Agricultural Survey

Survey Highlights

Bankers responding to the first-quarter survey reported overall weaker conditions across most regions of the Eleventh District. Survey respondents noted that extreme dry conditions are putting a strain on agricultural production. In addition, they noted that the increase in commodity prices is not enough to offset the bigger increase in input costs. “Inflation has hit rural America. Everything is costing more, and selection is limited,” a survey participant said.

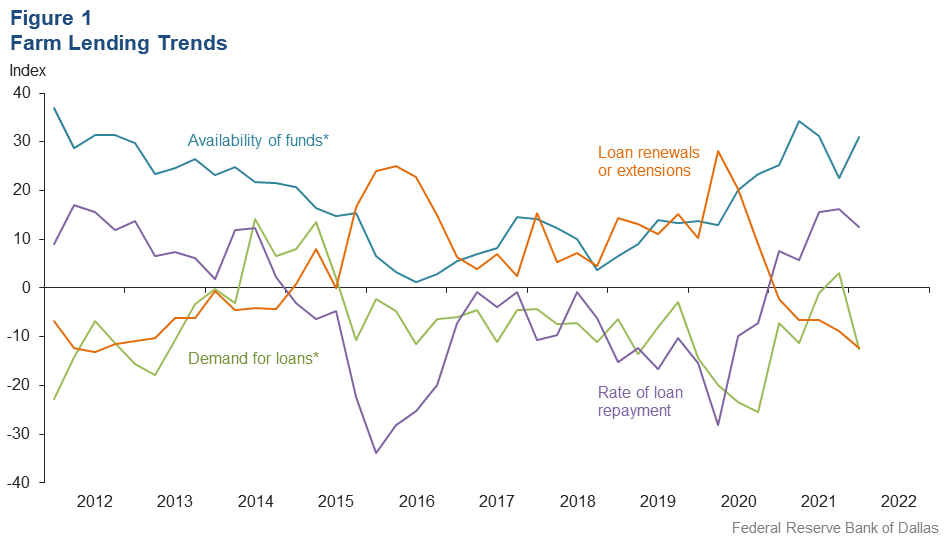

Demand for agricultural loans decreased in first quarter 2022, with the loan demand index returning to negative territory after posting its first positive reading since 2015 last quarter. Loan renewals or extensions fell for the fifth quarter in a row, while the rate of loan repayment continued to increase. Loan volume decreased for feeder cattle loans, dairy loans and crop storage loans compared with a year ago (Figure 1).

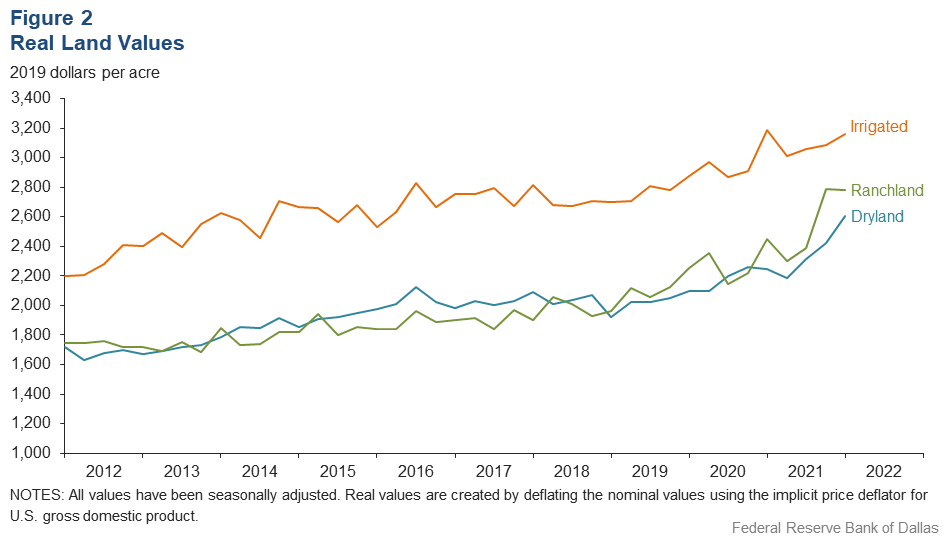

Irrigated cropland and dryland values rose this quarter, while ranchland values were steady (Figure 2). According to bankers who responded in both this quarter and first quarter 2021, cropland and ranchland values increased at least 10 percent year over year in Texas and northern Louisiana, with some segments seeing much higher increases (Table 1).

