Corporate debt as a potential amplifier in a slowdown

As a central bank policymaker, I closely monitor various types of excesses and imbalances that may be developing in the economy. One of the areas I monitor is the level and growth of indebtedness in the household, government and corporate sectors. In previous essays, I have commented on the positive impacts of the deleveraging of the household sector since the Great Recession, and I have raised a cautionary flag regarding the growth of U.S. government debt, including a substantial increase in the present value of unfunded entitlements.

The purpose of this essay is to focus on trends in corporate debt growth and credit quality in the U.S. and discuss potential implications for economic conditions and financial stability.

Background on indebtedness in the U.S.

In the decade since the Great Recession, there has been an improvement in household balance sheets. In particular, it is estimated that household debt declined from 97 percent of gross domestic product (GDP) at year-end 2008 to approximately 75 percent as of Sept. 30, 2018.[1] This trend has been aided by a strong jobs market and improving wage growth. This household deleveraging is very important because consumer spending is approximately 70 percent of U.S. GDP.[2]

While household balance sheets have improved, the U.S. government has become more highly indebted. Government debt (primarily in the form of Treasury obligations) held by the public as a percentage of GDP has grown from 44 percent at year-end 2008 to approximately 77 percent as of Dec. 31, 2018.[3] In addition, the present value of unfunded entitlements now stands at approximately $54 trillion.[4] This growing level of government debt as a percentage of GDP means, at a minimum, there is less capacity for infrastructure spending and other investments which might help build the productive capability of the U.S. economy. It also means that in the next downturn, there is likely to be less capacity for fiscal stimulus.

Historically, the U.S. government has tended to reduce its degree of leverage when the economy is strong—that has not been the case this cycle. At the later stages of a long economic expansion, recent fiscal actions have had the impact of increasing government debt to GDP and have provided meaningful stimulus to near-term growth. It is our view at the Dallas Fed that the current path of government debt to GDP is unlikely to be sustainable—and if we need to find ways to moderate our debt growth in the future, this moderation is likely to create headwinds for GDP growth.

In addition to household and government debt, Dallas Fed economists also keep track of the level and growth of corporate debt in the financial sector as well as the nonfinancial sector of the U.S. economy. On the positive side, U.S. financial sector debt has declined substantially from near its historical peak of approximately 124 percent of GDP at the end of 2008 to 78 percent as of Sept. 30, 2018.[5] This decline was accompanied by substantially more stringent postcrisis financial sector regulations and oversight intended to reduce the systemic risk and improve the resiliency of the U.S. financial sector.

