Texas Service Sector Outlook Survey

Growth in Texas service sector activity accelerates

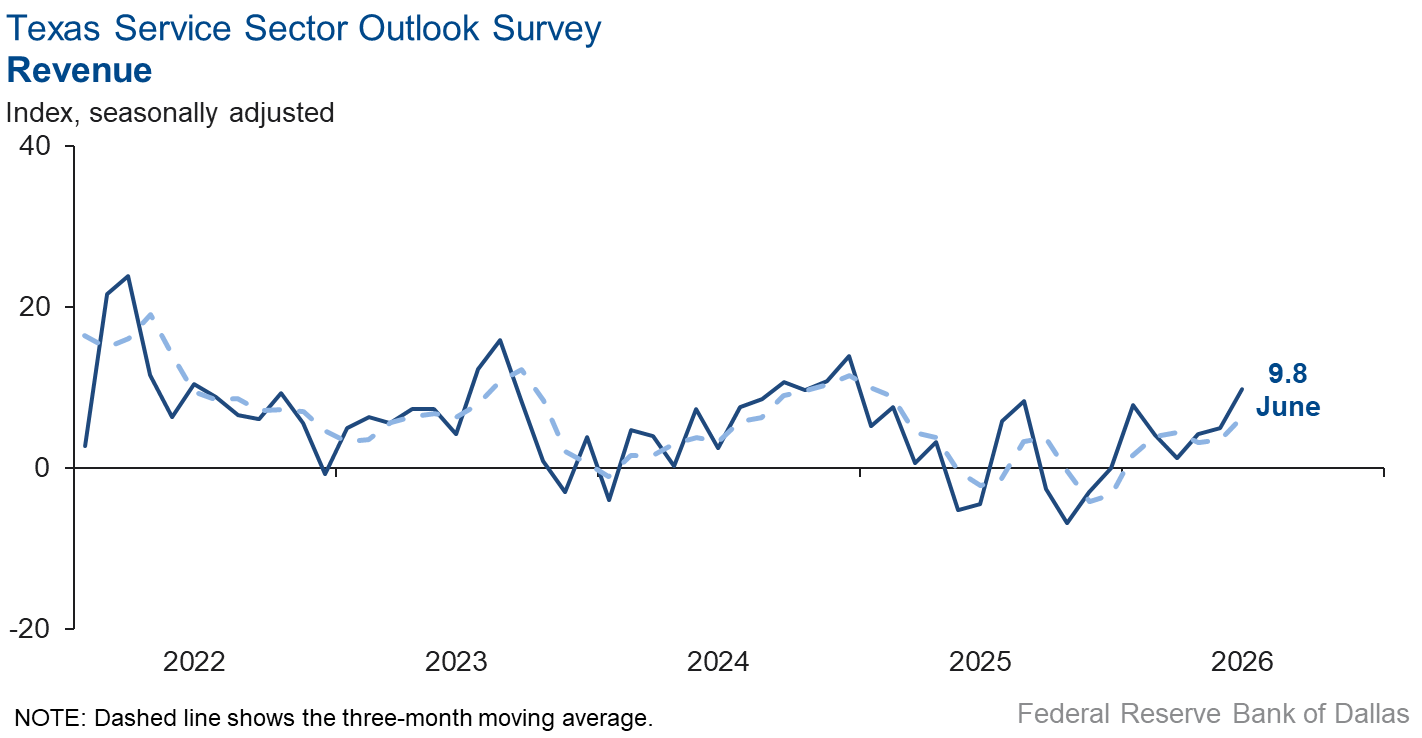

Texas service sector activity expanded at a faster pace in June than the prior month, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, increased five points to 9.8.

