Texas Service Sector Growth Weakens Further in May

Texas Service Sector Outlook Survey

Texas Service Sector Growth Weakens Further in May

For this month’s survey, Texas business executives were asked supplemental questions on supply-chain disruptions and costs. Results for these questions from the Texas Manufacturing Outlook Survey, Texas Service Sector Outlook Survey and Texas Retail Outlook Survey have been released together. Read the special questions results.

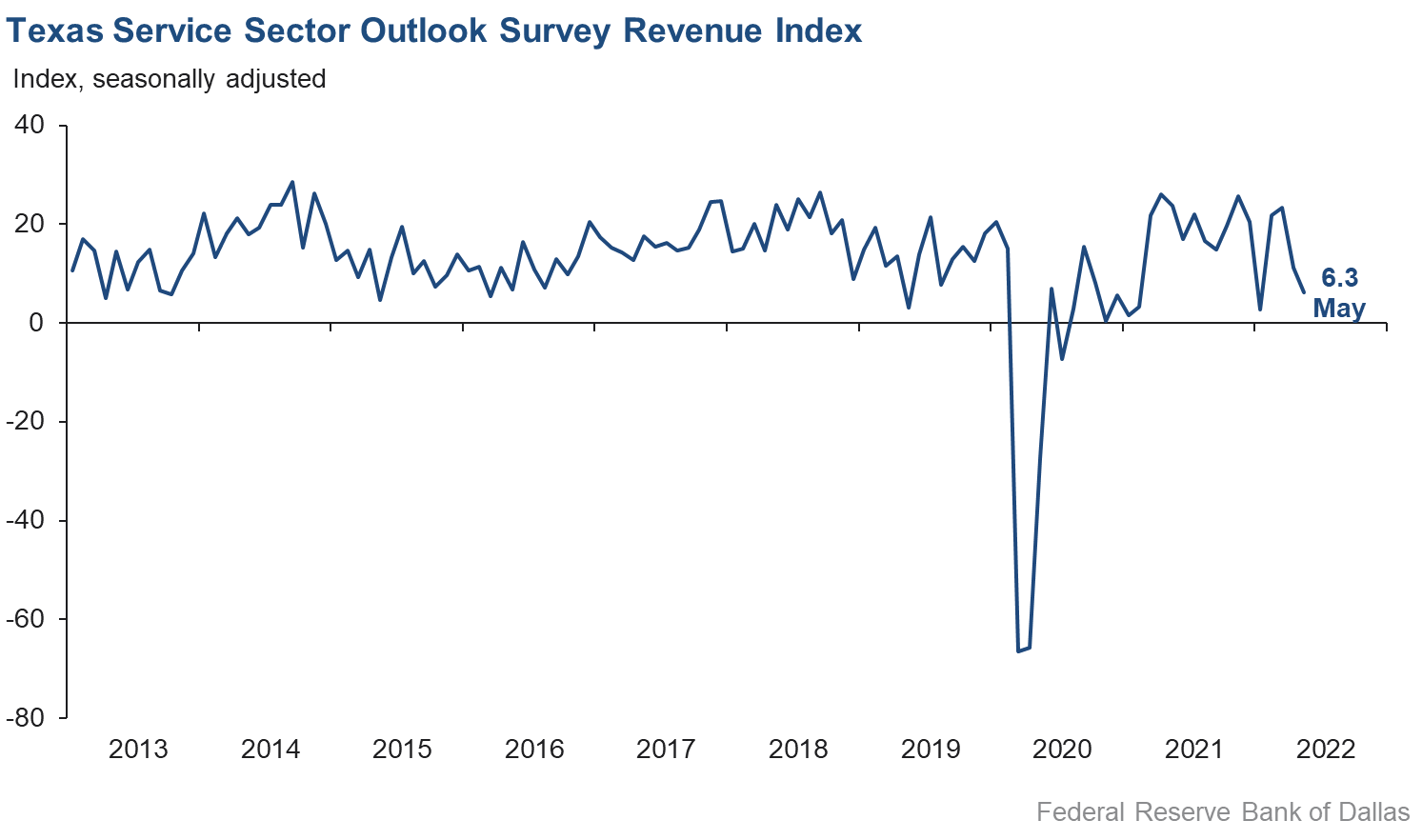

Activity in the Texas service sector decelerated in May, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, declined from 11.2 in April to 6.3 in May, as the share of firms reporting declining revenues increased from 18.5 percent to 21 percent.

