Energy Indicators

November 16, 2021

Global fossil fuel prices have soared in recent months for a spate of reasons. Stronger-than-expected global demand, trade and political frictions, underinvestment in productive capacity, and unusual weather patterns have all contributed to the tightening of energy supplies available to consumers. This has left seasonally adjusted inventories of many fuels at low levels compared with recent years, and while oil and gas drilling activity is rising globally, international rig counts remain well below prepandemic levels.

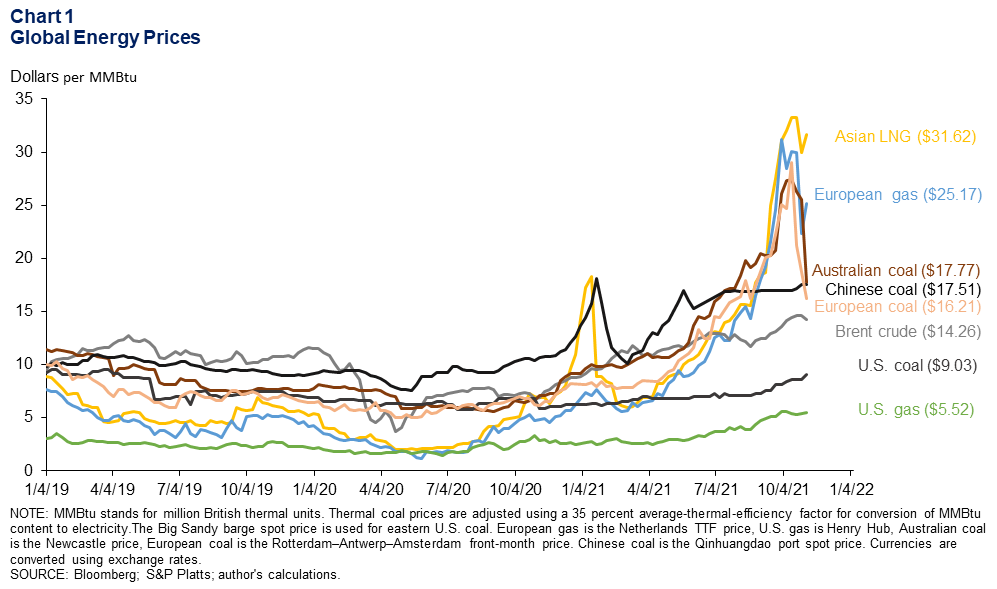

Global energy prices

Liquefied natural gas (LNG) prices in Asia (the Japan–Korea front-month futures contract) averaged nearly $32 per million British thermal units (MMBtu) the first week of November, an increase of 427 percent from the seasonal low point in March for heating and utility demand in the northern hemisphere (Chart 1). European natural gas climbed as high as $30 in mid-August before slipping to $25 in early November on comments from Russian officials that more gas would ship in the coming weeks. In sharp contrast, U.S. Henry Hub gas climbed only 86 percent to $5.52.

The sharp increases in gas costs revived demand for coal among utilities ahead of winter. Even Brent crude, which ended October 2021 at $14 per MMBtu, has been swept up as fuel switching in some power plants could add up to 0.5 million barrels per day (mb/d) of crude consumption, according to analyses by the International Energy Agency and others. (Crude MMBtu is a measure of the energy contained in fuel.)