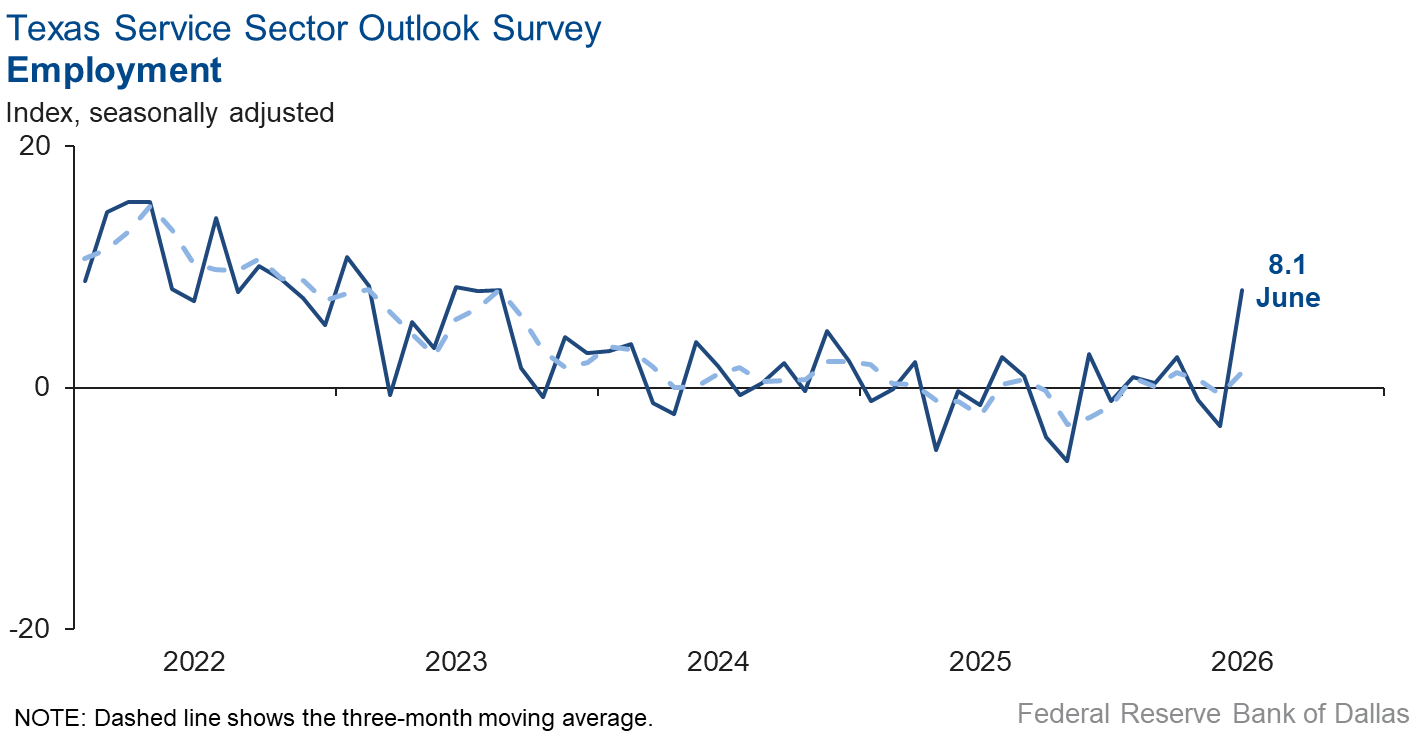

Labor market measures suggested a resumption of employment growth and an increase in workweeks in June. The employment index jumped to 8.1 from -3.2 in May. The part-time employment index was little changed at 2.4. Meanwhile, the hours worked index rose four points to 3.6.

