Special Questions

Special Questions

Texas Business Outlook Surveys

Data were collected June 14–22, and 366 Texas business executives responded to the surveys.

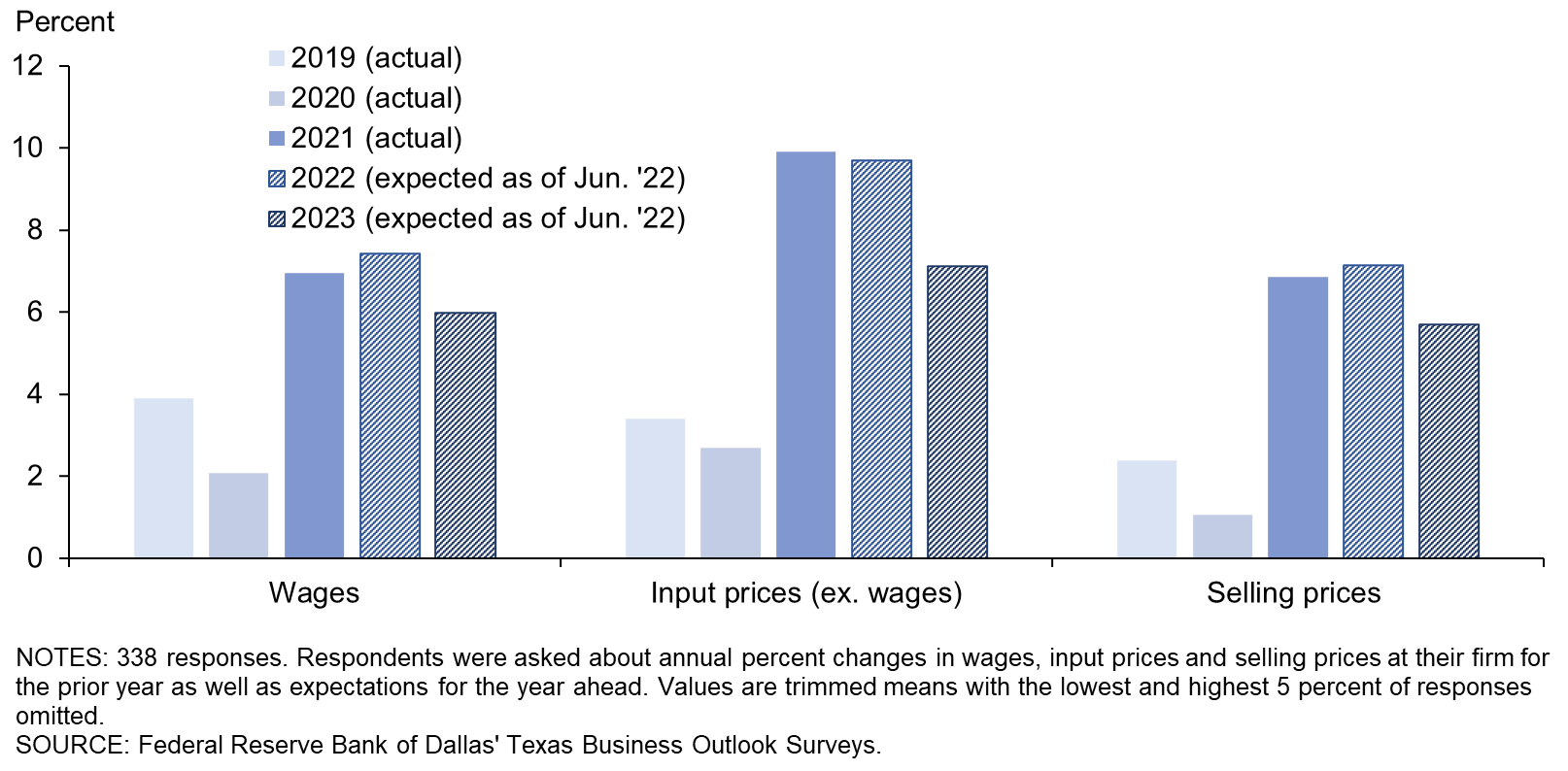

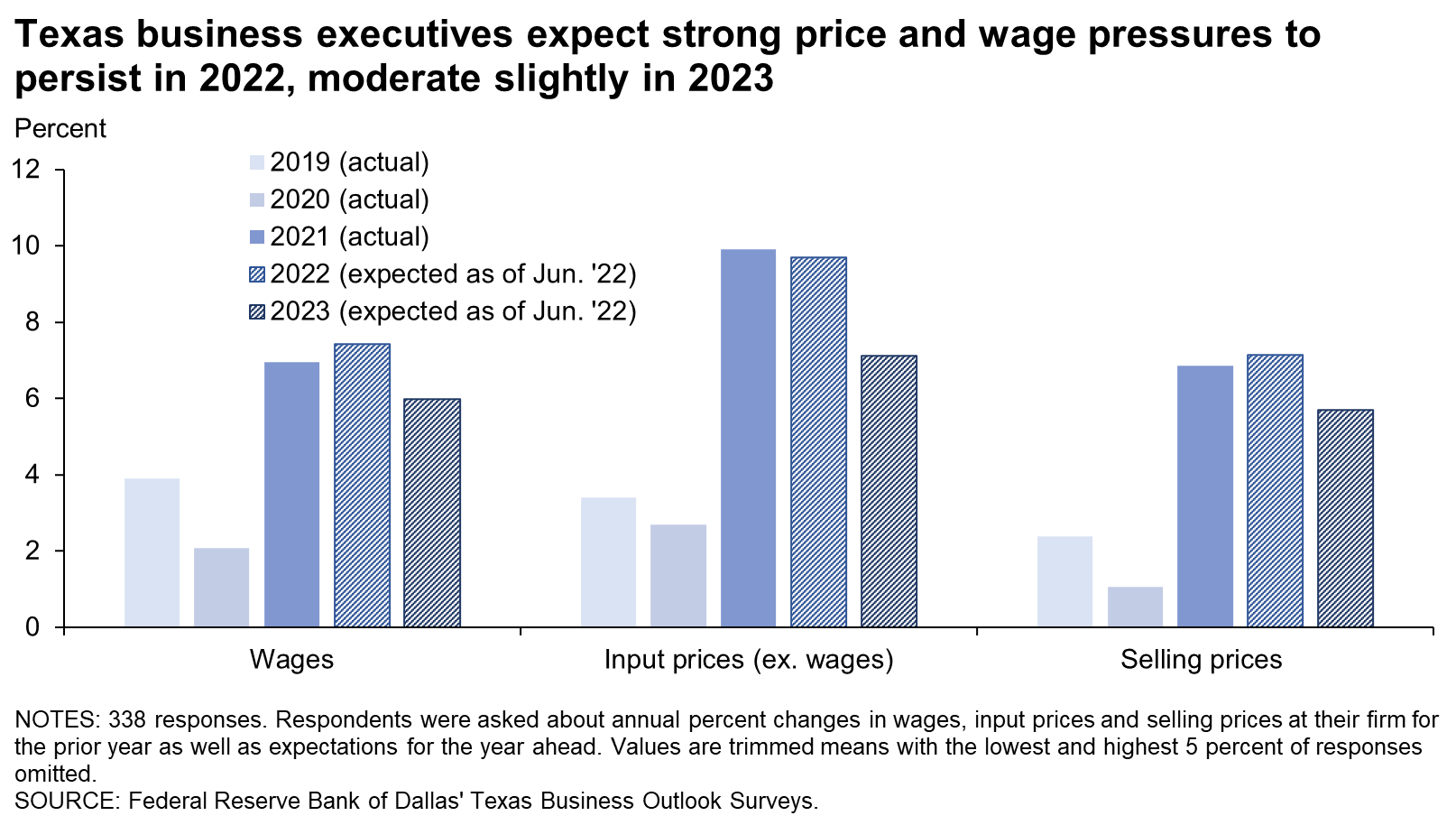

| 2019 | 2020 | 2021 | 2022 | 2023 | |||

| Actual (percent) |

Actual (percent) |

Actual (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

|

| Wages | 3.9 | 2.1 | 7.0 | 6.4 | 6.9 | 7.4 | 6.0 |

| Input prices | 3.4 | 2.7 | 9.9 | 7.1 | 8.5 | 9.7 | 7.1 |

| Selling prices | 2.4 | 1.1 | 6.9 | 6.4 | 6.4 | 7.1 | 5.7 |

| Data collected | Dec. '19 | Dec. '20 | Dec. '21 | Dec. '21 | Mar. '22 | Jun. '22 | Jun. '22 |

NOTES: 338 responses. Averages are calculated as trimmed means with the lowest and highest 5 percent of responses omitted.

{kind=link}

| Jul. '20 (percent) |

Aug. '21 (percent) |

Dec. '21 (percent) |

Mar. '22 (percent) |

Jun. '22 (percent) |

|

| Supply-chain disruptions | 16.9 | 40.8 | 44.3 | 50.0 | 50.6 |

| Limited operating capacity due to staffing shortages (difficulty hiring, absenteeism, COVID-19 infections and quarantining, vaccine mandates, etc.) | 21.4 | 31.8 | 45.8 | 38.6 | 40.8 |

| Weak demand | 57.3 | 23.9 | 19.4 | 15.1 | 26.4 |

| Reduced productivity due to alternative work arrangements | 14.8 | 9.0 | 9.2 | 7.2 | 8.6 |

| Limited operating capacity due to state/local restrictions | 20.6 | 5.4 | 4.3 | 2.1 | 2.9 |

| Other | 16.1 | 13.5 | 14.2 | 15.7 | 19.5 |

| None/not applicable | 12.4 | 21.1 | 14.8 | 18.4 | 14.1 |

NOTE: 348 responses.

Survey respondents were given the opportunity to provide comments. These comments can be found on the individual survey Special Questions results pages, accessible by the tabs above.

Texas Manufacturing Outlook Survey

Data were collected June 14–22, and 85 Texas manufacturers responded to the survey.

