Mexico seeks to reduce consumers' longstanding reliance on cash

The use of cash in the United States is declining, with the share of consumer transactions settled in dollars and cents falling from 32 percent in 2015 to 26 percent in 2018.[1] Consumers increasingly opt to pay with cards and apps that offer increased speed and convenience, a trend likely to continue.

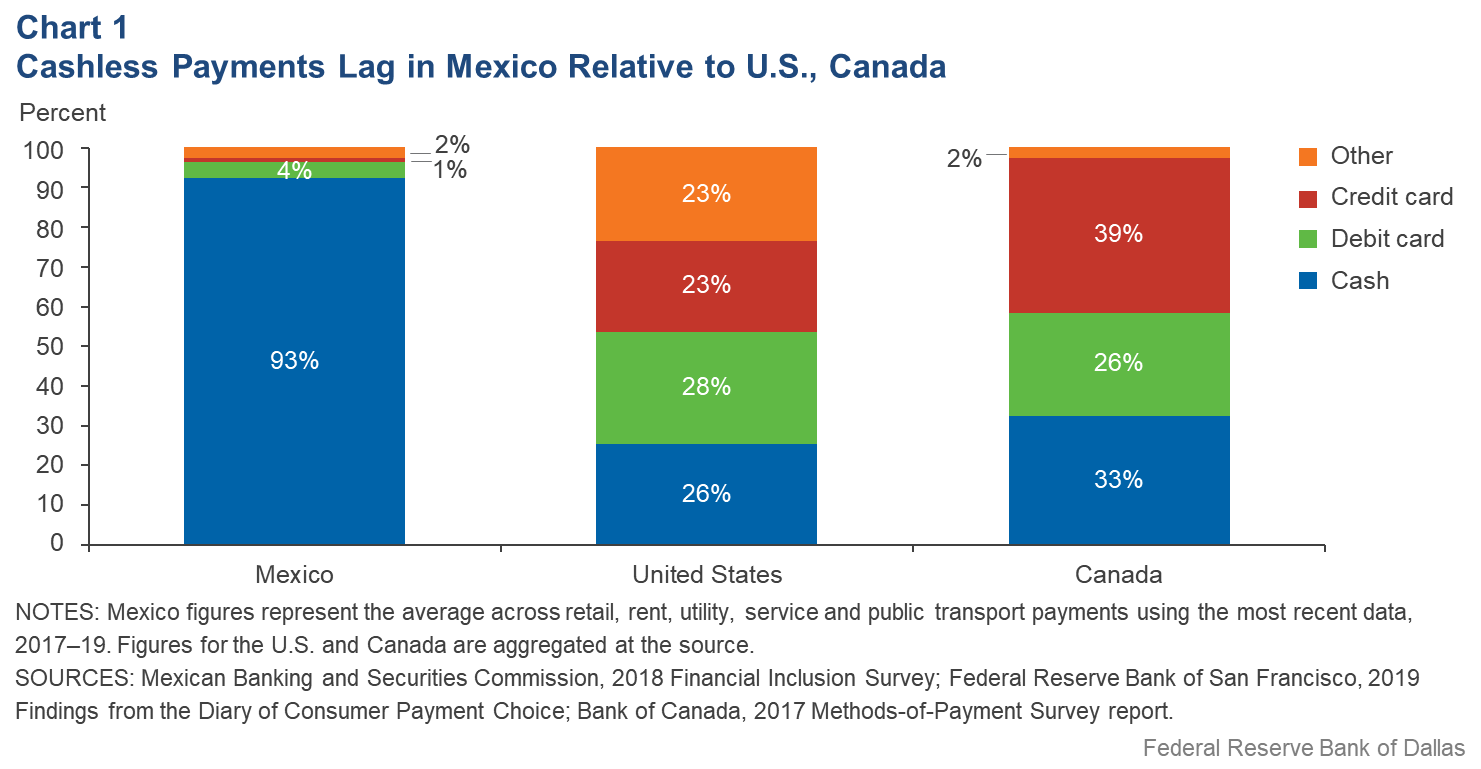

The situation is quite different in Mexico, where around 90 percent of retail, rent, utility, service and public transportation transactions were settled in cash in 2018—a share little changed in recent years.[2] Payments that could elsewhere be made easily over the web or through an app are instead made in person and in cash.