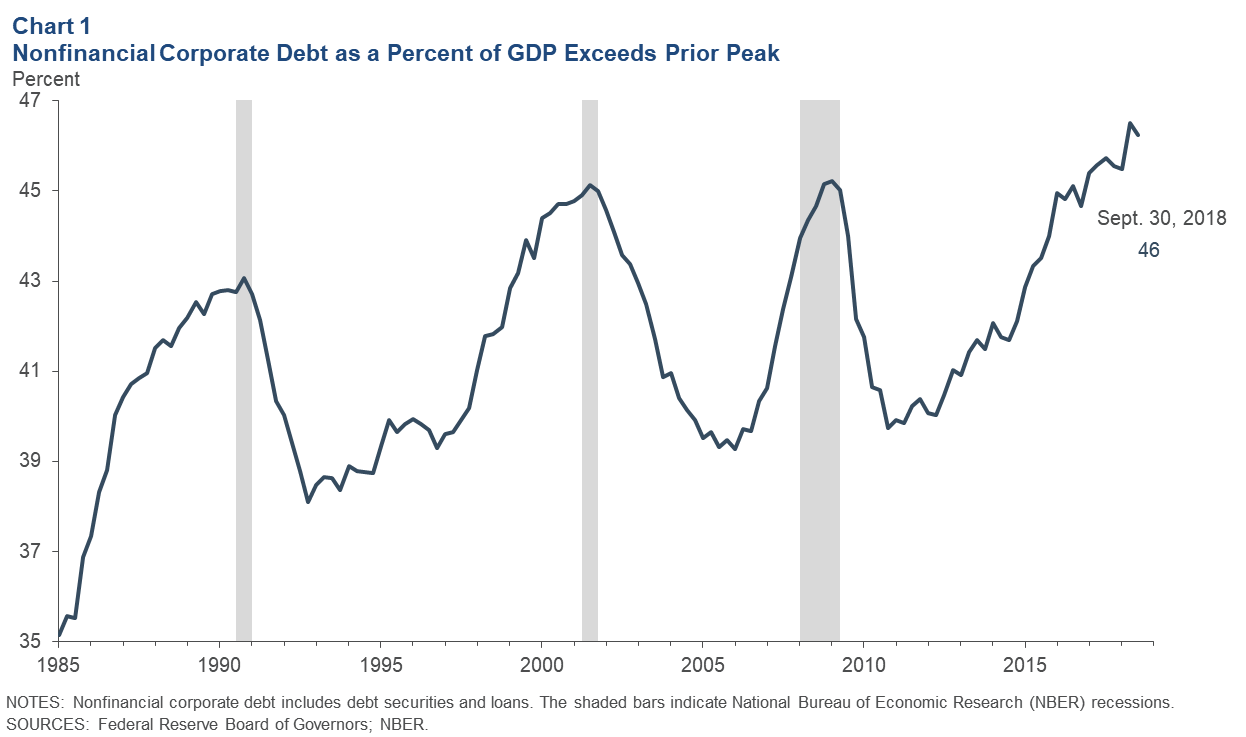

By contrast, U.S. nonfinancial corporate debt as a percentage of GDP is now higher than the prior peak reached at the end of 2008. As seen in Chart 1, U.S. nonfinancial corporate debt as a percentage of GDP declined substantially in the aftermath of the Great Recession, but then rebounded from a postrecession low of approximately 40 percent in 2010 to 46 percent as of Sept. 30, 2018.[6],[7]

This rebound in the amount of nonfinancial corporate debt is something I am carefully considering in assessing economic conditions and financial stability in the U.S. In particular, it is worth noting that a number of research studies have indicated that relatively higher levels of corporate debt to GDP could potentially amplify the severity of a recession.[8] Several of these papers also suggest that strong growth in corporate debt to GDP is more likely to amplify a downturn when corporate leverage is historically elevated, as it is today.[9]