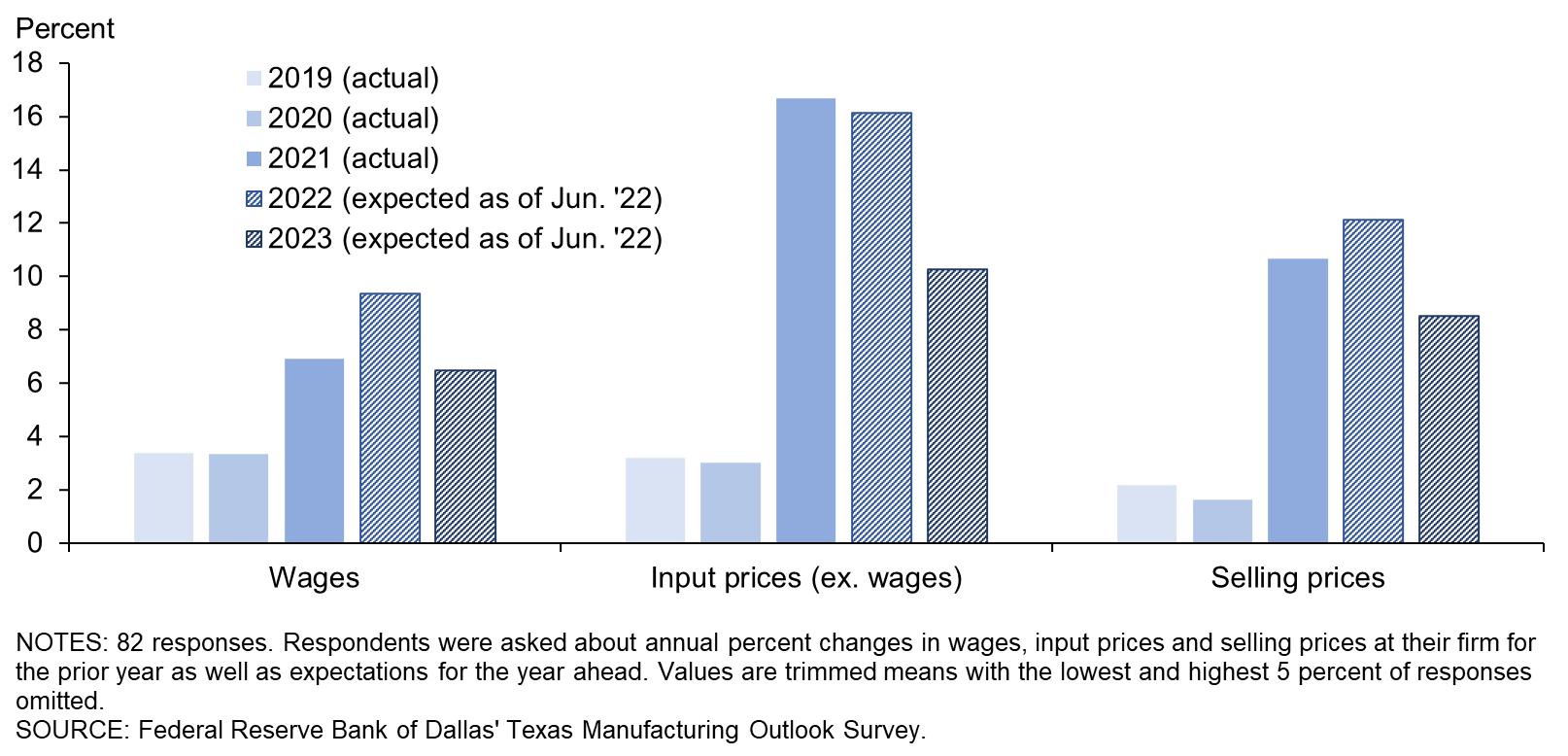

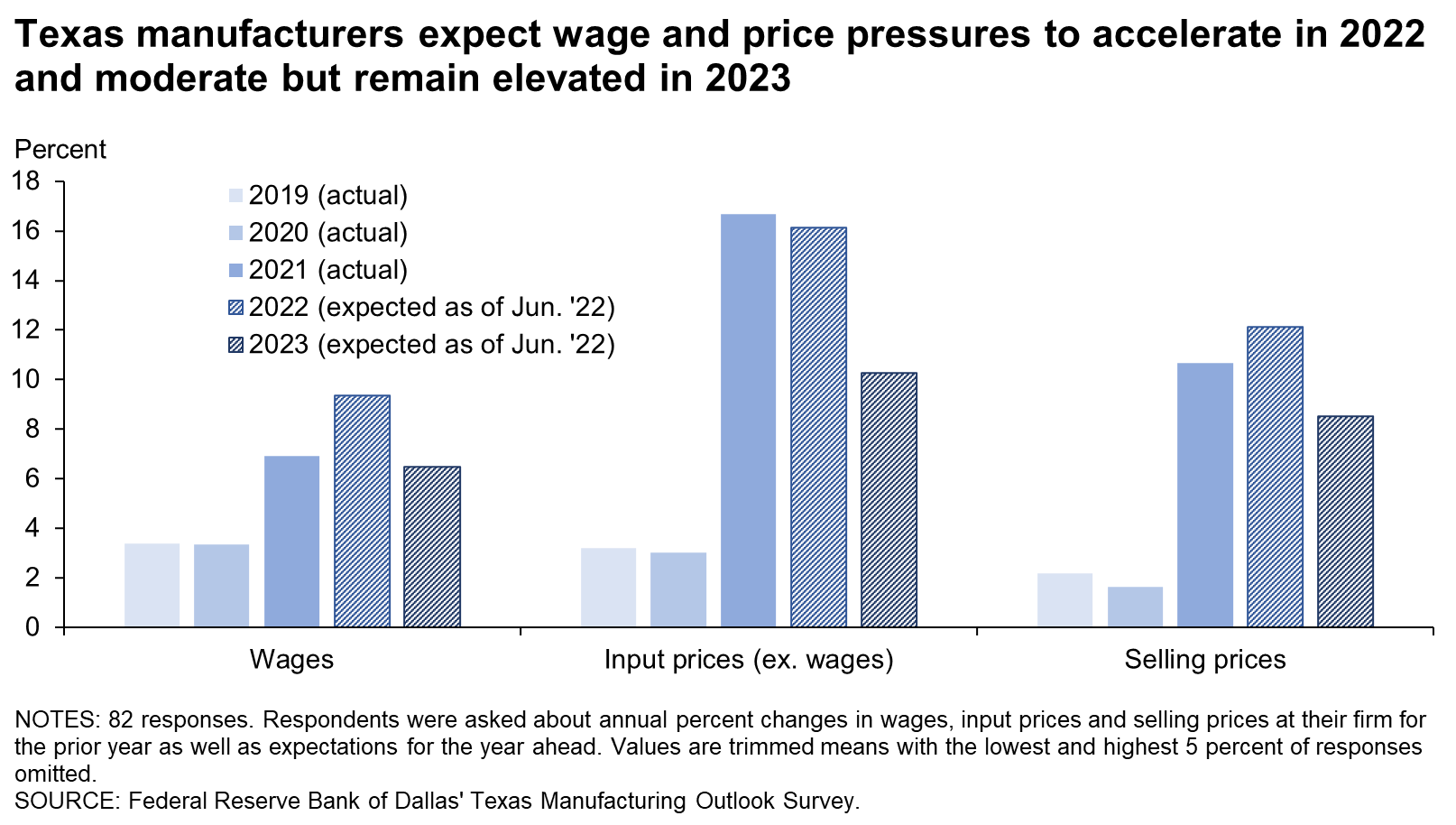

| 2019 | 2020 | 2021 | 2022 | 2023 | |||

| Actual (percent) |

Actual (percent) |

Actual (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

|

| Wages | 3.4 | 3.3 | 6.9 | 6.0 | 6.5 | 9.4 | 6.5 |

| Input prices | 3.2 | 3.0 | 16.7 | 8.5 | 13.1 | 16.1 | 10.3 |

| Selling prices | 2.2 | 1.6 | 10.7 | 8.1 | 9.4 | 12.1 | 8.5 |

| Data collected | Dec. '19 | Dec. '20 | Dec. '21 | Dec. '21 | Mar. '22 | Jun. '22 | Jun. '22 |

NOTES: 82 responses. Averages are calculated as trimmed means with the lowest and highest 5 percent of responses omitted.

