Energy Indicators

| Energy dashboard (April 2024) | |||

| WTI price avg. April 15–April 19 |

WTI price change from 4 weeks prior |

Henry Hub price avg. Feb. 26–March 1 |

Henry Hub price change from 4 weeks prior |

| $84/barrel | +2.0% | $1.73/MMBtu | +3.0% |

Gasoline prices have been on the rise, while crude oil and refined products inventories are healthy. The Dallas Fed’s Energy Survey showed that smaller firms need higher oil prices to profitably drill new wells, and energy headcounts are expected to hold steady in 2024. So far, 2024 payrolls are flat.

Crude and refined products

Gasoline prices tick up

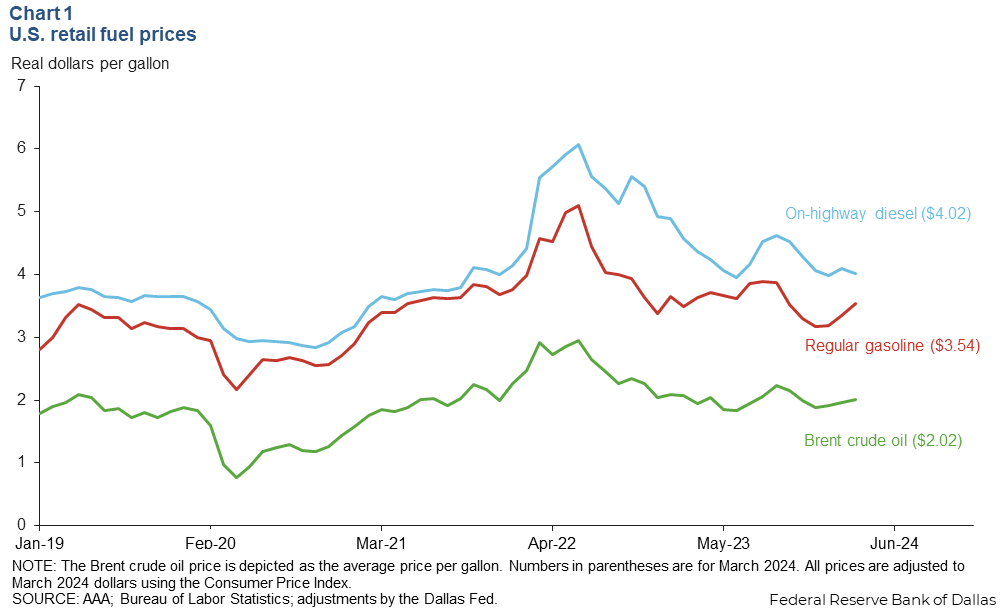

Retail gasoline prices have been on the rise. Regular gasoline rose to $3.54 per gallon for the month of March, up 8.7 percent since the start of the year (Chart 1). On-highway diesel rose to $4.02 for the same month, up only 1.3 percent. For comparison, the price of Brent crude, which made up 56 percent of the price of a gallon of gasoline and 47 percent of the price of diesel in March, rose 9.5 percent.

Fuel prices have risen on higher oil prices, healthy consumption and other factors. Unplanned refinery outages as well as routine maintenance in February and March reduced fuel production at the same time warmer weather in early spring enabled more travel demand. Ukrainian drone attacks on Russian refineries also may have played a role in higher prices, disrupting at least 10 percent of Russian capacity.

