Energy Indicators

January 19, 2023

Energy prices have been dropping since summer as softening economic data and warmer-than-normal weather lowered demand expectations. Oil production continued to increase in the U.S. shale oil basins. Oil executives expect to increase their capital spending in 2023 but are wary due to uncertainty surrounding the future price of crude oil and the current domestic political climate.

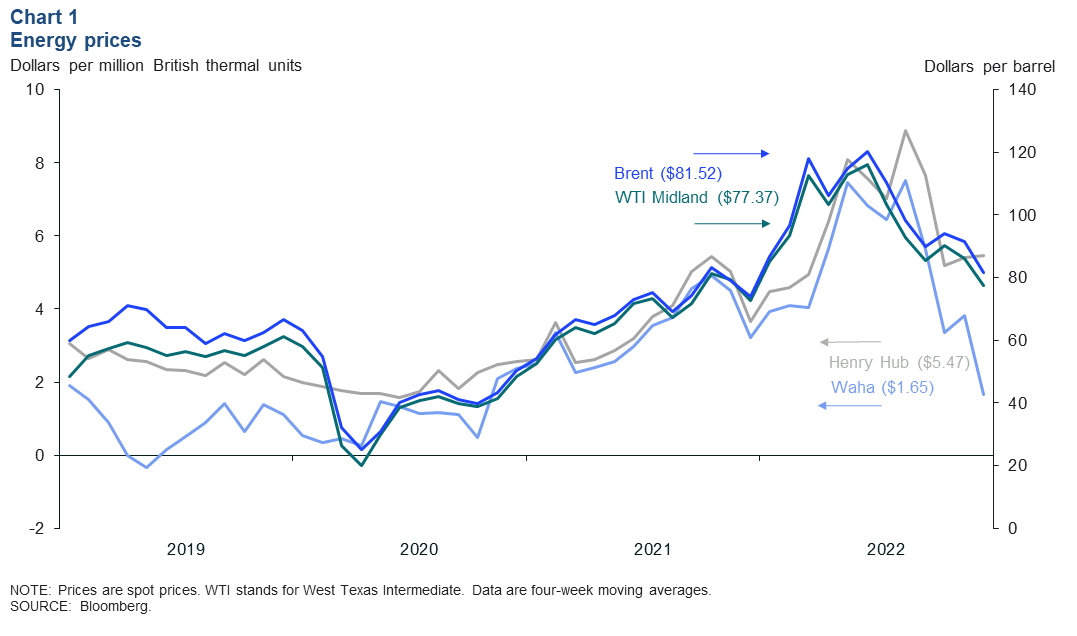

Energy prices

Energy prices broadly decreased in the fourth quarter of 2022. West Texas Intermediate (WTI) priced in Midland, closer to the wellheads of the Permian Basin, and Dated Brent spot prices were at $77.37 and $81.52 per barrel, respectively, for the four-week moving average ending Dec. 30, 2022. Those were the lowest nominal prices since December 2021, but they remain above prepandemic levels (Chart 1). Oil prices have been falling due to worries of a potential recession in Europe, rising interest rates and a COVID-19 policy in China that could curtail fuel demand. Prices have fallen roughly 30 percent from their peak in mid-2022.

West Texas’ Waha Hub natural gas spot price averaged $1.65 per million British thermal units (MMBtu) for December 2022 but swung as high as $5.40 due to a demand boost from a sharp but short lived wintry blast. It also swung as low as negative $3.90 per MMBtu after warmer weather returned and maintenance temporarily reduced takeaway capacity, trapping production in the basin—an increasingly likely scenario until new pipelines are built. The Henry Hub natural gas spot price averaged $5.47 per MMBtu for December, down 39 percent from its peak in August 2022.