{kind=link}

| Jul. '20 (percent) |

Aug. '21 (percent) |

Dec. '21 (percent) |

Mar. '22 (percent) |

Jun. '22 (percent) |

|

| Supply-chain disruptions | 25.2 | 72.2 | 75.9 | 72.6 | 75.3 |

| Limited operating capacity due to staffing shortages (difficulty hiring, absenteeism, COVID-19 infections and quarantining, vaccine mandates, etc.) | 31.1 | 44.4 | 56.3 | 46.4 | 44.7 |

| Weak demand | 65.0 | 21.1 | 19.5 | 15.5 | 31.8 |

| Reduced productivity due to alternative work arrangements | 10.7 | 8.9 | 12.6 | 6.0 | 5.9 |

| Limited operating capacity due to state/local restrictions | 3.9 | 2.2 | 2.3 | 4.8 | 2.4 |

| Other | 8.7 | 11.1 | 13.8 | 11.9 | 16.5 |

| None/not applicable | 10.7 | 7.8 | 0.0 | 6.0 | 7.1 |

NOTE: 85 responses.

Special Questions Comments

These comments have been edited for publication.

- We lost approximately $2.5 million in sales that would have been shipped to Russia.

- We are experiencing the highest unfilled job rates in recent history. Workforce shortages are crippling manufacturing sectors. We have found that despite significant wage increases, rich benefits and hiring bonuses for starting positions, both skilled and unskilled, we are struggling to find employees. If there is not some type of program implemented that allows for non-U.S. citizens to enter the workforce with proper identification, the situation will only worsen.

- Companies are bidding work below our cost to complete. There is fierce competition for the work with much larger fabricators.

- It is very difficult hiring new workers for the plant. And the cost of materials continues to rise.

- We’ve raised prices substantially over the past 12 months and will continue to do so. Our competitors got caught in the supply-chain problems and are now paying for it. A couple of our competitors have been forced to reduce their presence in bidding against us since they are unable to offer a product in a timely manner. We may see them go out of business. So, with our current inventory that we built up in 2021, we are positioned well for the future. And furthermore, our employees recognize what we’ve done as a company for their long-term benefits.

- The cost of living and especially property taxes are going up for employees, putting pressure on wages, which could ultimately drive up costs. I would like to see county and local government reduce property tax percentages to compensate for the much higher property values they are assessing to balance the equation for the residents.

- Material availability is the biggest thing. [It is leading to] long lead-times for new products in development.

- Supply-chain disruptions not only limit what products can be built, but the constantly changing availability dates increase challenges related to scheduling and hiring and fundamentally reduce the efficiency of operations. Not only are we facing rising costs on all sides and supply-chain delays, but we are also losing efficiency in operations with all the disruptions. This adds even more to the cost burden, which will ultimately be passed to consumers.

- We have a government that does not provide industry confidence. Total incompetence causes huge uncertainty. This will eventually trigger a forced recession, while developing countries are going exactly the opposite and we should join them for higher supply, constant growth and demand, and inflation stability. Instead, we as a country retract rather than change the strategy and continue to grow. This is insane.

- Everything that could be wrong with factors of production is wrong, with no help in sight other than the mid-term election cycle.

- Industrial real estate prices in the Dallas–Fort Worth area are still elevated. The low-interest environment caused real estate investment firms from all over the nation to enter the industrial real estate space and artificially raise the price per square foot by churning the properties just to turn a profit—not giving [the opportunity to] real end users such as manufacturers that actually provide value-added to products instead of just playing a rate arbitrage game to make money. The opportunity to invest in real estate for manufacturers lowered considerably in the past four years and was accelerated by the zero-percent federal-funds-rate environment, since leasing isn’t realistic because manufacturers spend considerable capital expenditures on capital-heavy improvements to operate, thus preferring to own the building.

- Raw material price increases are inflating at an unsustainable rate to maintain market competitiveness. Our customers are scrambling to find new vendors due to the rapid cost increases and preserve their margins. Many are contractually obligated to maintain a stable price to their customers for certain periods of time.

- Retail demand is softening; because everything is so expensive, the consumer is not buying as much as they were 30 days ago. In addition, our customers have a bulge of inventory due to a year of hoarding.

- Oil and gas customers haven’t increased their spending on promotions as their customers are hit with high fuel prices, which reduces their spending on non-fuel items. Supply-chain delays are limiting our ability to quickly quote and deliver on new customer requests.

- Difficulty in hiring and absenteeism trump all other reasons.

