As wages rise, are black workers seeing the smallest gains?

A recent Wall Street Journal article argued that black workers have received the smallest earnings gains among various race/ethnic groups since the beginning of the Great Recession. Our analysis suggests otherwise. When individuals entering and leaving the workforce are excluded, we find that black workers are seeing the same earnings gains as white (non-Hispanic) workers.

In the Wall Street Journal article, “As Wages Rise, Black Workers See the Smallest Gains,” Eric Morath and Soo Oh compare inflation-adjusted average weekly earnings, also known as real average weekly earnings, for workers in different race/ethnic groups since the beginning of the recession.

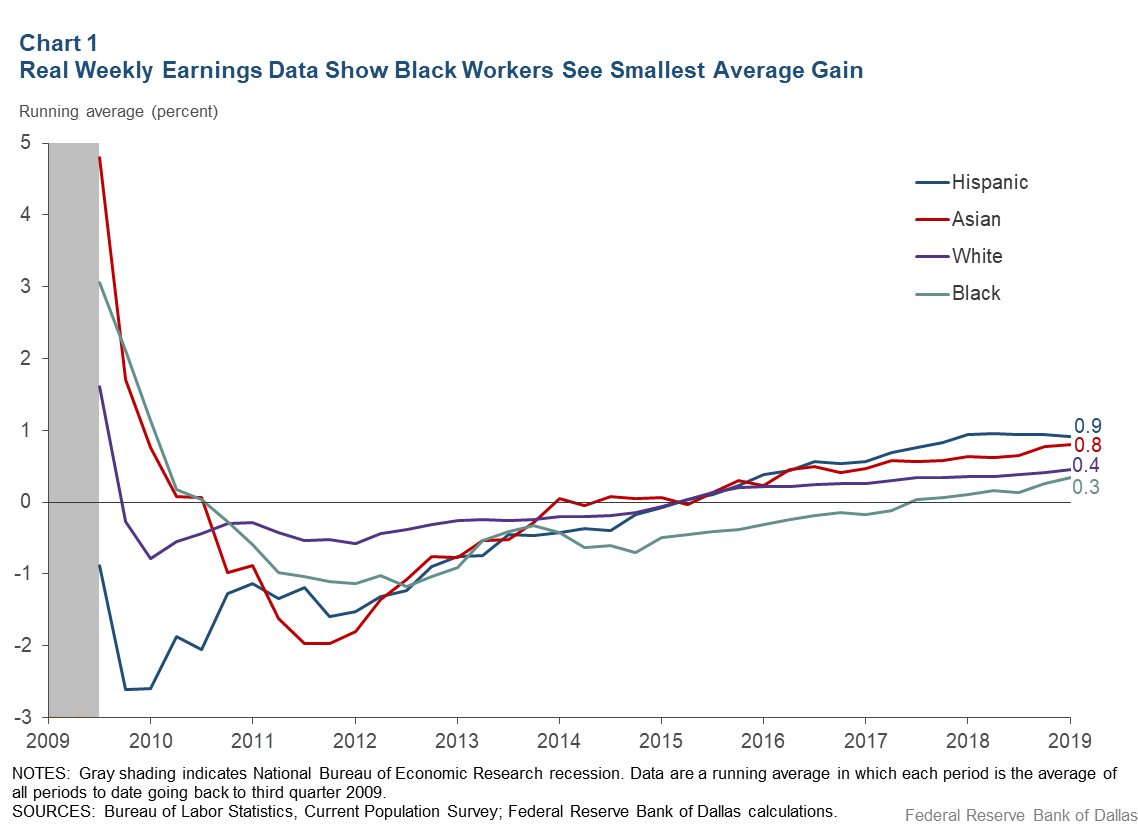

To focus on the relative benefits from the economic expansion, we change the reference point to the end of the recession. We also focus on the running average rather than the cumulative change for each group—that is, we recalculate the average every time we add an observation. The qualitative picture is the same as in the Wall Street Journal article, with an identical ordering across four groups—Hispanic, Asian, white and black (Chart 1).

Black workers experienced the lowest overall running average growth rate of 0.3 percent, 0.1 percentage point lower than that for whites.

Assessing composition effects

Importantly, the calculation of weekly earnings growth for a group is more than an expression of increases in wages and in hours experienced by individual group members working over the period (“stayers”). The calculation also reflects the number and weekly earnings of individuals from that group who enter the workforce (“entrants”) and who exit the workforce (“exiters”) over the period.