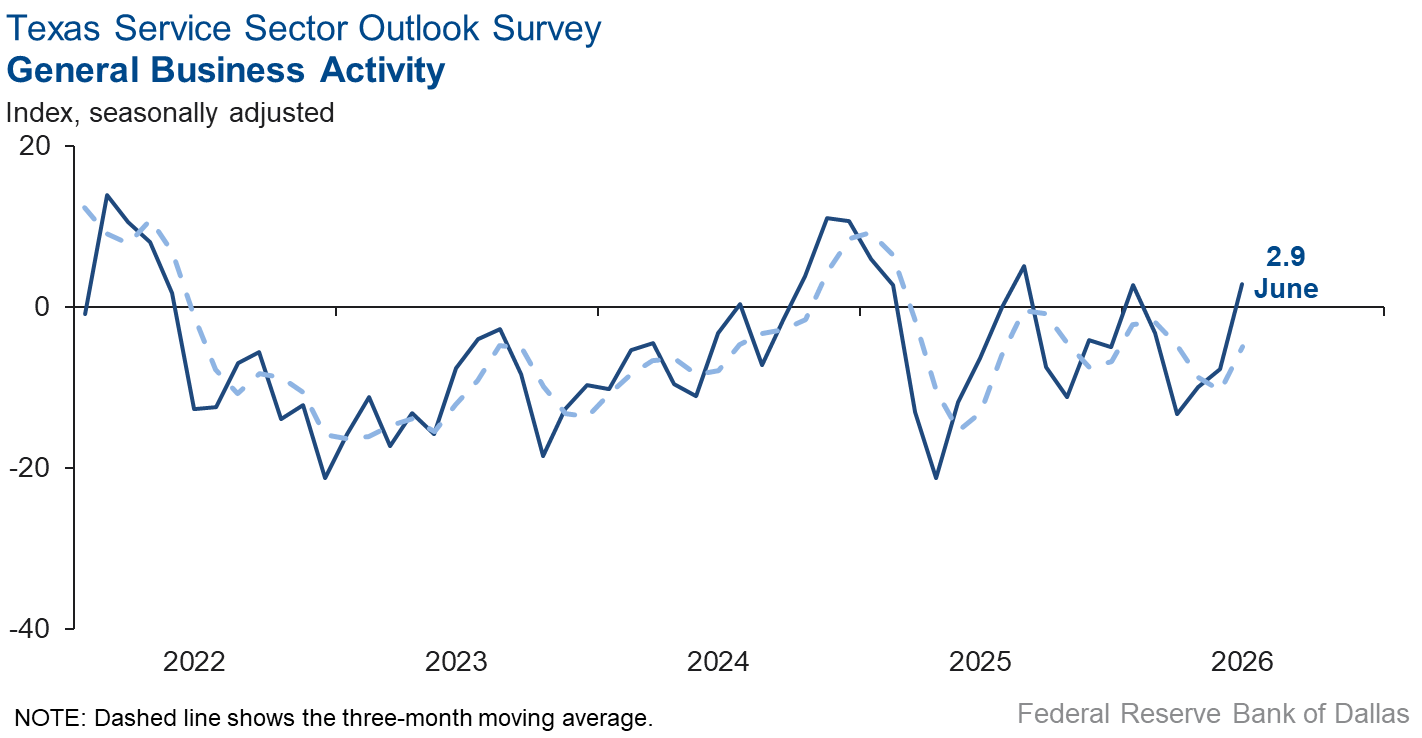

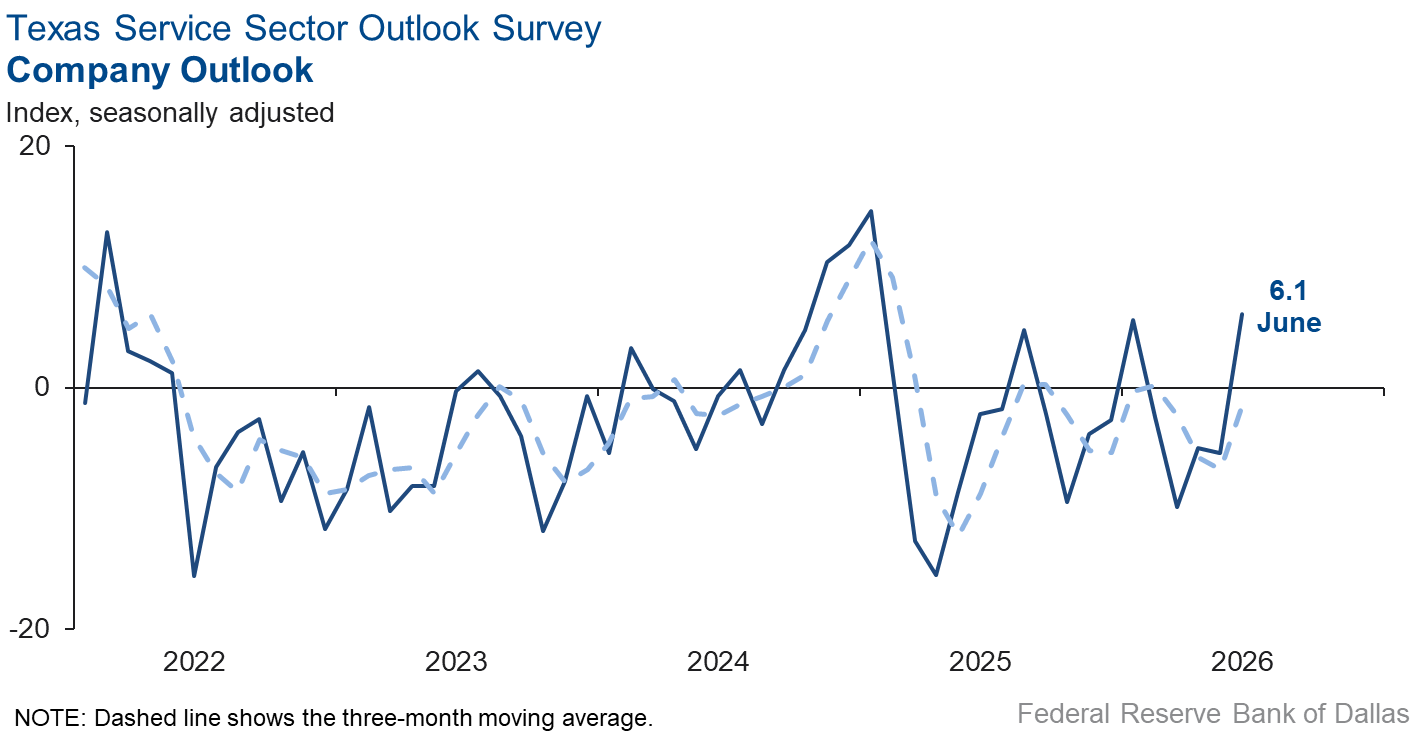

Perceptions of broader business conditions rebounded in June. The general business activity index moved up to 2.9 from -7.7. The company outlook index also bounced back into positive territory, surging 12 points to 6.1. Meanwhile, the outlook uncertainty index was little changed at 12.6.