Data show that Mexico substantially lags the U.S. and Canada in terms of debit, credit and other cashless payment channels that include digital payment platforms, checks and prepaid cards (Chart 1). This is despite the growing presence of banks throughout the country as well as wider availability of electronic point-of-sale and mobile payment platforms.

There is no denying that cash offers conveniences over cashless alternatives. Cash is widely accepted and does not impose interest or fees on consumers and businesses for executing transactions. It also encourages prudent spending and saving; cash users have a more tangible perspective on their financial position and are less likely to incur heavy loads of debt. And unlike electronic payment platforms, cash is not subject to cybersecurity attacks and identity theft.

However, cash also generates nontrivial costs and challenges for individuals, enterprises and regulators that outweigh its conveniences. It is expensive to transport and store, and it requires all parties involved in the transaction to meet in-person to settle their payments. Moreover, it is a facilitator of criminal activity. Cash does not leave a paper trail, making it the payment method of choice for those looking to avoid legal detection.

In Mexico, both public and private sector actors are collaborating on unique technological solutions to diminish the nation’s cash reliance and facilitate its transition to digital payments. Significant challenges await, the greatest of which will be shifting the preference for physical currency.

Cash Is King

Heavy cash use in Mexico is driven by multiple, intertwined factors. First, only 35 percent of the adult population has a bank account.[3] Since most electronic payment platforms require users to have a bank account through which payments can be remitted and received, many Mexicans are unable to use automated payments.

Why do so many Mexicans lack bank accounts? The huge informal sector’s role in Mexico’s $1.2 trillion economy is an important factor. It accounts for over a quarter of the gross domestic product (GDP) and employs more than half of Mexicans age 15 or older.[4] These individuals typically earn wages in cash, do not pay income taxes and may not have the documentation necessary to open a bank account.

The banking sector is another part of the problem. Banks tend to be expensive, subjecting account holders to minimum deposits, fees and penalties. Also, Mexican banks have little incentive to sell products and services to low-income Mexicans. Such products are not as profitable as those catering to more-affluent clients. In addition, the banking sector is heavily regulated and, as is the case in the U.S., bank customers are potentially subject to government scrutiny if fraudulent or illegal activity is suspected.

On the sidelines, financial technology companies, known as fintechs, have attempted to offer Mexicans an alternative path to financial inclusion. However, the sector is nascent in Mexico and out of reach for many. To that end, 62 percent of Mexican fintech firms have raised less than $500,000 in funding, making it difficult for them to achieve economies of scale and reach a wide customer base.[5]

Moreover, the sector is subject to regulatory uncertainty from recent implementation of a fintech law that some in the sector fear will create tough barriers to entry for start-ups and generate higher compliance costs.[6]

Hiding Transactions

Despite cash’s convenience, Mexico’s heavy reliance on it comes with significant risks. Cash needs to be safely transported and stored, and failure to do so subjects it to theft. This especially affects low-income individuals and small businesses, which are typically unable to afford sophisticated security and transportation services for holding and moving cash. They instead store physical cash in their homes and spend a large amount of time traveling to offices to pay utility bills and taxes.

Additionally, cash can be a conduit of financial fraud. Authorities attempting to catch criminals operating solely in cash find it difficult to overcome the lack of a digital footprint that electronic transactions provide.

