Corporate indebtedness: Improving financial stability monitoring

U.S. nonfinancial corporate credit—borrowings incurred by companies that aren’t financial institutions—has been identified as an area where growth in the quantity of debt and deterioration in the quality of underwriting could be a source of concern.

Financial stability monitoring involves assessing vulnerabilities on an ongoing basis and evaluating overall risks to the economy. Thus, policymakers work to develop reliable, robust metrics that identify potential cyclical risks to the financial system.

Considerable growth in credit levels relative to gross domestic product (GDP) is an indicator of increased leverage that can amplify the negative effects of an economic downturn. Most analyses focus only on a very narrow measure of debt—corporate bonds and loans—while excluding other types of nonfinancial corporate leverage. These exclusions can understate the full extent of corporate leverage.

Federal Reserve Flow of Funds data contain information on nonfinancial corporate liabilities beyond loans and bonds that provide important insight about other types of liabilities—for example, borrowings from private equity and hedge funds. Additionally, new rules covering the treatment of leases under U.S. accounting standards will likely improve the measurement of nonfinancial corporate leverage.

These additional data, taken together, suggest that the U.S. nonfinancial corporate sector is substantially more leveraged than commonly understood based on widely used “debt-to-GDP” measures.

Calculating debt-to-GDP

The Bank of International Settlements (BIS), an institution owned by the world’s principal central banks, researched financial stability metrics to detect excess credit growth following the global financial crisis a decade ago. The BIS sought measures that member countries, including the U.S., could use. It highlighted the importance of looking at trends in credit-to-GDP metrics.

The BIS produces quarterly data on credit aggregates across member countries. However, the BIS defines credit-to-GDP in terms of “debt,” specifically debt securities and loans, as these data categories are consistently available across BIS members, and econometric studies frequently draw on these underlying data.

