Modern refineries, shale boom upend traditional oil price relationships

Different crude oils can sell for dramatically different prices with sometimes far-reaching effects on the energy industry—from impacts on oil producers’ production decisions to oil refineries’ profit margins. The global refining sector‘s expanding ability to process low-quality crude oil and a growing supply of high-quality shale oil have significantly reduced price differences between low- and high-quality crude oils since the Great Recession.

These fundamental changes in the oil industry appear to have permanently affected the size of many quality-related oil price differentials. More recently, U.S. sanctions on Venezuela and OPEC production cuts have also played important roles in determining those differentials.

Quality underlies many oil price differentials

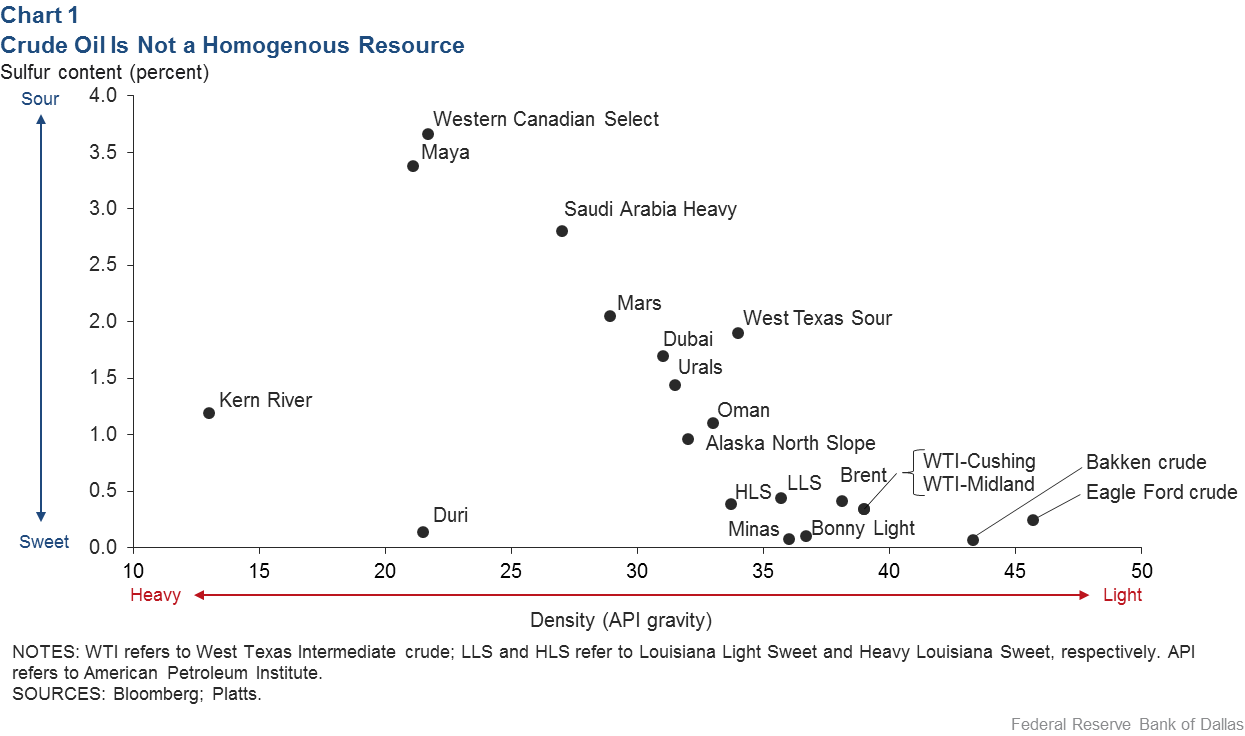

Crude oil can have a wide range of physical characteristics, a primary reason that oil price differentials exist. Two main characteristics of a crude oil are its American Petroleum Institute gravity (API gravity), which measures density, and its sulfur content. The industry labels a crude oil as light, medium or heavy based on its API gravity, and sweet or sour based on its sulfur content. Chart 1 plots a range of crude oils in terms of API gravity and sulfur.