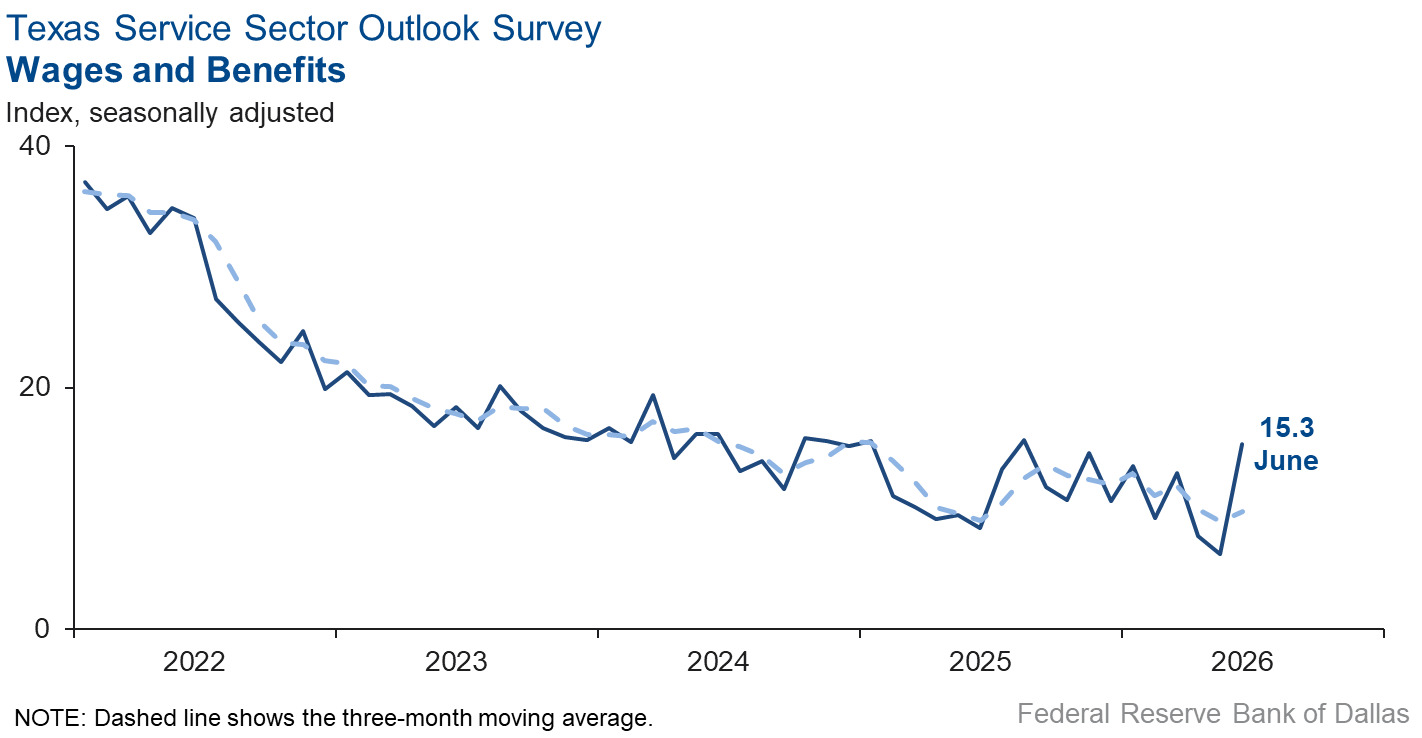

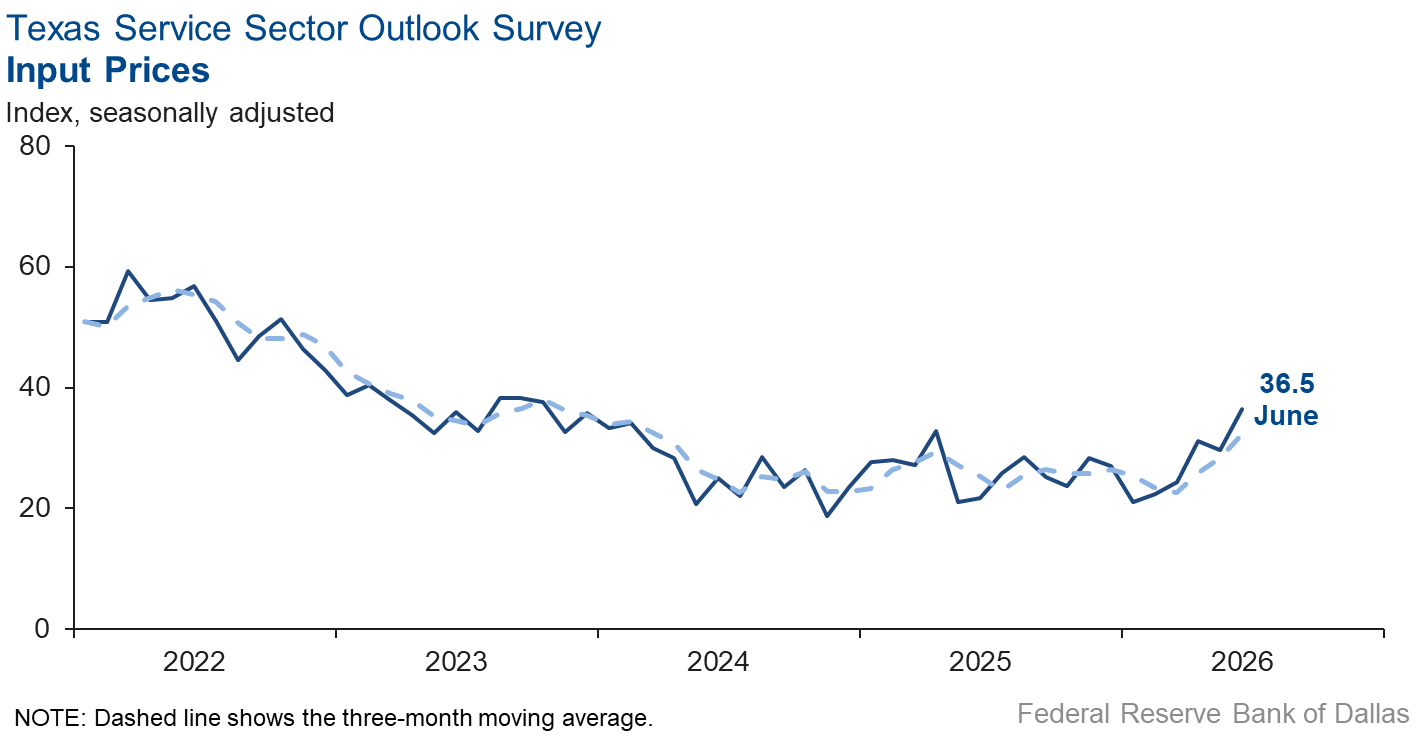

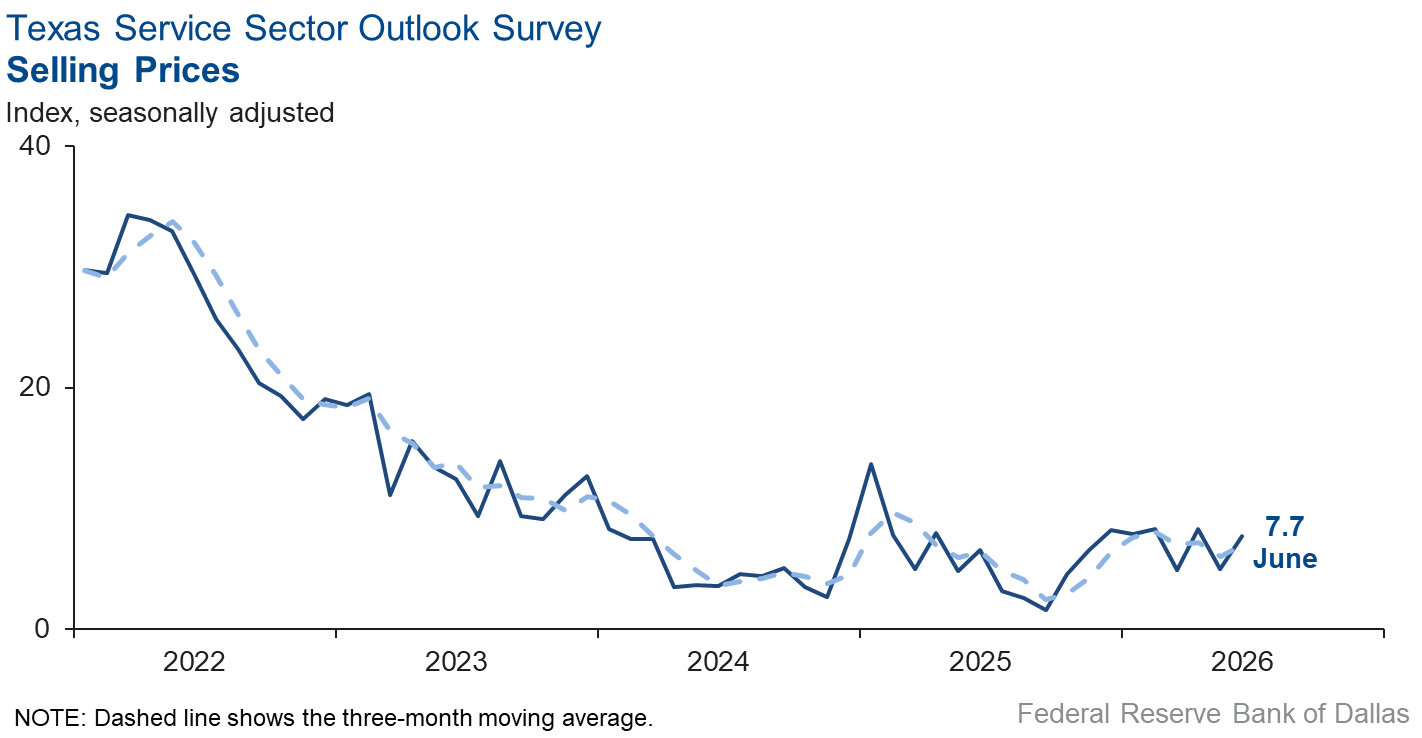

Selling price pressures increased slightly, while input price and wage pressures grew at a faster pace. The selling prices index edged up to 7.7 from 5.0. The input prices index moved up seven points to 36.5, registering well above the series average of 27.8. The wages and benefits index rose nine points to 15.3.

Respondents’ expectations regarding future service sector activity improved markedly. The future revenue index rose four points to 33.3, while the future general business activity index jumped