Austin Economic Indicators

December 5, 2019

The Austin economy continued to grow at a healthy pace in October. The Austin Business-Cycle Index grew near its long-term average. A tight labor market persisted as the metro unemployment rate remained near historical lows. Job growth slowed somewhat but was strong in the construction and leisure and hospitality industries. Office demand remained strong, while the residential housing market posted solid performance with increased home construction permits and existing-home sales.

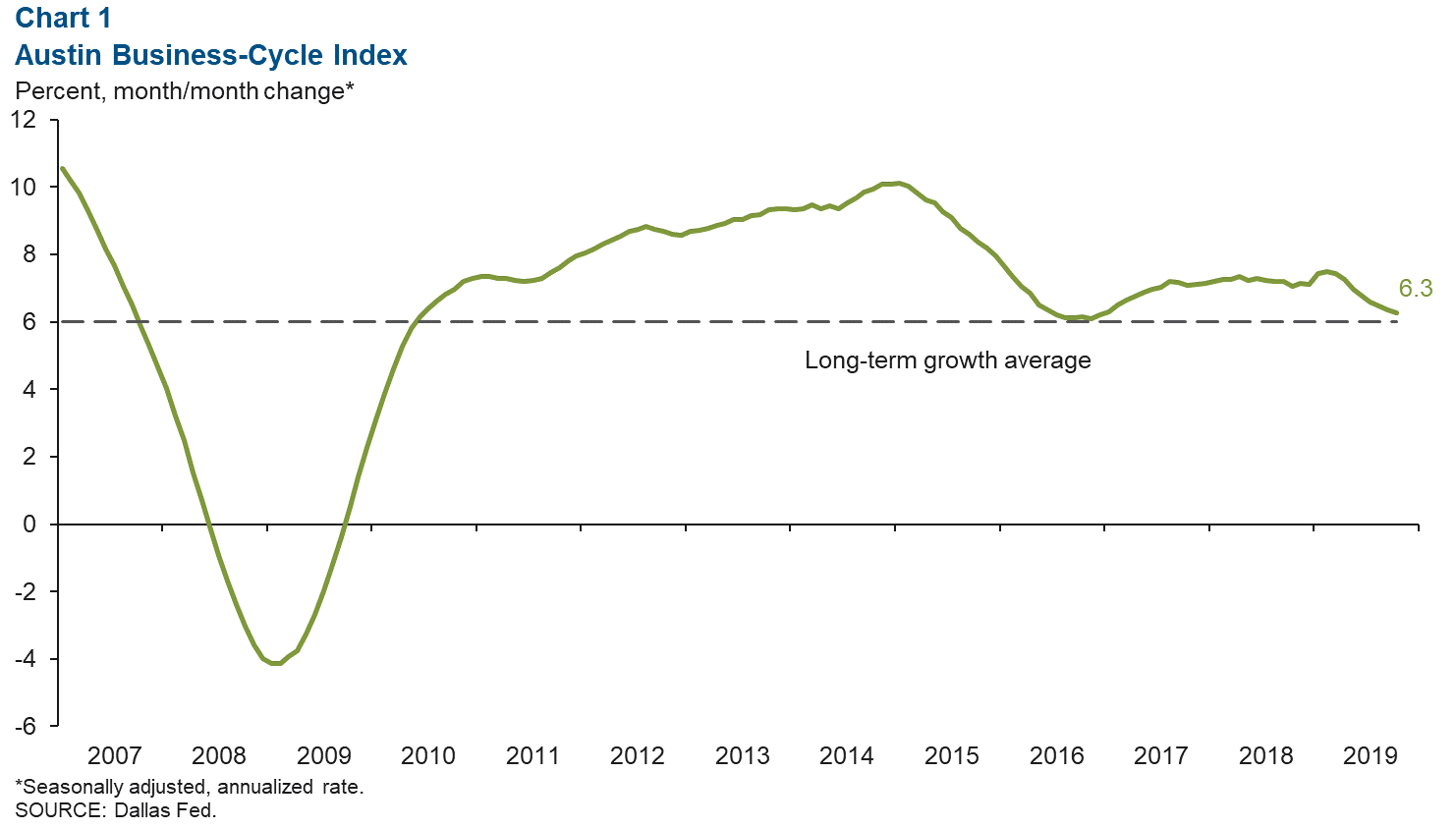

Business-Cycle Index

As of October, the Austin Business-Cycle Index expanded consecutively for more than 10 years (Chart 1). From September to October, the index grew 6.3 percent—slightly above its long-term trend of 6.2 percent but the lowest rate since December 2016. The recent moderation in growth in the index is likely due to tightness in the labor market constraining job growth.

