Banking Conditions Survey

Loan Demand Declines amid Rising Interest Rates

For this month’s survey, Eleventh District business executives were asked supplemental questions on deposits. Read the special questions results.

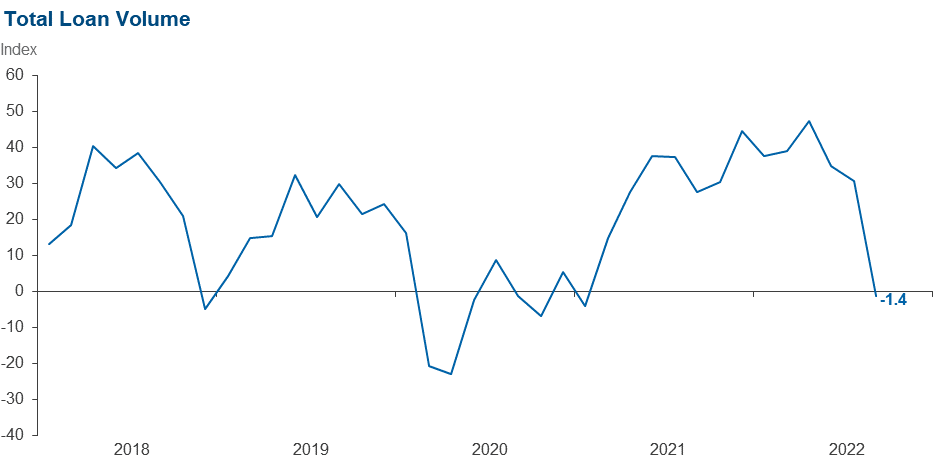

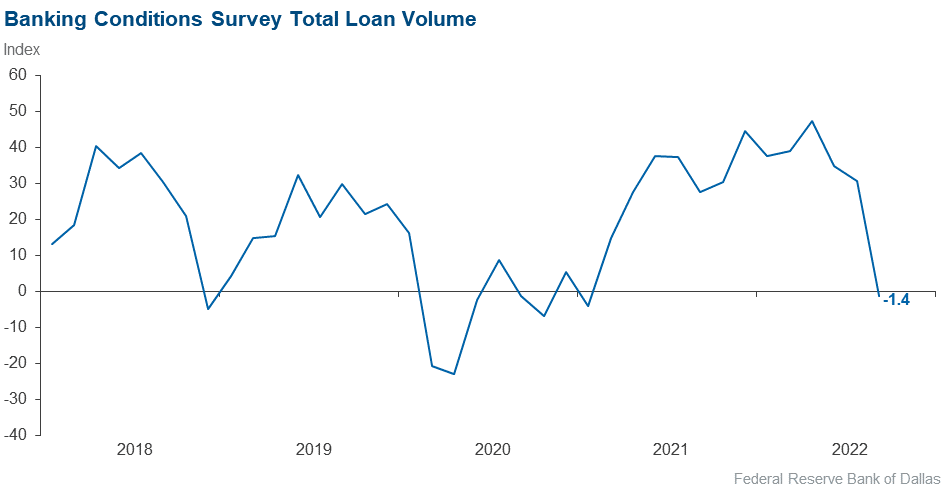

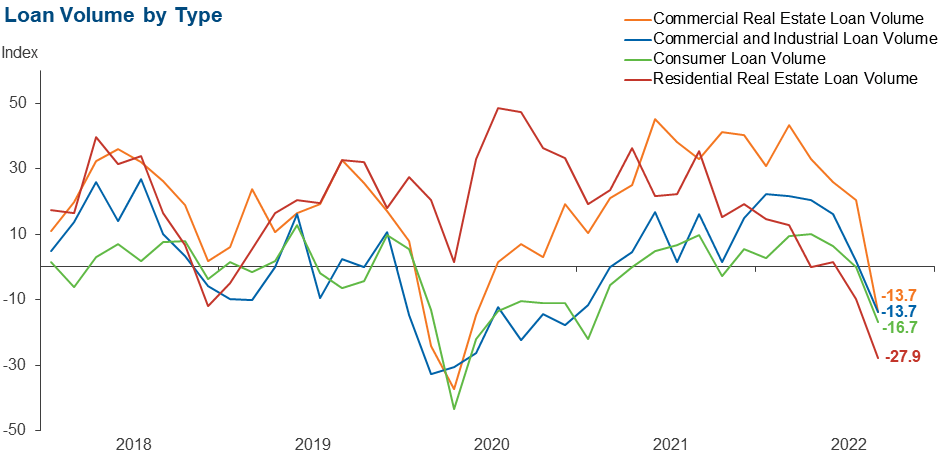

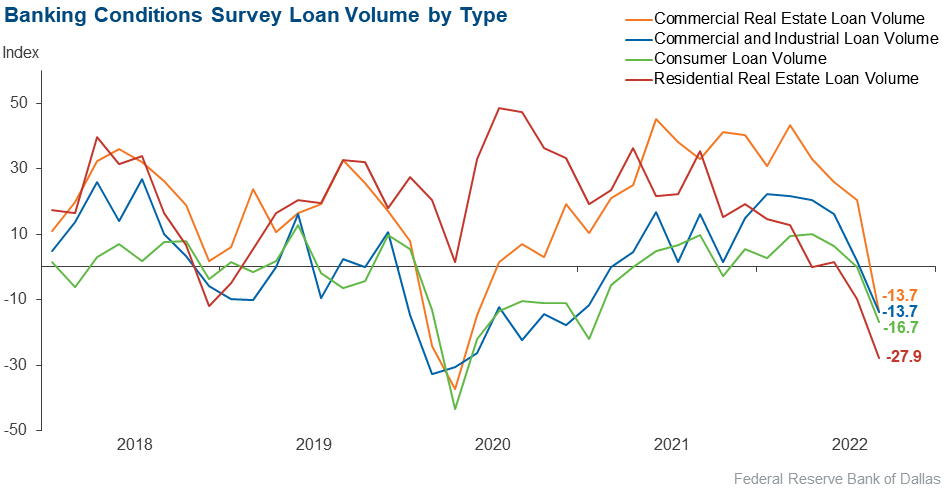

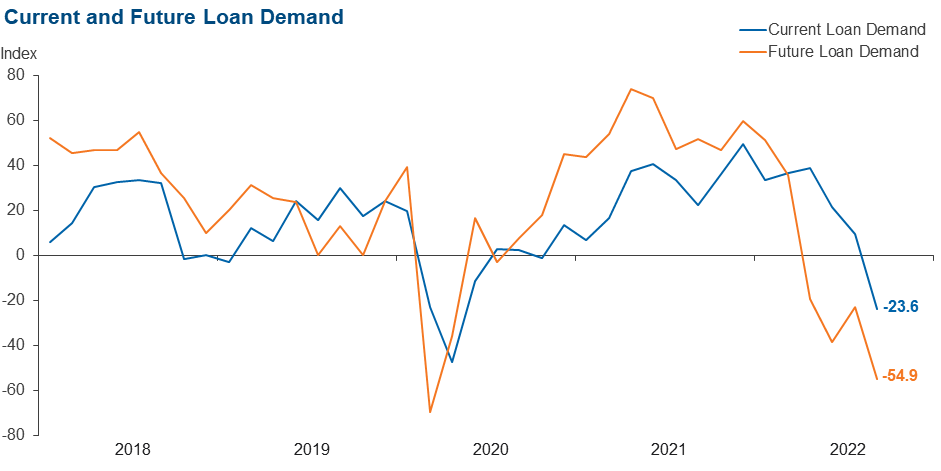

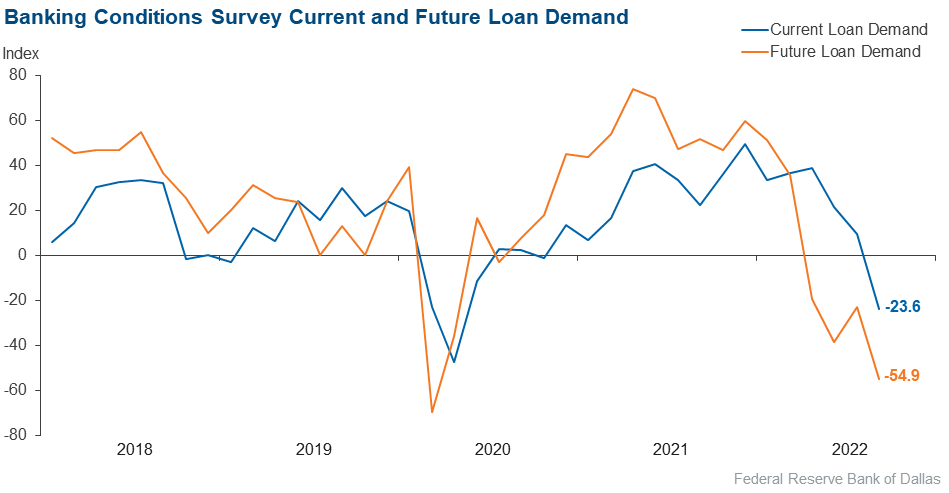

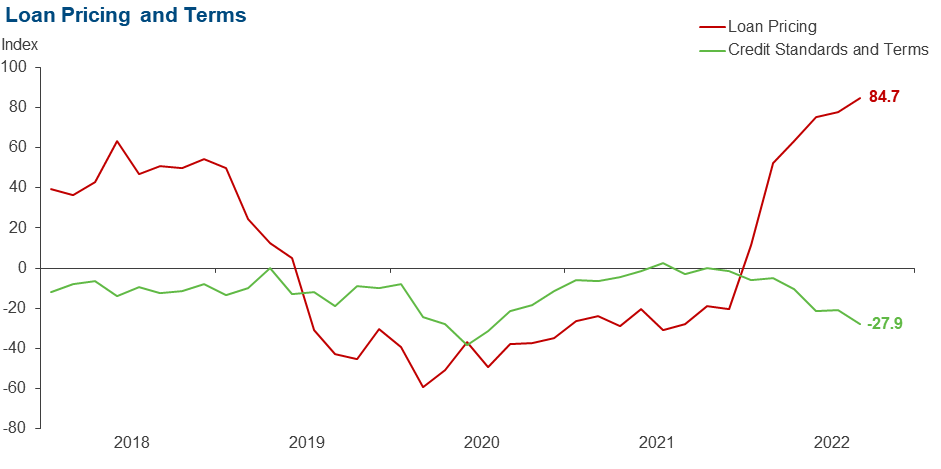

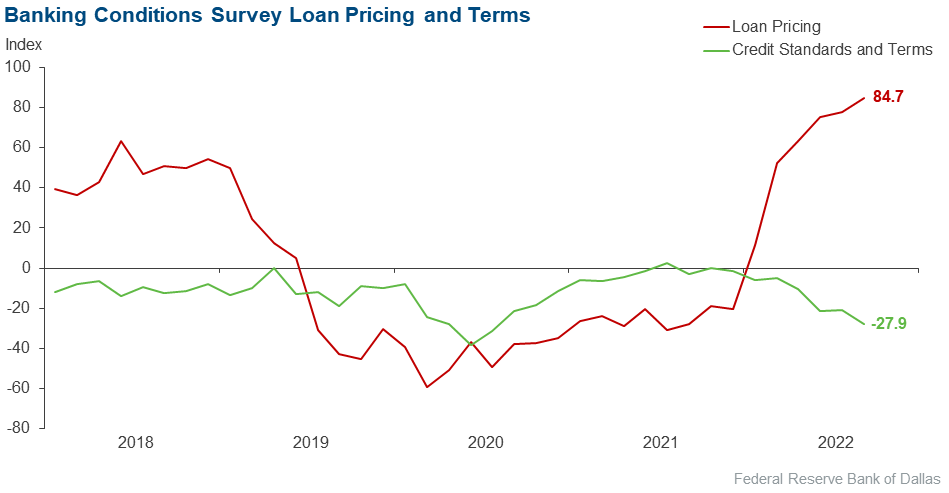

Loan demand declined for the first time in nearly two years, and overall loan volumes decreased over the past six weeks. Volume declines were seen in all loan categories, but the steepest came in residential real estate lending. Loan nonperformance varied by category but was largely unchanged overall. Loan pricing continued to rise notably, with 84.7 percent of contacts reporting an increase—the largest share since the survey began in 2017. Credit standards and terms tightened further. Looking six months ahead, contacts expressed greater pessimism than in the prior period and expect loan demand and general business activity to decrease and loan delinquency to increase.

Next release: November 14, 2022

Data were collected September 20–28, and 72 financial institutions responded to the survey. The Federal Reserve Bank of Dallas conducts the Banking Conditions Survey twice each quarter to obtain a timely assessment of activity at banks and credit unions headquartered in the Eleventh Federal Reserve District. CEOs or senior loan officers of financial institutions report on how conditions have changed for indicators such as loan volume, nonperforming loans and loan pricing. Respondents are also asked to report on their banking outlook and their evaluation of general business activity.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease (or tightening) from the percentage reporting an increase (or easing). When the share of respondents reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior reporting period. If the share of respondents reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior reporting period. An index will be zero when the number of respondents reporting an increase is equal to the number reporting a decrease.

Results Summary

Historical data are available from March 2017.

| Total Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –1.4 | 30.7 | 31.9 | 34.7 | 33.3 |

