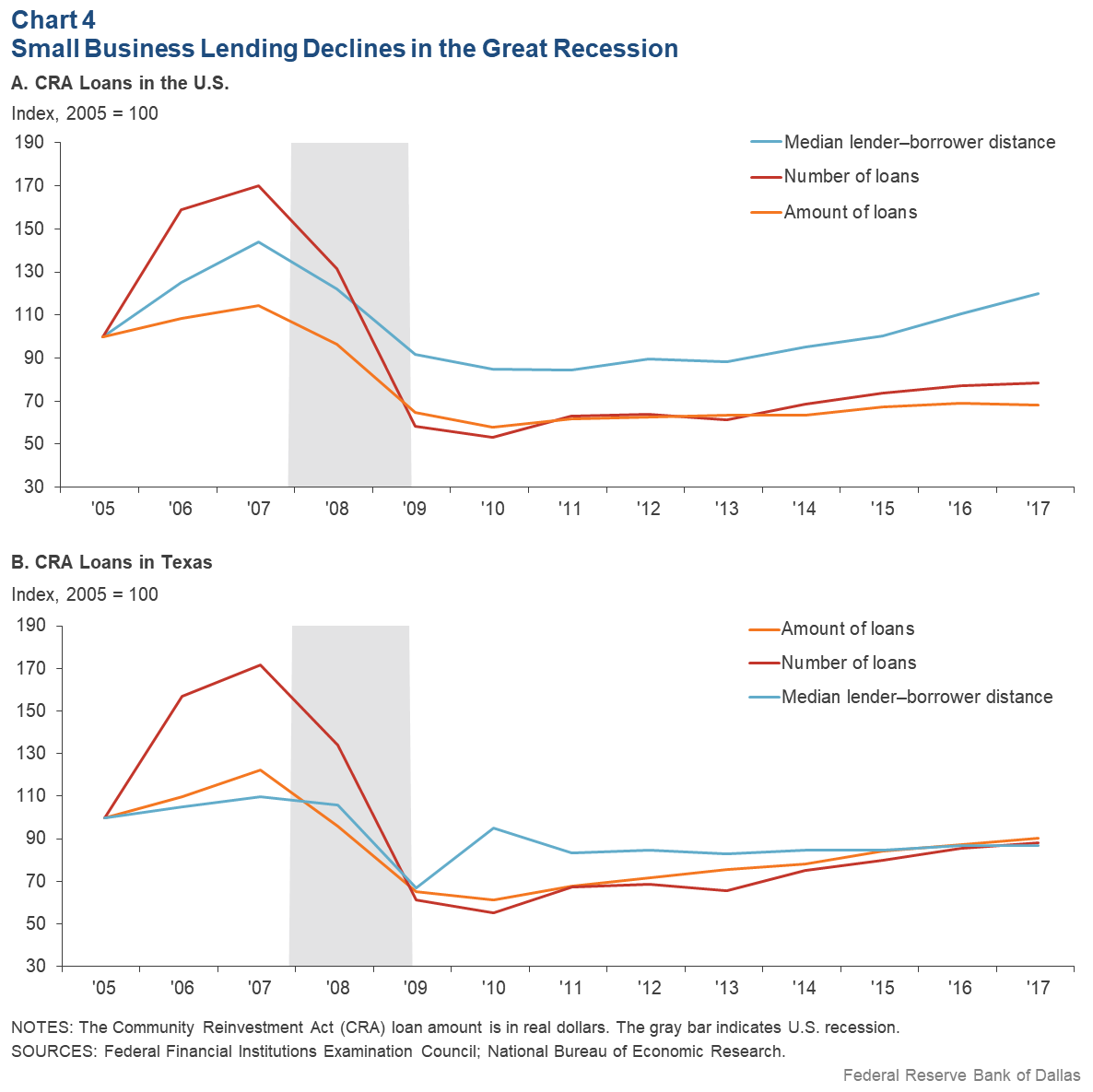

When the downturn is systemic and businesses need liquidity the most, lenders are often also especially constrained. Small business lending—measured by the number and amount of Community Reinvestment Act (CRA) loans relative to the levels in 2005—rose before the Great Recession, declined sharply afterward, and during the gradual recovery remained below prerecession levels (Chart 4).[20]

Another indicator of lending risk, the median physical distance between borrowers and lenders, follows a similar trend. During periods of stress, lenders from outside a market typically do not continue to service firms with which they do not have a longer-term relationship.

With businesses and lenders confronting financial challenges arising from COVID–19, the SBA’s fully guaranteed PPP loans help bridge the liquidity gap. In many cases, businesses initially sought PPP funding through community banks and large banks with local branches.