up 18 points to 17.2. Other future service sector activity indexes, such as employment and capital expenditures, remained in solidly positive territory.

Next release: July 28, 2026

Data were collected June 16–24, and 214 of the 349 Texas service sector business executives surveyed submitted responses. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month.

Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease.

Data have been seasonally adjusted as necessary.

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 9.8 | 5.0 | +4.8 | 9.9 | 6(+) | 26.8 | 56.2 | 17.0 |

Employment | 8.1 | –3.2 | +11.3 | 5.7 | 1(+) | 17.0 | 74.1 | 8.9 |

Part–Time Employment | 2.4 | 2.3 | +0.1 | 1.2 | 4(+) | 5.6 | 91.2 | 3.2 |

Hours Worked | 3.6 | –0.5 | +4.1 | 2.4 | 1(+) | 7.3 | 89.0 | 3.7 |

Wages and Benefits | 15.3 | 6.2 | +9.1 | 15.4 | 73(+) | 19.2 | 76.9 | 3.9 |

Input Prices | 36.5 | 29.7 | +6.8 | 27.8 | 74(+) | 38.1 | 60.3 | 1.6 |

Selling Prices | 7.7 | 5.0 | +2.7 | 7.4 | 71(+) | 13.8 | 80.1 | 6.1 |

Capital Expenditures | 10.2 | 6.4 | +3.8 | 9.7 | 71(+) | 14.8 | 80.6 | 4.6 |

| General Business Conditions Current (versus previous month) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 6.1 | –5.4 | +11.5 | 3.8 | 1(+) | 20.2 | 65.7 | 14.1 |