Trends in nonfinancial corporate debt

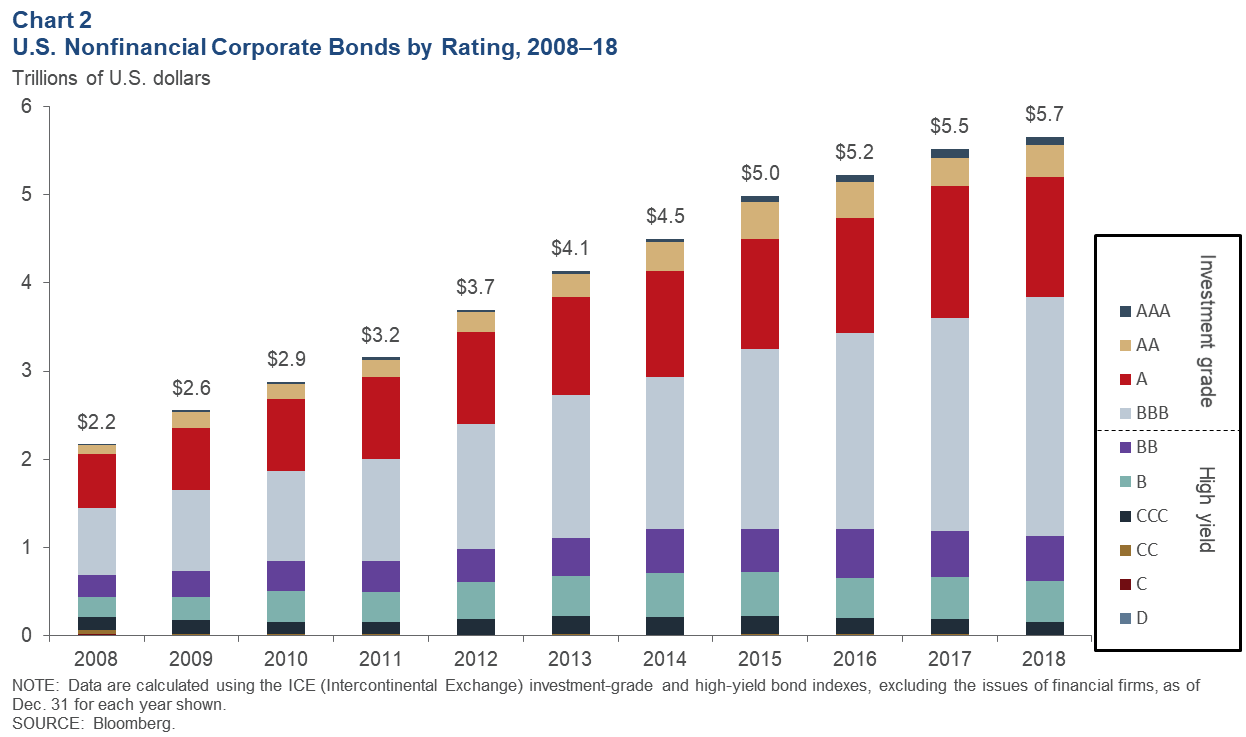

Nonfinancial corporate debt consists primarily of bonds and loans (commercial paper outstanding is less than 5 percent of the total). Nonfinancial corporate bonds outstanding in the U.S. grew from approximately $2.2 trillion in 2008 to approximately $5.7 trillion at year-end 2018 (Chart 2). The bulk of this growth occurred in the investment-grade sector. The amount of outstanding U.S. investment-grade nonfinancial corporate bonds grew from approximately $1.5 trillion in 2008 to $4.5 trillion at year-end 2018.[10]

Within the investment-grade sector, there was a notable increase in the amount of BBB bonds (the lowest level of investment-grade debt) outstanding, growing from approximately $0.8 trillion in 2008 to $2.7 trillion by year-end 2018.[11] In addition, the amount of high-yield (less than investment grade) nonfinancial corporate bonds outstanding grew from approximately $0.7 trillion in 2008 to $1.1 trillion by year-end 2018. This substantial growth in BBB and lower-rated bonds is indicative of a weakening in corporate credit quality in the U.S.

It is estimated that a substantial portion of the increase in nonfinancial corporate debt was used to fund share buybacks, dividends and merger activity.[12] This trend has been accompanied by more relaxed bond and loan covenants,[13] which have had the effect of reducing protections for investors.

There has also been an increase in syndicated leveraged loans over this period. Leveraged loans are loans made to highly indebted companies and are typically originated by commercial banks and then syndicated to nonbank investors, including special-purpose vehicles such as collateralized loan obligations (CLOs), private equity funds and other stand-alone entities. The size of the syndicated leveraged loan market, which is primarily made up of nonfinancial corporate borrowers, has increased from $0.6 trillion at the end of 2008 to $1.2 trillion at year-end 2018.[14] Much of this increase has occurred to fund corporate acquisitions and private-equity-backed transactions.[15]

In addition to the syndicated leveraged loan market, there is also a direct lending market for leveraged loans in the U.S. This market primarily involves nonbank financial firms—such as asset managers, private equity funds, business development corporations (BDCs), hedge funds, insurance companies and pension funds—lending directly to smaller, mid-market companies. While it is difficult to obtain precise information on the size of this market, Standard and Poor’s (S&P) estimates that the amount of outstanding leveraged loans in the U.S. direct lending market has grown significantly over the past several years and now likely exceeds several hundred billion dollars.[16]

CLO structure

CLOs are investment vehicles that buy pools of floating-rate leveraged loans from banks. The CLO packages loans into tranches of debt with credit ratings ranging from AAA to BB and with one nonrated tranche of equity, as illustrated in Chart 3. These tranches are securitized and then sold primarily to institutional investors.

The ability of a CLO to turn lower-credit-quality loans into mostly investment-grade-rated bonds via securitization hinges on three key factors: 1) overcollateralization, 2) tranching of securities based on levels of subordination, and 3) portfolio diversification. As loans are paid off, the income flows to the buyers of the CLO securities. In case of a default in one of the underlying loans, the lowest tranche (equity) is the first to experience a loss, whereas the AAA tranche would be the last to experience a loss. Unlike mortgage-backed securities, the CLO structure proved relatively resilient during 2008–09.