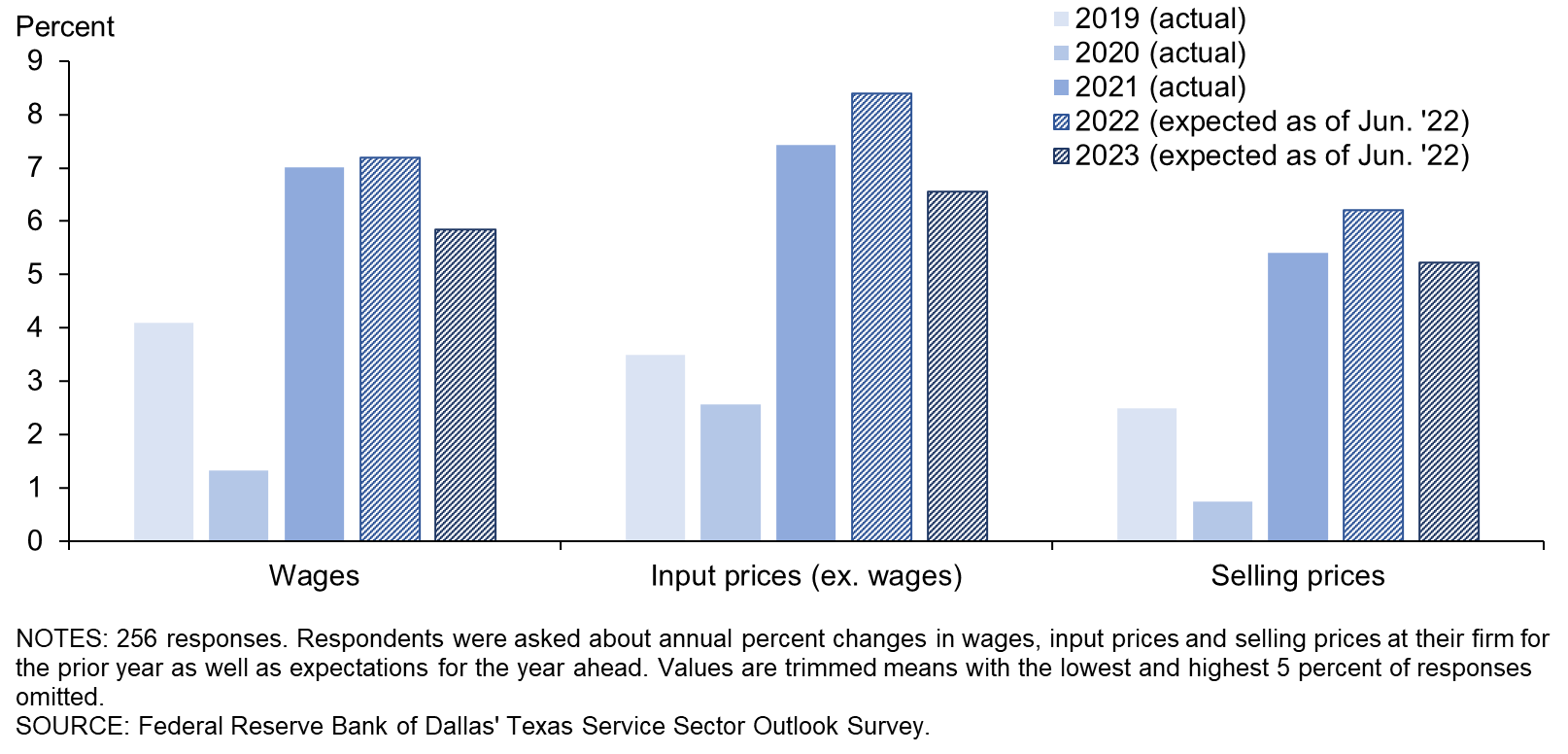

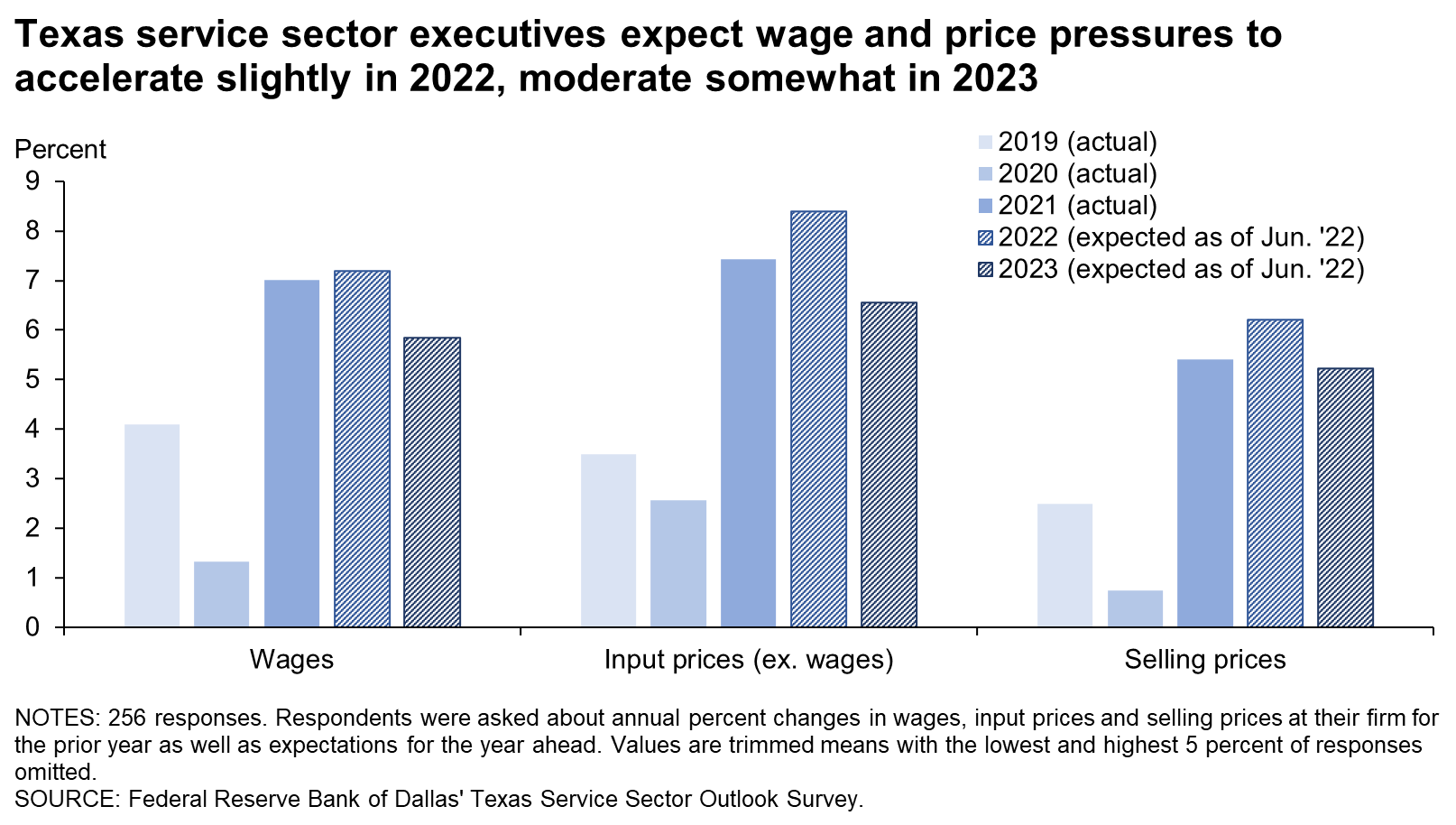

Texas Service Sector Outlook Survey

Data were collected June 14–22, and 281 Texas business executives responded to the survey.

