Oil and gas sector increasingly influences U.S. business fixed investment

With U.S. oil production more than doubling over the past decade, the upstream oil and gas sector—essentially exploration, production and oilfield services—has become a more important part of business investment in equipment and structures. Capital deployment in the sector boosted growth in nonresidential fixed investment during 2017 and the first half of 2018.

However, since then, oil prices have declined about 15 percent, with oil and gas firms cutting capital expenditures and becoming a drag on fixed investment growth. This suggests that some economic gains from lower oil prices for consumers might be offset by a less-robust investment environment in the oil and gas sector.

Rising oil production

U.S. crude oil output increased from about 5 million barrels per day (mb/d) in 2008 to about 12 mb/d in 2019, reflecting output brought to market because of technological improvements such as horizontal drilling and hydraulic fracturing. The share of the upstream oil and gas sector in the level of U.S. nonresidential fixed investment doubled from 3.4 percent in the decade before the shale oil boom to an average of 6.4 percent since 2008.

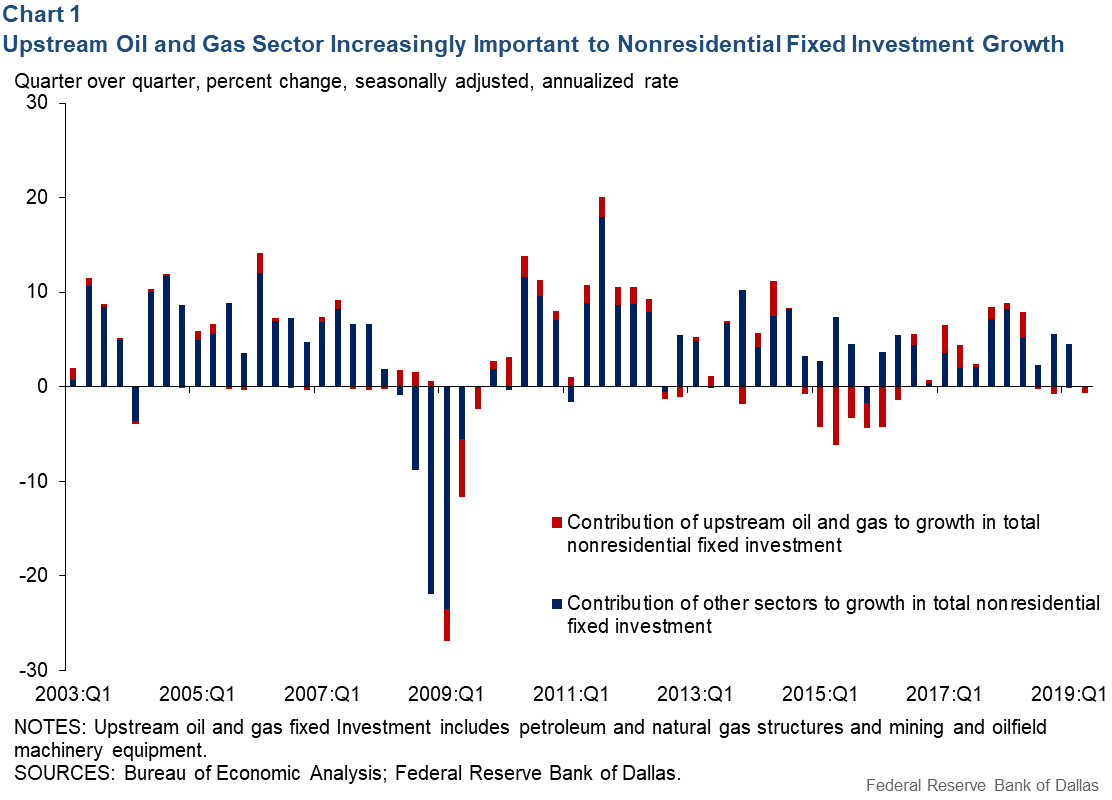

The oil and gas sector’s contribution to quarter-over-quarter fixed investment growth is also increasingly pronounced relative to other sectors of the economy since 2008 (Chart 1). While contributing positively to investment growth most of the time, upstream oil and gas became a drag from roughly 2014 to 2016 when oil prices fell about 50 percent.

In second quarter 2018, total nonresidential fixed investment grew 7.9 percent. Upstream oil and gas contributed strongly—about 2.7 percentage points—to this increase, while other sectors accounted for about 5.1 percentage points.

The situation has since reversed; the oil and gas sector has significantly contributed to a downturn in business fixed investment. In second quarter 2019, total nonresidential fixed investment contracted 0.6 percent, with upstream oil and gas investment accounting for virtually the entire decline. Put another way, absent the oil and gas sector, fixed investment would have been little changed rather than negative.