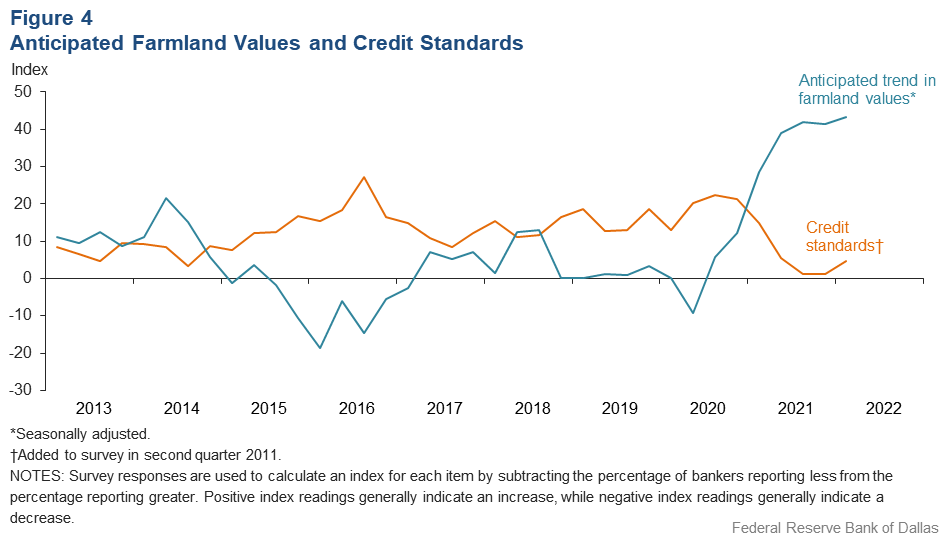

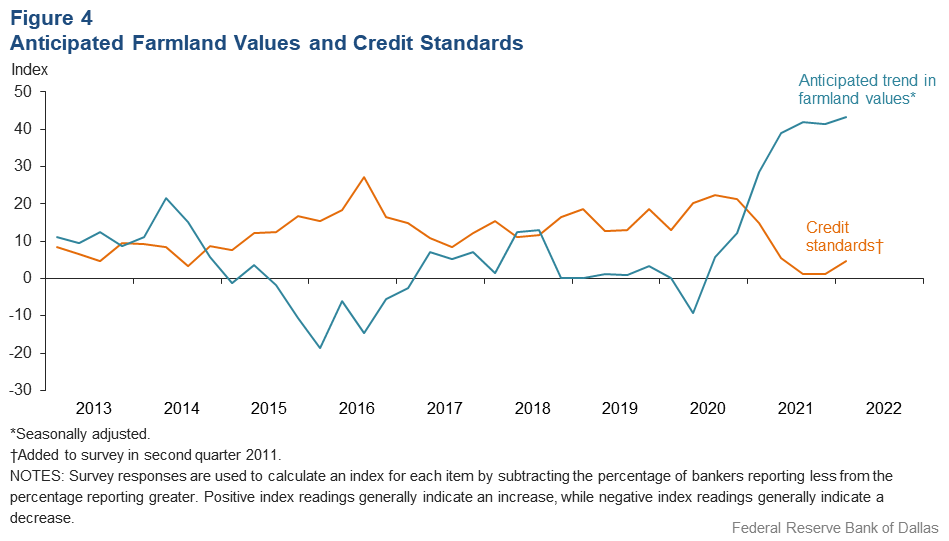

The anticipated trend in farmland values index pushed to a new high in the first quarter, suggesting respondents expect farmland values to continue increasing at a robust clip. The credit standards index ticked up and remained in positive territory. The continued positive value of the index indicates further tightening of standards on net (Figure 4).