General Business Activity | 2.9 | –7.7 | +10.6 | 1.7 | 1(+) | 19.1 | 64.8 | 16.2 |

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Outlook Uncertainty | 12.6 | 14.0 | –1.4 | 14.1 | 61(+) | 25.1 | 62.5 | 12.5 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend* | % Reporting Increase | % Reporting No Change | % Reporting Decrease |

Revenue | 33.3 | 28.9 | +4.4 | 37.1 | 74(+) | 45.7 | 42.0 | 12.4 |

Employment | 14.6 | 15.3 | –0.7 | 22.8 | 74(+) | 24.1 | 66.4 | 9.5 |

Part–Time Employment | 0.0 | 4.6 | –4.6 | 6.4 | 1() | 7.1 | 85.8 | 7.1 |

Hours Worked | 5.9 | 3.8 | +2.1 | 5.8 | 12(+) | 9.0 | 87.9 | 3.1 |

Wages and Benefits | 41.6 | 37.0 | +4.6 | 37.5 | 74(+) | 43.8 | 53.9 | 2.2 |

Input Prices | 48.2 | 45.9 | +2.3 | 44.2 | 234(+) | 51.2 | 45.8 | 3.0 |

Selling Prices | 24.2 | 22.0 | +2.2 | 24.4 | 74(+) | 29.8 | 64.6 | 5.6 |

Capital Expenditures | 21.2 | 16.7 | +4.5 | 22.4 | 73(+) | 27.4 | 66.3 | 6.2 |

| General Business Conditions Future (six months ahead) | ||||||||

| Indicator | Jun Index | May Index | Change | Series Average | Trend** | % Reporting Improved | % Reporting No Change | % Reporting Worsened |

Company Outlook | 17.1 | 0.6 | +16.5 | 15.2 | 14(+) | 31.6 | 53.9 | 14.5 |

General Business Activity | 17.2 | –0.7 | +17.9 | 11.8 | 1(+) | 31.3 | 54.6 | 14.1 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

Data have been seasonally adjusted as necessary.

Comments from survey respondents

Survey participants are given the opportunity to submit comments on current issues that may be affecting their businesses. Some comments have been edited for grammar and clarity.

- The continued international uncertainty and economic malaise is holding travel into San Antonio flat or down compared with last year.

- We are cautiously hopeful about the outlook but not yet believing it will actually happen.

- We caught a wave in May, with several former clients reaching out to fill mid- to senior-level direct-hire roles they'd struggled to fill on their own. That's the market in a nutshell: fewer openings overall, but real difficulty finding the right talent when a need does arise. As for the future, I'm as unsure today as I was six months ago—rising interest rates and the conflict with Iran weigh on our outlook, so we're focused on making hay while the sun shines.

- The uncertainty has been evident for some time with all the major events that have been going on. There is hope that the environment will settle down and we can get back to work on improving the economy and lowering inflation.

- Increasing costs for food, fuel and housing are affecting our operations directly with added indirect impact due to the effects on our students.

- Customers are only replacing the appliances that have broken down.

- We are beginning to face headwinds and some softening in sales and foot traffic at some locations for the first time in the company's 16-year history. Customers are pushing back on product costs, and demand has clearly softened. Our sense is that our customers may finally be feeling the pinch of high energy costs and general inflation.

- We are in the insurance business, and premiums are falling in most lines of commercial coverage. This is expected for the next 24 months.

- Inflation is affecting supply chains.

- I'm tempted to put "decreased" on the uncertainty box, but without a signed deal between Iran and the U.S., I'm not. If the deal is signed and everyone sticks to the agreement, fuel prices should fall. We're already seeing fuel prices (diesel) soften, but trucking companies aren't passing them down just yet. Our industry (transportation in the food service space) has implemented temporary fuel surcharges with the rapid increase in fuel costs, but everyone has established benchmarks to retract or lower the fuel surcharges. I see it on the horizon, but it hasn't come to pass.

- As long as we are paying these ridiculous tariffs, the economy will continue to stall, and so will our business. The government should also consider loan forgiveness for businesses that have kept up but are having a problem with their EIDLs (Economic Injury Disaster Loans).

- Consumer confidence is weak, and transaction prices are inflated. High interest rates are causing monthly payments to be more than consumers can afford.