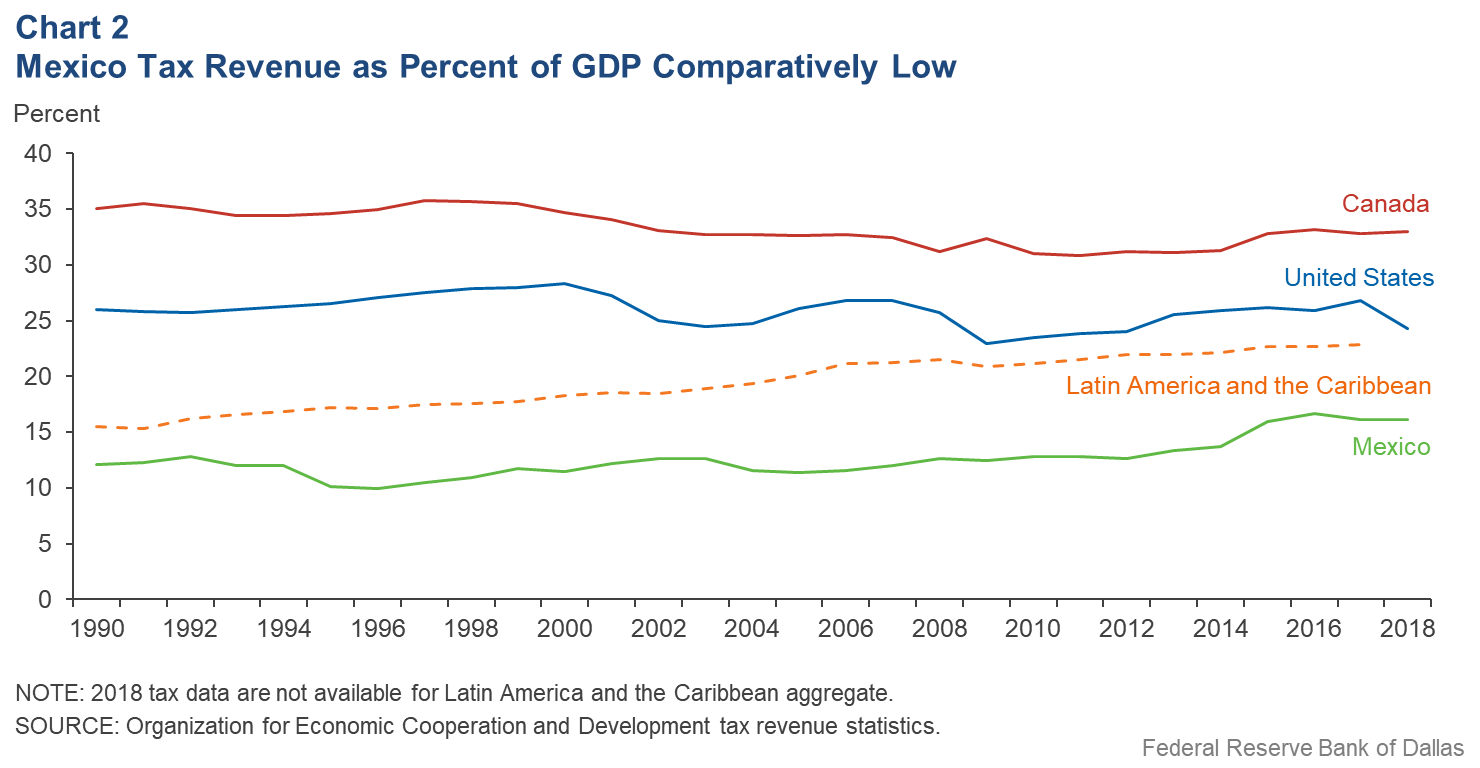

Cash operations also incentivize tax evasion, depressing public revenues. Mexico falls well behind Canada, the U.S. and Latin America in terms of total tax receipts as a percentage of GDP (Chart 2). While Mexico’s 2015 tax reform increased tax revenue, it failed to bring Mexico into alignment with its peers.[7]

More recently, the government has confronted a slowing economy. Mexico narrowly avoided a recession in 2019 after GDP failed to grow in each quarter.[8] Similar trends in 2020 could suppress public tax receipts, limiting the government’s ability to invest in programs that improve financial access and reduce cash dependence.