| 2019 | 2020 | 2021 | 2022 | 2023 | |||

| Actual (percent) |

Actual (percent) |

Actual (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

|

| Wages | 4.1 | 1.3 | 7.0 | 6.7 | 7.1 | 7.2 | 5.9 |

| Input prices | 3.5 | 2.6 | 7.4 | 6.5 | 7.6 | 8.4 | 6.6 |

| Selling prices | 2.5 | 0.8 | 5.4 | 5.7 | 5.7 | 6.2 | 5.2 |

| Data collected | Dec. '19 | Dec. '20 | Dec. '21 | Dec. '21 | Mar. '22 | Jun. '22 | Jun. '22 |

NOTES: 256 responses. Averages are calculated as trimmed means with the lowest and highest 5 percent of responses omitted.

{kind=link}

| Jul. '20 (percent) |

Aug. '21 (percent) |

Dec. '21 (percent) |

Mar. '22 (percent) |

Jun. '22 (percent) |

|

| Supply-chain disruptions | 13.8 | 30.2 | 32.8 | 42.3 | 42.6 |

| Limited operating capacity due to staffing shortages (difficulty hiring, absenteeism, COVID-19 infections and quarantining, vaccine mandates, etc.) | 17.8 | 27.5 | 42.0 | 35.9 | 39.5 |

| Weak demand | 54.3 | 24.9 | 19.3 | 14.9 | 24.7 |

| Reduced productivity due to alternative work arrangements | 16.3 | 9.1 | 8.0 | 7.7 | 9.5 |

| Limited operating capacity due to state/local restrictions | 26.8 | 6.4 | 5.0 | 1.2 | 3.0 |

| Other | 18.8 | 14.3 | 14.3 | 16.9 | 20.5 |

| None/not applicable | 13.0 | 25.7 | 20.2 | 22.6 | 16.3 |

NOTE: 263 responses.

Special Questions Comments

These comments have been edited for publication.

- As a small business owner, adding federal holidays to our yearly calendar is a hardship. Each one represents one more day per year with no revenue; however, the business' overhead continues to increase. Everyone wants goods on the shelves, but what is not considered is that those who bring them are constrained by an ever-decreasing window of time to get them there.

- The roller coaster continues with inflation becoming unanchored on top of slowing growth and higher caution in many business peoples’ opinions ... [this is] having lasting consequences globally.

- For our industry (broadband services) in metropolitan areas like Houston, there is intense competition among providers for consumers, with pricing becoming the competitive strategy. Couple this competitive landscape with the supply-chain disruptions and the resulting input price increases, and it is extremely difficult to pass these increases through to consumers and retain or grow the customer base. In the short term, we are staying the course and looking for supply-chain improvements and pricing stability in 2023.

- We have established a new entity to produce our own parts using additive manufacturing to address supply-chain issues.

- Capital is moving away from real estate. Bond yields are excellent and a much higher relative value than previously. This reallocation of capital, when combined with higher interest rates, is drawing capital out of the real estate markets generally. The resulting changes in development, acquisitions and refinancing generally will reduce activity and capital further.

- As demand diminishes and costs to operate increase, the economic growth is stalling, and it appears that will get worse. The fact that increased regulation is a major objective of the administration will result in further handcuffing community banks.

- We are a financial services/people business, so our primary costs are people. Travel to see clients is one of our "input" costs, and we expect that to be up. We have a fixed lease, so we have low real estate costs.

- As a management company, our selling price is a fixed percentage of rental income we are able to generate. While rents on new leases are up dramatically, existing leases are locked in for up to a year; therefore, our revenue lags well behind increases for supplies, insurance and even property taxes. This means wage increases have to wait.

- Demand continues to be strong, but delivering space to tenants is challenging due to delays in construction and utility connections, and supply constraints on suppliers for all types of materials and services.

- The government never does anything to make business more efficient; evidently it’s not their calling since few-to-none of them have ever been responsible for a payroll or a company P&L [profits and losses]. We have 24 locations in Texas, and each one is more difficult to build than the last due to some bureaucratic ridiculous regulation about the color or height or mounting or texture of something akin to a toilet seat. There is no telling what this country could produce and how efficiently we could do it if the government stayed out of areas they do not need to be in.

- Consulting in the energy arena has not been lucrative for the past two years.

- For those of us who service multiyear fixed-rate contracts, high inflation, increased government regulations/mandates, wage inflation, increased worker benefits and low productivity are narrowing profit margins to near zero. It will be difficult to hold on for long without making structural changes.

- [Our expectations on] input prices and selling prices are total guesses. We resell equipment, and our manufacturers set the list prices—which have gone up on some items over 25 percent already this year, a few items by 50 percent and others 5–10 percent. We pass on whatever price increases we get to our customers; with our standard markup for products, we can't afford not to.

- It is a very competitive market for young lawyers, but demand is still strong.

- Hiring talent is extremely complex right now.

- The labor market pricing for field service work is way out of balance. The same person can work inside for more money. There’s no reason to work outside in a dirty environment. I don't know what kind of money it is going to take to attract help.

- We are government and corporate contractors. Our contracts have been extended, and we are experiencing a large number of orders.

- In over 30 years in this business, I have never seen anything even close to the inflation rates we are currently experiencing. Our lower demand is being offset only by higher prices in our elite line of business. At the current rate of change, we will eliminate the ability for the average middle-class family to afford a swimming pool.

- Inflation is creating greater uncertainty regarding the direction of the economy, which is affecting the decisions of business owners and consumers. As business owners see consumers cut back, affecting their business, they make decisions to cut back on services.