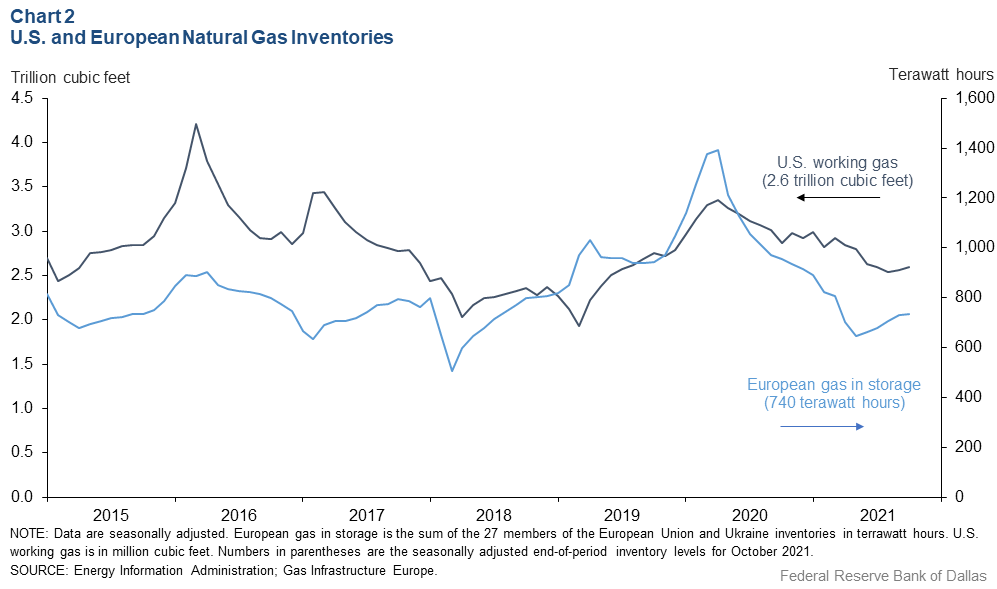

Natural gas inventories

Seasonally adjusted inventories of natural gas in Europe began to rise over the summer, though sources disagree on the timing and magnitude, and stocks remain low compared with prior years. According to Gas Infrastructure Europe, adjusted inventories in October 2021 were equivalent to 740 terawatt hours (TWh) (Chart 2).

Normal seasonal patterns the past six years caused European inventories to contract by an average of 709.2 TWh between October and March. Without a substantial increase in imports or production, a draw of that magnitude would put substantial upward pressure on prices, which is one reason European energy futures have soared ahead of winter.

Inventories of natural gas in the U.S. increased modestly to nearly 2.6 trillion cubic feet, or roughly 762 TWh, in October based on projections by the Energy Information Administration (EIA).

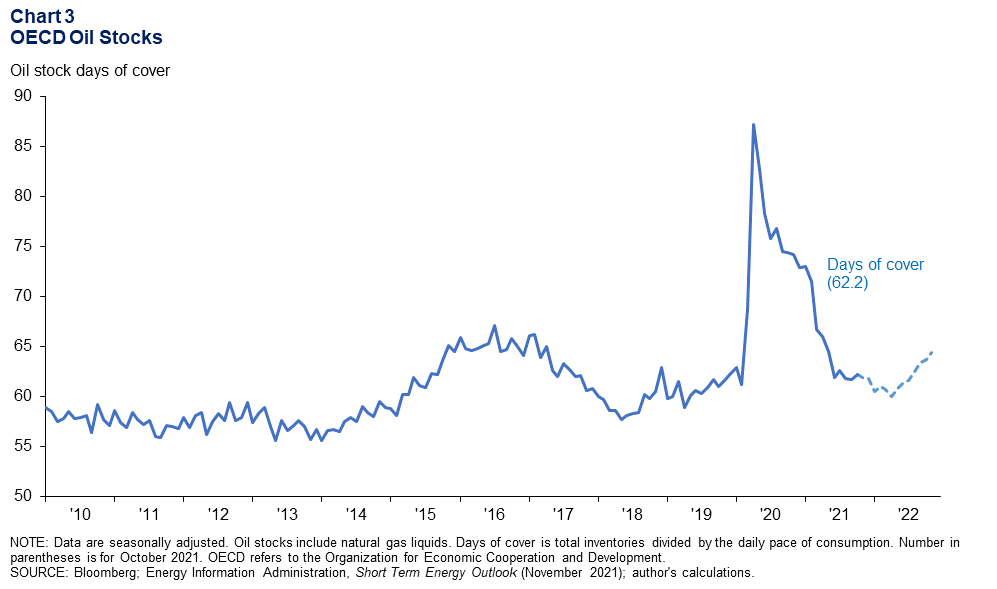

OECD oil days of cover

October stocks of crude oil and natural gas liquids in OECD (Organization for Economic Cooperation and Development) countries were adequate to cover 62.2 days of demand, seasonally adjusted (Chart 3). While below 2020 levels, stocks remain well above those seen in the early 2010s when oil prices were orbiting $100. The most recent EIA projections suggest inventories will continue to ease through February or March of 2022.