The Mexican government approved a tax reform package for 2020 in an attempt to address its persistent tax revenue gap. It seeks to align Mexico’s tax code to the Organization for Economic Cooperation and Development’s Base Erosion and Profit Shifting framework, an internationally focused initiative aimed at tackling tax evasion.[9]

The reform includes legal changes to Mexico’s income and corporate tax structures and harshly punishes tax evaders. However, it remains unclear whether regulators will enforce these new rules and whether the rules will meaningfully formalize Mexico’s largely informal economy.

Collaborative Solutions

The Mexican government is seeking to increase Mexicans’ access to the financial system, which would reduce the reliance on cash. Mexico’s Finance Minister Arturo Herrera has noted that financial inclusion is one of the biggest obstacles in the government’s fight against poverty, inequality and slow economic growth.[10]

As a result, the administration is seeking to encourage competition among private and public enterprises to lower bank product costs for low-income individuals. It also seeks to develop a sustainable technological infrastructure to improve Mexico’s digital payments network.

In 2018, the Mexican government initially proposed a bill to reduce banking fees. Subsequently, officials sought feedback in meetings with banks and financial regulators. The current proposal, which is still before Mexico’s Senate, requires banks to offer zero-fee accounts to low-income clients.[11] The measure also mandates that banks provide customers transparent explanations of their fee structures.

Technological Stepping Stone

Last year, Mexico’s central bank unveiled its digital payments platform CoDi, short for Cobros Digitales (Digital Charges). CoDi, which runs on the central bank’s Electronic Interbank Payment System, leverages the QR code technology commonly used on mobile devices to initiate real-time consumer-to-consumer and consumer-to-business payments.

The application is freely available to consumers and merchants, and transactions initiated over the CoDi network do not incur fees.[12] However, users must have an account at a financial institution as well as a smart device.

