Labor market slack disappeared by 2016

An important benchmark that policymakers consider when assessing current and future economic conditions is the rate of unemployment that would prevail in a “neutral” labor market—one absent all movement during a business cycle. This is known as the “natural rate” of unemployment.

The natural rate is not constant. It gradually changes, owing to demographic and other factors and isn’t directly observable. We previously described how, using data from the Current Population Survey (CPS) for 35 million U.S. individuals age 16 and older, we developed 360 separate cohort life-cycle unemployment rate profiles for the period 1976 to 2018. These profiles represent the expected unemployment rates in a neutral labor market for members of a cohort at each age.

In this article, we combine these profiles to create an aggregate natural rate of unemployment series. It is possible to examine the extent to which various factors have contributed to a lower natural rate of unemployment over the past 40 years. Moreover, the difference between a cohort-based natural unemployment rate and the actual jobless rate suggests that the current economic expansion eliminated labor market slack stemming from the Great Recession by mid-2015. Since then, the labor market has become increasingly tight.

Building an aggregate natural rate

For each month, individuals participating in the labor market (either working or actively looking for a job) are selected from the data. Each individual is a member of a specific cohort—for example, white females with a high school education, born in the 1960s.

Based on the individual’s cohort and age, each is assigned the relevant predicted neutral labor market unemployment rate. This assessment is derived from the estimated life-cycle unemployment rate profile for the cohort.

Because the same period will correspond to different ages in different cohorts (a 40-year-old born in 1955 in the 1950–59 cohort, and a 20-year-old born in 1975 in the 1970–79 cohort), we then average the predicted unemployment rates of all selected individuals in the same month to obtain the estimate of the natural rate of unemployment for the month. We repeat this procedure for all months in the dataset to derive the natural rate of unemployment series.

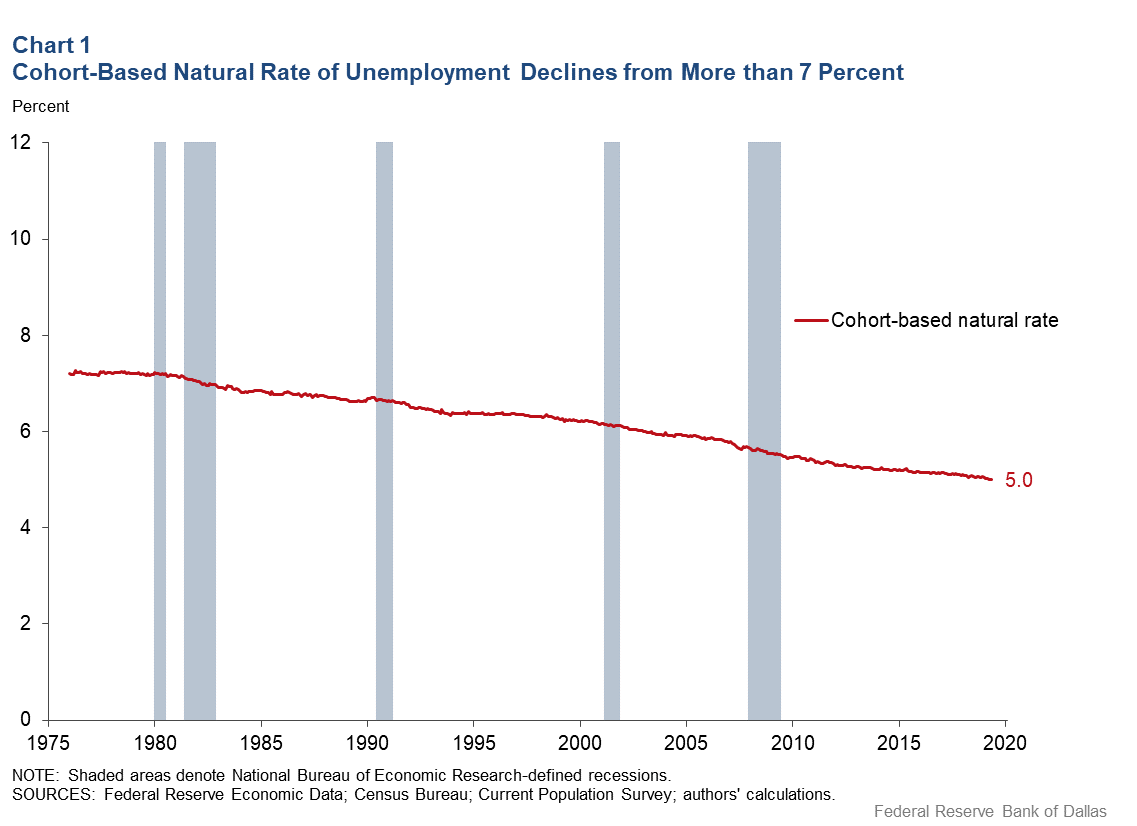

Chart 1 shows the cohort-based natural rate of unemployment from 1976 to 2017. It exceeded 7 percent in the mid-1970s. Over the next 40 years, demographic and other factors have acted to reduce the natural rate of unemployment by more than 2 percentage points.