Loan demand | –23.6 | 9.5 | 22.2 | 31.9 | 45.8 |

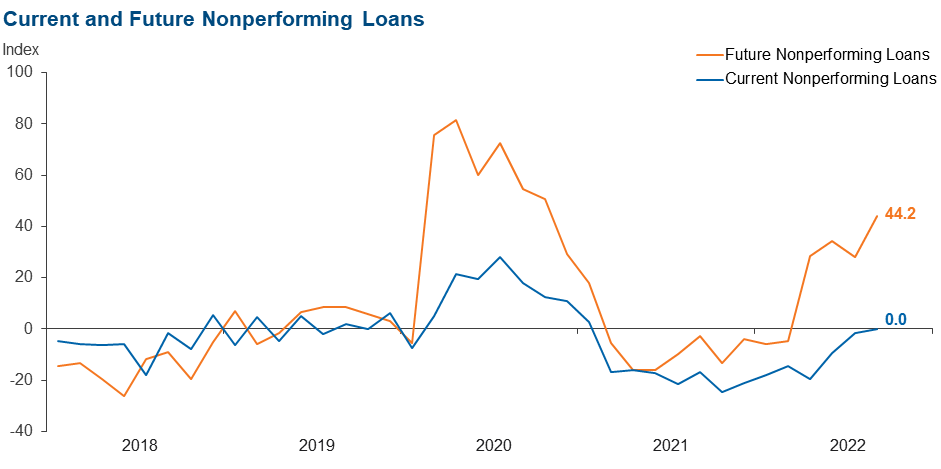

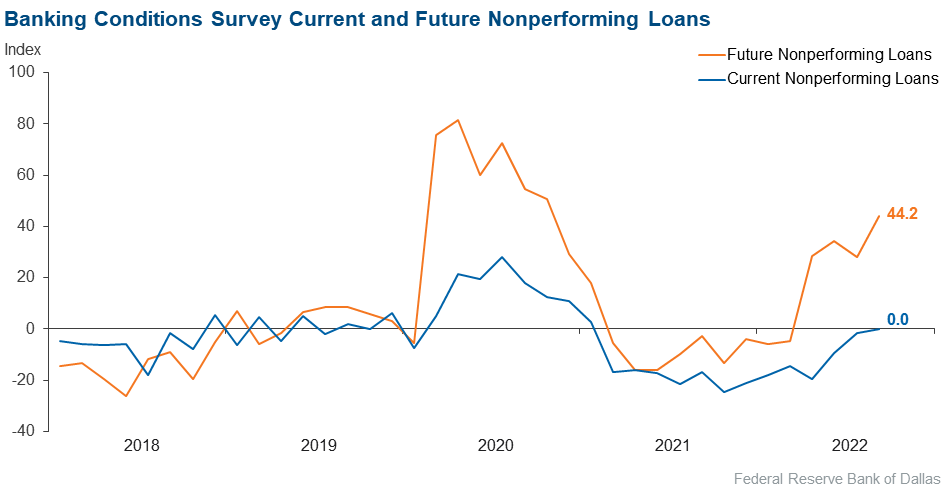

Nonperforming loans | 0.0 | –1.5 | 11.1 | 77.8 | 11.1 |

Loan pricing | 84.7 | 77.8 | 84.7 | 15.3 | 0.0 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –27.9 | –20.6 | 0.0 | 72.1 | 27.9 |

| Commercial and Industrial Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –13.7 | 1.7 | 13.6 | 59.1 | 27.3 |