Labor market indicators moderated, as growth in employment and hours worked declined compared with April. The employment index fell from 14.5 to 8.1—its lowest level since February 2021—while the part-time employment index was unchanged at 3.0. The hours worked index declined three points to 5.6—tied with a September 2021 low.

Perceptions of broader business conditions were largely unchanged in May, although uncertainty increased sharply. The general business activity index fell from 8.2 to 1.5, a reading indicative of almost no net change, as the 20 percent share of firms noting a worsening of business activity nearly matched the share reporting an improvement in activity. The company outlook index dipped from 2.4 to 0.9, while the outlook uncertainty index surged six points to 25.2—its highest reading since July 2020.

Price pressures remained near record highs in May, while wage growth accelerated slightly. The selling prices index softened one point to 32.6, with 36 percent of respondents noting monthly price increases, while the input prices index was unchanged at 53.5. The wages and benefits index added two points to rise to 35.0, only slightly off a record 37.4 reading in January 2022.

Respondents’ expectations regarding future business activity were markedly less optimistic compared with April. The future general business activity index fell into negative territory at -3.9, its first negative reading in nearly two years, and the future revenue index declined nearly 12 points to 35.5. Other future service sector activity indexes such as employment and capital expenditures remained in positive territory, suggesting expectations for continued growth over the second half of the year.