If entrants tend to have lower weekly earnings than stayers, entrants will act to lower the growth of average weekly earnings for that group. Similarly, if exiters tend to have higher weekly earnings than stayers, exiters will also act to lower the growth of average weekly earnings for that group. Moreover, this labor turnover effect can mask the underlying weekly earnings growth of the stayers that, we argue, offers a better basis to evaluate the gains of a particular group.

We can illustrate both of these points using a simple example. Assume that a group we want to follow has three individuals: Mary, Bob and Frank. Mary and Bob both work 40 hours per week and are employed in 2017 and 2018. In 2017, Mary receives a wage of $20 per hour and Bob a wage of $10 per hour. In 2017, Frank is unemployed. The group’s average weekly earnings in 2017 are $600.

In 2018, both Mary and Bob get a 10 percent wage increase. In addition, Frank becomes employed at a job paying $10 per hour for 40 hours per week. Because Frank entered employment with weekly earnings below the average for Mary and Bob, their average weekly earnings in 2018 fall to $573. Consequently, average weekly earnings decline by 4.5 percent. Here is a depiction of this simple example:

| 2017 | 2018 | ||||

| Wage (dollars/hour) |

Weekly earnings (dollars) |

Wage (dollars/hour) |

Weekly earnings (dollars) |

||

| Mary | 20 | 800 | 22 | 880 | |

| Bob | 10 | 400 | 11 | 440 | |

| Frank | — | — | 10 | 400 | |

| Average weekly earnings | 600 | 573 | |||

If Frank had not entered employment, average weekly earnings for the group would have increased to $660, matching the 10 percent wage increases Mary and Bob received. Similarly, exits from the workforce can also impact the growth in average weekly wages. For example, if Mary retired at the end of 2017, average weekly earnings would have fallen to $420.

The impact of entry and exit from the workforce as illustrated in this simple example is called a “composition effect” because it captures the variation in a labor market outcome—average weekly earnings in this example—resulting from changes in the composition of the workforce. The composition effect is magnified in periods where the number of individuals entering the workforce is high. This is what we would expect during an expansion following a severe recession.