Production and rigs

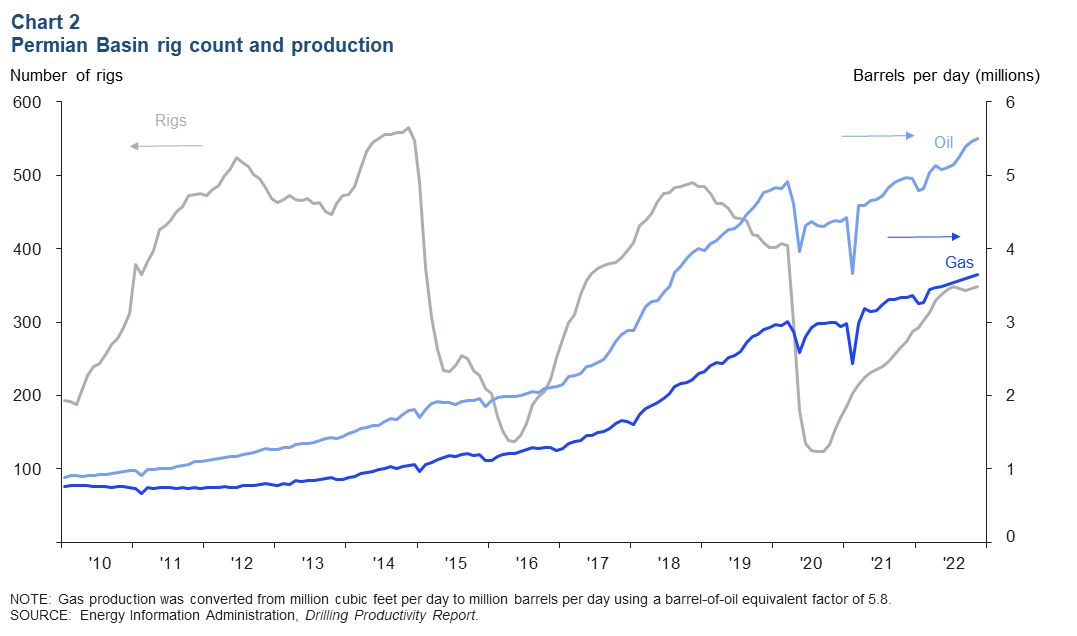

Production in Permian Basin continues to rise

The Permian Basin saw continued production increases to close out 2022. Oil production is up 11 percent from the year-ago level. Total production for both oil and gas together is up 19 percent from prepandemic levels. November saw 5.5 million barrels per day (mb/d) of oil production and, using an oil-equivalent conversion factor, 3.7 million barrels per day of gas (Chart 2). However, producers in the region are uncertain about the growth outlook in 2023 because of cost inflation and shortages in drilling equipment, rigs and crews.

With gas production on the rise, analysts, and industry leaders worry that the Permian’s natural gas infrastructure capacity will become constrained by late 2023 and limit production increases.

The region achieved this production growth in part by drilling longer wells and substantially improving efficiency. The Permian rig count in the U.S. Energy Information Administration’s drilling productivity report totaled 349 at the end of November, up 28 percent year over year, but still 14 percent below its prepandemic level.

