Banking Conditions Survey

For this survey, Eleventh District banking executives were asked supplemental questions on deposits, credit standards, commercial real estate lending and interest rates. Read the special questions results.

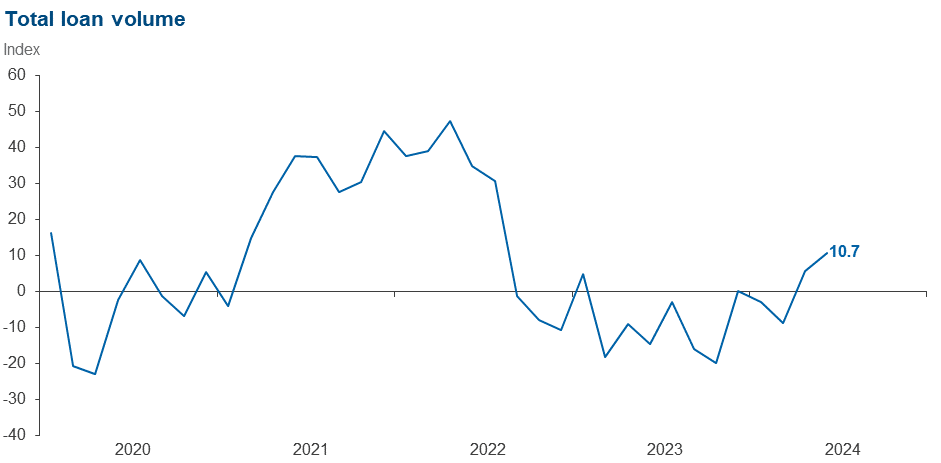

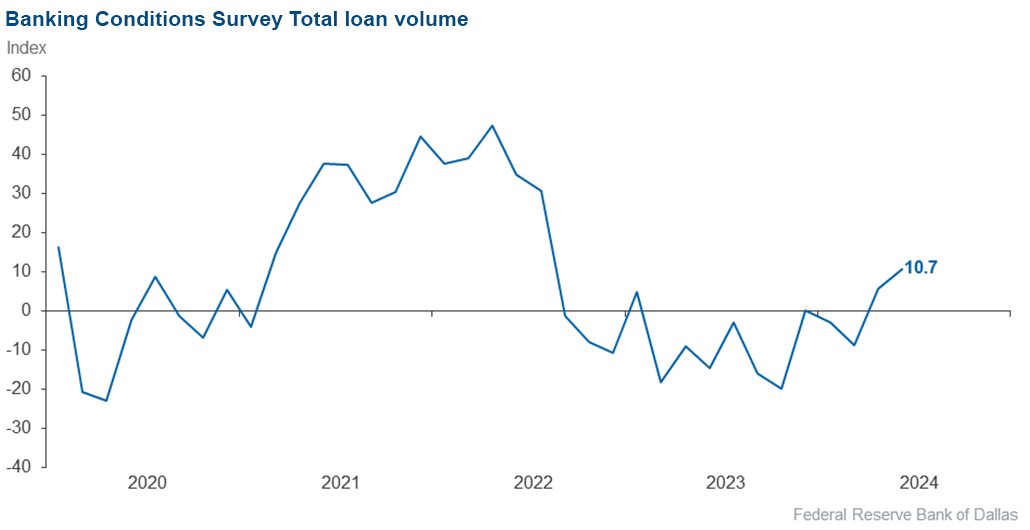

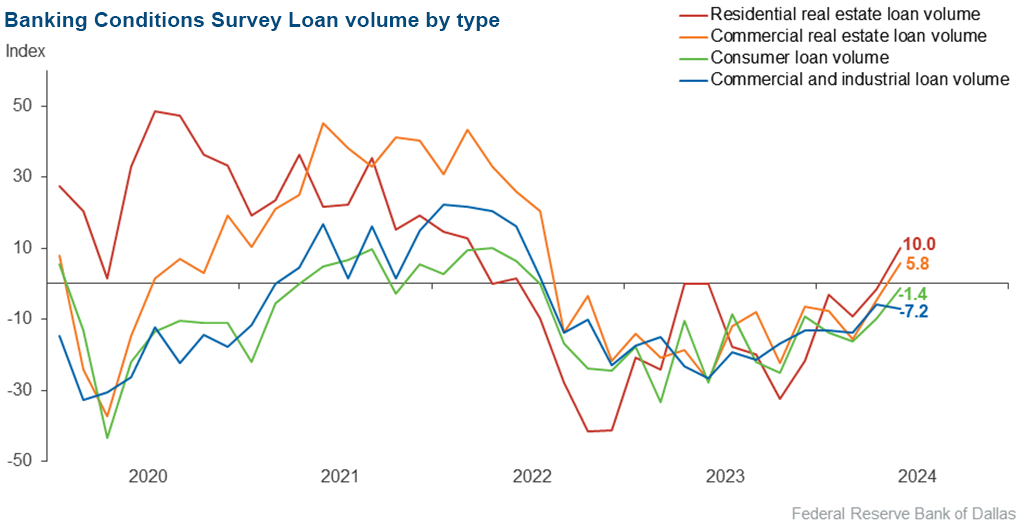

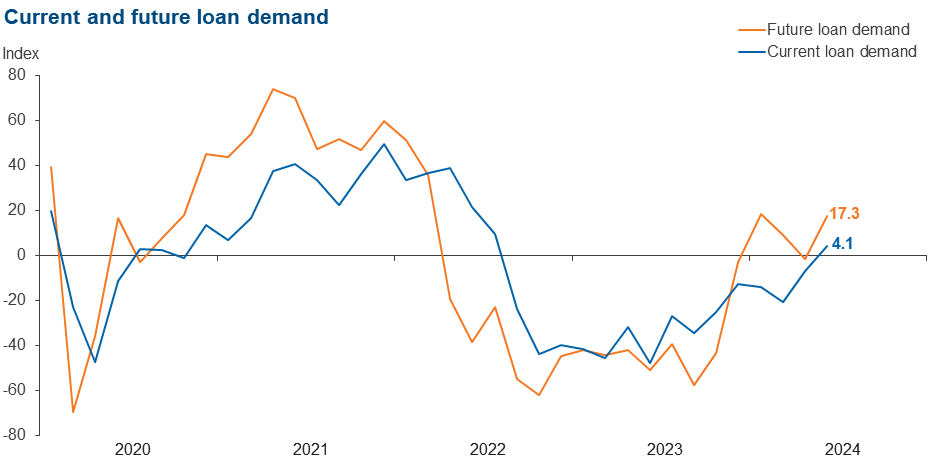

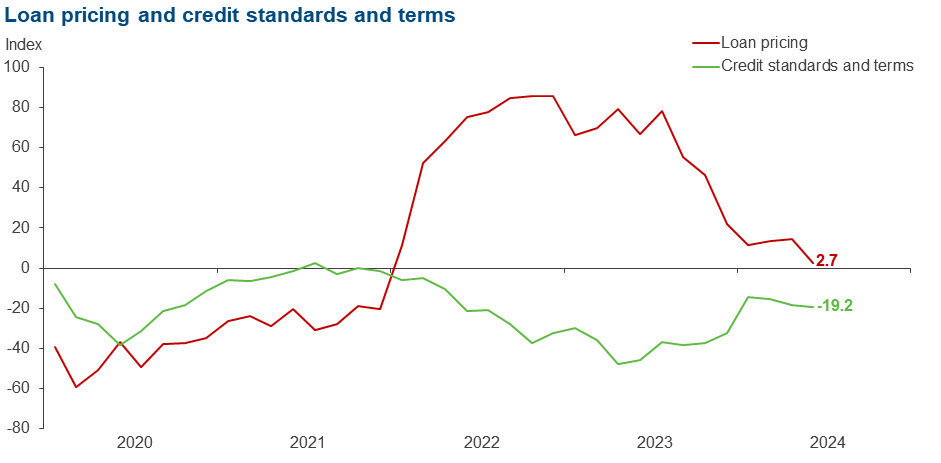

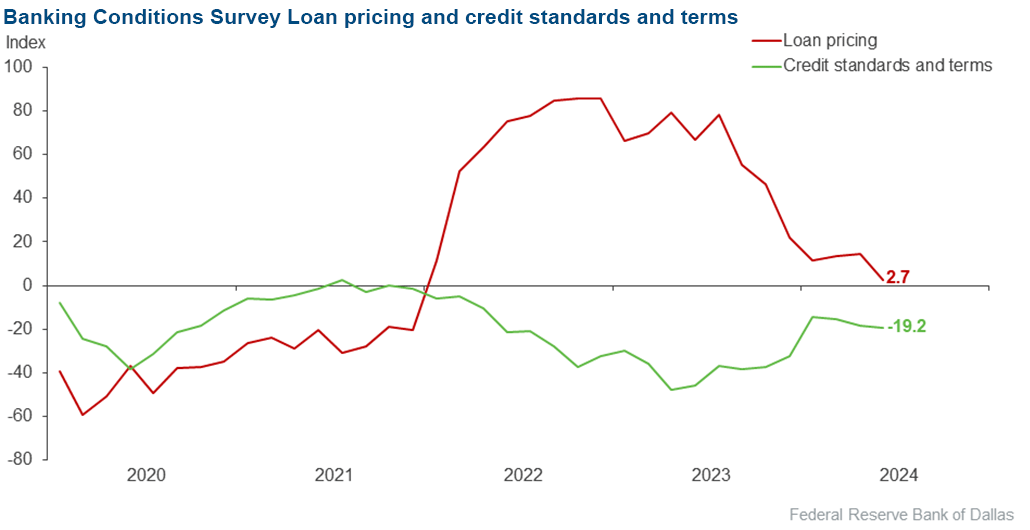

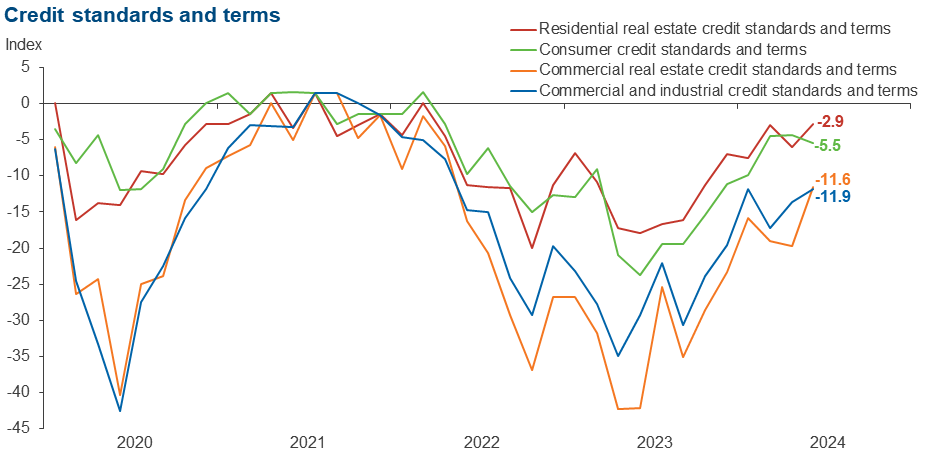

Loan volumes grew at a faster pace in June as loan demand increased despite credit standards continuing to tighten. Credit tightening decelerated for all loan types except for consumer loans. Loan price increases moderated. Loan nonperformance continued to rise, particularly for consumer and commercial and industrial loans. Bankers’ outlooks remain mixed: they expect an increase in loan demand six months from now, but a deterioration in loan performance and business activity, although the expectations of a decline have moderated toward stabilization.

Next release: August 19, 2024

Data were collected June 18–26, and 75 financial institutions responded to the survey. The Federal Reserve Bank of Dallas conducts the Banking Conditions Survey twice each quarter to obtain a timely assessment of activity at banks and credit unions headquartered in the Eleventh Federal Reserve District. CEOs or senior loan officers of financial institutions report on how conditions have changed for indicators such as loan volume, nonperforming loans and loan pricing. Respondents are also asked to report on their banking outlook and their evaluation of general business activity.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease (or tightening) from the percentage reporting an increase (or easing). When the share of respondents reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior reporting period. If the share of respondents reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior reporting period. An index will be zero when the number of respondents reporting an increase is equal to the number reporting a decrease.

Results Summary

Historical data are available from March 2017.

| Total Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 10.7 | 5.6 | 40.0 | 30.7 | 29.3 |