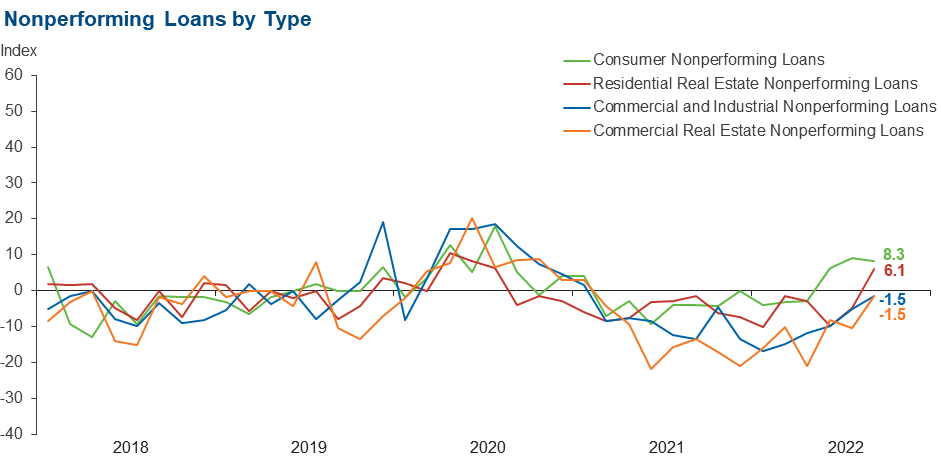

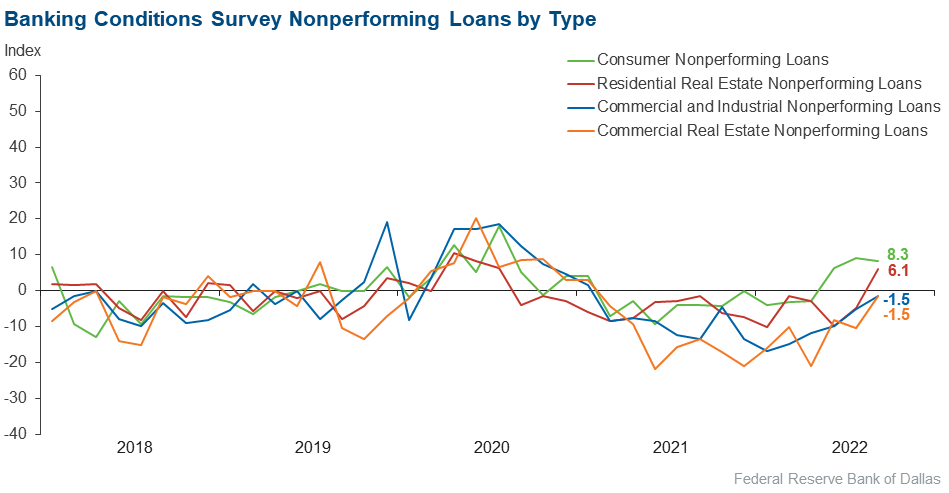

Nonperforming loans | –1.5 | –5.0 | 3.0 | 92.4 | 4.5 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –24.2 | –15.0 | 0.0 | 75.8 | 24.2 |

| Commercial Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –13.7 | 20.4 | 24.2 | 37.9 | 37.9 |

Nonperforming loans | –1.5 | –10.4 | 3.0 | 92.4 | 4.5 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –29.2 | –20.7 | 0.0 | 70.8 | 29.2 |

| Residential Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –27.9 | –9.9 | 16.2 | 39.7 | 44.1 |

Nonperforming loans | 6.1 | –4.9 | 9.1 | 87.9 | 3.0 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –11.7 | –11.5 | 1.5 | 85.3 | 13.2 |

| Consumer Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –16.7 | 0.0 | 13.9 | 55.6 | 30.6 |

Nonperforming loans | 8.3 | 9.2 | 13.9 | 80.6 | 5.6 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –11.4 | –6.2 | 0.0 | 88.6 | 11.4 |

| Banking Outlook: What is your expectation for the following items six months from now? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Total loan demand | –54.9 | –23.1 | 16.9 | 11.3 | 71.8 |

Nonperforming loans | 44.2 | 28.1 | 47.1 | 50.0 | 2.9 |

| General Business Activity: What is your evaluation of the level of activity? | |||||

| Indicator | Current Index | Previous Index | % Reporting Better | % Reporting No Change | % Reporting Worse |