- Uncertainty of the Iran war has become muted, so we are starting to see a little more stability in our retail business. That said, high prices continue to magnify spending decisions.

- There are too many things impacting our business that are beyond our control.

- We sell propane, gasoline and diesel. The Iran war has increased our uncertainty regarding pricing over the next nine months.

- The Iran war [is an issue impacting our business].

- Uncertainty continues even though we have all become used to it. Things will continue to bounce up and down based on the daily [statements] of the president. We will not be making very many major investment decisions.

- I feel the sales and approval cycle will be longer.

- Not in particular to the firm itself, but we are concerned about the pull-in demand in infrastructure projects, whether that is from the tax benefits, the data center and electric utilities boom or the fear from a rising 10-year yield (which we see early signs of pressuring refinancings in 2027).

- The cost of fuel is affecting the cost of doing business because we have a large pickup truck vehicle fleet.

- Wage pressure still exists when trying to hold on to workers with 20 or more years of experience in the architecture, engineering and construction industries. The experienced pool is drying up as baby boomers are retiring. Entry-level workers will take 10 years or more to become close to equivalent replacements.

- June employee count is up compared with May because of summer hires. Wages and benefits will be up six months from now because of inflation-driven salary pressures. Our cost to provide services is now higher because of inflation. However, we are expecting modest gains in the next six months.

- Economic indicators, including inflation over 4 percent and an unemployment rate of 4.3 percent, have contributed to a contraction in demand for products and services. In addition, recent immigration treatment of soccer World Cup visitors, including reports involving prominent Black players, has negatively affected the perception of the United States as a country committed to equal application of the rule of law and broad economic opportunity. These factors may be contributing to a decline in tourism and foreign investment.

- We are finding that nonprofits are starting to tighten their spending in anticipation that the economy won't improve. They are making decisions to focus on client services, and if there is additional funding, to put it toward direct-impact rather than capacity-building work in a lot of situations. We are still receiving inquiry calls, but they are for smaller projects or they say they can't afford what they could last year or the year before. This is happening at the same time that it is costing us more to do business (travel and mileage, equipment costs, etc.) resulting in us feeling the pinch.

- We are still seeing a lot of energy in the real estate market, but the uncertainty lingering about inflation and interest rates is still a concern. If an agreement with Iran can be reached, we feel the market will recover slowly over the next year.

- Outside of a very select number of sectors being bolstered by inflows of institutional and government capital, the economy seems to be experiencing very mediocre and lackluster conditions. Artificial intelligence has not had any material impact on cost reduction or growth acceleration despite an increasing amount of investment. As our clients struggle to find growth, we are seeing more contractual disputes and conflicts as well. Many of the macroeconomic uncertainties that were much discussed over the last year seem to be manifesting at the microeconomic level now, creating a business environment that, while not acutely catastrophic, is less than appealing.

- The federal government, including the Department of War, is even more unpredictable, taking budgeted funds away at the last minute. This makes doing business even more difficult.

- It is [becoming] more difficult for first time buyers to afford homes.

- Workforce apartment renters are struggling more but are generally figuring out how to get by. In analyzing the personal finances of delinquent renters, we find it is not so much about inadequate pay or rents that are too high; many are wasting inordinate amounts on delivery services, fast food, buy-now-pay-later schemes, media services, vices and other financial sinkholes. Getting by without these is a foreign concept to many, so we're teaching them as fast as we can. Often it is just a matter of budgeting and prioritizing. Sometimes it’s learning to buy fresh ingredients and cooking. Americans learned to do without many things during the Great Depression and World War II. It seems many are having to learn this all over again.

- Demand for new lease space has declined substantially since the end of last year.

- Oil prices and interest rates have an impact on our business. Uncertainty has increased.

- We should be having a great cotton harvest season.

- We are hoping that current geopolitical uncertainties subside and allow for more business confidence and stability.

- Cost of diesel fuel is very impactful [to our business].

- Since the Iran war has settled down, things are looking better.

- The end of hostilities in the Middle East will likely decrease the volumes moving through the port but will hopefully return some level of normalcy to operations and outlook.

Special questions

For this month’s survey, Texas business executives were asked supplemental questions on wages, prices and outlook concerns. Results below include responses from participants from both the Texas Manufacturing Outlook Survey and Texas Service Sector Outlook Survey. View individual survey results.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see data definitions.

| Unadjusted |

| Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Isabel Brizuela.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.