The lack of a longstanding relationship likely stymied many PPP applications, and an overwhelmed system derailed others. Online, nonbank fintech lenders provided an alternative if they were previously certified SBA lenders or had been quickly approved for program participation.[21]

Public–Private Partnership

Small businesses—key contributors to the economy—require credit access, especially during difficult times. Social distancing mandates to contain the COVID–19 spread and protect public health have damped demand for the services and products of small businesses. This poses an unprecedented threat. Small businesses need rapid financing or cash assistance to survive.

Loan programs in the COVID–19 federal fiscal package provide funding to help small businesses cope with the economic upheaval. Traditional banks and fintech lenders are dealing with the challenges to keep small businesses alive until those enterprises can more fully reopen. The crisis will test the capacity of the public–private partnership in small business lending.

Notes

- “Place Matters: Small Business Financial Health in Urban Communities,” by Carlos Grandet, Chris Wheat and Diana Farrell, JPMorgan Chase Institute, September 2019.

- Data are from Homebase’s survey of over 60,000 businesses and 1 million hourly employees active in the U.S. in January 2020, (accessed May 11, 2020).

- “People Need Loans as Coronavirus Spreads. Lenders Are Making Them Tougher to Get,” by AnnaMaria Andriotis and Peter Rudegeair, Wall Street Journal, March 28, 2020.

- Data are from the Census Bureau, Statistics of U.S. Businesses, (accessed April 27, 2020).

- For more information, see “2019 Small Business Profiles for the States and Territories,” Small Business Administration (SBA) Office of Advocacy, April 2019.

- For more information, see "Small Business GDP 1998–2014," by Kathryn Kobe and Richard Schwinn, SBA Office of Advocacy, December 2018.

- See note 1.

- The Coronavirus Preparedness and Response Supplemental Appropriations Act, Families First Coronavirus Response Act, and Coronavirus Aid, Relief, and Economic Security (CARES) Act were signed into law in March 2020.

- Although the SBA has waived its “no credit elsewhere” test, the SBA and Treasury still require borrowers to certify in good faith that their PPP loan request was necessary under the current circumstances.

- Main Street Lending Program, Board of Governors of the Federal Reserve System, accessed May 11, 2020.

- Businesses in the hotel and food services industries (NAICS code 72) or franchises in the SBA’s franchise directory that receive financial assistance from small business investment companies licensed by the SBA can have more than 500 employees if they meet applicable SBA employee-based size standards for those industries.

- “The CARES Act Works for All Americans,” U.S. Department of the Treasury, accessed May 11, 2020.

- “Giant U.S. Lenders Outpaced by Rivals in Small Business Rescue,” by Hannah Levitt, Bloomberg, April 17, 2020.

- “Did the Paycheck Protection Program Hit the Target?” by Joao Granja, Christos Makridis, Constantine Yannelis and Eric Zwick, University of Chicago, Becker Friedman Institute for Economics Working Paper no. 2020–52, May 2020.

- "Paycheck Protection Program (PPP) Report, Approvals Through 05/16/2020,” Small Business Administration, accessed May 27, 2020.

- For more information, see “Small Business Facts,” SBA Office of Advocacy, June 2012.

- For more information, see “Cash is King: Flows, Balances, and Buffer Days: Evidence from 600,000 Small Businesses,” by Diana Farrell and Chris Wheat, JPMorgan Chase Institute, September 2016.

- Data are from the Small Business Credit Survey, Federal Reserve Banks (accessed May 11, 2020).

- For more information, see “2018 U.S. Digital Lending Market Report,” by Nimayi Dixit, S&P Global Market Intelligence, November 2018.

- About $265.4 billion in loans were originated or purchased in 2017, according to Community Reinvestment Act (CRA) data. The CRA requires all banks and bank holding companies with total assets exceeding $1 billion (2005 dollars) to report loans; it is estimated to represent 70 percent of all small business bank lending.

- As a measure of online lending activity, in 2017, 16 percent of SBA loans were originated with more than 100 miles between borrower and branch, and 4 percent of loans were originated by an institution other than a bank or credit union. See “Remote Competition and Small Business Loans: Evidence from SBA Lending,” by Wenhua Di and Nathaniel Pattison, Federal Reserve Bank of Dallas Working Paper no. 2003, January 2020.

About the Authors

Southwest Economy is published quarterly by the Federal Reserve Bank of Dallas. The views expressed are those of the authors and should not be attributed to Banco de México, the Federal Reserve Bank of Dallas or the Federal Reserve System.

Articles may be reprinted on the condition that the source is credited to the Federal Reserve Bank of Dallas.

Full publication is available online: www.dallasfed.org/research/swe/2020/swe2002.