Texas Retail Outlook Survey

Texas Retail Sales Continue to Decline in May

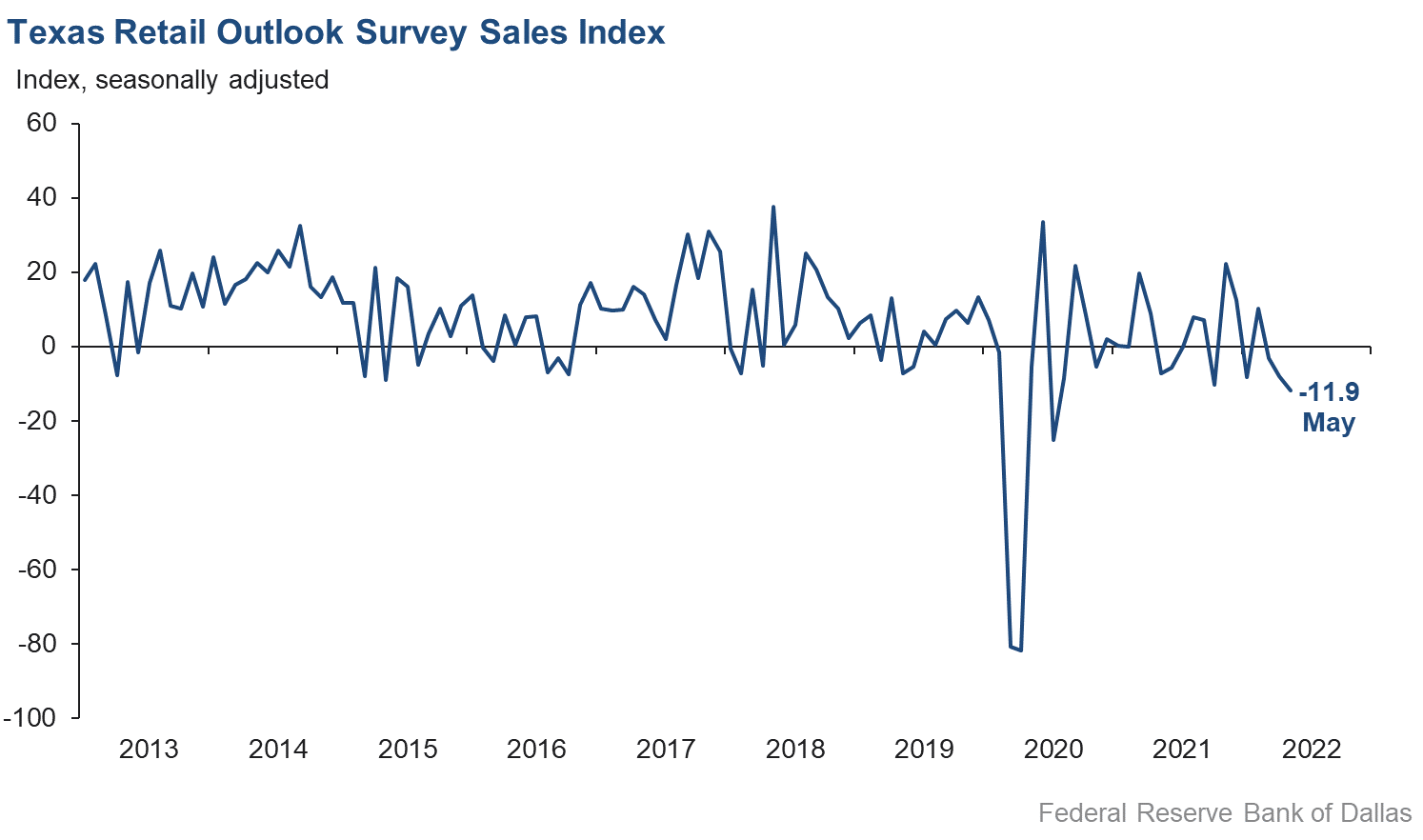

May retail sales activity continued to deteriorate, according to business executives responding to the Texas Retail Outlook Survey. The sales index, a key measure of state retail activity, weakened by four points to -11.9 in May. Retailers’ inventories held roughly flat, as the inventories index was steady at -1.3.

Retail labor market indicators plateaued in May. The employment index declined over eight points to 0.8—suggesting no net change in jobs—while the part-time employment index similarly declined to a neutral reading of 0.2. The hours worked index slipped one point to 1.4, suggesting little net change in hours worked for retail employees.

Retailers’ perceptions of broader business conditions were negative compared with April. The general business activity index shed nearly five points to -3.2, while the company outlook index held in negative territory at -4.1. The outlook uncertainty index increased from 14.6 to 18.2, with 32 percent of respondents noting greater uncertainty.

Retail price and wage pressures eased but were still at historically elevated levels in May. The selling prices index fell 12 points to 42.5, while the input prices index dropped five points to 50.1. The wages and benefits index dipped three points to 31.1, though 36 percent of respondents still reported increasing labor compensation over the month compared with just 5 percent reporting a decrease.

With a third consecutive month of declining retail activity, expectations for future growth continued to ease. The future general business activity index fell two points to -3.5—its worst reading in nearly two years—while the future sales index plunged 17 points to 18.3. Other indexes of future retail activity held mostly steady, suggesting expectations for continued growth for the rest of 2022.

The Texas Retail Outlook Survey is a component of the Texas Service Sector Outlook Survey that uses information only from respondents in the retail and wholesale sectors.

Next release: June 28, 2022

Data were collected May 17–25, and 274 Texas service sector business executives, of which 44 were retailers, responded to the survey. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease. Data have been seasonally adjusted as necessary.

Texas Service Sector Outlook Survey

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 6.3 | 11.2 | –4.9 | 11.3 | 22(+) | 27.7 | 50.9 | 21.4 |