Crude oil prices rise above $80 a barrel

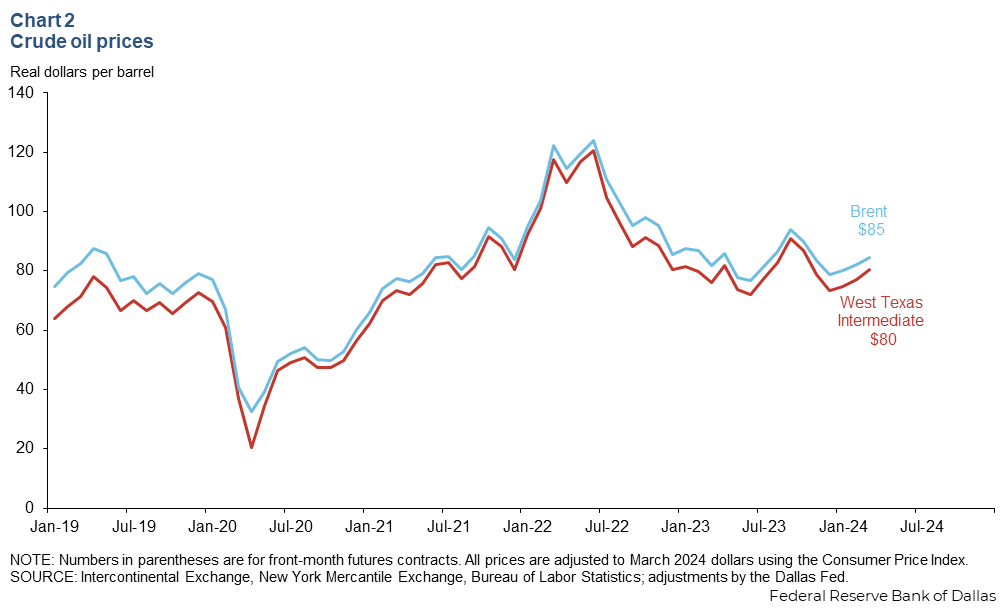

The rise in monthly average crude oil prices was unabated over the first three months of the year. Brent crude rose from an average of $79 a barrel in December 2023 to $85 a barrel in March, while West Texas Intermediate (WTI) went from $73 a barrel to $80 a barrel (Chart 2).

The increase was due in part to the extension of OPEC+ cuts keeping supply off the market, geopolitical concerns regarding the Israeli-Hamas conflict, fears of wider tensions in the Middle East and global oil demand outpacing expectations in the first quarter of the year.

Inventories on par with five-year averages

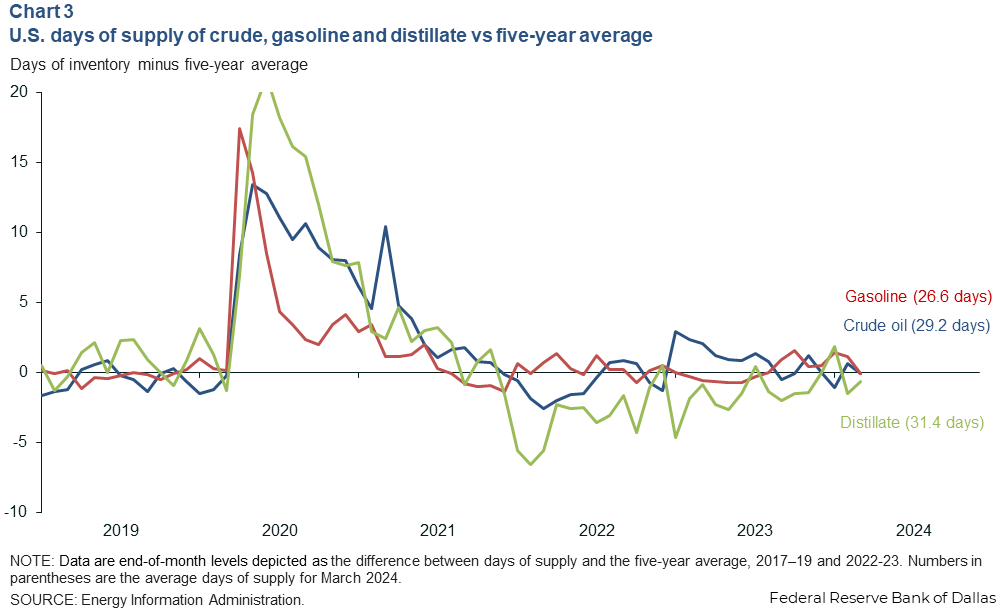

There were 31.4 days of cover (the number of days domestic inventories would likely last at the recent pace of consumption) for distillate at the end of March. That is 0.7 days below the five-year average (excluding the pandemic) for March (Chart 3). Crude oil and gasoline days of cover were on par with their five-year averages at 29.2 and 26.6, respectively.

From the last week of February to the last week of March, days of supply of gasoline in the U.S. declined 11 percent mainly due to an increase in consumption, which rose 9 percent during the same time frame.