- Most wage growth is in staff salaries where we can hire into higher job classifications. Salaries for existing faculty are largely unchanged but are up for new hires due to market pressure.

- We are a public school operating under a charter, which is 100 percent state/federal funded. Revenue is set by the state, and federal granting agencies are primarily using a per-student formula.

- It is still enormously challenging to find radiologic technologists and front desk staff.

- Due to the hike in gas prices, employees are looking for more wages. It is not easy to find potential employees with the current pay scale. We are forced to offer more wages to find talent.

- We are a nonprofit and don't have a selling price.

- The rapid run-up in gas prices is impacting our leisure demand over the next 90 days. As prices rise, more people will likely forgo travel.

- We still can't hire or retain staff to be open 100 percent despite increasing the rate of pay, benefits and flexibility. We are operating at about 85 percent capacity. We see no slowdown in increase of input costs and a likely turndown in demand as customers grapple with their own increase in costs.

- We forecast that labor and input costs/prices will both continue to increase in the near term. However, pricing power is declining and may have peaked, so we may not be able to cover cost increases with price increases. This is pointing strongly to an accelerated shift in automation to reduce labor costs and keep margins at satisfactory levels.

- We are getting more applicants, but we are still short staffed. My company is still dealing with high employee turnover due to a shift in work dynamics brought on by the pandemic. The work ethic of new employees is drastically different than the work ethic of prepandemic employees.