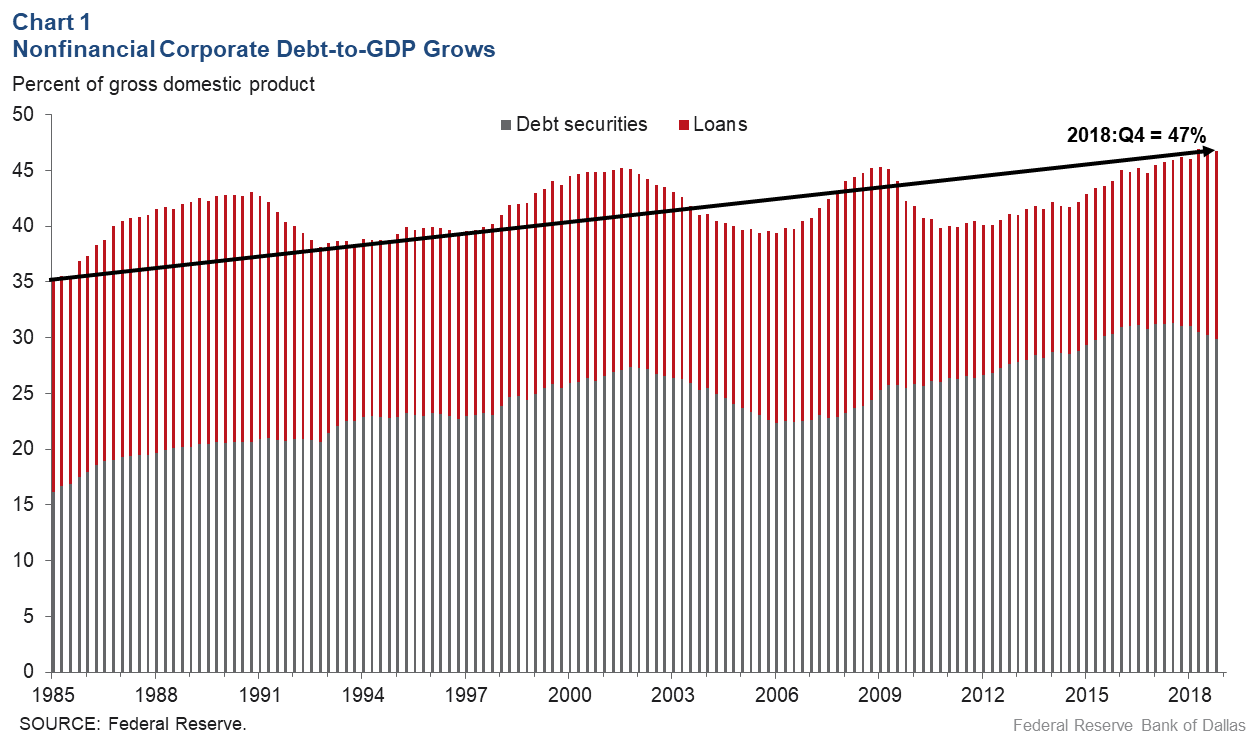

Even though there are additional data in the U.S. by virtue of the more granular nature of the Flow of Funds, potential vulnerabilities from rising corporate leverage are often monitored using this narrow measure of debt that only includes bonds and loans. Chart 1, drawing on this definition, suggests that nonfinancial corporate leverage in third quarter 2016 began exceeding prior peaks in 2008 and 2000, and that it continues to grow.

Measuring leverage more broadly

Although the BIS definition is based on loans and bonds, there is no reason to exclude other corporate liabilities that can also contribute to risk in the economy. After all, a liability is any obligation—no matter its name—that promises the return of an asset to the creditor in the future.

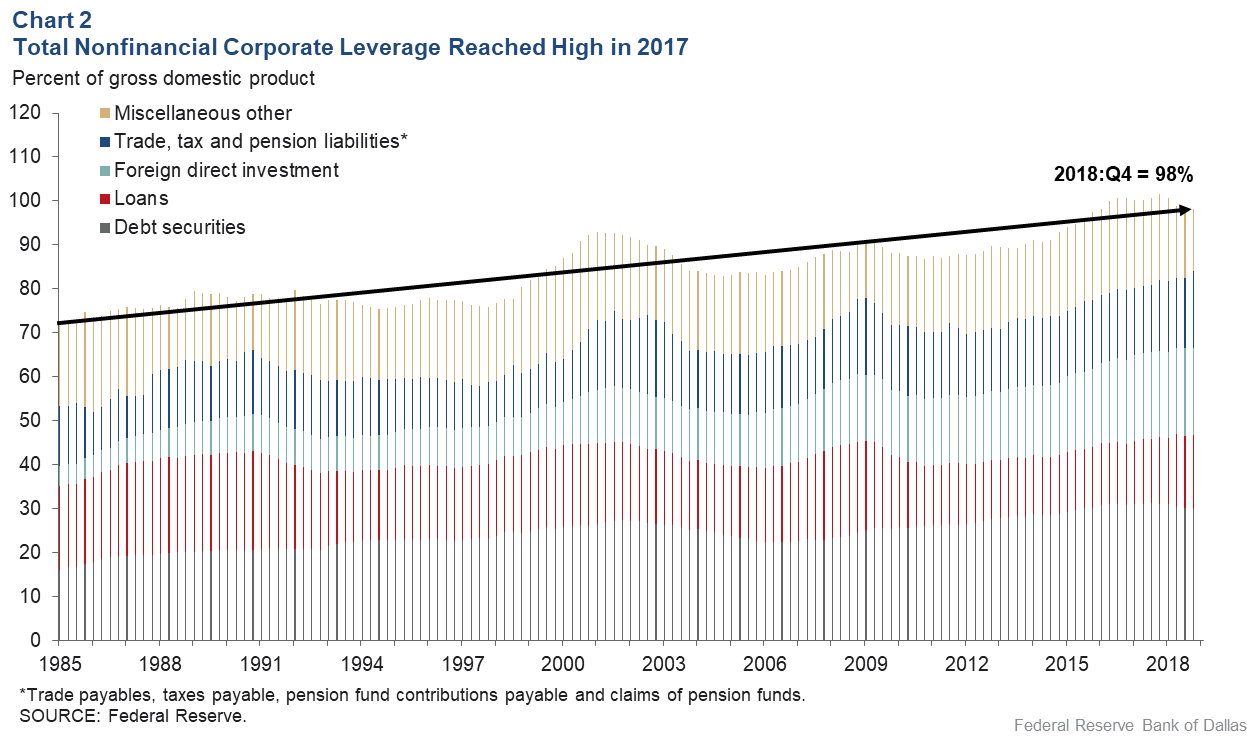

“Total Nonfinancial Corporate Liabilities” is the broadest measure of indebtedness in the Flow of Funds. In addition to nonfinancial corporations’ outstanding loans and bonds, this metric includes loans from private equity funds and hedge funds, trade finance and foreign direct investment, which sometimes has both debt and equity components.