Using a four-week moving average, U.S. refinery inputs of crude oil declined 624,000 barrels per day (4 percent) from the week ending Dec. 29, 2023 to the week ending March 29, 2024, helping push crude oil days of cover up 7 percent over the same time frame.

The four-week moving average for refinery capacity utilization now stands at 87.9 percent. The Energy Information Administration reports U.S. crude oil stocks for the week of March 29 at 815.1 million barrels. That is an increase of 0.5 percent from the previous week but a decrease of 3.1 percent from a year ago.

Well drilling

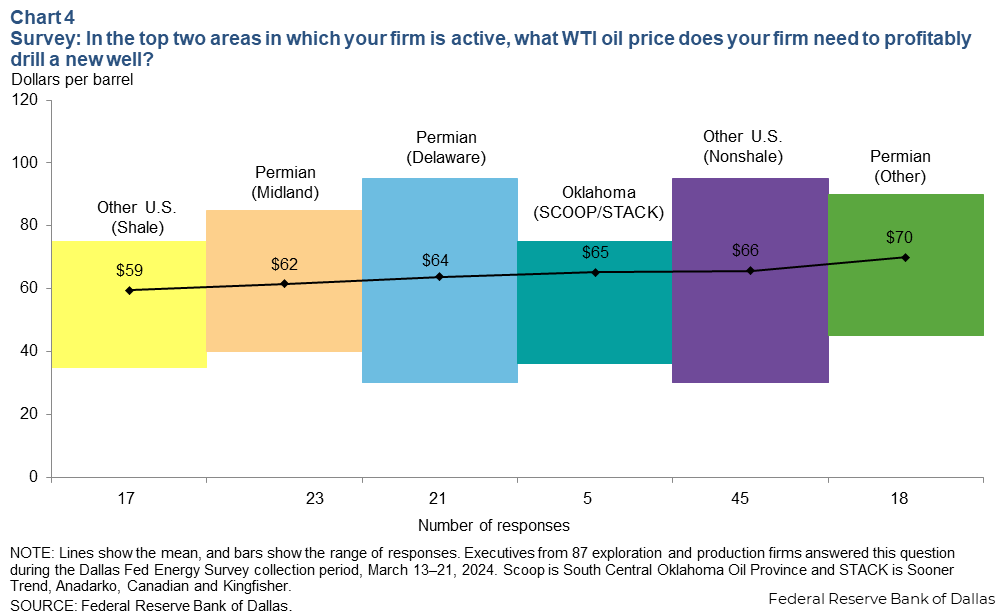

Executives of exploration and production (E&P) firms said in the Energy Survey the WTI oil price needed to profitably drill a new well ranged from $59 a barrel to $70 a barrel (Chart 4). There is a notable difference between the break-even price per barrel for large and small firms; large firms require only $58 per barrel for profitability, compared with small firms that require $67.