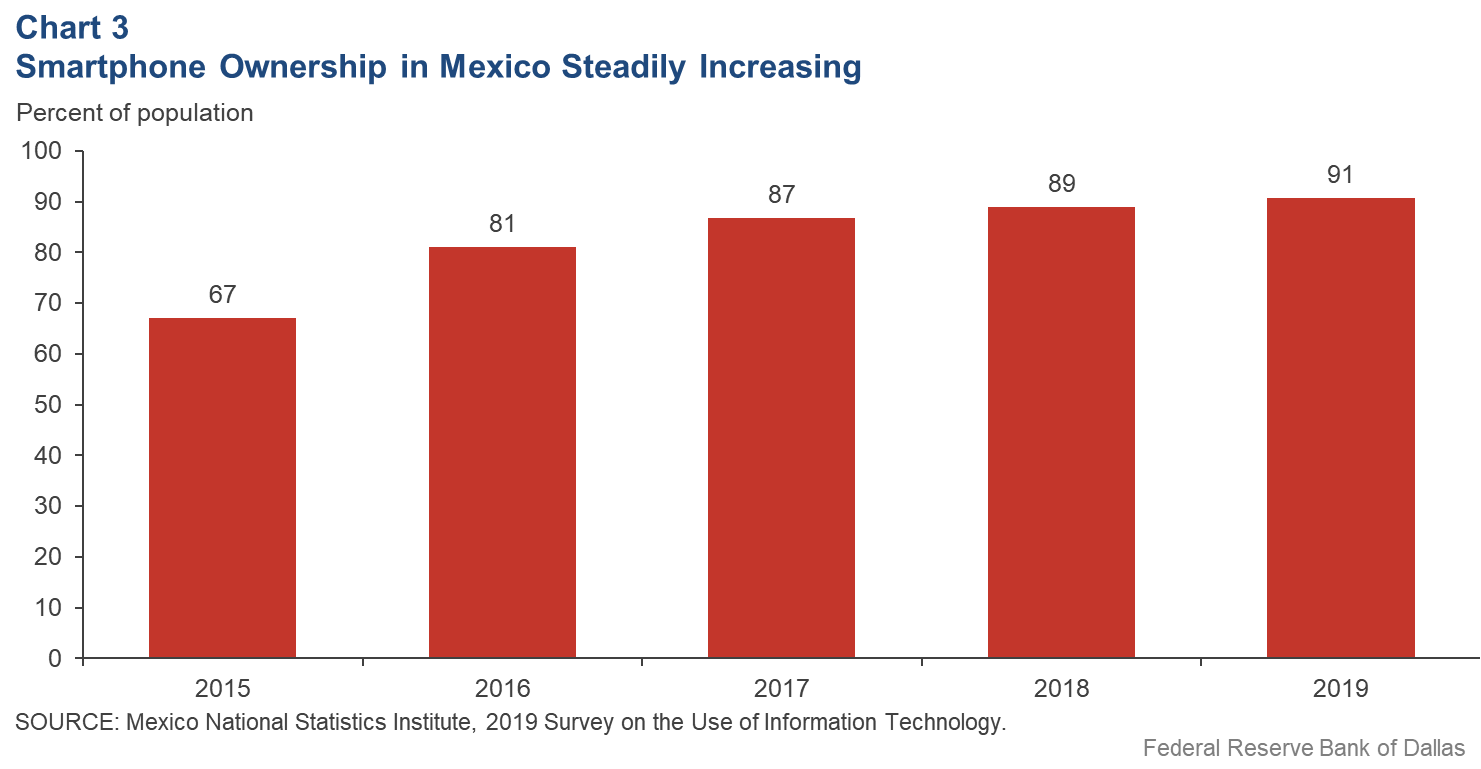

While bank account ownership in Mexico has remained low, smartphone usage is rising (Chart 3). Studies show that over 90 percent of Mexicans own a smart device, up from 67 percent in 2015.

CoDi ultimately seeks to reduce Mexico’s reliance on cash by offering an easy, fee-less and secure digital alternative. The theory is that CoDi’s simple, cost-free convenience will be enough to encourage consumers and merchants to adopt it and, in turn, inspire them to open bank accounts.

To use CoDi, a payment recipient generates a payment order using a CoDi-enabled mobile application. That order has a QR code, scanned by the remitter, which contains the transaction details. The remitter reviews the transaction details and approves it. Approval typically requires an authentication factor such as a PIN number, token, fingerprint or facial scan.