There is a hierarchy of quality in terms of density, with light at the top and heavy at the bottom, and in terms of sulfur content, from sweet crudes to sour ones. Prices follow the same order—with light-sweet crudes usually selling at a premium and heavy-sour crudes at a discount. The premiums attached to light crude oil can be substantial, at times exceeding 30 percent.

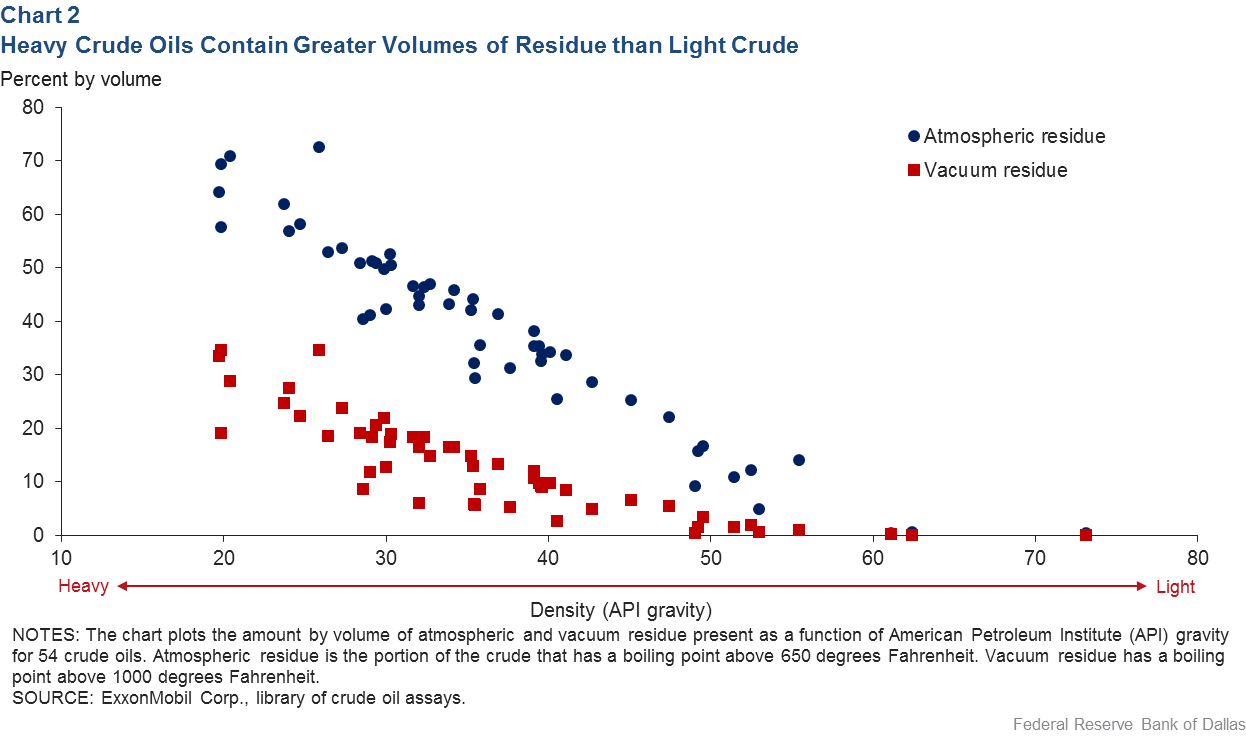

Light-sweet crude commands this price edge because when distilled—the first step of processing any crude oil—it yields a large percentage of high-valued petroleum products, such as gasoline and diesel. Denser oils (medium and heavy crudes) yield less of those products when distilled and more of what is known as atmospheric residue (Chart 2).

Most modern refineries distill atmospheric residue using special equipment. This process produces its own leftover, often referred to as vacuum residue. As with the first-stage distillation, low-quality crude oil contains more vacuum residue than high-quality crude oil, as seen in Chart 2.

Essentially, vacuum residue is residual fuel oil, a low-value product mostly used to fuel ships. The price differences between products such as gasoline and residual fuel oil are generally very large.