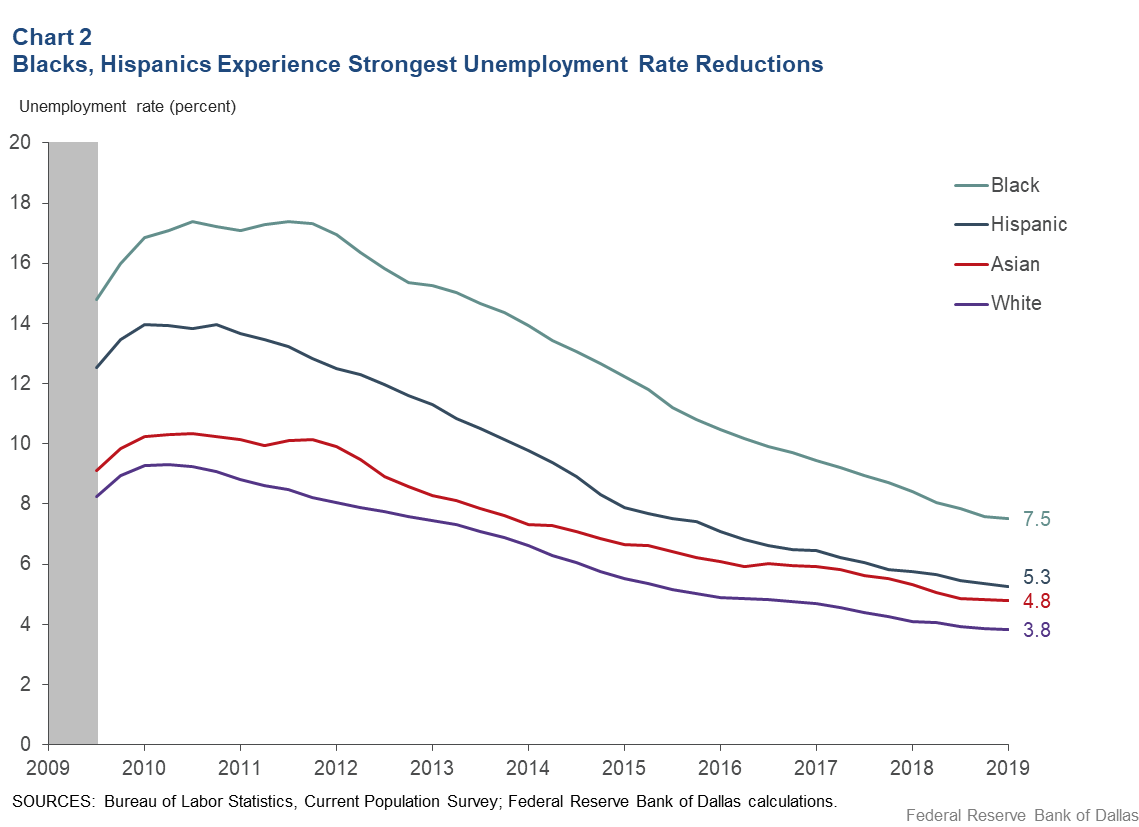

We would also expect the composition effect to differ between groups depending on the relative magnitude of the unemployment experienced during the recession and, therefore, the subsequent re-employment in the expansion. Black workers experienced the largest declines in unemployment over this expansion, suggesting that composition effects may play an especially important role for the group (Chart 2).

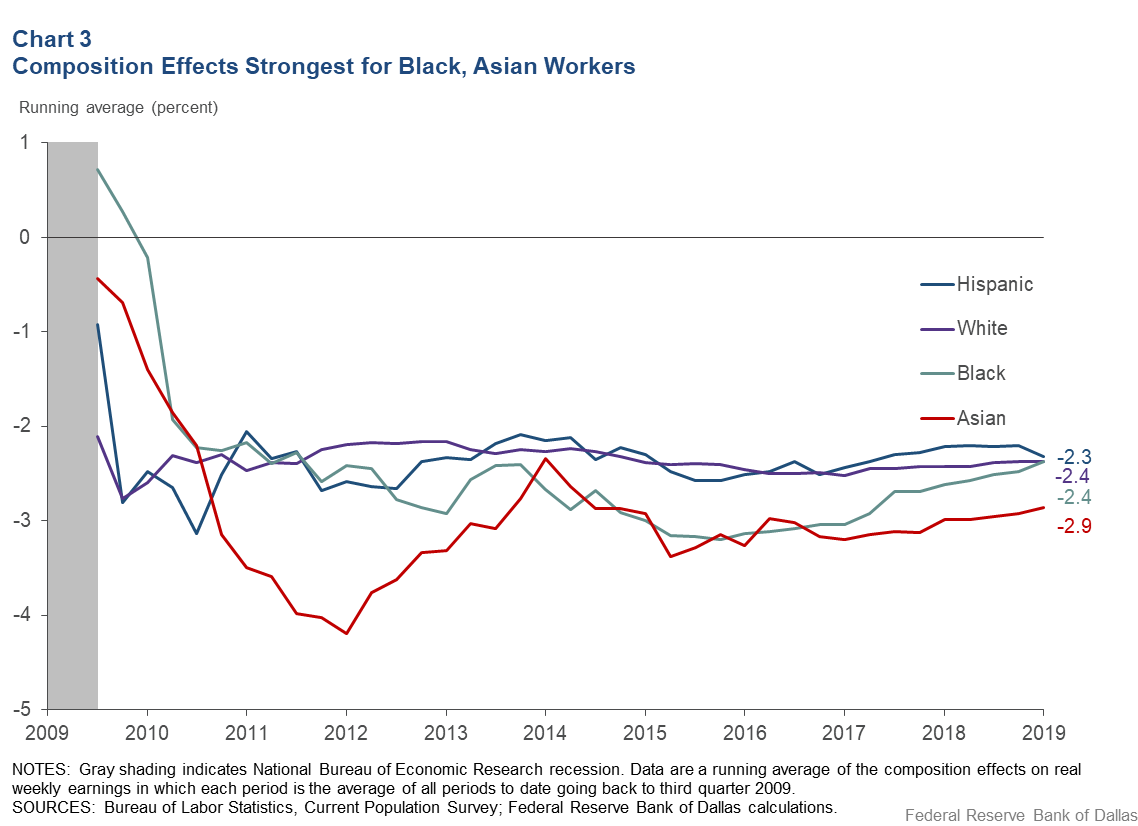

Chart 3 illustrates our estimated composition effects for the four groups and is the product of a statistical procedure that allows us to take a closer look at changes since the end of the Great Recession. Over this period, the composition effects have restrained the growth of average weekly earnings for all four groups. For much of the expansion, the composition effects for Asian and black workers have exerted stronger downward pressure on the growth of average weekly wages for their groups. The running averages of the composition effects have converged recently for all groups except for the Asian group.