Employment | 8.1 | 14.5 | –6.4 | 6.5 | 22(+) | 18.3 | 71.5 | 10.2 |

Part–Time Employment | 3.0 | 2.9 | +0.1 | 1.6 | 18(+) | 8.7 | 85.6 | 5.7 |

Hours Worked | 5.6 | 9.5 | –3.9 | 2.8 | 21(+) | 11.3 | 83.0 | 5.7 |

Wages and Benefits | 35.0 | 33.0 | +2.0 | 15.3 | 24(+) | 37.4 | 60.2 | 2.4 |

Input Prices | 53.5 | 54.2 | –0.7 | 26.6 | 25(+) | 57.0 | 39.5 | 3.5 |

Selling Prices | 32.6 | 33.7 | –1.1 | 6.8 | 22(+) | 36.4 | 59.8 | 3.8 |

Capital Expenditures | 14.7 | 13.2 | +1.5 | 10.0 | 21(+) | 20.3 | 74.1 | 5.6 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 0.9 | 2.4 | –1.5 | 5.6 | 4(+) | 18.5 | 63.9 | 17.6 |

General Business Activity | 1.5 | 8.2 | –6.7 | 4.1 | 17(+) | 21.0 | 59.5 | 19.5 |

| Indicator | May Index | Apr Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 25.2 | 19.2 | +6.0 | 11.8 | 12(+) | 34.0 | 57.2 | 8.8 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 35.5 | 47.0 | –11.5 | 38.0 | 25(+) | 48.9 | 37.7 | 13.4 |

Employment | 32.9 | 33.0 | –0.1 | 23.0 | 25(+) | 38.7 | 55.5 | 5.8 |

Part–Time Employment | 8.6 | 11.5 | –2.9 | 7.0 | 24(+) | 14.0 | 80.6 | 5.4 |

Hours Worked | 8.8 | 7.3 | +1.5 | 6.1 | 25(+) | 12.5 | 83.8 | 3.7 |

Wages and Benefits | 50.5 | 52.3 | –1.8 | 36.9 | 25(+) | 51.6 | 47.3 | 1.1 |

Input Prices | 61.9 | 59.6 | +2.3 | 44.2 | 185(+) | 64.5 | 32.8 | 2.6 |

Selling Prices | 40.4 | 41.6 | –1.2 | 24.1 | 25(+) | 45.4 | 49.5 | 5.0 |

Capital Expenditures | 28.5 | 27.7 | +0.8 | 23.6 | 24(+) | 34.1 | 60.4 | 5.6 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 0.2 | 14.5 | –14.3 | 17.0 | 22(+) | 22.5 | 55.2 | 22.3 |

General Business Activity | –3.9 | 6.5 | –10.4 | 14.1 | 1(–) | 24.4 | 47.3 | 28.3 |

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Retail (versus previous month) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | –11.9 | –7.9 | –4.0 | 5.3 | 3(–) | 18.6 | 50.9 | 30.5 |

Employment | 0.8 | 9.3 | –8.5 | 2.0 | 10(+) | 12.9 | 75.0 | 12.1 |

Part–Time Employment | 0.2 | 5.7 | –5.5 | –1.5 | 15(+) | 9.2 | 81.8 | 9.0 |

Hours Worked | 1.4 | 2.5 | –1.1 | –1.6 | 4(+) | 11.5 | 78.4 | 10.1 |

Wages and Benefits | 31.1 | 34.2 | –3.1 | 10.7 | 22(+) | 36.1 | 58.9 | 5.0 |

Input Prices | 50.1 | 55.3 | –5.2 | 21.6 | 25(+) | 60.3 | 29.5 | 10.2 |

Selling Prices | 42.5 | 54.6 | –12.1 | 13.4 | 24(+) | 54.3 | 33.9 | 11.8 |

Capital Expenditures | 12.6 | 11.3 | +1.3 | 8.1 | 16(+) | 20.3 | 72.0 | 7.7 |

Inventories | –1.3 | –0.4 | –0.9 | 1.9 | 5(–) | 26.3 | 46.1 | 27.6 |

| Companywide Retail Activity | ||||||||

Companywide Sales | –12.9 | 0.5 | –13.4 | 6.7 | 1(–) | 17.5 | 52.1 | 30.4 |

Companywide Internet Sales | –18.2 | 6.1 | –24.3 | 5.6 | 1(–) | 7.3 | 67.2 | 25.5 |

| General Business Conditions, Retail Current (versus previous month) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –4.1 | –4.9 | +0.8 | 3.5 | 3(–) | 20.1 | 55.7 | 24.2 |

