Global Perspectives: Maya MacGuineas on stabilizing the federal debt

A good measure of a nation’s ability to repay its obligations is the ratio of the stock of indebtedness to the flow of output produced in a given year. In recent years, this ratio has increased for the U.S. government, raising new questions about how the nation manages a debt burden that is approaching an all-time high.

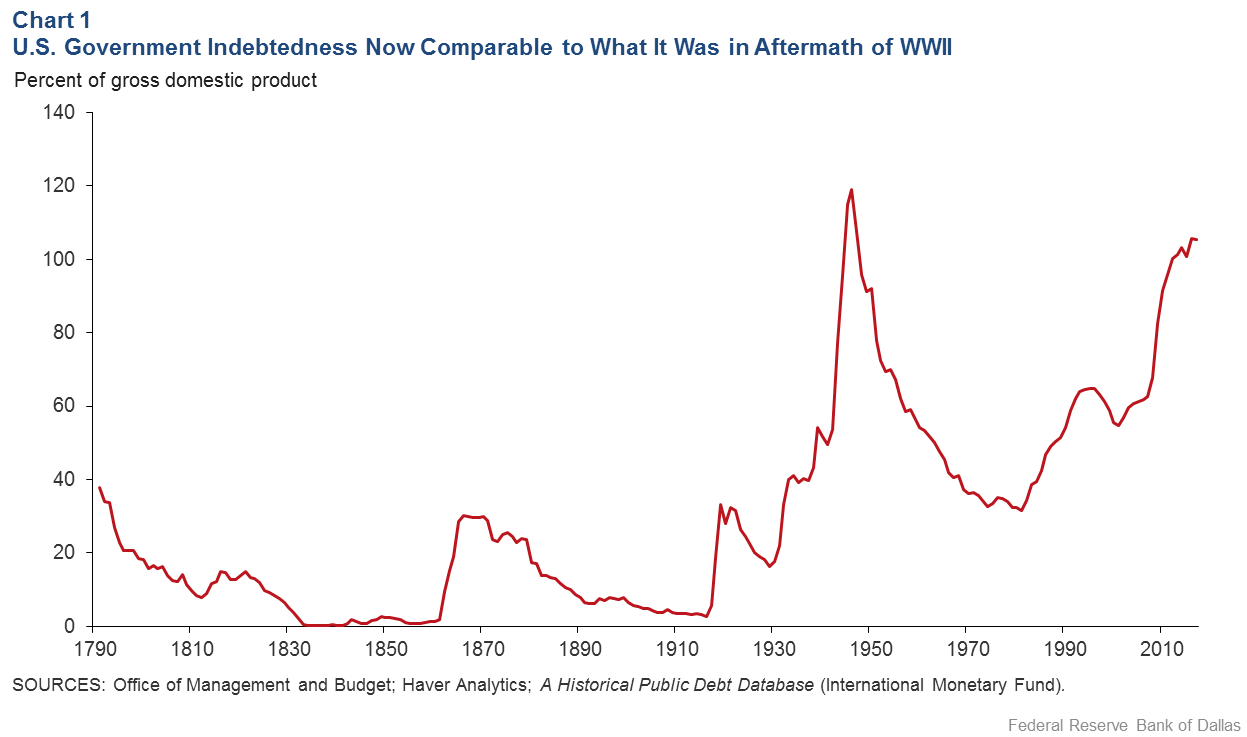

Chart 1 shows the evolution of this ratio—gross federal debt as a percent of gross domestic product (GDP)—for the United States from 1790 to 2017. It illustrates how the nation traditionally ran up large federal government debts only in wartime or in times of national economic emergency.

The debt-to-GDP ratio was just under 40 percent in 1790, the product of debts the states incurred to fight the Revolutionary War. The ratio fell steadily until the War of 1812, when it ticked up again, before declining to close to zero by the mid-19th century.

There were other peaks associated with the Civil War, World War I, the Great Depression and World War II, when the ratio reached 121 percent. It then declined steadily until the 1970s, when the ratio again neared the post-Revolutionary War level.

Then something changed. The United States began running large deficits, which persisted through the mid-1990s, pushing the debt-to-GDP ratio to 66 percent. A combination of a strong economy and a focus on fiscal consolidation briefly sent the ratio lower in the latter half of the 1990s, but for most of the past two decades, the ratio has grown steadily and is now almost back where it was at after World War II. Some of this increase is due to the severity of the Great Recession, though the ratio’s continuing upward trajectory appears more attributable to structural problems.

Last month, the Federal Reserve Bank of Dallas hosted Maya MacGuineas, president of the Committee for a Responsible Federal Budget, a bipartisan, nonprofit organization, at its Houston Branch as part of the Global Perspectives speaker series. This series was launched at the beginning of 2016 to bring leaders from the worlds of business, academia and policy making to the Dallas Fed to share their insights on global, national and regional developments.