Earnings during an expansion

To understand the earnings benefits that a group is receiving over the expansion, our earlier simple example shows we should exclude the impact of individuals entering and exiting the workforce. A strong economy that draws individuals back into the workforce is a benefit, even if the earnings of these entrants act to reduce the growth of average weekly earnings for their group as a whole.

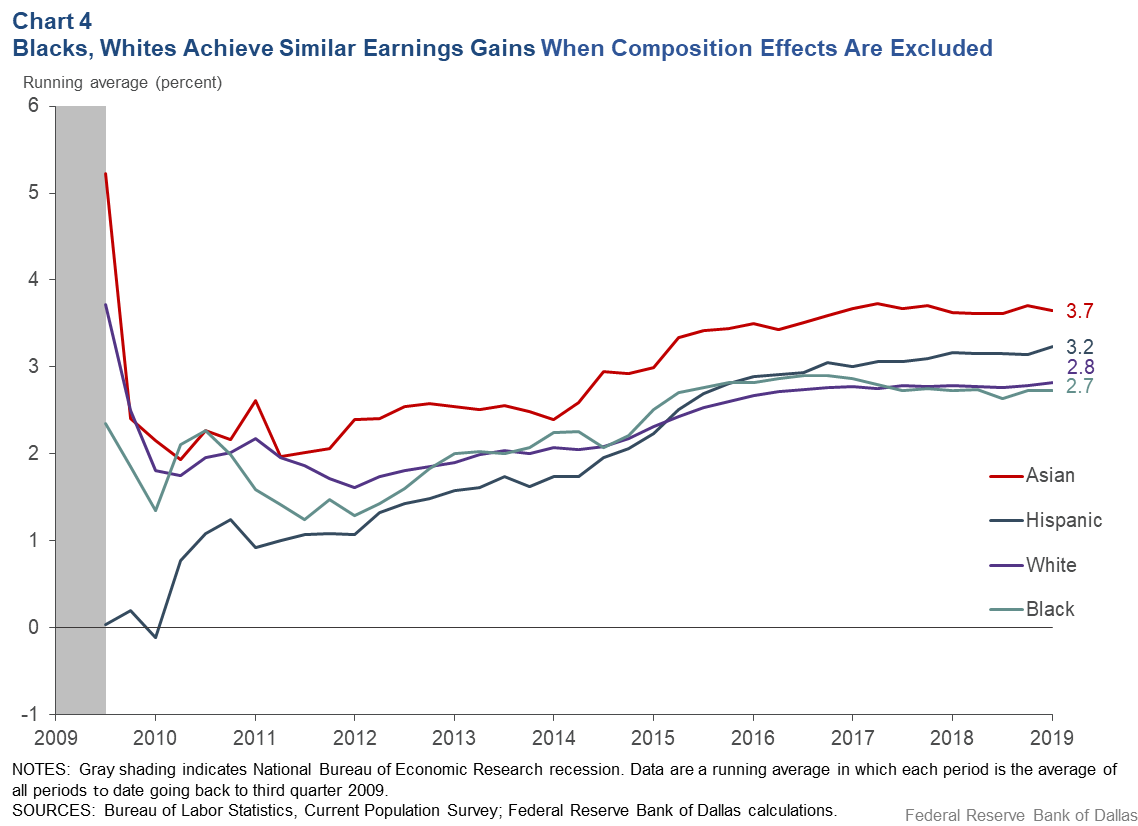

Chart 4 shows the running average real weekly earnings growth for each group, excluding the estimated composition effects. Movements in the series reflect only average real wage growth and growth in hours for each group.

Removing the composition effects has an important impact on the relative real earnings growth between groups. In contrast with Chart 1, black workers caught up with white workers in 2013 and slightly outpaced them until mid-2017. Hispanics lagged the other three groups for most of the expansion and caught up in 2016. Currently, Asians and Hispanics are experiencing the strongest running average growth in real average weekly earnings.

Increasing wages among groups

In our earlier simple example, notice that there was also a difference between the average wage growth (10 percent looking at Mary and Bob) and the growth in average weekly earnings (-4.5 percent looking at all three workers).

This suggests that another way to look at how different groups of workers have benefited from the expansion is to look at real wage growth rather than real weekly earnings growth. We start with the same data on real average weekly earnings used in Chart 1 but, instead, compute individual real wage growth for workers in these same race/ethnic groups.