General Business Activity | –3.2 | 1.4 | –4.6 | –0.1 | 1(–) | 17.7 | 61.4 | 20.9 |

| Outlook Uncertainty Current (versus previous month) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty† | 18.2 | 14.6 | +3.6 | 9.5 | 12(+) | 31.8 | 54.5 | 13.6 |

| Business Indicators Relating to Facilities and Products in Texas, Retail Future (six months ahead) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

| Retail Activity in Texas | ||||||||

Sales | 18.3 | 34.9 | –16.6 | 32.9 | 25(+) | 39.2 | 39.9 | 20.9 |

Employment | 22.0 | 21.8 | +0.2 | 13.3 | 25(+) | 30.0 | 62.0 | 8.0 |

Part–Time Employment | 0.5 | 5.0 | –4.5 | 1.8 | 22(+) | 8.1 | 84.3 | 7.6 |

Hours Worked | 4.0 | 3.7 | +0.3 | 3.2 | 25(+) | 11.3 | 81.4 | 7.3 |

Wages and Benefits | 50.1 | 48.1 | +2.0 | 28.9 | 25(+) | 50.4 | 49.3 | 0.3 |

Input Prices | 50.0 | 48.9 | +1.1 | 34.1 | 25(+) | 57.1 | 35.7 | 7.1 |

Selling Prices | 47.6 | 42.6 | +5.0 | 30.1 | 25(+) | 57.1 | 33.3 | 9.5 |

Capital Expenditures | 30.9 | 26.7 | +4.2 | 18.1 | 24(+) | 33.3 | 64.3 | 2.4 |

Inventories | 3.1 | 27.8 | –24.7 | 10.6 | 25(+) | 28.9 | 45.3 | 25.8 |

| Companywide Retail Activity | ||||||||

Companywide Sales | 14.6 | 32.4 | –17.8 | 31.5 | 25(+) | 36.3 | 41.9 | 21.7 |

Companywide Internet Sales | 17.2 | 17.1 | +0.1 | 22.8 | 26(+) | 28.6 | 60.0 | 11.4 |

| General Business Conditions, Retail Future (six months ahead) | ||||||||

| Indicator | May Index | Apr Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | –3.5 | 4.9 | –8.4 | 17.4 | 1(–) | 23.1 | 50.3 | 26.6 |

General Business Activity | –3.5 | –1.5 | –2.0 | 13.2 | 2(–) | 23.3 | 49.9 | 26.8 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

†Added to survey in January 2018.

Data have been seasonally adjusted as necessary, with the exception of the outlook uncertainty index which does not yet have a sufficiently long time series to test for seasonality.

Texas Service Sector Outlook Survey

Texas Retail Outlook Survey

Texas Service Sector Outlook Survey

Comments from Survey Respondents

These comments are from respondents’ completed surveys and have been edited for publication.

- We are really hoping for a rebound in economic activity.

- Supply chain and lack of trained workers [are issues].

- Inflation is raising the cost of everything we do. When combined with the broken supply chain, it makes business a real challenge!

- Hiring: We are in a hiring push at the moment, still trying to fill the 20 new heads that were approved in our 2022 budget. Also, we will be adding 30 interns in May for the summer season, our most ever. Revenues: Outlook is improving as the U.S. moves to produce more oil and gas for export to Europe as a result of Europe's efforts to get off Russian oil and gas. Much of that export will move through the Port of Corpus Christi.

- Supply-chain challenges for some of our clients, including government and commercial, seem to be more in flux.

- The company's revenue and growth is closely tied to the financial services industry, which we expect to do well in a recessionary period.

- We have been through downturns in our industry before. Most have not. For decades, the residential mortgage industry has done well with refinancing. With interest rates up, that is over. The vast majority in our industry have never seen interest rates go up or staff counts go down.