Next release: June 29, 2022

Agricultural Survey is compiled from a survey of Eleventh District agricultural bankers, and data have been seasonally adjusted as necessary. Data were collected March 1–9, and 85 bankers responded to the survey.

Quarterly Comments

District bankers were asked for additional comments concerning agricultural land values and credit conditions. These comments have been edited for publication.

Region 1—Northern High Plains

- Very dry, winter wheat is in poor condition, the spring and summer crop outlook is not promising at this time, and there are skyrocketing input costs.

- There are extreme drought conditions. Cattle were off wheat pasture early, and they are lighter than normal. Input costs are much higher for farm operations.

- Inflation has hit rural America. Everything is costing more, and selection is limited. Gas is $3.19 per gallon today. Consumer confidence is at a low. We have had several large cash withdrawals recently from people concerned about cyberattacks. I will continue to trust that God will bless America.

Region 2—Southern High Plains

- This past crop year has been a Godsend for the majority of producers on the South Plains. There were good yields and good prices. However, for 2022, we are back to extremely dry conditions compared with early 2021. Producers have been advised to watch expenses closely due to the cost of inputs being up drastically. If insurance prices come out like we expect, most producers will wait until they have adequate rainfall to proceed with the crop.

- Thank goodness for last year. Agriculture really needed it. All of our line-of-credit loans were able to be paid in full. Drought conditions are hurting us in West Texas, and we could sure use a slow, soaking rain soon.

- Dry conditions continue to be a primary concern for the coming crop year. Insurance pricing helps to mitigate risk but at a higher cost to producers. Government program assistance (agriculture risk coverage and price loss coverage) is not anticipated outside of ad hoc disaster payments. Increased input cost and scarcity created great uncertainty and inherently higher risk. Demand for commodities remains high, and shipments continue despite historic pricing.

Region 3—Northern Low Plains

- Extremely dry conditions and high input costs outweigh high commodity prices. Cattle liquidation has started with stocker cattle going to market sooner than anticipated due to drought. Dryland wheat crop is nonexistent. Producers are concerned about availability and price of chemicals, fertilizer and parts for this crop season. The increase in commodity prices is not enough to offset the bigger increase in input cost.

- We are experiencing the driest conditions seen in my lifetime. Three fourths of the wheat planted in the county has not emerged or is just now emerging. No cattle are grazing for the first time in years. This county is 95 percent wheat/cattle. The upside is price support from revenue protection through crop insurance.

Region 4—Southern Low Plains

- Rain is needed. Commodity prices are good, but costs have increased significantly.

Region 6—North Central Texas

- Input cost for 2022 is much higher than last year. We need rain! Diesel is going through the roof; we need to start drilling and become energy independent again.

- Smaller tracts of rural land (10–25 acres) are selling for approximately $15,000. These tracts appear to be primarily being purchased for home sites not considered to be agricultural properties for ranching.

Region 7—East Texas

- Dry conditions as well as cold have row crop farmers behind in planting. As expected, input costs have risen but are hopefully offset by good projected commodity prices. Pastures need rain; January/February freezes severely damaged small grain fields. Recent high real estate sales in the area are getting a lot of attention.

- Demand remains strong for all types of agriculture loans.

Region 8—Central Texas

- Land values continue to climb. The biggest factor at this time is tax-free exchanges; lots of people in the I-35 corridor are selling long-held properties and are doing exchanges for rural land. Lots of people are still getting out of the big cities and moving to rural areas. We missed most of the rains the past few months, and we are beginning to feel the drought coming back. Lots of hay were feed the past 30 days, and with fertilizer prices still at all-time highs, hay could get more expensive as the months drag on. Oil and gas drilling is still in the area, with oilfield traffic picking up.