Labor Market

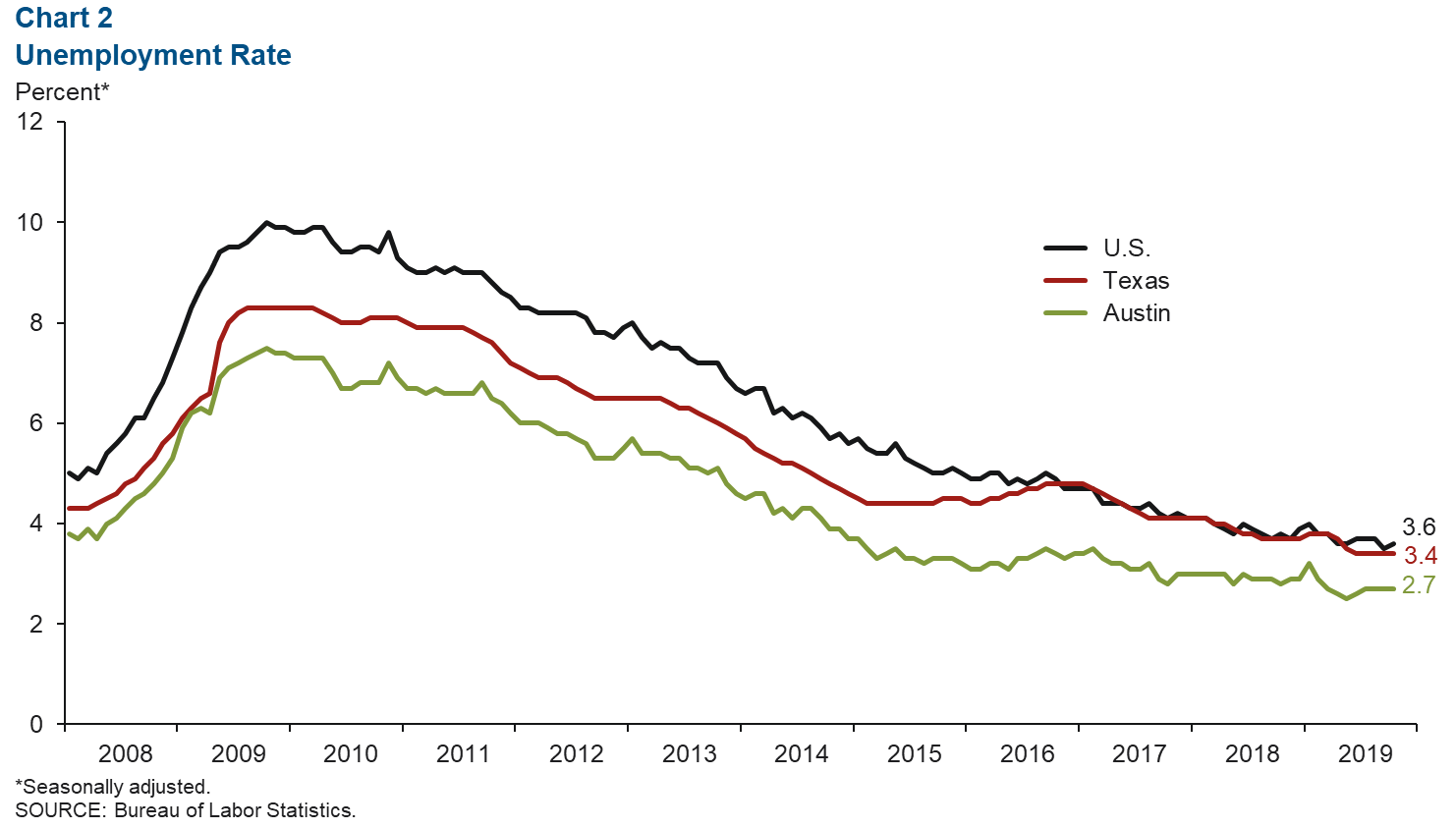

Unemployment Rates Hold Near Historical Lows

Austin’s unemployment rate remained at 2.7 percent in October, unchanged since July (Chart 2). The unemployment rate for the state lingered at 3.4 percent for the fourth consecutive month, while the jobless rate for the nation ticked up to 3.6 percent. This year through October, the metro’s labor force expanded 2.1 percent annualized, lagging in growth relative to the same period in 2017 (3.6 percent) and 2018 (2.7 percent).