Loan demand | 4.1 | –7.1 | 31.1 | 41.9 | 27.0 |

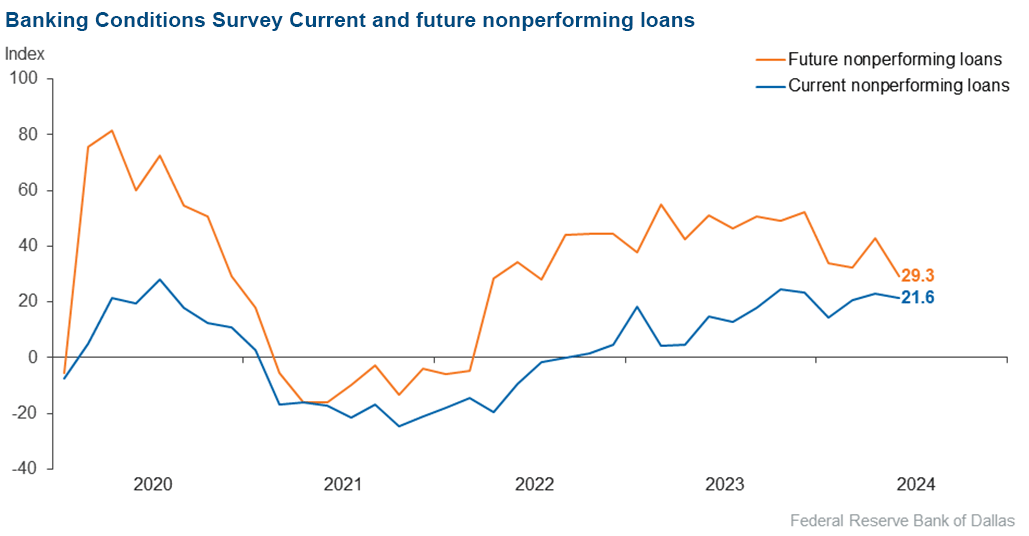

Nonperforming loans | 21.6 | 22.9 | 31.1 | 59.5 | 9.5 |

Loan pricing | 2.7 | 14.5 | 8.1 | 86.5 | 5.4 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –19.2 | –18.2 | 0.0 | 80.8 | 19.2 |

| Commercial and Industrial Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –7.2 | –5.9 | 15.7 | 61.4 | 22.9 |

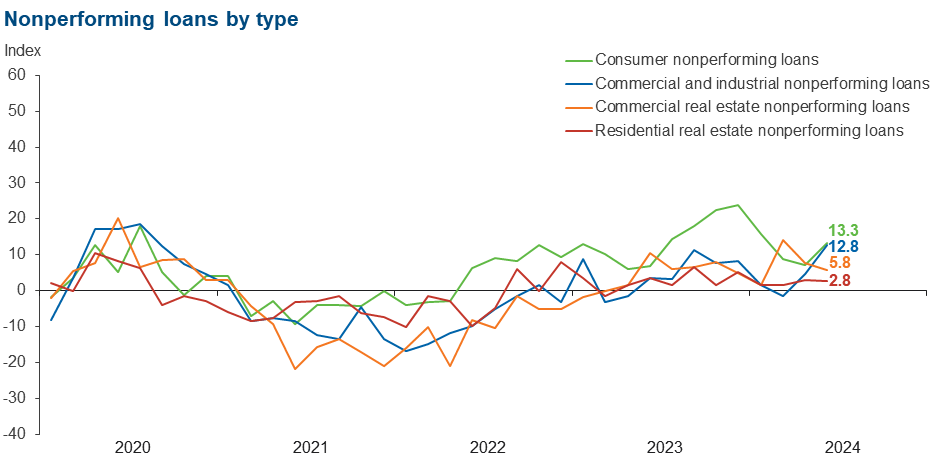

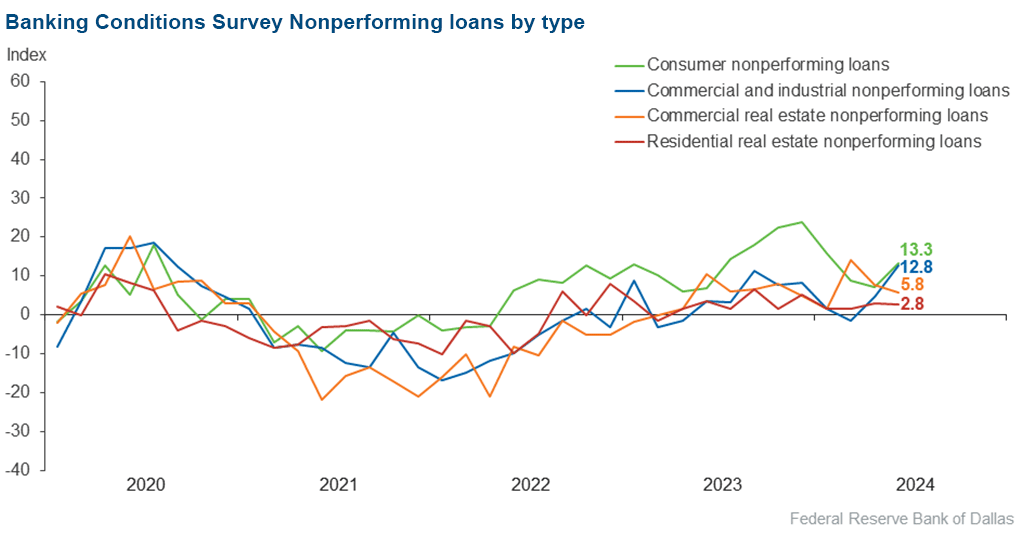

Nonperforming loans | 12.8 | 4.6 | 15.7 | 81.4 | 2.9 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

