Room to grow? Inflation and labor market slack

Compared with the usual ex-food-and-energy measure, the Dallas Fed’s Trimmed Mean PCE inflation rate sends a clearer, more reliable signal about whether cyclical inflation pressures are building.

In a previous post, we noted a couple advantages of the trimmed mean inflation rate over the more-common ex-food-and-energy measure of core inflation, namely its lower volatility and better real-time tracking of long-run headline inflation trends.

In this post—which draws on some recent research—we highlight another advantage: Real-time trimmed mean inflation has a stronger, more stable relationship with labor market slack than does ex-food-and-energy inflation. Put a little differently, trimmed mean inflation better captures the part of inflation that varies with the business cycle.

Slack and Inflation

By “slack,” we mean resources—people, plants and equipment—that are underutilized due to weak aggregate demand. Measuring slack directly is difficult in real time, so policymakers and analysts often look to the behavior of inflation to draw inferences about the slack. If, say, inflation fails to increase despite high rates of labor utilization, some observers might conclude that the sustainable unemployment rate was lower than previously believed.

For example, the Congressional Budget Office (CBO), which estimates the economy’s natural rate of unemployment (the unemployment rate at which labor market slack would be exactly zero), has in the past often revised those estimates based on the behavior of inflation.

More recently, according to the minutes of the policy-rate-setting Federal Open Market Committee’s March 2019 meeting, some FOMC participants “cited the combination of muted inflation pressures and expanding employment as a possible indication that some slack remained in the labor market.”

Inferences like these are reliable only to the extent that there is a tight empirical link between slack and the inflation measure on which policymakers and analysts are focused. If the inflation measure includes a large amount of variation unrelated to slack, policymakers risk drawing the wrong conclusions—inferring a need for accommodation when underlying cyclical inflation pressures are actually building, or a need for policy restraint when underlying cyclical pressures are waning.

The trimmed mean certainly filters out more noise than the usual ex-food-and-energy inflation measure. As we’ll show, it also succeeds in better reflecting, in real time, the economy’s cyclical position.

Our Approach

We want to assess the strength and robustness of the relationship between early-release estimates of our inflation measures—the estimates policymakers have in hand as they deliberate—and labor market slack. We look at latest-vintage estimates of slack since these are presumably more accurate than earlier vintages.

In particular, we use the latest-vintage estimates of the natural rate of unemployment from the CBO and measure slack as the gap between actual unemployment and its natural rate. (Importantly for our analysis, the CBO does not revise its natural-rate estimates based on the behavior of trimmed mean inflation. We are not “cooking the books” by using a measure of slack specifically designed to explain trimmed mean inflation.)

Trimmed mean, ex-food-and-energy and headline inflation all drifted downward during the 1980s and early 1990s as the public gained confidence in the Federal Reserve’s commitment to long-run price stability. To control for that drift, we de-trended each of these series using a survey measure of long-run inflation expectations from the Philadelphia Fed’s Survey of Professional Forecasters (SPF).

Next, we regressed de-trended early-release inflation estimates on latest-vintage estimates of the unemployment gap (lagged four quarters), plus a constant term. This framework is consistent with a wide variety of macroeconomic models that see inflation as depending on expected inflation and slack. It is simple enough to be useful to policymakers as they try to explain their thinking and their actions.

We ran these regressions over three sample periods, one beginning in 2005 (the earliest we have real-time trimmed mean data), one beginning in 1996 (the earliest we have real-time ex-food-and-energy data) and a longer sample beginning in 1981.

Trimmed Mean Dominates

We find that deviations of trimmed mean inflation from long-run expected inflation are more strongly and more reliably related to labor market slack than are deviations of ex-food-and-energy inflation from long-run expected inflation.