This measure of indebtedness initially peaked at 93 percent of GDP in 2001 during the dot-com bubble and reached a new high of 102 percent at year-end 2017. It stood at approximately 98 percent in fourth quarter 2018 (Chart 2). This measure is anticipated to grow in coming quarters as new U.S. lease accounting standards are phased in.

How leverage is measured may influence policymakers’ perception of the financial system’s associated vulnerability. At 98 percent of GDP, the total liability metric as a measure of nonfinancial corporate leverage is more than double the narrow “debt” metric that consists of bonds and loans.

One key difference between the narrow and more comprehensive measures is inclusion of a residual “Miscellaneous Other Liability” category, which grew sharply after the financial crisis and peaked at $4 trillion during fourth quarter 2016.

This category includes many forms of debt that escape simple categorization, such as liabilities of nonfinancial corporations to hedge funds and private equity funds and various loan obligations bundled together in debt securities to form collateralized loan obligations (CLOs).

Contrary to what “Miscellaneous Other Liability” would indicate, this category of liabilities is far from immaterial. Presently at $3 trillion, it remains the fourth-largest category of debt for nonfinancial corporations and was the third largest as recently as fourth quarter 2017. Trends in these items are arguably of prime interest when monitoring financial stability developments.

The inclusion of these additional debt categories is demonstrably important not only because it increases the level of credit relative to GDP, but also because it alters the timing of the peaks and troughs in corporate leverage. The comprehensive measure—total liabilities—exceeded the 2001 dot-com peak in fourth quarter 2014, while the debt (loans and bonds) measure took another five quarters to signal that nonfinancial corporate leverage reached a new peak. Total liabilities-to-GDP also signaled rising vulnerabilities in the corporate sector three quarters earlier than the debt-to-GDP measure in the lead-up to the 2000–01 dot-com fallout.

If less well-understood forms of leverage can result in the emergence of financial stability vulnerabilities, it becomes particularly worthwhile to consider developments broadly and monitor all forms of debt.