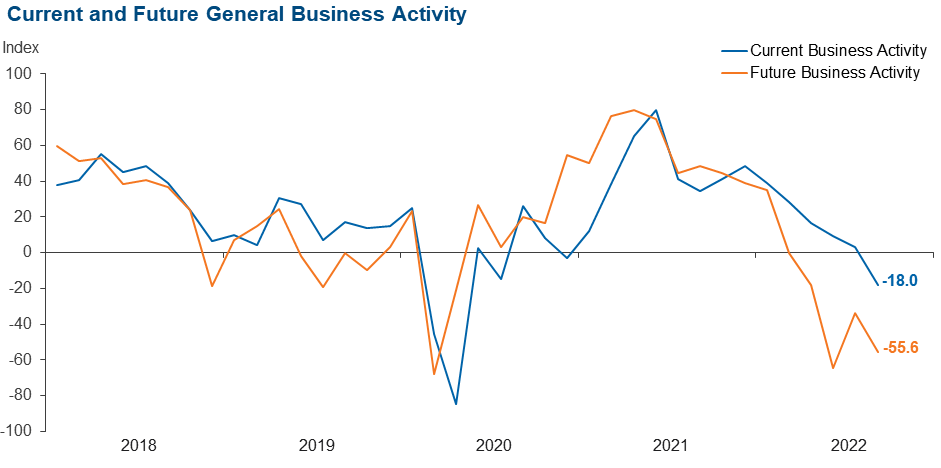

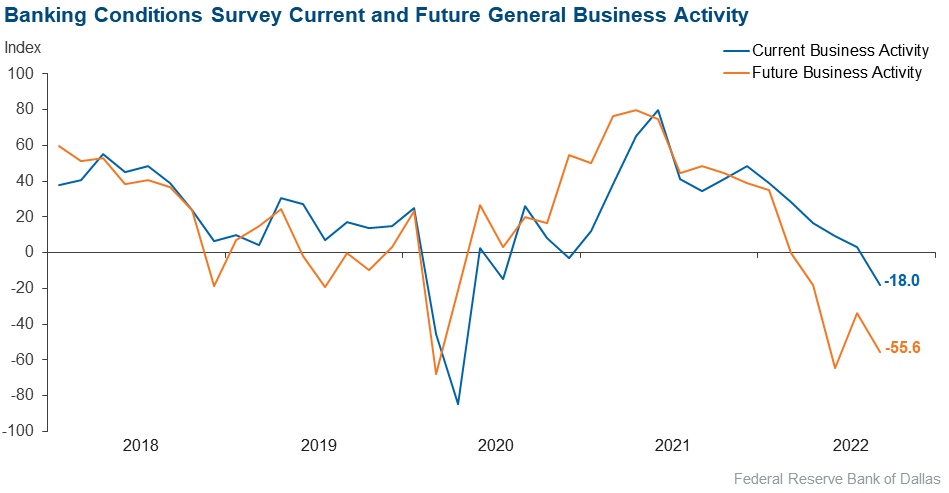

Over the past six weeks | –18.0 | 3.1 | 13.9 | 54.2 | 31.9 |

Six months from now | –55.6 | –33.8 | 12.5 | 19.4 | 68.1 |

| General Business Activity: What is your evaluation of the level of activity? | |||||

| Indicator | Current Index | Previous Index | % Reporting Better | % Reporting No Change | % Reporting Worse |

Over the past six weeks | 3.1 | 9.1 | 27.7 | 47.7 | 24.6 |

Six months from now | –33.8 | –64.6 | 15.4 | 35.4 | 49.2 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Comments from Survey Respondents

Respondents were given an opportunity to comment on any issues that may be affecting their business.

These comments are from respondents’ completed surveys and have been edited for publication.

- Fed tightening should result in an economic slowdown, leading to increases in nonperforming loans.

- Uncertainty over interest rates, a possible increase in the cost of funds and the competition/pricing for talent [are issues of concern].

- We have had an increase in farm and ranchland real estate loans.

- The Fed going too far with interest rate hikes and bringing the economy to a grinding halt [is an issue of concern].

- There is an imminent recession ahead. Inflation will likely run longer and unemployment higher than anticipated. And on top of all that, we have an administration allowing regulators to subject banks to undue risk―i.e., person-to-person fraud liability―and overbearing regulations. It sounds like the perfect storm for a financial disaster.

- We are beginning to see signs of the economic environment impacting consumers. A continued need for unsecured credit, decreasing demand for real estate loans, use of deposits built up during the pandemic, larger depositors rate shopping, and an uptick in account fraud and early-stage delinquency.