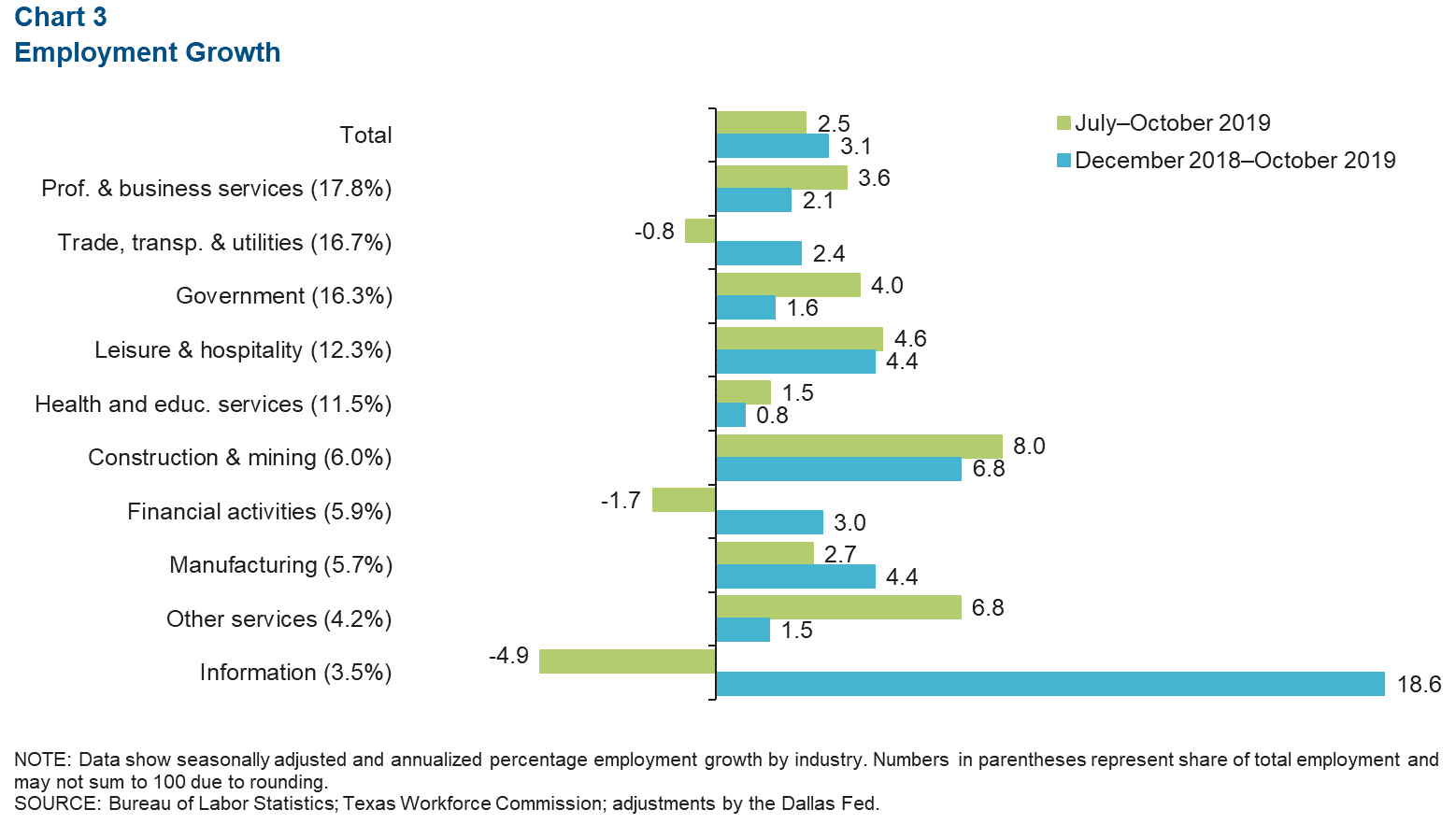

Job Growth Broad Based

In the three months ending in October, Austin added jobs at a 2.5 percent annualized rate, or a net 6,900 jobs (Chart 3). Most sectors experienced positive job growth. The construction sector led expansion through an addition of 1,279 net jobs (8.0 percent). Also posting strong job growth were leisure and hospitality (1,555, 4.6 percent), government (1,780, 4.0 percent) and professional and business services (1,770, 3.6 percent). Industries that shed jobs during this period were information (-490), financial activities (-290) and trade, transportation and utilities (-385).