Region 9—Coastal Texas

- It would help if banks could compete with the nontaxable funding sources—for instance, the farm credit system. They have a tax advantage over banks in funding loans as they do not pay income tax. We would hope that Congress would also extend the same treatment to community banks.

Region 11—Trans-Pecos and Edwards Plateau

- Agricultural land values are being supported a great deal by recreational-use buyers and some investors, with true agricultural operators being less in numbers. Pastures are very dry, and rainfall is desperately needed. While some old grass remains, its nutritional value is questionable. Supplemental feeding is critical and increasingly more costly due to increased feed costs. The one positive is that the market values on livestock—sheep, goats and to a lesser extent cattle—are exceptionally good and seem relatively stable currently.

Historical Data

Historical data can be downloaded dating back to first quarter 2000.

Figures

Farm Lending Trends

What changes occurred in non-real-estate farm loans at your bank in the past three months compared with a year earlier?

| Index | Percent reporting, Q1 | ||||

| 2021:Q4 | 2022:Q1 | Greater | Same | Less | |

Demand for loans* | 3.1 | –12.6 | 9.7 | 68.0 | 22.3 |

Availability of funds* | 22.6 | 31.0 | 34.0 | 63.0 | 3.0 |

Rate of loan repayment | 16.3 | 12.5 | 20.0 | 72.5 | 7.5 |

Loan renewals or extensions | –8.8 | –12.4 | 3.7 | 80.3 | 16.1 |

What changes occurred in the volume of farm loans made by your bank in the past three months compared with a year earlier?

| Index | Percent reporting, Q1 | ||||

| 2021:Q4 | 2022:Q1 | Greater | Same | Less | |

Non–real–estate farm loans | 0.0 | –2.5 | 13.6 | 70.4 | 16.1 |

Feeder cattle loans* | –15.4 | –22.1 | 3.0 | 71.9 | 25.1 |

Dairy loans* | –11.6 | –8.7 | 5.5 | 80.3 | 14.2 |

Crop storage loans* | –6.5 | –9.4 | 8.4 | 73.8 | 17.8 |

Operating loans | 2.5 | 2.6 | 15.4 | 71.8 | 12.8 |

Farm machinery loans* | 0.4 | –9.2 | 12.0 | 66.8 | 21.2 |

Farm real estate loans* | 12.2 | 3.7 | 18.0 | 67.7 | 14.3 |

| *Seasonally adjusted. NOTES: Survey responses are used to calculate an index for each item by subtracting the percentage of bankers reporting less from the percentage reporting greater. Positive index readings generally indicate an increase, while negative index readings generally indicate a decrease. |

|||||

Real Land Values

Real Cash Rents

Anticipated Farmland Values and Credit Standards

What trend in farmland values do you expect in your area in the next three months?

| Index | Percent reporting, Q1 | ||||

| 2021:Q4 | 2022:Q1 | Up | Same | Down | |

| Anticipated trend in farmland values* | 41.3 | 43.3 | 45.3 | 52.7 | 2.0 |

What change occurred in credit standards for agricultural loans at your bank in the past three months compared with a year earlier?†