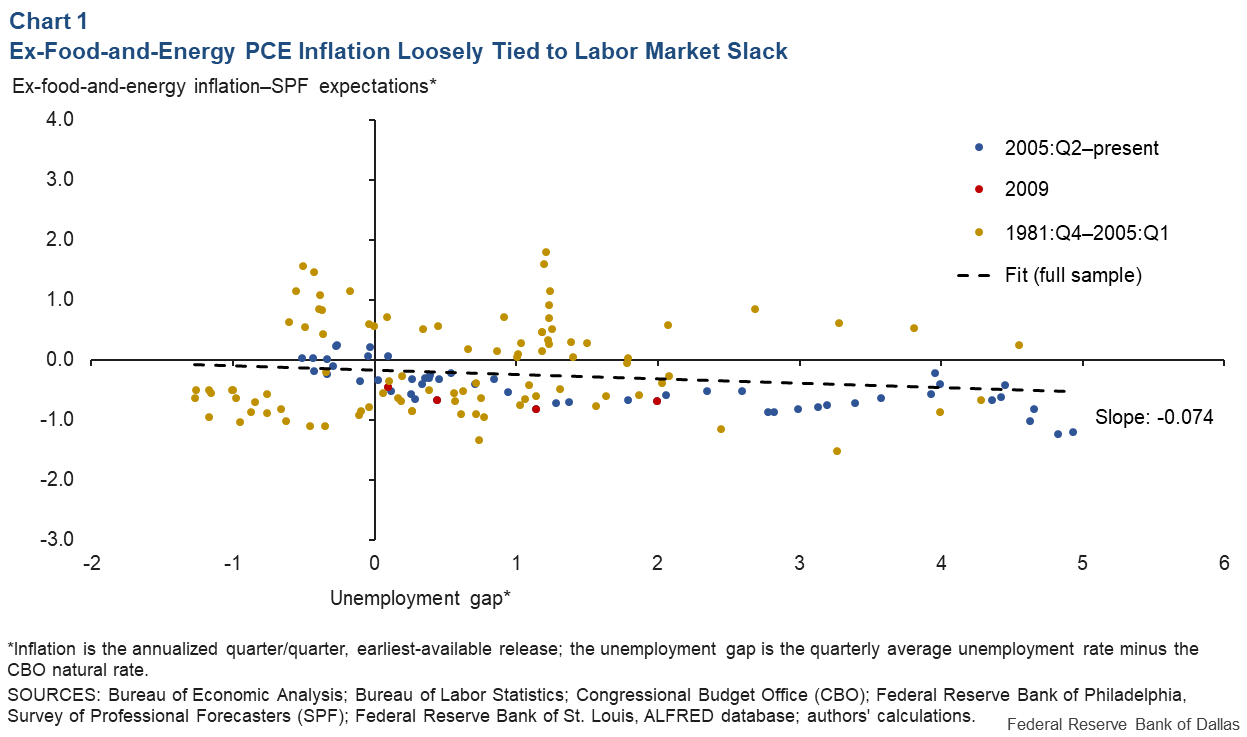

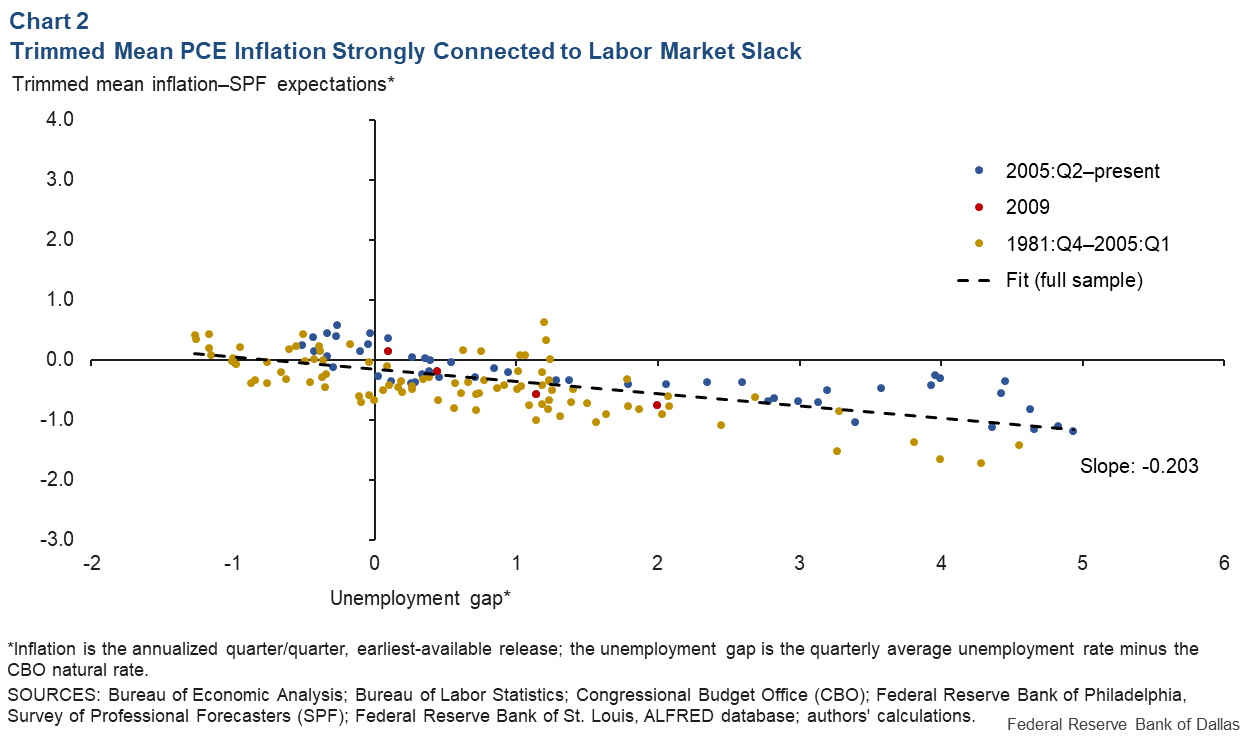

The coefficient measuring the impact of the unemployment gap on inflation is larger in magnitude in the trimmed mean regressions and is highly statistically significant. There is also no evidence that the relationship between trimmed mean inflation and the unemployment gap has deteriorated over time. A 100-basis-point decline in the unemployment gap implies a roughly 20-basis-point increase in de-trended trimmed mean inflation in all three samples.

In contrast, the relationship between the unemployment gap and ex-food-and-energy inflation is typically smaller, and is statistically significant in only one of the three sample periods (the one beginning in 2005).

Charts 1 and 2 tell the story. The charts show the relationship between the lagged unemployment gap (horizontal axis) and deviations of early-release inflation from SPF longer-run expectations (vertical axis).

The relationship between trimmed mean inflation and labor market slack (Chart 2) is clearly both stronger and tighter than that between ex-food-and-energy inflation and slack (Chart 1). The trimmed mean relationship is stable over time and seems to hold up well even during the financial crisis in 2009.

A Superior Policy Tool

Putting these results together with those described in our previous post, we conclude that trimmed mean inflation shares a long-run trend with headline inflation and, compared with ex-food-and-energy inflation, provides a better real-time signal of cyclical inflation pressures.

These features make trimmed mean inflation a more useful tool for drawing inferences about slack and, we would argue, for formulating and communicating Federal Reserve policy decisions.

About the Authors

Jim Dolmas

Dolmas is a senior economist and policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

Evan F. Koenig

Koenig is a senior vice president and principal policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.