The U.S. CLO market has grown from roughly $300 billion at the end of 2008 to $615 billion at the end of 2018.[17] However, it is important to recognize that CLO loan-credit quality today is estimated to be somewhat weaker than 10 years ago.

S&P estimates that in 2018, CLOs and loan mutual funds purchased approximately 60 percent and 20 percent, respectively, of syndicated leveraged loan volumes. It is estimated that less than 10 percent of new issuance was purchased by banks in the U.S. The remaining volumes were purchased by insurance companies, finance companies and others.[18] Because CLOs are today the largest buyer of these syndicated leveraged loans, disruptions to CLO creation could increase the likelihood that leveraged loans remain on bank balance sheets, which could, in turn, limit the ability of affected banks to extend credit during periods of stress.

Implications of rising levels of BBB and less-than-investment-grade corporate debt

As a central banker, I am carefully tracking the growth in BBB and less-than-investment-grade debt. In the event of a downturn, highly indebted companies may be more vulnerable to seeing their credit quality deteriorate, which could negatively impact their capital spending and hiring plans. If this deterioration were sufficiently widespread, credit spreads would likely widen in order to compensate lenders/bondholders for greater risk. This type of widening would likely be indicative of an overall tightening in financial conditions that could, in turn, lead to a more significant slowing in the economy.

In a downturn, some proportion of BBB bonds may be at risk of being downgraded to less than investment grade. These downgrades, if they happen in sufficient size, could create dislocations for investors who tend to have specific allocations or restrictions based on credit-rating categories. These dislocations could further negatively impact credit spreads and market access for more highly indebted companies.

Market liquidity

One further issue is whether there is sufficient liquidity in the various corporate debt markets. Ample liquidity is particularly important in the event of market stress or dislocation.

While there is debate regarding the evidence of a decline in various measures of corporate bond market liquidity—such as round-trip trading costs, bid–ask spreads or turnover[19]—it is generally agreed that bank-affiliated broker-dealers have been committing less capital to corporate bond trading since the financial crisis. In particular, it is estimated that inventories of corporate debt held by broker-dealers declined from $29.2 billion at the end of 2013 to $14.2 billion at the end of 2018.[20]

This decline is notable given that the total corporate bond market increased 36 percent over this period. The decline in inventories held by broker-dealers may be due, at least in part, to postcrisis regulation, such as the Volcker rule (effective April 2014), as well as the growth in electronic trading and other market-related factors.[21]

In the event of an economic downturn and some credit-quality deterioration, the reduction in bank broker-dealer inventories and market-making capability could mean that credit spreads might widen more significantly, and potentially in a more volatile manner, than they have historically. This concern may be somewhat heightened in light of the rapid growth in BBB and lower-rated securities issuance over the past 10 years.

Conclusion: Continued Vigilance

I will continue to closely monitor the level, growth and credit quality of corporate debt. Vigilance is warranted as these issues have the potential to impact corporate investment and spending plans. In the event of an economic downturn, these issues could also contribute to a deterioration in financial conditions which could, in turn, amplify the severity of a growth slowdown in the U.S. economy.

I am also sensitive to these corporate debt developments in light of the historically high level of U.S. government debt and the forward estimates for the path of government debt to GDP. An elevated level of corporate debt, along with the high level of U.S. government debt, is likely to mean that the U.S. economy is much more interest rate sensitive than it has been historically.

Notes

- Data are from the Bureau of Economic Analysis (BEA), Federal Reserve Board and Haver Analytics. Household debt is from the Federal Reserve Board’s flow of funds series and is defined as households and nonprofit organizations; debt securities and loans; liability.

- Data are from the BEA.

- Data are from the BEA, U.S. Treasury and Haver Analytics. Government debt is from the U.S. Treasury, Monthly Statement of the Public Debt, as total public debt outstanding held by the public.

- “The 2018 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds,” Centers for Medicare and Medicaid Services, June 5, 2018.

- Data are from the BEA, Federal Reserve Board and Haver Analytics. Financial sector debt is from the Federal Reserve Board’s flow of funds series and is defined as the debt securities and loans of the domestic financial sector.

