Inverted yield curve (nearly always) signals tight monetary policy, rising unemployment

With long-term interest rates falling and short-term rates rising, there has been increasing talk of a possible yield-curve inversion and speculation about what an inversion might mean for the U.S. economy.

The yield curve shows how the yields on government debt securities vary with time to maturity. A yield-curve inversion occurs when the return to holding soon-to-mature securities exceeds the return to holding securities that will mature later.

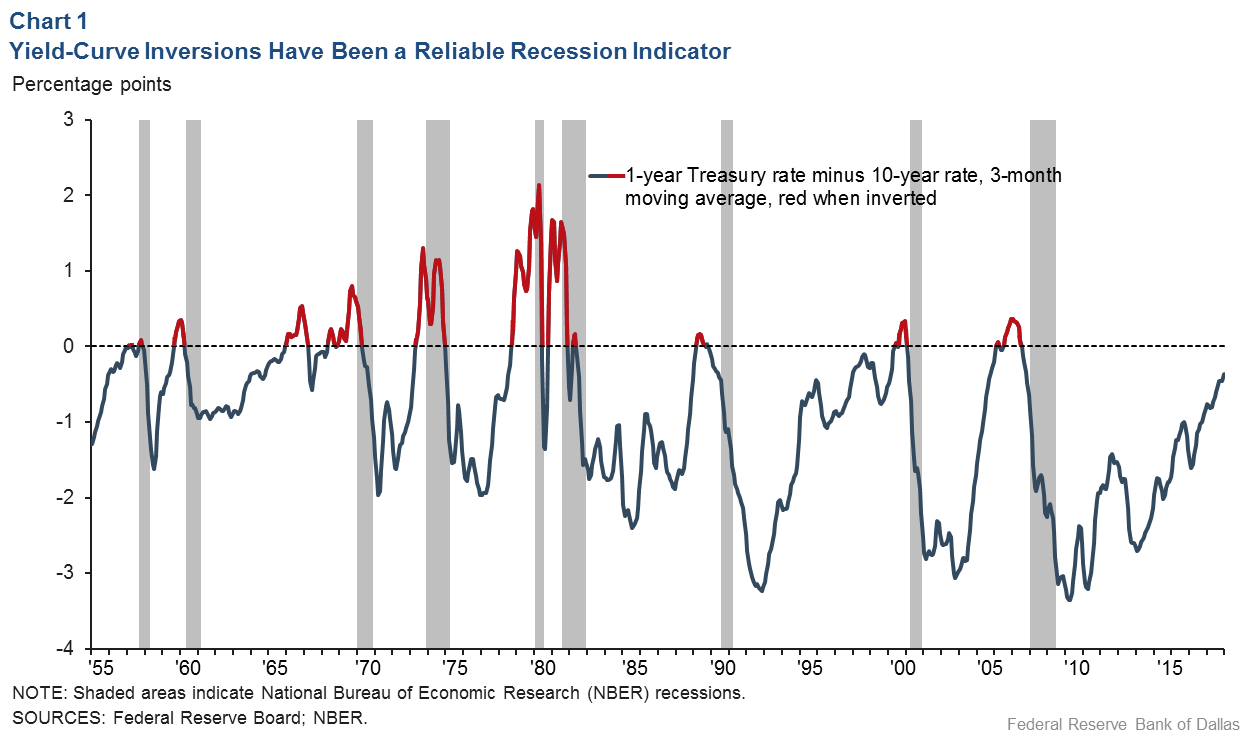

We look specifically at the difference in yield between Treasuries maturing in one year and those maturing in 10 years. Using that definition, every U.S. recession during the past 60 years has been preceded by a yield-curve inversion, and every significant, sustained inversion but one has been followed by a recession (Chart 1). In the single exception, during the mid-1960s, the economy’s growth slowed sharply, but fiscal stimulus prevented a downturn.

We argue that yield-curve inversions are a signal that monetary policy is tight, and we show that tight policy has a substantially larger impact on the economy than easy policy. In other words, monetary policy’s brake pedal is more powerful than its gas pedal. To complicate matters, both pedals operate with a significant lag, making it difficult for policymakers to respond to economic shocks in a timely way.