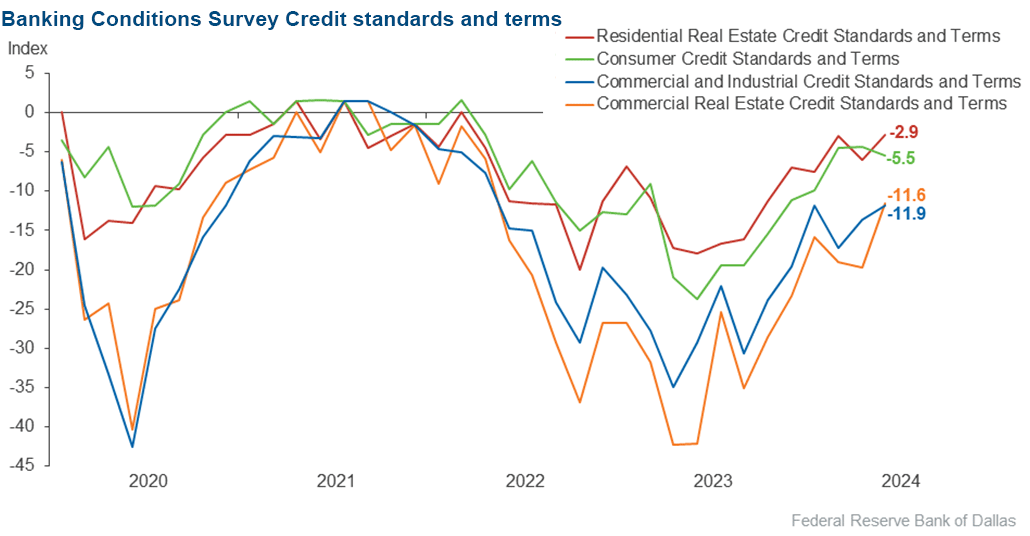

Credit standards and terms | –11.9 | –13.6 | 0.0 | 88.1 | 11.9 |

| Commercial Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 5.8 | –4.6 | 33.3 | 39.1 | 27.5 |

Nonperforming loans | 5.8 | 7.6 | 11.6 | 82.6 | 5.8 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –11.6 | –19.7 | 0.0 | 88.4 | 11.6 |

| Residential Real Estate Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | 10.0 | –1.5 | 31.4 | 47.1 | 21.4 |

Nonperforming loans | 2.8 | 3.0 | 5.7 | 91.4 | 2.9 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –2.9 | –6.0 | 0.0 | 97.1 | 2.9 |

| Consumer Loans: Over the past six weeks, how have the following changed? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Loan volume | –1.4 | –9.9 | 18.9 | 60.8 | 20.3 |

Nonperforming loans | 13.3 | 7.1 | 17.3 | 78.7 | 4.0 |

| Indicator | Current Index | Previous Index | % Reporting Eased | % Reporting No Change | % Reporting Tightened |

Credit standards and terms | –5.5 | –4.3 | 0.0 | 94.5 | 5.5 |

| Banking Outlook: What is your expectation for the following items six months from now? | |||||

| Indicator | Current Index | Previous Index | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Total loan demand | 17.3 | –1.4 | 41.3 | 34.7 | 24.0 |

Nonperforming loans | 29.3 | 42.9 | 40.0 | 49.3 | 10.7 |

| General Business Activity: What is your evaluation of the level of activity? | |||||

| Indicator | Current Index | Previous Index | % Reporting Better | % Reporting No Change | % Reporting Worse |