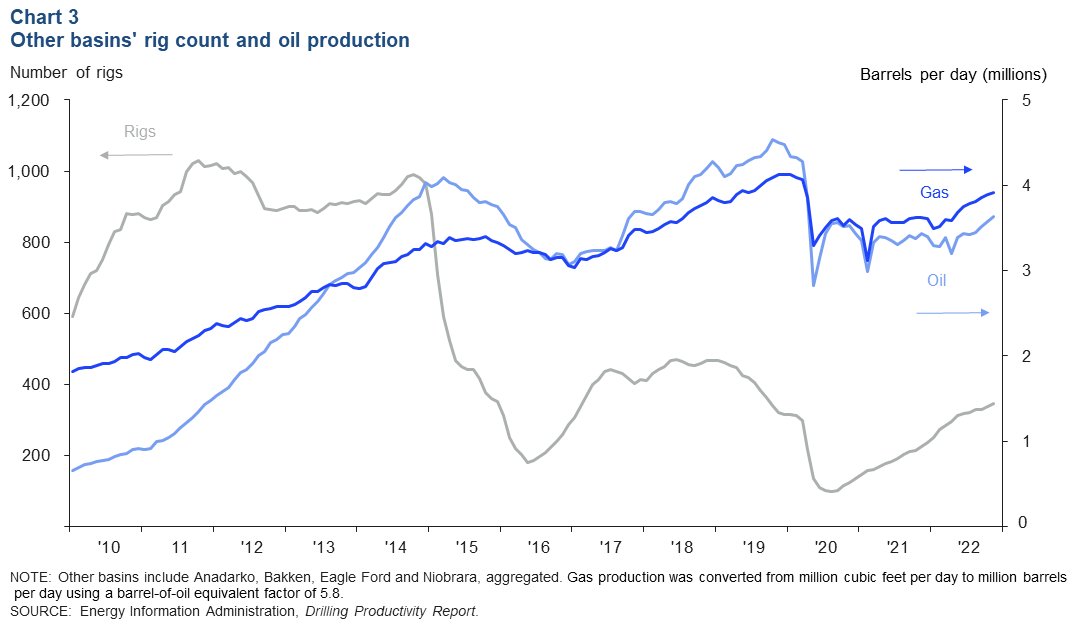

Production growth outside Permian more modest; rig count rises

Aggregate oil and gas production in other oil-focused shale basins (the Anadarko, Bakken, Eagle Ford and Niobrara) rose 7 percent to 7.5 mb/d in November 2022 (Chart 3). That level is still 10 percent below prepandemic levels. Oil production rose from 3.4 to 3.6 mb/d, 16 percent below prepandemic levels.

Total U.S. oil production stood at 130 mb/d from January to November of last year, with the Permian accounting for 44 percent of total production and the other basins mentioned accounting for only 29 percent combined.

Rig counts in the other major oil basins have been rising since mid-2020, going from 110 in June 2020 to 346 in November 2022 and rising 38 percent more from the start of the year. The count accelerated as energy prices rose for most of 2022.

The modest production increases seen in the other basins may not last in 2023. Recent comments from some oil producers indicate that shale output growth in the U.S. could slow to 300,000 to 400,000 barrels a day in 2023, compared with between 500,000 and 600,000 in 2022.