Yield curve slope signals Fed policy stance

The dividing line between tight and easy monetary policy is called the “neutral rate of interest” and is denoted by R*. Policy is tight if the short-term interest rate, R, exceeds R*. Policy is easy if R is below R*. We equate R to the one-year Treasury rate, which reflects both the current setting and expected near-term path of the overnight borrowing rate controlled by Federal Reserve policymakers.

The Federal Reserve has a dual mandate to promote full employment and price stability, so one would expect tight policy (R > R*) when inflation is high or unemployment is unsustainably low, and easy policy (R < R*) when inflation is low or the unemployment rate is high. In a healthy economy, at full employment with price stability, one would anticipate seeing R = R*.

Federal Reserve economists estimate R* using a variety of sophisticated techniques. For our purposes, however, it is enough that people expect policy to converge to neutral over time. If we have a reasonably accurate measure of where investors expect short-term interest rates to settle some years ahead, that estimate should also approximate R*.

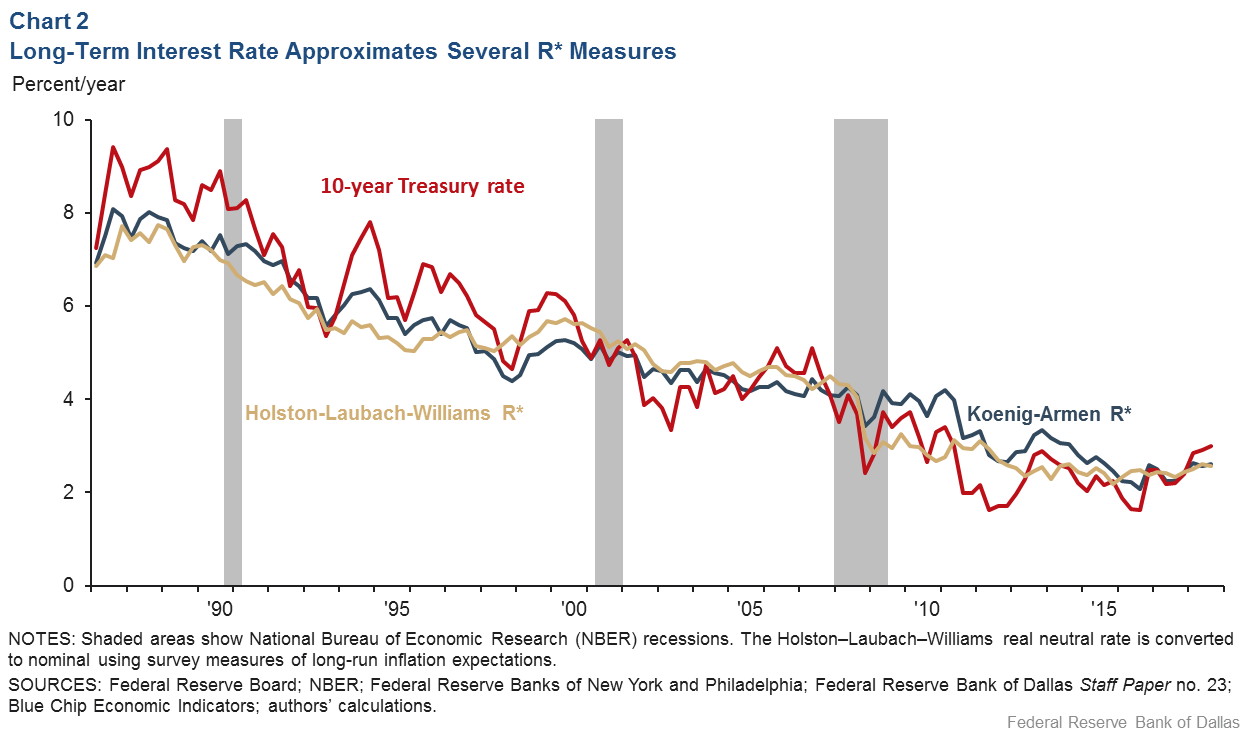

Because long-term interest rates are heavily influenced by investors’ short-term rate expectations, long-term rates likely well-approximate R*. In fact, the 10-year Treasury yield moves fairly closely with R* estimates produced by sophisticated statistical models (Chart 2). It follows that the slope of the yield curve approximates R – R*, the stance of monetary policy. A yield-curve inversion signals that monetary policy is tight (R > R*). Conversely, a steep yield curve signals that monetary policy is easy (R < R*).