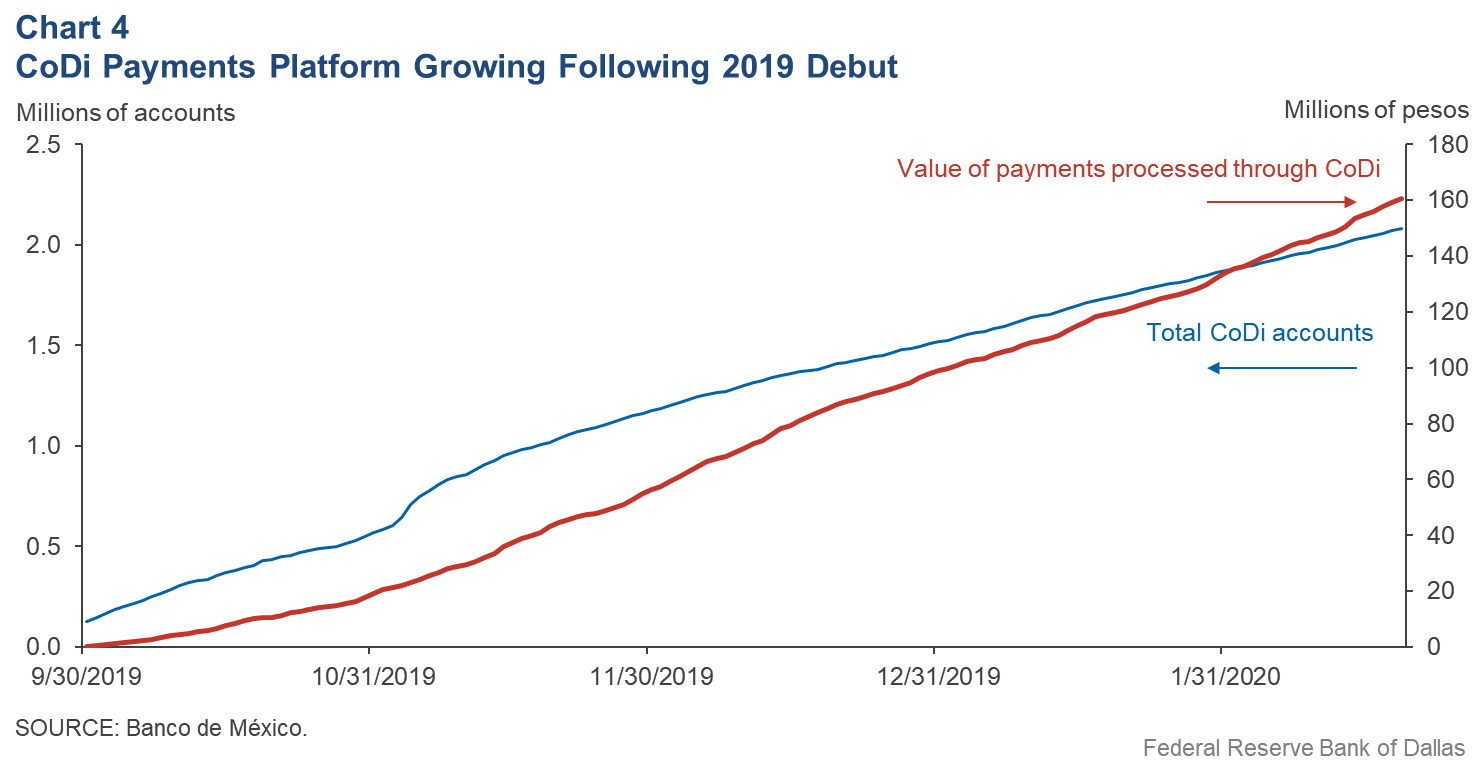

Since CoDi’s release to the public last September, more than 2 million CoDi accounts have been opened, and the platform has registered field transactions totaling more than 160 million pesos ($8.4 million). The platform processes an average of 1,646 transactions daily, each averaging 600 to 700 pesos ($31 to $37) (Chart 4).[13]

Those numbers are expected to increase as a result of government mandates. The Mexican central bank requires all banking institutions operating in Mexico to offer CoDi, though only 38 of the nation’s 51 commercial banks have built it into their digital banking applications.[14] Moreover, banks and fintechs are encouraged to develop innovative applications that leverage the CoDi network, which could potentially further drive down costs and improve financial access.

However, the platform has a long way to go before achieving scale—active CoDi accounts represent only 2 percent of total accounts open at Mexico’s commercial banks.[15]

Many hurdles stand in the way of wider acceptance, particularly the required bank account, which excludes much of Mexico’s informal workforce. Regulatory changes stipulating that banks offer fee-less accounts to low-income customers may ease that situation.

However, Mexico’s regulators will need to actively engage with the financially excluded populace to convince it of the benefits of digital payments—a particularly hard sell when dealing with consumers and enterprises bent on evading taxation or those who are engaged in other criminal activities.