Dallas Fed Energy Survey special questions

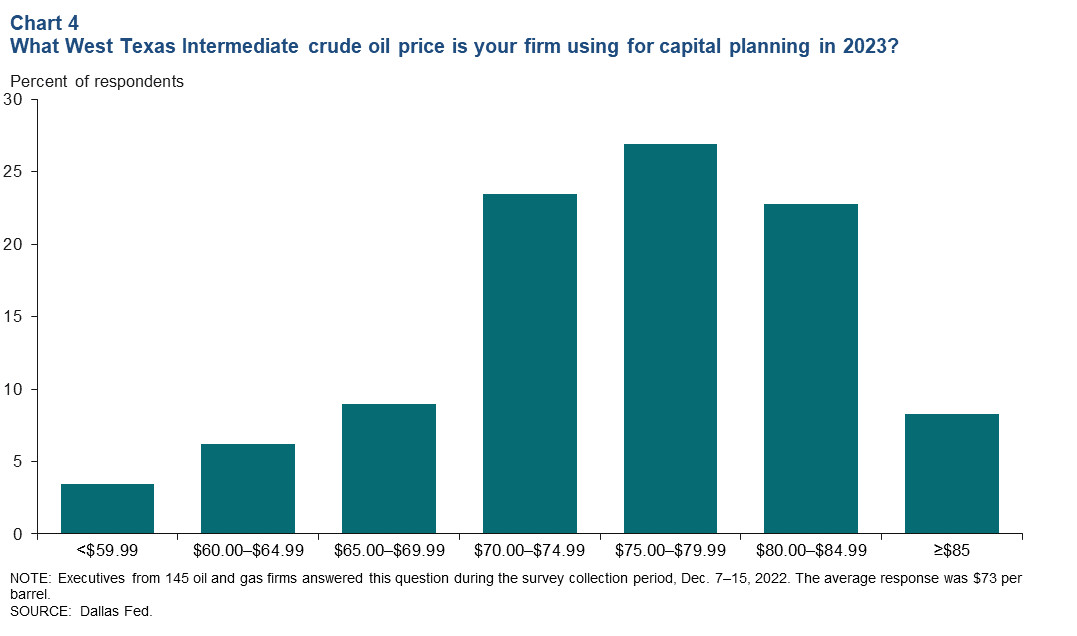

Crude oil price used for planning ticks up

Oil production firms interviewed between December 7 and 15 for the Dallas Fed’s Energy Survey said they expect oil and fuel prices to creep up this year due to underinvestment in the fossil fuel sector, a cooperative OPEC+ willing to limit supply, and a lack of refining capacity. On average, oil executives said they were using a price of $73 per barrel for their capital planning in 2023 (Chart 4), compared with the $64 per barrel used for planning in 2022. Respondents also indicated that there is still a lot of price uncertainty as world economic growth is projected to slow in 2023, with many believing the supply level will remain stable.

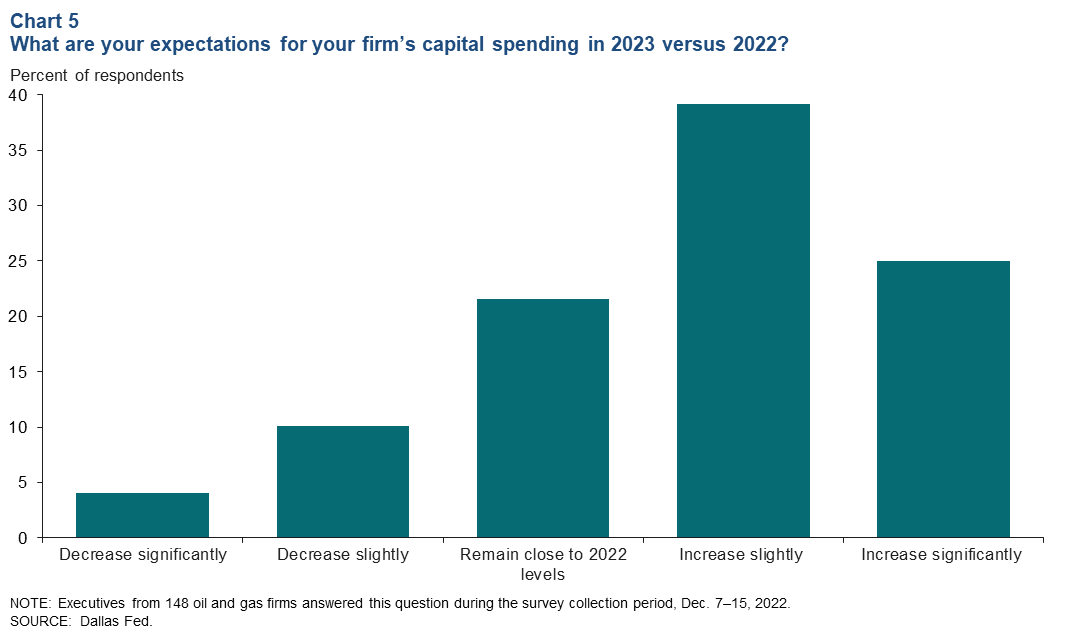

Increase in capital spending expected

Thirty-nine percent of respondents said they expect capital spending to increase slightly in 2023 versus 2022, but it isn’t clear if that will be due to greater activity or elevated input costs (Chart 5). Twenty-five percent of respondents predict a significant increase in capital spending, while only 14 percent of respondents anticipate a reduction in spending.

Some respondents noted a lack of capital available to increase supply. Many blamed the Biden administration’s vilification of the fossil fuel industry and the accelerated push to clean energy. Concerns centered on policies that could result in increased regulation and extra taxation. Even with so much uncertainty, Barclay’s recent spending survey found that oil and gas companies’ global spending is expected to increase 13 percent in 2023 following a 20 percent upsurge in 2022.

About Energy Indicators

Questions can be addressed to Kenya Schott at kenya.schott@dal.frb.org. Energy Indicators is released monthly and can be received by signing up for an email alert. For additional energy-related research, please visit the Dallas Fed’s energy home page.