- Inflation [is an issue of concern]. Higher interest rates are expected to slow down loan growth. [Other issues of concern are] the outcome of the November elections, the Russian–Ukrainian war, consumer ability to repay loans, and rising gas and energy prices as temperatures fall.

- I am worried that the rising interest rates will cause our debt-coverage ratios to continue to decline on our commercial loans as we adjust the size of loan payments to keep loans on their original amortizations. This will start causing loans to go past due. I hope it doesn’t happen, but it is a risk our bank is concerned about.

- Our primary concerns are inflation, the increased risk of an economic downturn and an increased government regulatory burden.

- Rapid interest rate increases are devastating to our members. They can’t afford vehicles to get to work, can’t afford to borrow money to fix the vehicles they have [and are finding it] difficult to buy food, clothing and gas. The Fed appears clueless, reacting instead of acting.

- Inflation, the supply chain and labor shortages [are issues of concern].

- We have seen the supply-chain issues and higher costs associated with construction projects start to impact the cash flow of construction contractors.

Historical Data

Historical data can be downloaded dating back to March 2017. For the definitions, see data definitions.

NOTE: The following series were discontinued in May 2020: volume of core deposits, cost of funds, non-interest income and net interest margin.

Questions regarding the Banking Conditions Survey can be addressed to Emily Kerr at emily.kerr@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Banking Conditions Survey is released on the web.