Real Estate

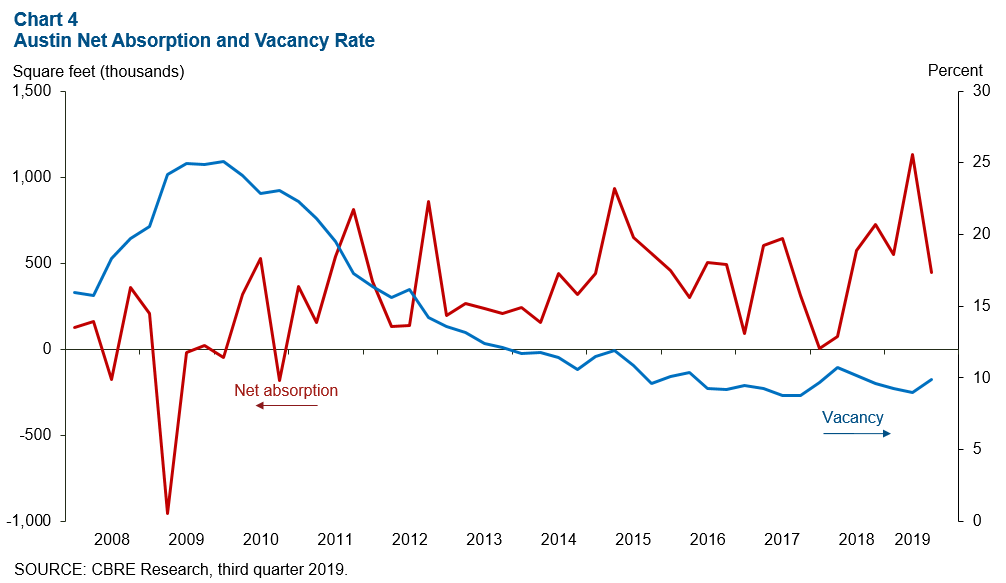

Office Space Demand Steady

Demand for office space remained strong in the third quarter (Chart 4). Net absorption was 446,637 square feet, putting the quarterly average this year at its highest since the data began in 2008. The vacancy rate remained the lowest of the large metros in the state but ticked up slightly to 9.9 percent. Average asking rents increased a slight 0.5 percent from the previous quarter but rose 9.6 percent year over year.