- There are many variables that are affecting or could affect the future forecast. We see inflation beginning to impact buying habits, supply of some goods are deficient, and rising price of fuel is deterring travel. The lack of fossil fuel production is impacting not just consumers but the oil industry as a whole, and now we are suffering through a drought, which has drastically changed the outlook for agriculture over a large area of the state. There are a lot of moving parts, and it is beginning to change consumers’ attitude and optimism. Rising rates help some and hurt others.

- Our anticipation of an increase in our level of activity is largely predicated on the assumption that as short-term floating rate commercial mortgage debt becomes increasingly more expensive if the FOMC [Federal Open Market Committee] continues tightening monetary policy, commercial owners will be more inclined to want to fix their cost of capital for a longer period of time.

- Inflation is higher than the FRB [Federal Reserve] estimated, and it will probably take a recession to get inflation under control.

- Inflation is an issue. We see wage/cost increases without productivity gains and an inability to pass through costs quickly.

- My business is focused on the oil and gas advisory and capital investment space. Activities have been increasing in this space, and there are seemingly more participants coming back to the segment.

- There are many uncertainties as to how the recent Fed [Federal Reserve] action will whipsaw certain parts of the economy. Prices may flatten out but not without damage to the lending industry and long-term growth.

- The labor market cost increase and lack of access to labor is hurting business growth. The increase in wages has been consumed by cost increases for our employees—so no winners at all.

- We continue to see property insurance rates and deductible increases with Texas storms and last year's freeze. There has been some slowing of payroll increases (on workers’ compensation audits) due to the economy, but we'll see how the next few quarters run.

- Lack of border enforcement, energy costs, international uncertainty, inflation and crime are pervasive challenges to business and commerce.

- The national media keeps talking recession, but every market we look at or talk to is doing very well, particularly in Texas and on both coasts, so I don’t understand why the negativity. Yes costs are up and so are wages, but businesses are investing and expanding and growing. What is wrong with that picture?

- Employees are so burned out after all the COVID challenges, it is proving difficult to get them refocused on business fundamentals.

- I lived through the ’70s and ’80s so I think I know how to prepare my company for the "fake" higher revenues we are showing that can stop faster than you can think possible and the very real and permanent higher expenses we are incurring. Supply chain is still a very real threat to our survival; higher labor and benefits are becoming a greater threat, and margins are squeezing because it is getting tougher to pass on 20–30 percent price increases we have received from manufacturers.

- We continue to be busy with our backlog. Economic uncertainly is palpable, and retaining/hiring a qualified workforce continues to rein in capacity and desire to grow. Constant news about workforce shortage and employee demands is causing stress and pressure on employers. We've seen small businesses cut back hours and long-time small businesses just calling it quits so as not to have to deal with employee issues anymore.

- Inflation is very high, and the economy seems to be slowing a lot in the U.S. and worldwide.

- Trials are getting very busy. Courts are rarely shutting down or postponing due to COVID concerns.

- There are a lot of negative headwinds in our economy and concerns where we will end up. Hopefully, the increase in interest rates will slow down inflation, but we have a lot of other hurdles to get past. We will know more in the next six months.

- There is a lot of uncertainty with inflation.

- It’s a train wreck: inflation, gasoline at $6 per gallon, the border crisis, stock market, supply-chain issues, baby formula [shortage], more COVID variants, war and threats of wars and nuclear war. High and low-skill labor shortages continue.

- Things are slow. We came off of a very strong year after the freeze in Texas, so I expect things to be a little slower than last year, but this is slower than ever in our industry.

- Employee retention is becoming a problem. Outside opportunities allow easy movement of employees for reasons that appear to be purely a desire to "try something different."

- I am not seeing activity in the energy arena that gives me reason to believe a significant number of projects are moving forward.

- Long term, I’m nervous about 2023 and a market slowdown due to interest rate increases.

- I am feeling many small businesses are starting to give up and resign to less growth in 2022. They just can't keep up with the raising costs and remain competitive, and they are tired of trying to compete, and they fear there is a recession coming, so they are planning for longer-term decreases now. This is the sentiment I am hearing with our customers and starting to feel myself.

- Inflation, recession, stagflation? There are too many unknowns right now to commit to a path forward; we just need to be ready for anything, and none of it is good.