- Data are from the BEA, Federal Reserve Board and Haver Analytics. Nonfinancial corporate debt is from the Federal Reserve Board’s flow of funds series and is defined as the debt securities and loans of the nonfinancial corporate business sector.

- A broader measure of nonfinancial corporate indebtedness is total liabilities, which increased from 91 percent of GDP at the end of 2008 to 102 percent at the end of 2017, and has since declined to 99 percent as of Sept. 30, 2018. This measure includes other liabilities that are excluded from the series displayed in Chart 1, such as loans from private equity funds and hedge funds, trade finance and foreign direct investment, which has both a debt and an equity component.

- See, for example, “U.S. Corporate Leverage: Developments in 1987 and 1988,” by Ben S. Bernanke, John Y. Campbell and Toni M. Whited, Brookings Institution, Brookings Papers on Economic Activity, vol. 21, no. 1, 1990, pp. 255–86; and “The Financial Accelerator in a Quantitative Business Cycle Framework," by Bernanke, Mark Gertler and Simon Gilchrist, Handbook of Macroeconomics, edition 1, vol. 1, John B. Taylor and Michael Woodford, ed., Elsevier, 1999, pp. 1,341–93.

- See, for example, “Down in The Slumps: The Role of Credit in Five Decades of Recessions,” by Jonathan Bridges, Chris Jackson and Daisy McGregor, Bank of England Staff Working Paper no. 659, April 2017.

- Data are from Bloomberg and are calculated using the ICE (Intercontinental Exchange) investment-grade and high-yield bond indexes, excluding the issues of financial firms, as of Dec. 31 for each year shown.

- Note that, according to Moody’s Investors Service, BBB-rated corporate bonds are highly concentrated, with 20 issuers totaling 45 percent of outstanding BBB-rated debt out of a universe of approximately 300 BBB-rated issuers.

- Data are from Standard and Poor’s (S&P) Global Market Intelligence’s Leveraged Commentary and Data (LCD). Also see “Buybacks to Top Use of S&P 500 Companies’ Cash in 2019: Goldman Sachs,” Reuters, Oct. 5, 2018.

- See, for example, the Monetary Policy Report—February 2019, Federal Reserve Board, Feb. 22, 2019.

- Data are from S&P Global Market Intelligence’s LCD.

- For an explanation of leveraged loans, see S&P Global’s LeveragedLoan.com.

- Private sector estimates for the size of the direct nonbank leveraged lending market include estimates of $900 billion. (Note that some portion of this category may not be captured in the nonfinancial corporate debt series used in Chart 1.) See “Six Key Risks in Leveraged Lending for Financial Institutions,” S&P Global, Nov. 26, 2018.

- Data are from the Securities Industry and Financial Market Association.

- See “Six Key Risks in Leveraged Lending for Financial Institutions,” S&P Global, Nov. 26, 2018.

- See, for example, “Report to Congress on Access to Capital and Market Liquidity Study,” Securities Exchange Commission, 2017.

- Inventories of corporate debt held by broker-dealers are from the Federal Reserve Bank of New York, Primary Dealer Statistics, net position of corporate commercial paper and corporate bonds, notes and debentures.

- See, for example, “The Volcker Rule and Market Making in Times of Stress,” by Jack Bao, Maureen O’Hara and Xing (Alex) Zhou, Journal of Financial Economics, vol. 130, no. 1, 2018, pp. 95–113; and “Capital Commitment and Illiquidity in Corporate Bonds,” by Hendrik Bessembinder, Stacy Jacobsen, William Maxwell and Kumar Venkataraman, Journal of Finance, vol. 73, no. 4, 2018, pp. 1,615–61.

About the Author

Robert S. Kaplan was president and CEO of the Federal Reserve Bank of Dallas, 2015–21.

From the Author

I would like to acknowledge the contributions of Tyler Atkinson, Michele Brown, Jill Cetina, Jennifer Chamberlain, Justin Chavira, Jim Dolmas, Marc Giannoni, James Hoard, Alexander Johnson, Amy Jordan, Evan Koenig, Alex Musatov, Laton Russell, William Simmons, Irfan Taj, Kathy Thacker and Joe Tracy in preparing these remarks.

The views expressed are my own and do not necessarily reflect official positions of the Federal Reserve System.