The discount placed on low-quality crude creates a potential arbitrage opportunity for anyone who has a way to transform residual content into higher-value products. This is where complex refineries come into play. They possess specialized equipment—crackers and cokers—that enable them to produce more gasoline and diesel from a given barrel of low-quality feedstock. The most complex refiners processing a heavy crude can often produce as much gasoline and diesel as many simpler refineries can with more expensive, high-quality crude oil.

A fundamental shift after the Great Recession

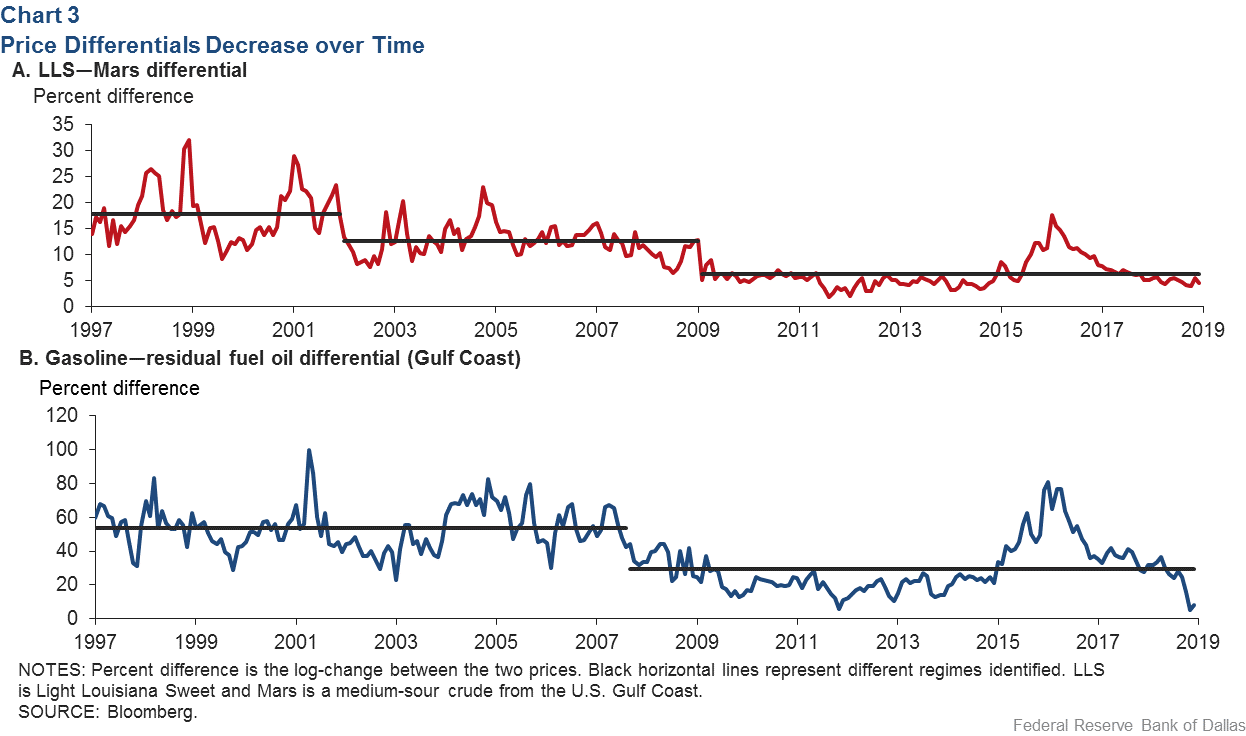

Price differentials between grades of crude have decreased substantially since 1997, our recent study found. Chart 3, Panel A, illustrates an example of this by plotting the percent difference between two crudes on the U.S. Gulf Coast: a light-sweet oil, LLS, and a medium-sour crude, Mars.

The decline is a worldwide phenomenon, with a major break around the Great Recession (2007–09) affecting more than 20 quality-related differentials. The average value of many of those differentials has declined to half of what it was before the recession.

One explanation for why quality-related differentials have not rebounded since the Great Recession is that the global refining sector has added a significant amount of capacity to process low-quality crude oils over the last decade. In essence, complex refiners arbitraged away much of the quality-related price differential that previously existed.