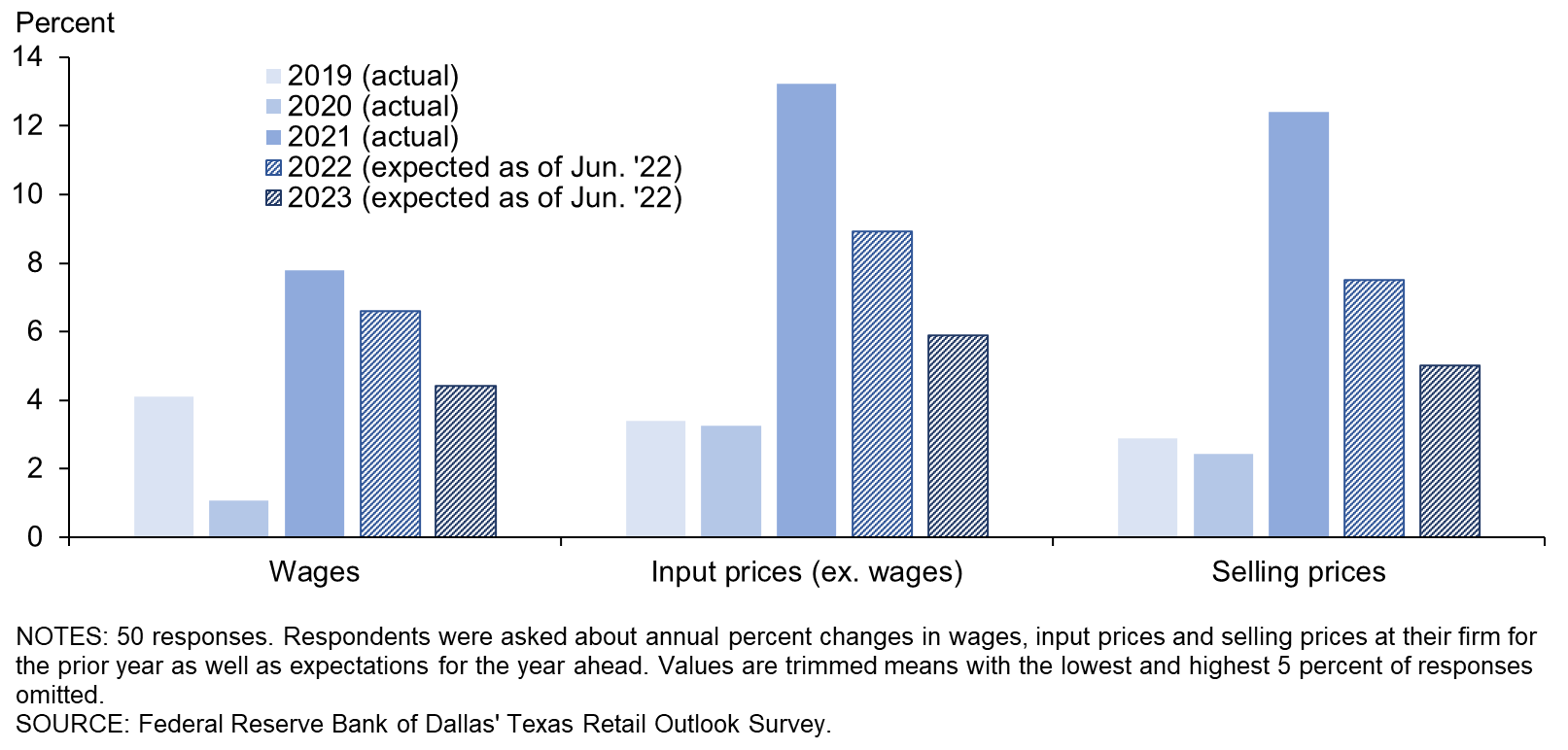

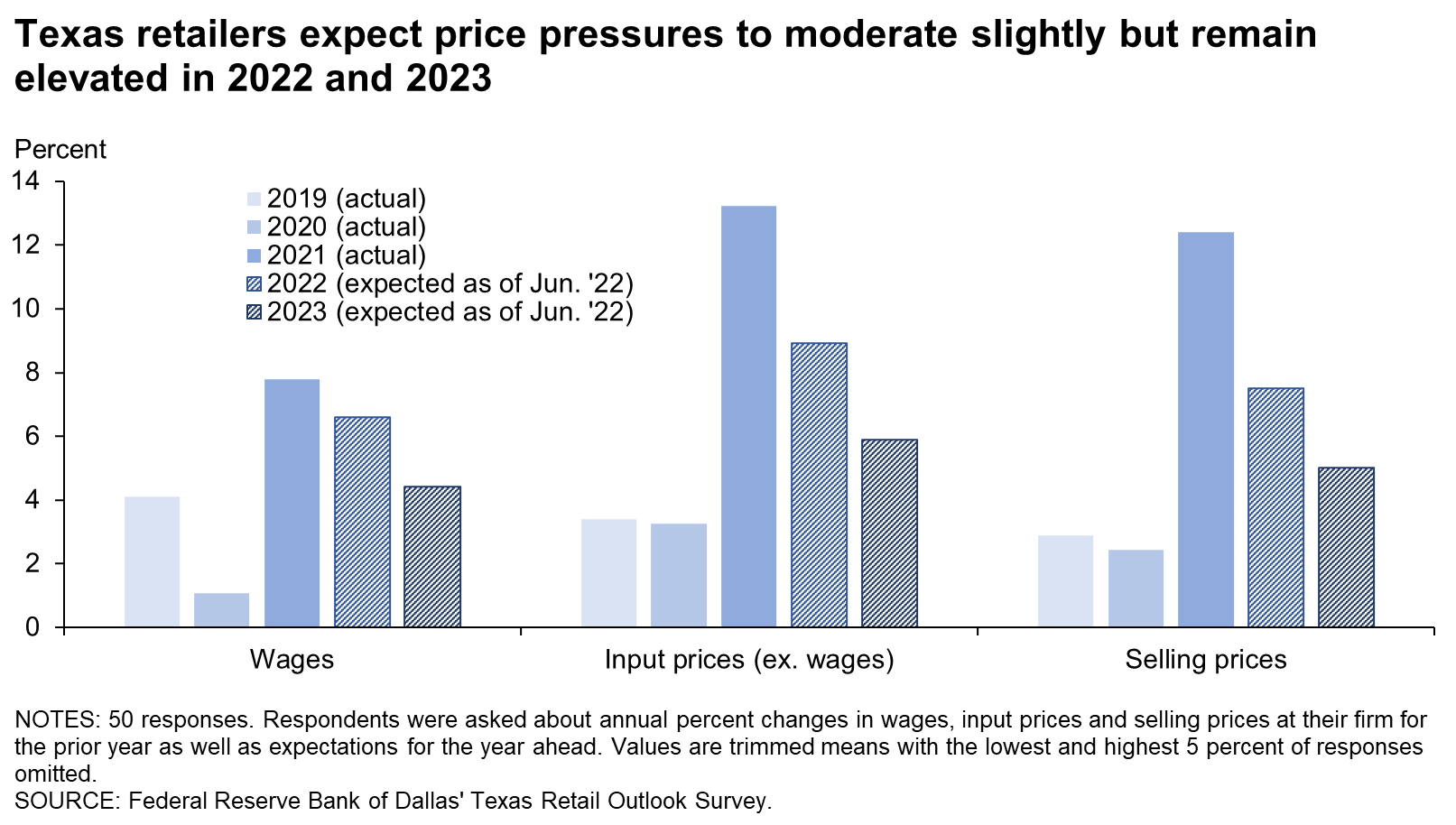

Texas Retail Outlook Survey

Data were collected June 14–22, and 55 Texas retailers responded to the survey.

| 2019 | 2020 | 2021 | 2022 | 2023 | |||

| Actual (percent) |

Actual (percent) |

Actual (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

Expected (percent) |

|

| Wages | 4.1 | 1.1 | 7.8 | 8.3 | 7.2 | 6.6 | 4.4 |

| Input prices | 3.4 | 3.3 | 13.2 | 8.9 | 9.4 | 8.9 | 5.9 |

| Selling prices | 2.9 | 2.4 | 12.4 | 8.7 | 8.8 | 7.5 | 5.0 |

| Data collected | Dec. '19 | Dec. '20 | Dec. '21 | Dec. '21 | Mar. '22 | Jun. '22 | Jun. '22 |

{kind=link}

| Jul. '20 (percent) |

Aug. '21 (percent) |

Dec. '21 (percent) |

Mar. '22 (percent) |

Jun. '22 (percent) |

|

| Supply-chain disruptions | 51.0 | 73.8 | 78.4 | 78.6 | 72.0 |

| Limited operating capacity due to staffing shortages (difficulty hiring, absenteeism, COVID-19 infections and quarantining, vaccine mandates, etc.) | 22.4 | 23.8 | 40.5 | 26.2 | 32.0 |

| Weak demand | 49.0 | 26.2 | 18.9 | 19.0 | 26.0 |

| Reduced productivity due to alternative work arrangements | 12.2 | 7.1 | 8.1 | 4.8 | 6.0 |

| Limited operating capacity due to state/local restrictions | 20.4 | 4.8 | 5.4 | 0.0 | 2.0 |

| Other | 20.4 | 7.1 | 2.7 | 7.1 | 22.0 |

| None/not applicable | 6.1 | 9.5 | 5.4 | 11.9 | 6.0 |

NOTE: 50 responses.

Special Questions Comments

These comments have been edited for publication.

- Domestic protein producers are still not able to "get ahead" of production. Our POs [product orders] are still being shorted, and lead times are still longer than typical. Historically, most protein suppliers kept inventory in the freezer. Since COVID started, producers are shipping everything from production, and there isn't any meaningful inventory in the freezer.

- The automobile business continues to see inventory conditions worsen after more than 12 months of parts shortages. Our manufacturers are stating there will be no relief until late 2023. This will continue to limit sales and will ultimately reduce affordability.

- We have staffing shortages mainly in skilled repair techs.

- Pharmacy benefit managers (PBMs) cause unwarranted economic hardship on patients and pharmacies.

- We can't get truck drivers licensed because the DPS [Department of Public Safety] has paralyzed the process. It can take up to six months for a driver to get a CDL [commercial driver’s license] with HAZMAT [hazardous materials]. The local DPS offices won't even answer the phone. Fuel is high because the government is limiting [both] drilling and building refineries.

Questions regarding the Texas Business Outlook Surveys can be addressed to Emily Kerr at emily.kerr@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest surveys are released on the web.