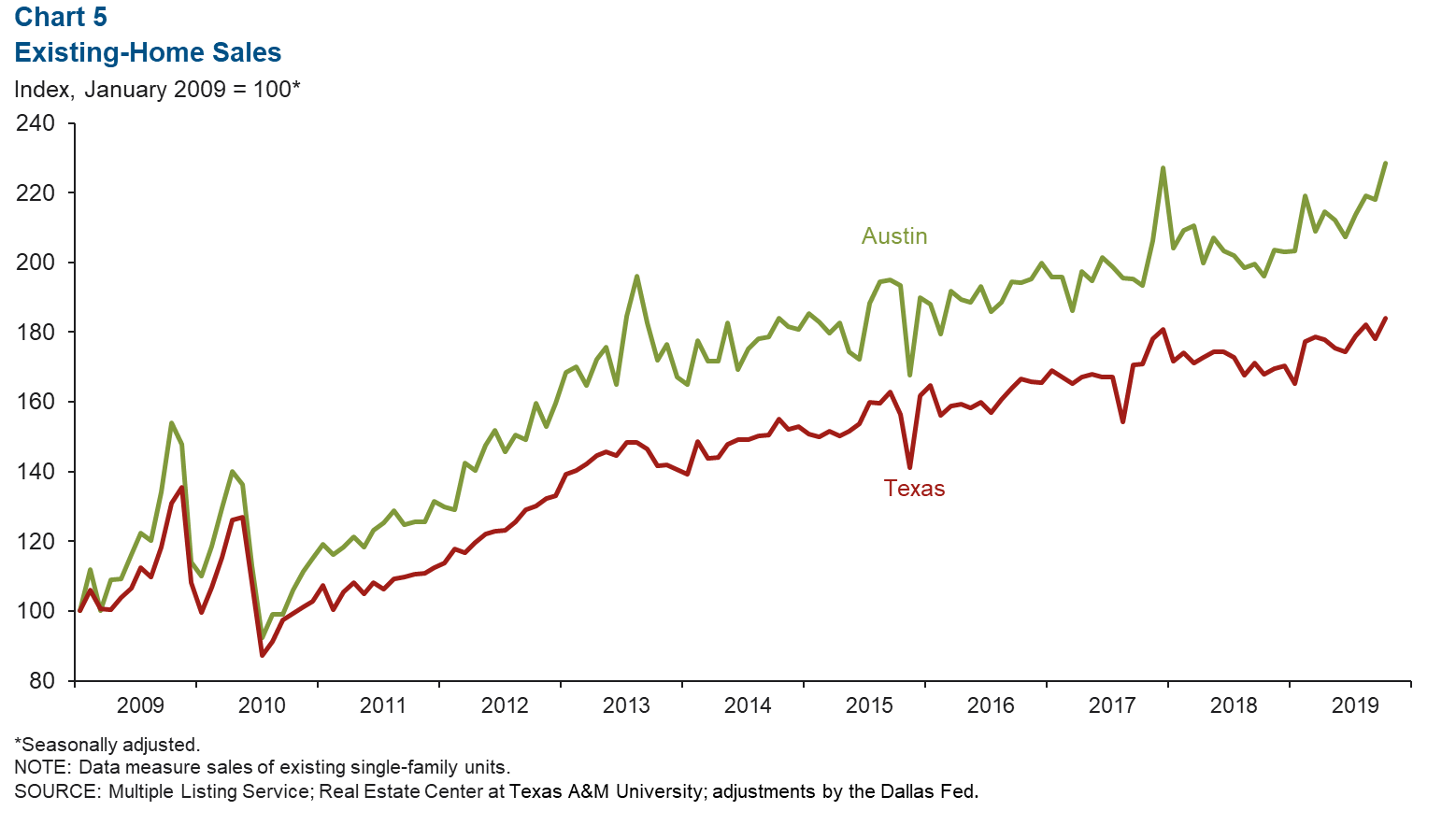

Metro Existing-Home Sales Activity Healthy

Austin existing-home sales increased 4.9 percent month over month, well above Texas’ 3.3 percent (Chart 5). This year through October, Austin home sales are up 5.7 percent compared with the same period in 2018, while Texas total home sales are up 3.1 percent during the same time frame. Austin’s home sales volume in October was 12.6 percent higher than the monthly average in 2018, while the state’s home sales volume was 7.3 percent higher.