Composition, quantity of leverage

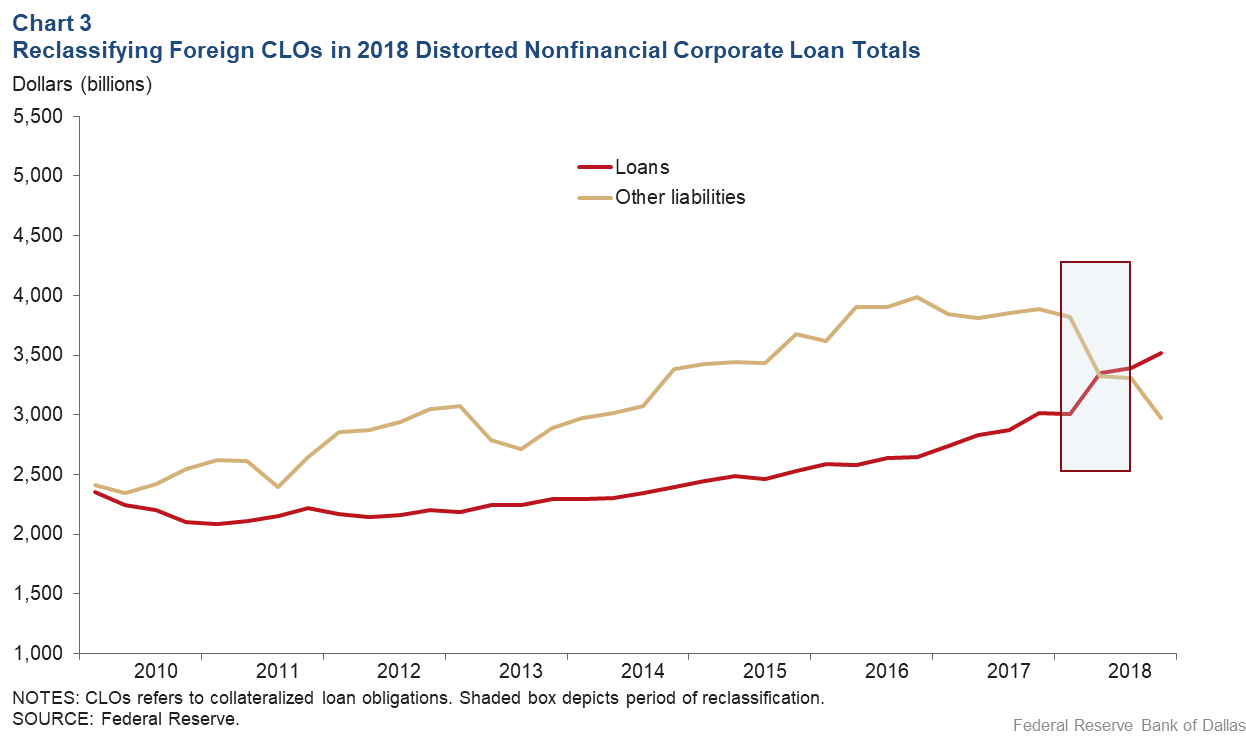

Classification of corporate liabilities matters, too. For example, a recent improvement in data quality highlights the importance of thinking of corporate debt more comprehensively. A change in the U.S. Treasury’s international capital data collection in second quarter 2018 identified CLOs domiciled abroad.

Chart 3 illustrates the effect of this change by moving these securitizations from the “Miscellaneous Other” category and into the Flow of Funds “Loan” category, making it appear that the amount of loans outstanding grew significantly. Thus, using a narrow metric as a means of assessing financial stability suffers from the problem of capturing changes involving the ability to categorize the data across different types of liabilities as opposed to capturing the underlying trend in overall sectoral leverage.

Another data quality development will likely affect Flow of Funds reporting and, by extension, the measurement of aggregate corporate indebtedness. The Financial Accounting Standards Board, which defines the guidelines for U.S. Generally Accepted Accounting Principles (GAAP), published a new set of lease accounting standards in early 2016. It requires that companies report leases on their balance sheets as liabilities. While not affecting the intrinsic level of corporate leverage, these changes in GAAP will affect the Flow of Funds’ measurement of aggregate nonfinancial corporate leverage, since historically, only bank-financed leases to nonfinancial corporations were captured. Bank-financed leases were reported in banks’ regulatory filings, while other leases were off-balance-sheet items.

This accounting change is anticipated to be quite material for U.S. corporations. For example, one private sector impact assessment finds that approximately $3 trillion in leases will be reclassified as liabilities on the balance sheets of U.S. firms. While the U.S. financial sector holds some leases, nonfinancial corporations appear to hold the bulk, which will affect reported “total liabilities” in the Flow of Funds.

Picking an early warning indicator

How leverage is measured has real-world consequences for identifying financial stability vulnerabilities, as different measures may more readily flag excesses. A broad total liability metric has many advantages in the U.S., though it hasn’t undergone the large-scale econometric studies that back the more commonly used credit-to-GDP or debt (bonds and loans) measures.

The broad measure boasts several advantages. First, it recognizes that all liabilities are, in fact, leverage. Second, it also avoids the problem of conflating data enhancements in measuring the composition of liabilities with changes in underlying trends. Finally, it captures some of the more opaque types of leverage.

These additional data, taken together, suggest that the U.S. nonfinancial corporate sector is substantially more leveraged than commonly understood based on widely used debt-to-GDP measures. With the broader total liability metric at almost 100 percent of GDP, the level of overall U.S. corporate leverage appears to be high and worthy of policymakers’ attention.

About the Authors

Jill Cetina

Cetina is a vice president in Banking Supervision at the Federal Reserve Bank of Dallas.

Alex Musatov

Musatov is a financial specialist in the Supervisory Risk and Surveillance Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.