Dallas Fed Energy Survey suggests oil price drop won’t cause sector collapse in 2019

Following a banner year in 2018, will U.S. oil producers retrench and reduce capital spending after the recent double-digit oil price decline? The latest Dallas Fed Energy Survey provides some clues about what may be next.

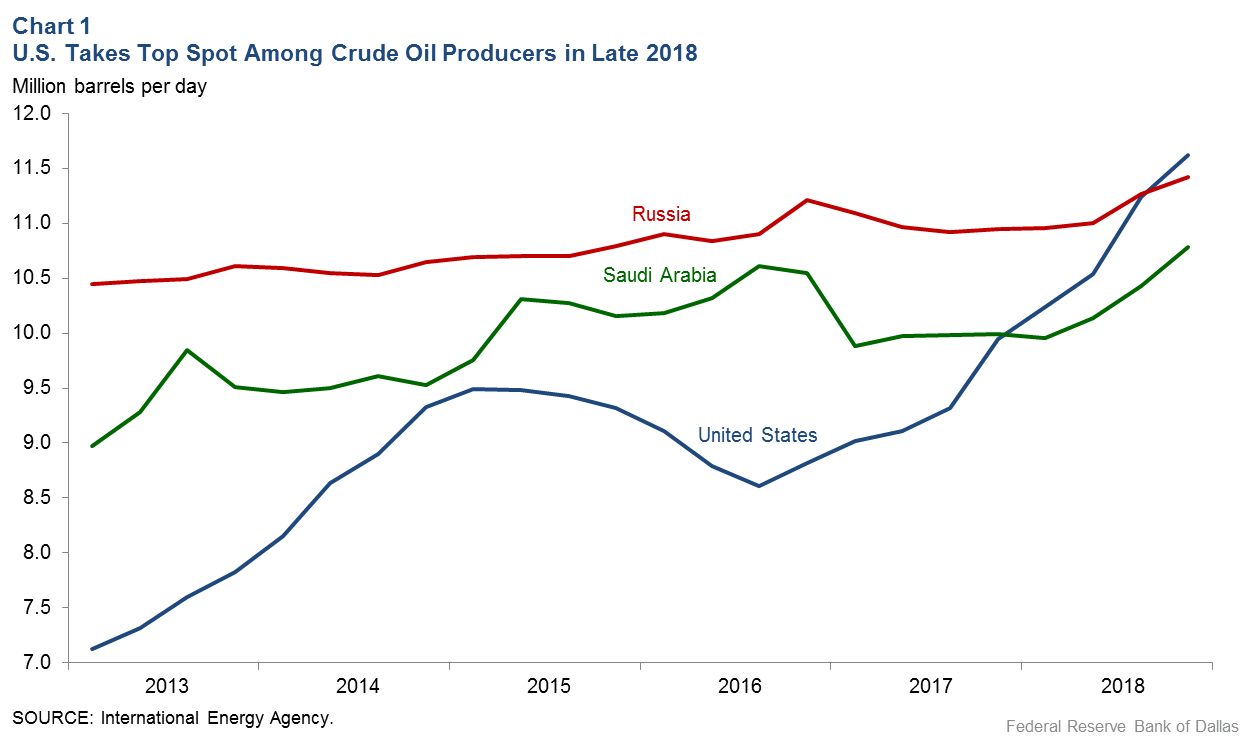

By many accounts, 2018 was a good year for the U.S. oil sector. U.S. oil production grew by 1.6 million barrels per day—a record annual increase—and by year-end, the U.S. was the world’s No. 1 crude oil producer (Chart 1).

However, volatility is a long-standing feature of the industry, a function of the ever-shifting price of oil. After exceeding $70 a barrel for a good portion of last summer, West Texas Intermediate (WTI) crude prices ended 2018 down 40 percent from those highs. While prices have recovered somewhat since then, they remain about 30 percent below the recent peak in October 2018.

A natural question is how this decline might affect the outlook for 2019, as falling oil prices lower revenue and profits for oil companies. Specifically, will firms contract and cut back on capital spending, and what could it mean for energy sector employment and regional economic growth?

Results from the recent Dallas Fed Energy Survey suggest that a dramatic contraction in activity, as occurred during the last bust, appears unlikely. While activity levels plateaued in fourth quarter 2018, and uncertainty about the outlook is up dramatically, capital spending in 2019 is likely to remain close to prior-year levels, precluding a dramatic contraction in activity.

Energy Survey provides insights on health of industry

The oil and gas industry plays an important role in the regional economy, one that has grown during the shale boom. More than half of the nation’s crude oil production comes from Texas and neighboring states, and the Gulf Coast, already home to a massive refining and petrochemical complex, has become a major export hub for crude oil and liquefied natural gas. Numerous industries, including manufacturing and hospitality, are connected either directly or indirectly to activity in the oil and gas sector.

Each quarter, the Dallas Fed Energy Survey asks 200 oil and gas companies about business conditions and the outlook for their firms. Executives assess whether overall activity and employment have increased, decreased or remained the same relative to the previous quarter. Their responses provide an indication of quarterly change and a gauge of executive sentiment regarding the outlook for the next six months.