Oil and gas jobs

Oil and gas payrolls are steady

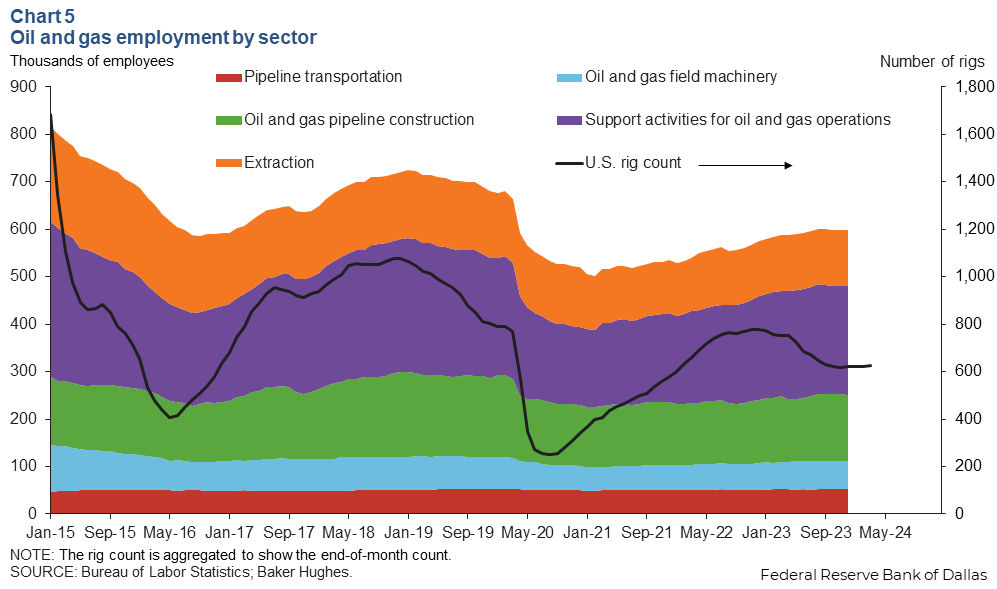

In the latest monthly data from the U.S. Bureau of Labor Statistics, oil and gas jobs increased very slightly in February to 606,700 (Chart 5). Of those jobs, 231,400 are support roles for oil and gas operations, and another 143,900 are in pipeline construction. February marks the highest total for these sectors since March 2020. The industry has added 7,700 jobs in the first two months of the year.

In contrast, the rig count has only increased 2 rigs from the beginning of the year to March. Looking at the major U.S. basins, the Permian added 4 rigs, the Eagle Ford added 2 and the Bakken added 2, while the Barnett lost 1, the DJ-Niobrara lost 2 and the Haynesville lost 4.

The stagnation in the rig count is especially evident with the Bakken, in North Dakota and Montana, where the rig count has been between 32 and 34 since late summer 2023.

Headcount to hold steady

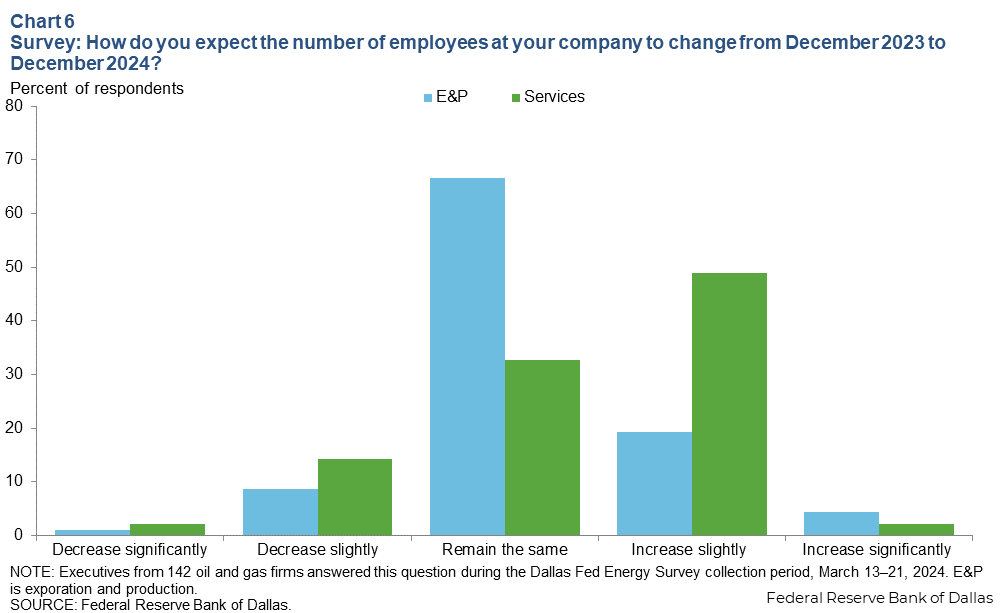

Of the oil and gas executives who answered the Dallas Fed Energy Survey, 67 percent of E&P firms said they plan to keep the number of employees steady in 2024, while only 33 percent of oil field service firms said the same (Chart 6). Of oil field service firms, 49 percent instead said they are planning to slightly increase headcount. Survey respondents noted the cost of labor continues to challenge their bottom lines and is thinning margins.

About Energy Indicators

Questions can be addressed to Kenya Schott at kenya.schott@dal.frb.org. Energy Indicators is released monthly and can be received by signing up for an email alert. For additional energy-related research, please visit the Dallas Fed’s energy home page.