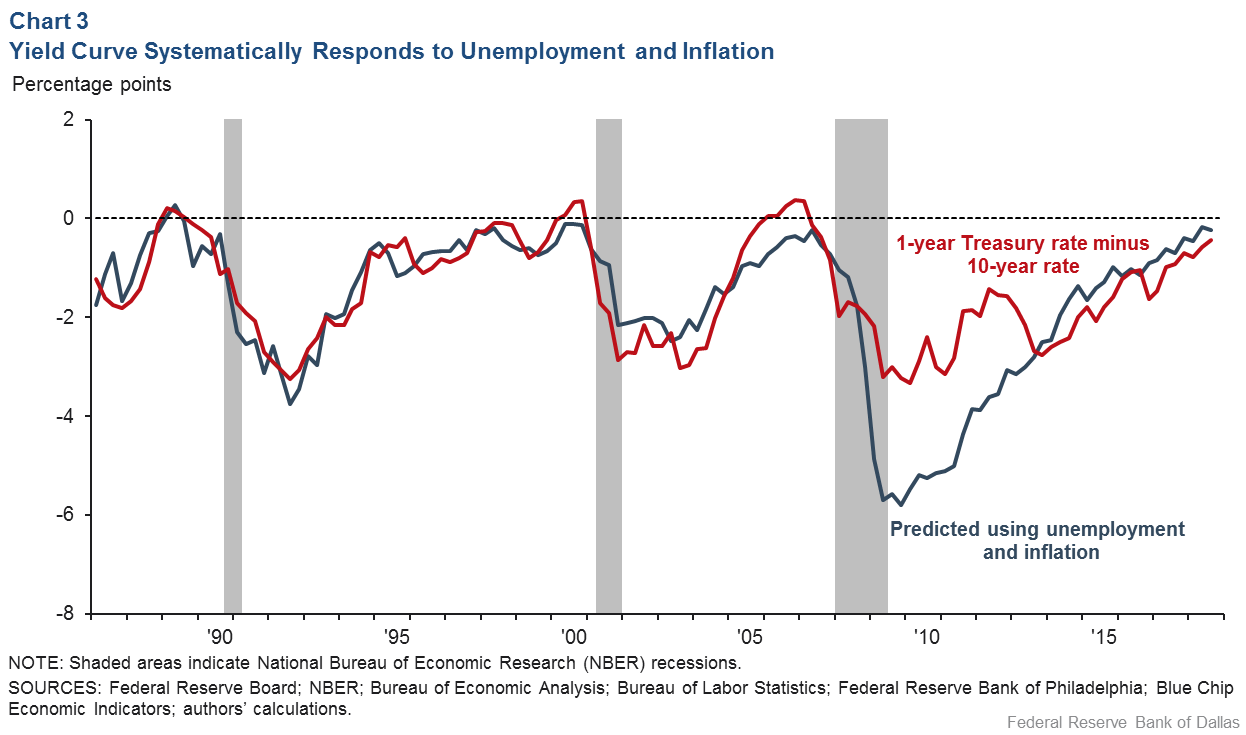

If this argument is correct, two things should be true. First, reflecting the Fed’s pursuit of its dual mandate, movements in the unemployment and inflation rates should explain yield-curve movements. The yield curve should be steep—with long-term interest rates significantly above short-term rates—when unemployment is high or inflation is low. The yield curve should be flat or inverted when unemployment is low or inflation is high. This has, indeed, been the case (Chart 3). The only notable departure from the expected pattern occurred from 2009 through 2013, when short-term rates were close to zero and the Federal Reserve could not easily further reduce them.