| 2021:Q4 | 2022:Q1 | Up | Same | Down | |

| Credit standards | 1.2 | 4.8 | 8.3 | 88.1 | 3.6 |

Tables

Rural Real Estate Values—First Quarter 2022

| Banks1 | Average value2 | Percent change in value from previous year3 | ||

Cropland–Dryland | ||||

District* | 63 | 2,697 | 23.1 | |

Texas* | 57 | 2,720 | 23.0 | |

1 | Northern High Plains | 10 | 1,060 | 10.5 |

2 | Southern High Plains | 8 | 1,075 | 20.3 |

3 | Northern Low Plains* | 3 | 997 | 8.3 |

4 | Southern Low Plains* | 4 | 1,962 | 68.4 |

5 | Cross Timbers | n.a. | n.a. | n.a. |

6 | North Central Texas | 6 | 4,667 | 27.3 |

7 | East Texas* | 4 | 3,547 | 14.8 |

8 | Central Texas | 9 | 6,944 | 32.3 |

9 | Coastal Texas | 5 | 2,440 | 6.1 |

10 | South Texas | n.a. | n.a. | n.a. |

11 | Trans–Pecos and Edwards Plateau | 5 | 3,550 | 18.4 |

12 | Southern New Mexico | n.a. | n.a. | n.a. |

13 | Northern Louisiana | 4 | 4,050 | 31.7 |

Cropland–Irrigated | ||||

District* | 50 | 3,270 | 9.5 | |

Texas* | 42 | 2,616 | 10.2 | |

1 | Northern High Plains | 10 | 2,295 | 6.5 |

2 | Southern High Plains | 8 | 2,050 | 12.7 |

3 | Northern Low Plains* | n.a. | n.a. | n.a. |

4 | Southern Low Plains | 3 | 3,233 | 51.6 |

5 | Cross Timbers | n.a. | n.a. | n.a. |

6 | North Central Texas | 3 | 5,500 | 32.0 |

7 | East Texas | 3 | 4,400 | 14.8 |

8 | Central Texas | 4 | 5,100 | 12.7 |

9 | Coastal Texas | 3 | 2,233 | 8.0 |

10 | South Texas | n.a. | n.a. | n.a. |

11 | Trans–Pecos and Edwards Plateau | 4 | 4,325 | 37.1 |

12 | Southern New Mexico | 4 | 7,250 | 0.7 |

13 | Northern Louisiana | 4 | 5,700 | 21.3 |

Ranchland | ||||

District* | 69 | 2,879 | 19.7 | |

Texas* | 62 | 3,459 | 20.4 | |

1 | Northern High Plains | 10 | 888 | 16.4 |

2 | Southern High Plains | 6 | 925 | 4.9 |

3 | Northern Low Plains | 3 | 967 | 11.1 |

4 | Southern Low Plains* | 4 | 2,347 | 97.8 |

5 | Cross Timbers | 3 | 3,300 | 41.4 |

6 | North Central Texas | 6 | 5,167 | 30.8 |

7 | East Texas | 8 | 3,806 | 23.4 |

8 | Central Texas | 9 | 9,544 | 26.1 |

9 | Coastal Texas | 5 | 2,820 | 8.8 |

10 | South Texas | n.a. | n.a. | n.a. |

11 | Trans–Pecos and Edwards Plateau | 6 | 3,658 | 20.4 |

12 | Southern New Mexico | 3 | 367 | –2.1 |

13 | Northern Louisiana | 4 | 2,700 | 16.9 |

| *Seasonally adjusted. 1 Number of banks reporting land values. 2 Prices are dollars per acre, not adjusted for inflation. 3 Not adjusted for inflation and calculated using responses only from those banks reporting in both the past and current quarter. n.a.—Not published due to insufficient responses but included in totals for Texas and district. |

||||

Interest Rates by Loan Type—First Quarter 2022

| Feeder cattle | Other farm operating | Intermediate term | Long-term farm real estate | Fixed (average rate, percent) |

2021:Q1 | 5.77 | 5.76 | 5.55 | 5.13 |

2021:Q2 | 5.65 | 5.67 | 5.53 | 5.20 |

2021:Q3 | 5.55 | 5.61 | 5.45 | 5.15 |

2021:Q4 | 5.59 | 5.61 | 5.48 | 5.19 |

2022:Q1 | 5.69 | 5.62 | 5.54 | 5.30 | Variable (average rate, percent) |

2021:Q1 | 5.32 | 5.33 | 5.22 | 4.95 |

2021:Q2 | 5.33 | 5.31 | 5.24 | 5.00 |

2021:Q3 | 5.23 | 5.31 | 5.23 | 4.93 |

2021:Q4 | 5.40 | 5.38 | 5.33 | 4.96 |

2022:Q1 | 5.42 | 5.33 | 5.25 | 4.93 |

For More Information

Questions regarding the Agricultural Survey can be addressed to Jesus Cañas at Jesus.Canas@dal.frb.org.