- Despite the headlines since the beginning of 2022, actual business activity has increased significantly in terms of requests from clients, etc.

- We will be branching out into more after-market service offerings over the course of the next 24 months.

- Labor shortages and supply issues continue to be challenging. Fuel costs and supplier price increases are significant headwinds to our operations. Profitability and employee retention continue to cause concern for management.

- We are very concerned about the real impact of a recession on business travel and the trickle down that will create.

- We are unsure and uneasy about how inflationary pressures will affect the candidate-driven job market and how employers will adjust workforce planning. In order to secure the strongest talent, salary offers are getting higher, and sign-on bonuses and other financial incentives are being offered without hesitation.

- We deliver training services to corporations and mid-size companies. The contracts are smaller and more short term.

- Inflation is contributing to a lot of requests for compensation increases among our staff.

- Medical services have fixed pricing with almost no ability to raise prices from contracts and decreasing [pricing] from federal programs. Rises in employee cost, insurance, disposables and rent are massively squeezing margins. (Smaller private groups do not have access to capital markets.)

- Regardless of Davos [annual meeting of the World Economic Forum] buzz, massive economic malaise; triple bear markets and war, challenging to appraise; delayed and slower production; assets undergoing destruction; Fed has insanely difficult task mandates, so give praise!

- Inflation—especially food costs and fuel costs—in addition to supply-chain delays of mechanical equipment continues to be a challenge to deal with. Also, labor shortages are still a major issue.

- Inflation has not yet appeared to cause a pullback on demand for thrift donations, but I believe we are getting close.

- More suppliers do not have parts and are telling us that it will be August/September before they will have goods from their sources.

- As we approach the summer leisure travel season, we are concerned about the impact that inflation, the stock market declines and higher gas prices may have on travel.

- This administration is giving the Carter administration a run for its money. Federal policies are making many of the supply-chain issues worse.

- Labor force shortage is the No. 1 issue that is holding back sales growth and expansion. Some form of immigration must be passed immediately by Congress if small and big businesses are to survive. There are not enough Americans to fill the hospitality industry. Labor shortages are also affecting our vendors’ ability to fill our orders from bacon manufacturers and paper bags and Styrofoam cups and plates manufacturers. The ever-increasing costs are shrinking our margins.

- Wages and input costs continue to rise. We are able to raise prices, however, margins are eroding due to higher costs. Hiring continues to be a problem. It is difficult to find talent in our industry.

- We are beginning to see some business travel and entertaining, which is good. It is still an incredible struggle to hire and retain staff with rising wages with lower productivity. [There are] major increases in all input costs. Inflation fears are becoming reality. I don't know how much more we can pass on in price increases.

- We are having more people apply for jobs. We are still understaffed but are gaining more traction.

- It is a deeply concerning time for our enterprise and the businesses we represent.

- Many of our manufacturing companies are experiencing significant raw material and component cost increases, which have been absorbed but are now being passed along to their customers. This is now beginning to have a negative impact on their sales. Automotive suppliers tell me the huge backlog of over 500 ships waiting to pick up goods in China will impact automotive assembly plants and component manufacturing firms dramatically this summer. The delay is caused by port congestion and COVID-related restrictions in China.

- Increasing problems with supply chains on key commodities and semiconductors are continuing to extend lead times on capital equipment orders.

- We have seen a slight uptick in traffic and a small increase in sales per transaction.

- Getting truck drivers to move products is our biggest challenge. We are having a hard time finding drivers, and when we do, they are usually higher priced than the previous time we made a similar move.

- Supply-chain issues in the automobile business seem to be getting worse instead of better. It is nearly impossible to hire anyone —no applicants for well-paying jobs.

- There is still no steady supply of inventory.

- We are concerned about interest rates increasing and how it will affect vehicle financing.

- Lack of inventory continues to hamper sales.

- I think [the Federal Reserve] waited too long to raise rates and now you're going up too fast. It should be 1/4 point [interest rate increases] for six months then stop for four quarters and see what happens.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Christopher Slijk at christopher.slijk@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.