Specifically, for each worker, we compute the percent change in their real wage over a 12-month period (for example, from January 2018 to January 2019) and average these individual real wage gains across the workers in each group. We then compute the running average real wage growth for workers in each group.

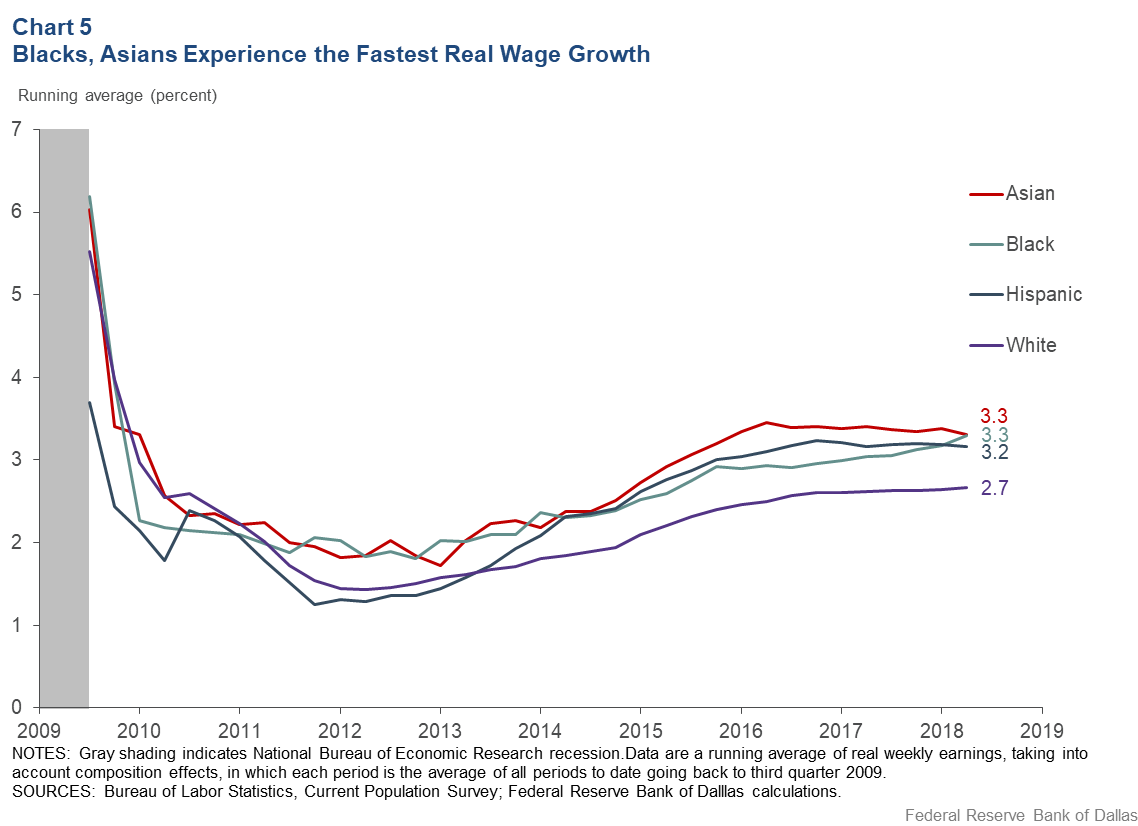

As shown in Chart 5, a very different picture emerges. Recall that Chart 1 showed black workers had experienced the smallest running average gain in real average weekly earnings. However, data for the most recent 12-month period indicate that Asians and blacks saw the highest average real wage growth, 3.3 percent. Since 2014, whites have received the lowest running average real wage growth, with a current value of 2.7 percent.

Greater wage growth parity

In comparing average weekly earnings growth between different groups, it is important to be aware of how composition effects can affect measured growth rates. We argue that composition effects should be excluded when considering how different groups have benefited during the expansion.

When such an exclusion occurs, it appears that since the recession, black workers have seen the same weekly earnings gains as white workers, while Hispanic workers have experienced even stronger earnings growth. In terms of real wages, Asians and blacks have achieved the highest growth rates.

About the Authors

Michael Morris

Morris is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Robert Rich

Rich is a senior economic and policy advisor in the Research Department at the Federal Reserve Bank of Cleveland.

Joseph Tracy

Tracy is executive vice president and senior advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.