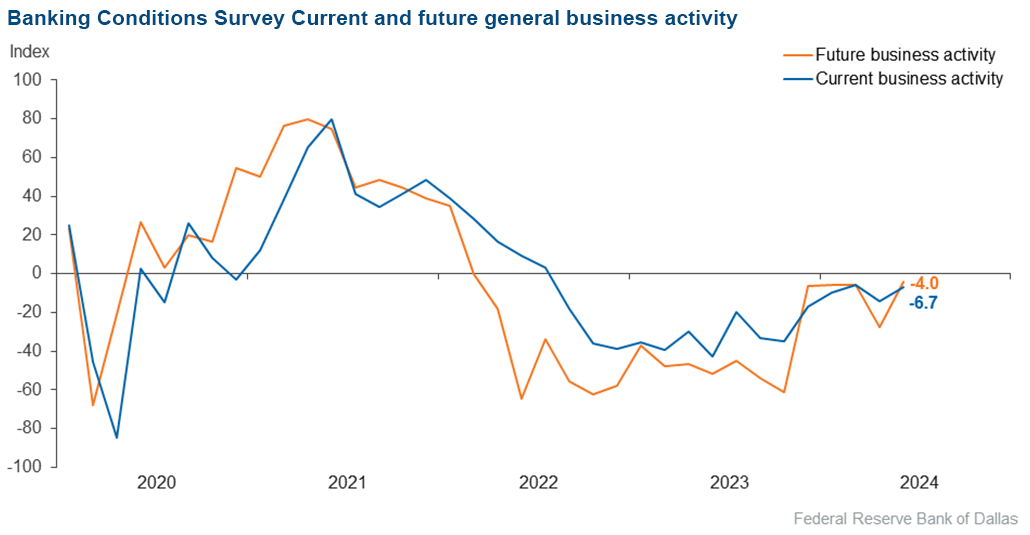

Over the past six weeks | –6.7 | –14.3 | 13.3 | 66.7 | 20.0 |

Six months from now | –4.0 | –27.6 | 25.3 | 45.3 | 29.3 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Respondents were given an opportunity to comment on any issues that may be affecting their business.

These comments are from respondents’ completed surveys and have been edited for publication.

- Additional regulatory requirements like the Bank Secrecy Act, data governance, etc. require so many more employees that they are contributing to increasing cost. That makes it harder to give investors a fair return on capital.

- High interest rates, labor costs and the housing inflation are having an increasingly adverse impact on loan demand and credit quality. I expect the impact to gradually worsen over the next six months, all things being equal.

- The macro impacts of higher-for-longer are resulting in decreased economic growth.

- We feel Texas is healthier than the rest of the country. Generally, we are concerned that as long as unemployment remains low, if the Federal Open Market Committee (FOMC) lowers rates prematurely, the economy will expand and reignite it. We are also concerned about the polarizing election and economic impact from that and from tax and stimulus sunsets in 2026. Our greatest concern is how the government will disrupt the economy given its huge size and lack of coordination with monetary policy. We feel it is and can be very destructive.

- The Federal Reserve appears to be ignoring the number of bankruptcies and layoffs that continue to negatively affect stores that employ and sell products to the lower and middle class. FOMC action that would lower the federal funds rate could greatly improve historically depressed bank net interest margins.

- We are experiencing a slowdown in all categories of loans.

- Interest rates are not declining as anticipated. The upcoming presidential election, inflation issues, regulatory burdens, rising consumer debt levels and the high price of autos [are sources of concern].

- The regulatory burden being placed on banks by the Office of the Comptroller of Currency, the Federal Deposit Insurance Corporation and the Consumer Financial Protection Bureau (CFPB) has already and will continue to hurt our customers as we bankers try and take care of the financial needs of our communities. Our customers, and our banks, need the government to get off the necks of free markets and let the economy grow without government interference and restriction.

- Commercial real estate loans originated in 2019 and 2020 on five-year rate adjustments are starting to re-price. We are being pro-active to review these loans. So far, although the rate increases have been significant, we have not observed any cash flow concerns. The consumer spending slowdown has already started to be observed in the restaurant industry in our markets.

- CFPB rulemaking [is having a significant] impact on banking. The latest CFPB effort to curb junk fees on mortgages will drive people out of business if implemented. What will be left are providers outside of the regulatory framework that can create chaos in the system similar to the Great Financial Crisis of 2008.

- We are starting to see people walk away from their auto loans. We don't know if the lower quality of cars produced during the pandemic is a factor contributing to this.

Historical data can be downloaded dating back to March 2017. For the definitions, see data definitions.

NOTE: The following series were discontinued in May 2020: volume of core deposits, cost of funds, non-interest income and net interest margin.

Questions regarding the Banking Conditions Survey can be addressed to Mariam Yousuf at mariam.yousuf@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Banking Conditions Survey is released on the web.