Outlook, prices pressure investment

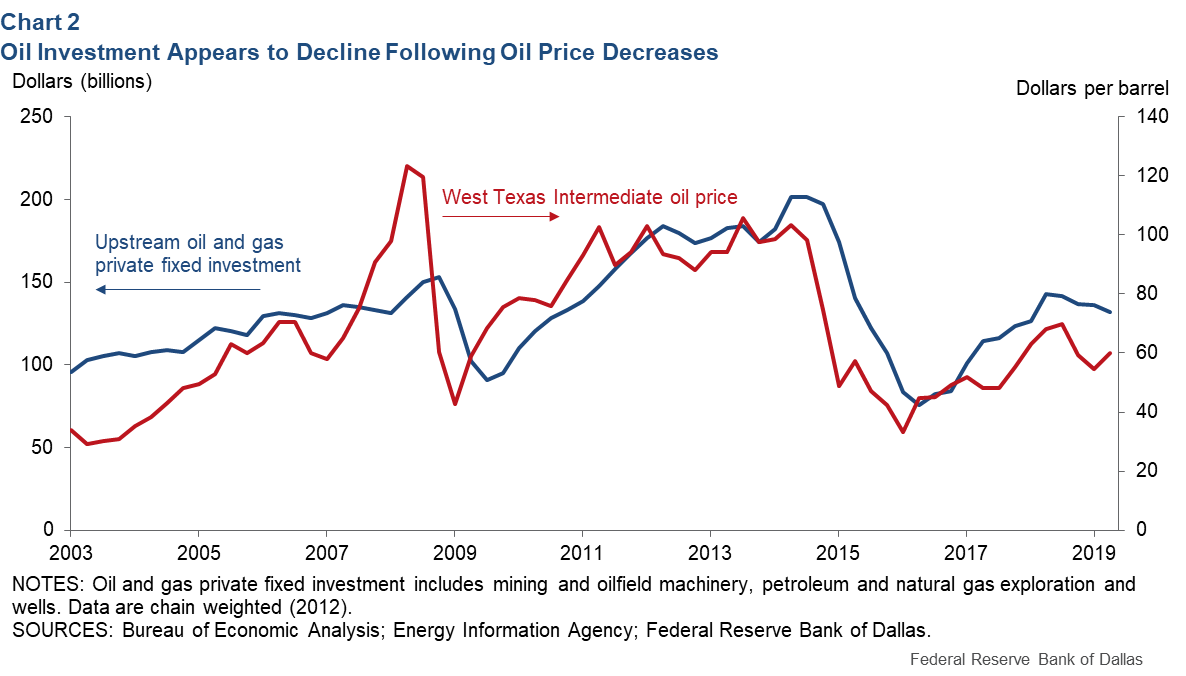

Oil and gas investment is quite volatile as its movements closely track oil prices (Chart 2). Oil and gas investment declined as oil prices slipped about 15 percent in the second half of 2018. The second quarter Dallas Fed Energy Survey of about 200 energy firms headquartered in the region pointed to greater pessimism about future business conditions. It indicated that substantially more companies responded that their outlook had worsened rather than improved during the quarter. This coincided with 58 percent of respondents saying uncertainty rose. If oil prices fail to recover, we should expect a continued drag from the oil and gas sector on business investment.

The increased contribution of oil and gas investment relative to total nonresidential investment also aids evaluation of the effect of oil price changes on the U.S. economy, research has found. While U.S. consumers tend to increase consumption in response to declining oil prices, the negative impact of declining oil and gas investment partly offsets these gains.

The exact extent of oil prices’ effects on investment remains unclear. Breakeven prices—the price that producers need to profitably drill new wells—play a role and likely produce a nonlinear relationship between oil prices and investment. For example, with average breakevens of around $50 per barrel across the U.S., a $10 oil price decline from $55 to $45 might have a much larger effect on investment than a $10 decline from $85 to $75.

It is also important to look at the underlying shocks driving oil prices. If prices fall because of an unexpected downturn in the global economy, the slowdown could simultaneously influence investment in oil and gas as well as in other sectors.

Overall, the oil and gas sector has become more important to swings in nonresidential fixed investment. A damping effect on total investment is likely in the presence of persistent oil price declines. This will likely partially offset the positive effects of lower oil prices on consumers.

About the Authors

Karel Mertens

Mertens is a senior economic policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

Grant Strickler

Strickler is a former research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Martin Stuermer

Stuermer is a senior research economist in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.