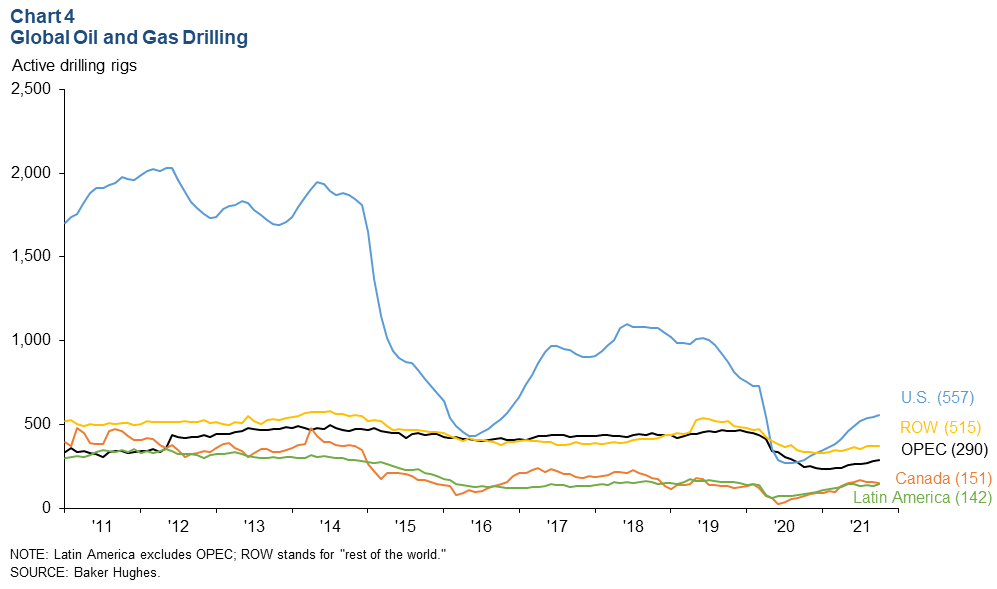

Global drilling

The international rig count is rising, but it remains well below prepandemic levels in most regions (Chart 4). The rig count for OPEC nations is 38 percent below December 2019 levels at 290 active rigs, seasonally adjusted. The relative dearth of drilling is contributing to concerns that insufficient spending—and unplanned outages in some member countries—will leave the group with less spare production capacity than expected over the next year. Many analysts project that spare capacity will be needed to balance global consumption by the end of 2022.

Latin American drilling is down only 5 percent at 142 rigs, and that activity is mostly in Mexico and Argentina. However, Brazil is producing the lion’s share of the region’s output, with nearly 4 mb/d of production this year. The EIA’s November Short-Term Energy Outlook projects nearly 0.3 mb/d of annual output growth in 2022 from Brazil, just enough to offset declines elsewhere in Latin America.

The U.S. averaged 557 active rigs in October 2021. Domestic drilling has increased in part to offset the dwindling inventory of uncompleted wells left from 2020. Most major agencies, private forecasters and the Dallas Fed are projecting modest U.S. crude output growth this year and some acceleration in 2022, though projections for 2022 vary widely.

Substantially more rigs will have to come online in 2022 for the U.S. to increase production. U.S. producers are likely to continue to prioritize investor returns going forward, but substantially improved cash flow and an expectation that West Texas Intermediate crude prices will hold well above $60 and natural gas well above $3 next year are likely to leave room to fund substantial drilling increases—assuming enough workers can be hired to run the equipment.

About Energy Indicators

Questions can be addressed to Jesse Thompson at jesse.thompson@dal.frb.org. Energy Indicators is released monthly and can be received by signing up for an email alert. For additional energy-related research, please visit the Dallas Fed’s energy home page.