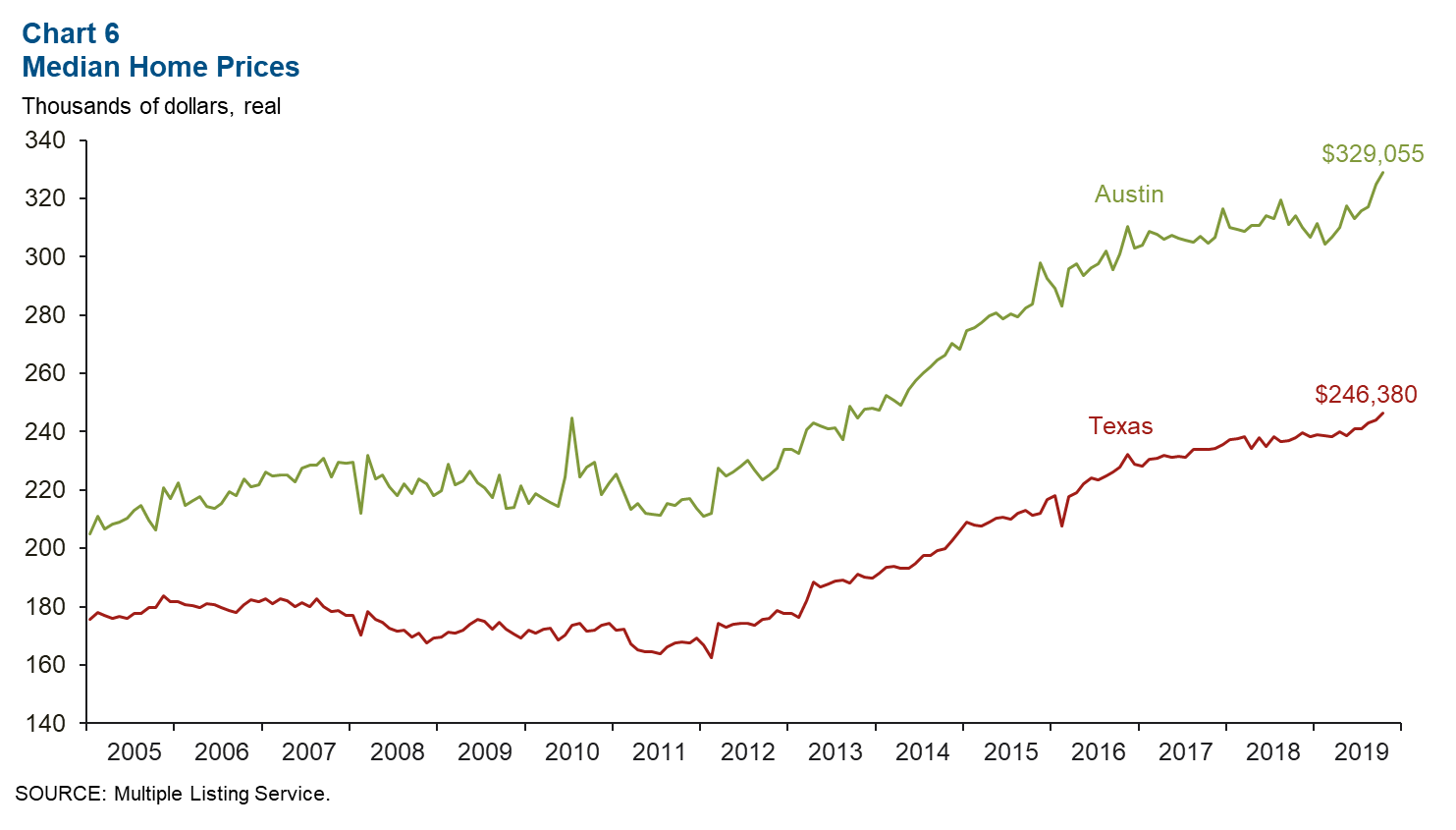

Metro Home Prices on the Rise

The median home price in Austin ticked up to $329,055 in October, up 4.8 percent year over year (Chart 6). The median home price for the state ticked up to $246,380, or a 3.5 percent increase year over year. This year through October, total housing permits (single family and multifamily), which lead building activity by approximately three months, swelled 37.3 percent in Austin. This surge is substantially higher than Texas’ 8.8 percent growth during the same period. Metro inventory stood at 2.2 months, far below the six months considered a balanced market.

NOTE: Data may not match previously published numbers due to revisions.

About Austin Economic Indicators

Questions can be addressed to Judy Teng at judy.teng@dal.frb.org. Austin Economic Indicators is released on the first Thursday of every month.