MacGuineas discussed the growing burden of U.S. debt with Dallas Fed President Robert Kaplan. In the excerpt of their conversation, edited for clarity, they consider how to address this problem.

President Kaplan: A lot of time [when] people talk about rules for monetary policy, we’ve asked the question, “How come there aren’t any rules here for fiscal policy?” Most countries in the world … try to have enough internal reserves to match the amount of overseas debt they [have issued].

Maya MacGuineas: We have nothing close to a fiscal rule. In fact, the Joint Select Committee [on Budget and Appropriations Reform] that was thinking about this for the past year was contemplating, “Should we institute debt targets in this country?” It’s a glide path where you’re shooting to get your debt to a certain level.

So, the crazy idea that I have is we should pick a target in this country and we should do a sensible plan. We cut spending, we raise taxes, lots of things, but as soon as we get to that target, everybody starts getting tax rebates, and it’s called bribery.

I’ve gotten to the point of desperation, where I think we should have something like this. We need to find some things to unite around. We need to have some common aspirations. And then, if you put this [into a] tangible [form]—once debt gets to 60 percent of GDP, everybody gets a rebate every year—that’s just [the] kind of thing that could work.

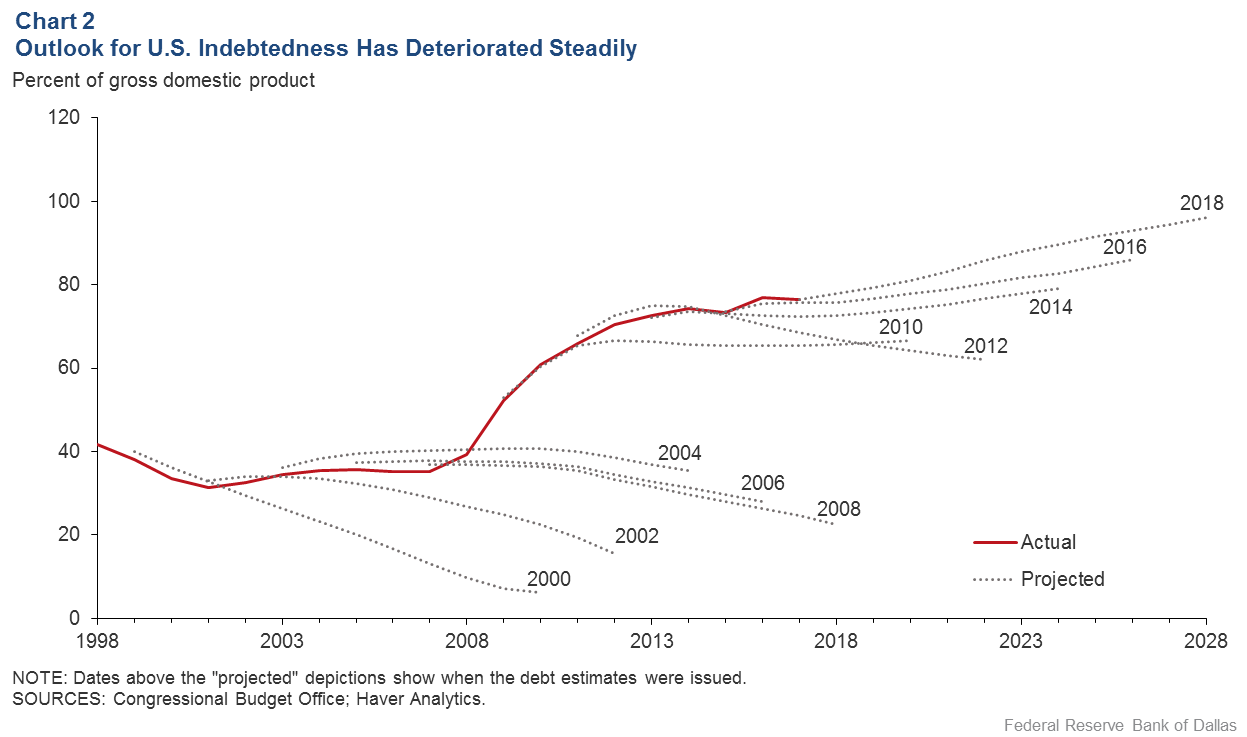

An alternative measure of indebtedness focuses on just debt held by the general public. The ratio of this number to GDP is lower than the overall number but shows the same broad trend. As of 2017, federal debt held by the general public was equivalent to about three quarters of GDP. The Congressional Budget Office’s (CBO) projections of the ratio over the past 20 years have deteriorated steadily, as depicted in various vintages of such CBO projections (Chart 2).

In 2000, the CBO was projecting the debt-to-GDP ratio would decline to a mere 6.3 percent by 2010. In 2018, the CBO projected the debt to GDP ratio would rise to 96 percent by 2028.

This steady deterioration in the outlook highlights the urgency of the need for some type of fiscal rules to cap debt at a sustainable level.

About the Author

Mark A. Wynne

Wynne is vice president and associate director of research in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the author and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.