The platform has also generated some pushback from Mexico’s fintech industry, displeased that CoDi’s development did not include input from its members that already operate digital payment platforms in Mexico.[16] This could drive some fintechs to develop competing platforms that leverage more familiar cashless payment technologies such as cards and mobile points of sale.

Shortly after CoDi’s release, Mexican fintech startup Clip announced a joint venture with credit/debit card giant Visa to accelerate small- and medium-sized enterprises’ acceptance of electronic payments.[17] Competition, while potentially driving more financial inclusion, might also limit CoDi’s reach if alternative platforms gain traction.

In practice, CoDi won’t fully address financial inclusion in Mexico, but it may lay the groundwork for an effective and secure digital payments platform as the country looks to improve its technological infrastructure and expand formal finance’s reach in the Mexican economy.

Finding a Path Forward

Recent trends suggest that Mexico’s government is prioritizing a payments transition. The Mexican public and private sectors will need to effectively coordinate and innovate to ensure long-term success.

While CoDi lays meaningful groundwork for what an inclusive electronic payment system will look like in Mexico, much remains to be done to communicate its benefits to the public and inspire a shift in preferences and practices away from cash.

Additionally, the government will need to adequately enforce its new tax reform plan and consider meaningful policies that help formalize informal pockets in Mexico’s economy.

Notes

- See “2019 Findings from the Diary of Consumer Payment Choice,” by Raynil Kumar and Shaun O’Brien, Cash Produce Office, Federal Reserve System, June 2019.

- See “National Survey for Financial Inclusion 2018,” National Banking and Securities Commission (CNBV in Spanish).

- See “Mexico Struggles to Move into Digital Payment Age,” by Michael Perez and Justin Chavira, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter, 2019.

- See “Employment and Occupation,” by the National Statistics Institute (INEGI), accessed March 6, 2020.

- See “Fintech Radar 2019,” Finnovista, May 2019.

- For more information on Mexico’s fintech law, see “Mexico’s Nascent Fintech Offers Promise, Faces New Rules,” by Michael Perez, Federal Reserve Bank of Dallas Southwest Economy, Fourth Quarter, 2018.

- See “Mexico’s Fiscal Reform Earns Mixed Reviews,” by Jesus Cañas, Federal Reserve Bank of Dallas Southwest Economy, Second Quarter, 2019.

- See “GDP and National Accounts,” INEGI, accessed March 6, 2020.

- See “Mexico Approves Significant Tax Reform,” PricewaterhouseCoopers (PwC), October 2019.

- See “Mexico’s New Government Wants Fintech, Banks to Help Financial Inclusion,” by Stefanie Eschenbacher, Reuters, Aug. 21, 2018.

- See “Senate Changes Proposal and Will Not Prohibit Banking Commissions, They Will Inform Them,” by Antonio Hernández, El Universal, Feb. 2, 2020.

- Payments initiated via the CoDi network are capped at 8,000 pesos (about $420).

- See “CoDi,” Banco de México, accessed March 6, 2020.

- Banks not actively implementing CoDi in their mobile banking apps may be subject to fines in the future.

- The figure is based on the author’s calculations using data from Banco de México and the National Banking and Securities Commission.

- The government’s development of CoDi makes it unique relative to other QR-based payment applications around the world (e.g., WePay in China and M-Pesa in Kenya). See “Mexico's Fintech Solution for the Unbanked Is ‘Great, but Flawed,’” by Helgi Gudmundsson, S&P Global Intelligence, June 2019.

- See “Visa and Clip Team Up to Accelerate Digital Payment Acceptance in Mexico,” Visa, November 2019.

About the Authors

Michael Perez

Perez is a financial industry analyst in the Supervisory Risk and Surveillance division at the Federal Reserve Bank of Dallas.

Southwest Economy is published quarterly by the Federal Reserve Bank of Dallas. The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

Articles may be reprinted on the condition that the source is credited to the Federal Reserve Bank of Dallas.

Full publication is available online: www.dallasfed.org/research/swe/2020/swe2001.