Results from the first three quarters of 2018 signaled robust growth in activity and production, along with a healthy labor market that experienced rising employment and wages in the sector. Outlooks for firms remained positive, and uncertainty was little changed apart from a small uptick in the third quarter.

The fourth-quarter survey was open Dec. 12–20, and responses pointed to several important shifts:

- Business activity levels, which had been growing since second quarter 2016, plateaued in the fourth quarter.

- Executives were more pessimistic on the near-term outlook.

- Uncertainty skyrocketed with roughly 58 percent of executives reporting increased uncertainty, while numerous respondents’ comments referenced it.

Although the mood was markedly different, more executives reported that oil and natural gas production grew rather than declined in the fourth quarter, while firms continued to add employees on net. These will be important indicators to watch through 2019.

Special questions focus on spending outlook

We periodically ask respondents special questions, and their answers provide insight on specific issues with which their companies may be dealing. The most recent survey focused specifically on the outlook for capital spending in 2019. From these questions, we learned:

- Fifty-three percent of executives reported trimming spending plans for 2019 in response to lower oil prices.

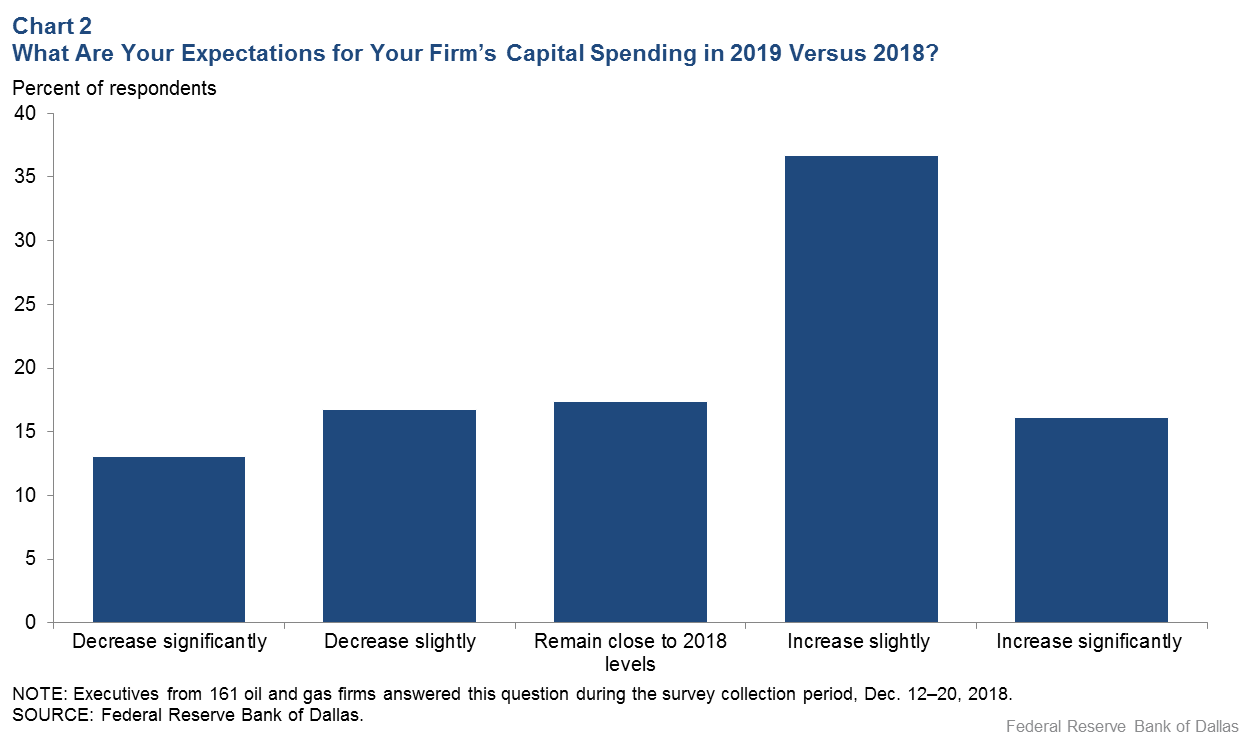

- Despite this, 70 percent of executives said that capital spending in 2019 will either be close to or above 2018 levels (Chart 2).

- Although many companies based their 2019 budgets on a conservative estimate of oil prices relative to 2018 levels, the budgets of more than half of respondents are, in fact, predicated on oil prices that exceed recent WTI spot prices, which are in the low-$50 range.

The persistence of the oil price decline will be key to how events unfold in 2019. So far, survey respondents believe that the recent drop is temporary. A significant percentage, 64 percent, expect oil to be at $60 or higher by year-end.

Obviously, if prices remain near $50 a barrel, further cutbacks could occur. Smaller firms, in particular, are likely to make more notable moves, reflecting less access to capital and greater operational flexibility.

Overall, while a bust does not seem likely this year, slower growth seems inevitable as the sector is coming off a year of sustained expansion. This will have implications for economic growth in the region, as the area has benefited from the recent production boom in the Permian Basin and the overall health of the industry, more generally. It also signals the potential for much slower growth in U.S. crude production in 2019 relative to last year.

About the Authors

Michael Plante

Plante is a senior research economist in the Research Department at the Federal Reserve Bank of Dallas.

Kunal Patel

Patel is an associate economist in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.