Put differently, there is now a much greater ability to transform the residual from medium and heavy crude oils into more valuable products. It is perhaps not surprising that differentials between high- and low-valued refinery outputs have also significantly narrowed since the Great Recession. Chart 3, Panel B, shows an example of this using the percent difference in gasoline and residual fuel oil spot prices on the Gulf Coast.

Shale boom boosts light oil supply

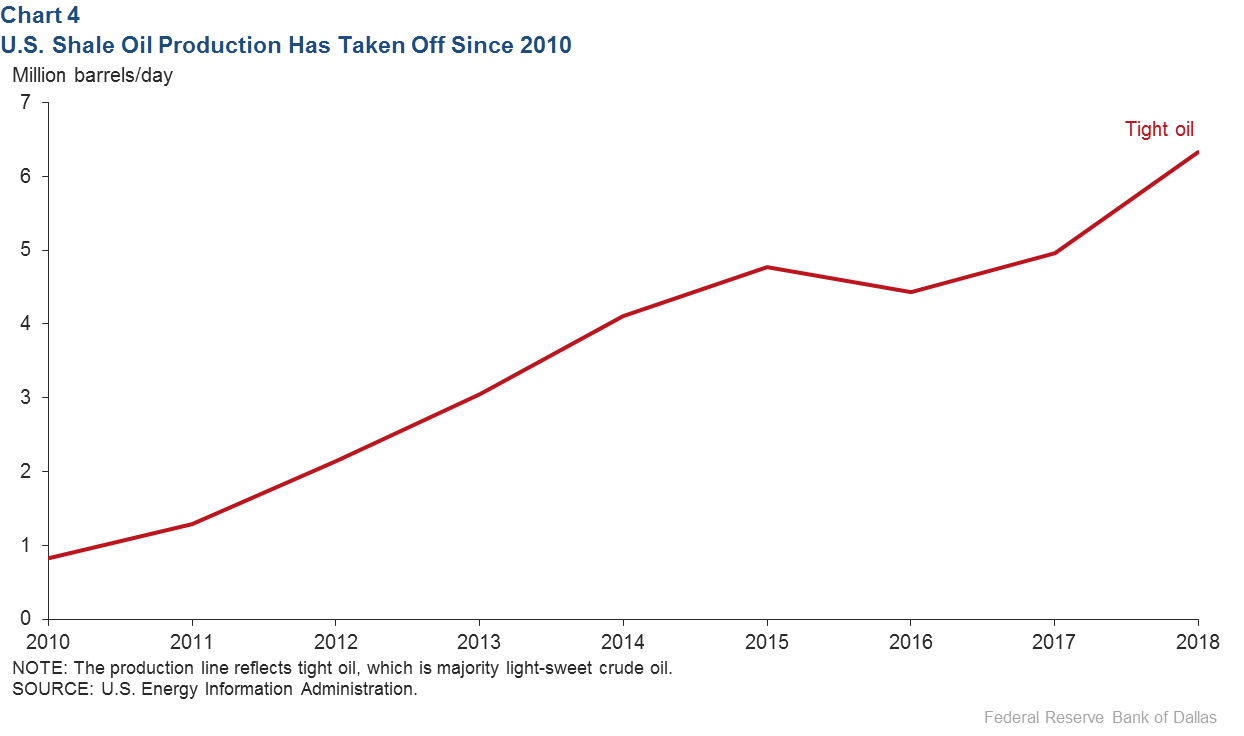

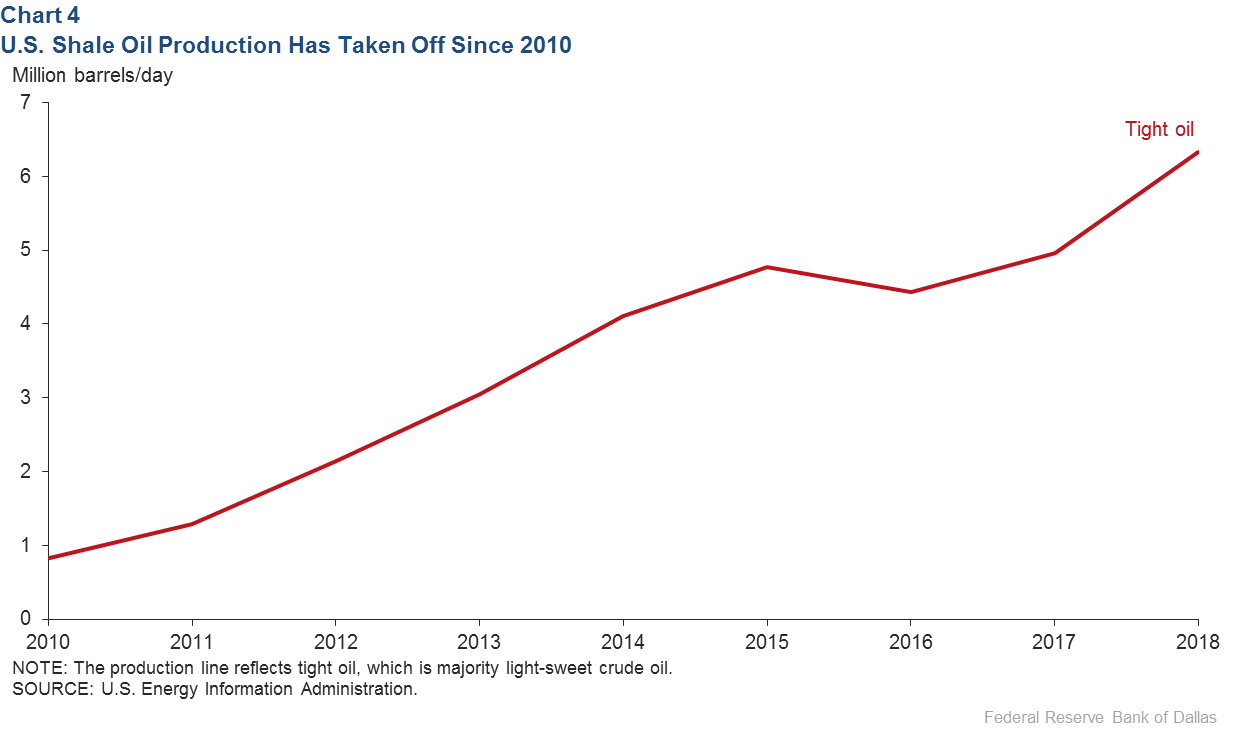

The emergence of shale tells another, complementary part of the story. The shale boom produced a very large, unexpected increase in the supply of U.S. tight oil, which is primarily light-sweet crude oil (Chart 4). This oil contains relatively small amounts of residual products. As a result, the boom naturally compresses price differences between high- and low-valued petroleum products, such as gasoline and residual fuel oil and, thus, price differences between high- and low-quality crude oil.

{kind=link}

Venezuelan sanctions, OPEC cuts affect differentials

Recent U.S. economic sanctions on Venezuela have restricted U.S. companies from buying its crude. U.S. Gulf Coast refiners, many designed to handle lower-quality oil, have historically depended on Venezuela as an important supplier. Those refiners have had to look elsewhere for their supplies, further narrowing price differences between high- and low-quality crude, particularly on the U.S. Gulf Coast.

OPEC production cuts—voluntary or otherwise—have also contributed to narrowing differentials. Saudi Arabia, Kuwait and the United Arab Emirates collectively cut output by more than 1 million barrels per day from November 2018 to February 2019. Production in Iran, previously OPEC’s third-largest supplier, declined by more than a million barrels per day from May 2018 to February 2019 following a reimposition of U.S. sanctions. All of these countries produce a substantial amount of medium-sour crude.

Although quality-related differentials could again widen, there is no reason expect a long-term return to levels seen before the Great Recession. The increased complexity of the global refining sector and the shale production boom are long-lasting factors whose influence will be around for years to come.

About the Authors

Grant Strickler

Strickler is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Michael Plante

Plante is a senior research economist in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.