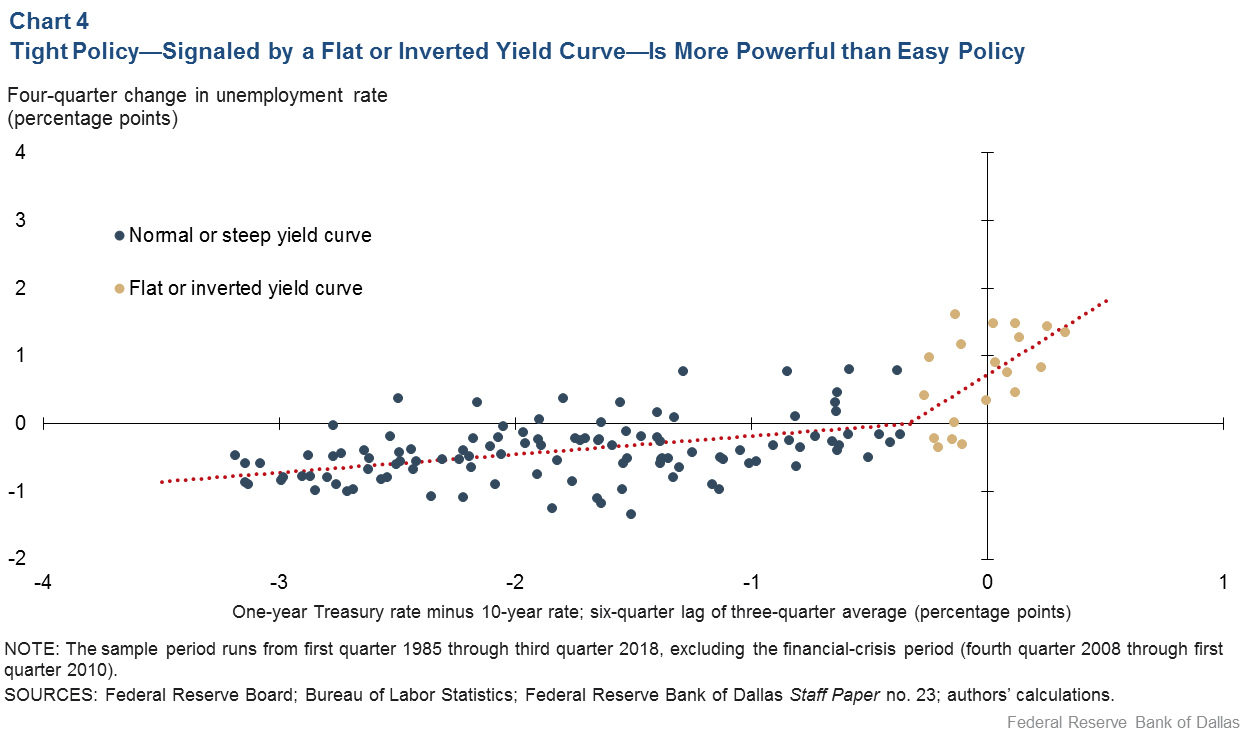

Second, the yield curve’s slope should be a good predictor of the economy’s future strength. Sure enough, the unemployment rate tends to fall when the yield curve is steep and to rise (with a lag that is long and variable) when the yield curve is inverted (Chart 4). The transition from unemployment decreases to unemployment increases occurs a bit before the yield curve inverts—when the short rate is near, but still below, the long rate.

Interestingly, the unemployment rate responds much more strongly to a flat or inverted yield curve than to a steep yield curve, as Chart 4 also shows. That fact may help explain why some policymakers questioned the predictive power of the yield curve in the late 1990s, toward the end of a very long economic expansion.

Watch the yield curve

Mind the yield curve. An inverted yield curve likely signals that monetary policy has become quite restrictive—perhaps because policymakers feel they need to push hard on the brake pedal to hold inflation in check. If the inversion is large or sustained, a rising unemployment rate is likely to follow. More generally, as the gap between long-term and short-term interest rates narrows, small policy moves may suddenly have a larger economic impact than before.

About the Authors

Evan F. Koenig

Koenig is a senior vice president and principal policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

Keith R. Phillips

Phillips is an assistant vice president and senior economist in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.