From the mid-1970s to the mid-1990s, this decline was fairly steady, lowering the natural rate by roughly 0.05 percentage point per year. Over the next 10 years, the estimated natural rate of unemployment was relatively constant. It resumed its decline, but at a slower pace, in the mid-2000s. Our current cohort-based estimate of the natural rate of unemployment is 5 percent.

Comparing the CBO natural rate

This estimate differs from the Congressional Budget Office’s (CBO’s) natural rate series. The main methodological dissimilarity between the two series is that the CBO constructs its natural rate by carefully examining the cohort of married men, and then extrapolating the natural rate for married men to the rest of the cohorts.

In contrast to the CBO approach, our method not only has a much higher number of cohorts (360 as compared to 28), but also allows the life-cycle unemployment profile for every individual cohort to vary independently. This captures more variation across time.

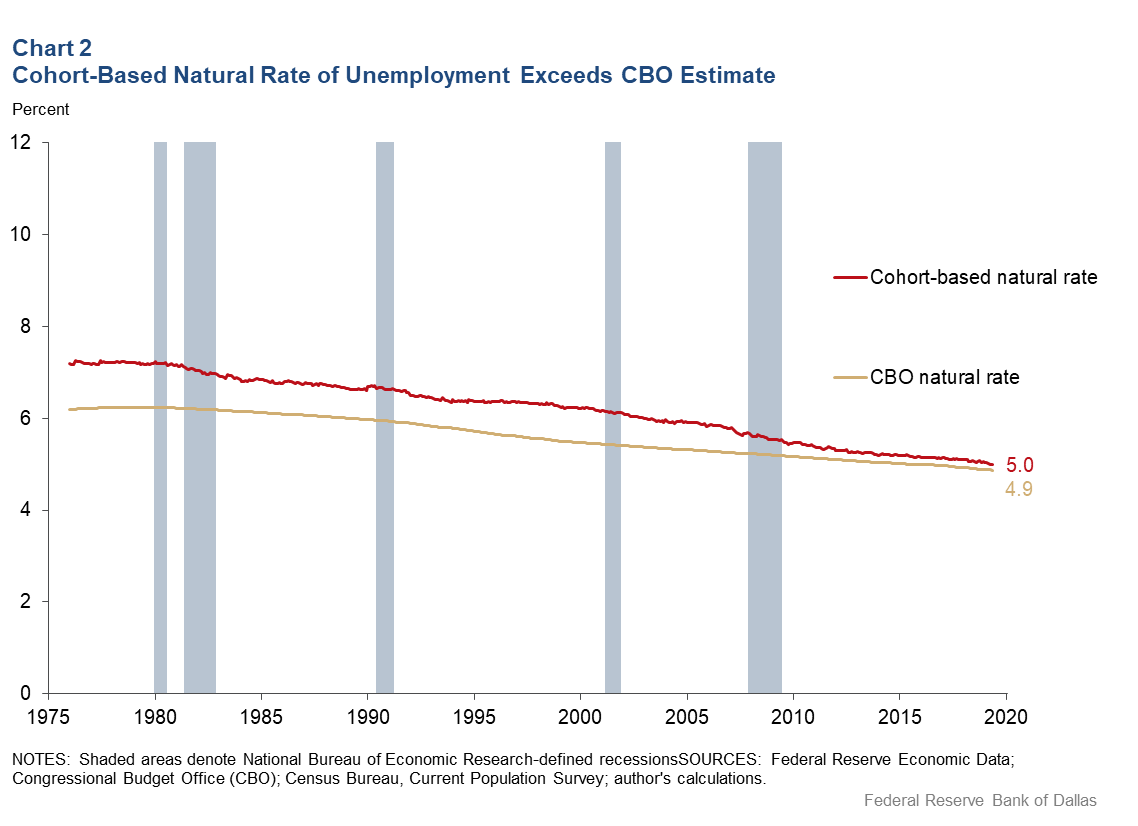

Several important differences become apparent in a depiction of the CBO and the cohort-based natural rate of unemployment series (Chart 2). The cohort-based rate is always higher than the CBO estimate. In 1976, the difference between the two estimates is a full percentage point.

The gap between the two has been narrowing since. The CBO’s natural rate is relatively constant in the late-’70s and early-’80s, while the cohort-based natural rate declines rapidly. In contrast, the CBO rate declines in the late-1990s when the cohort-based rate is relatively constant. The CBO’s current estimate at 4.9 percent is below the 5 percent cohort-based estimate.

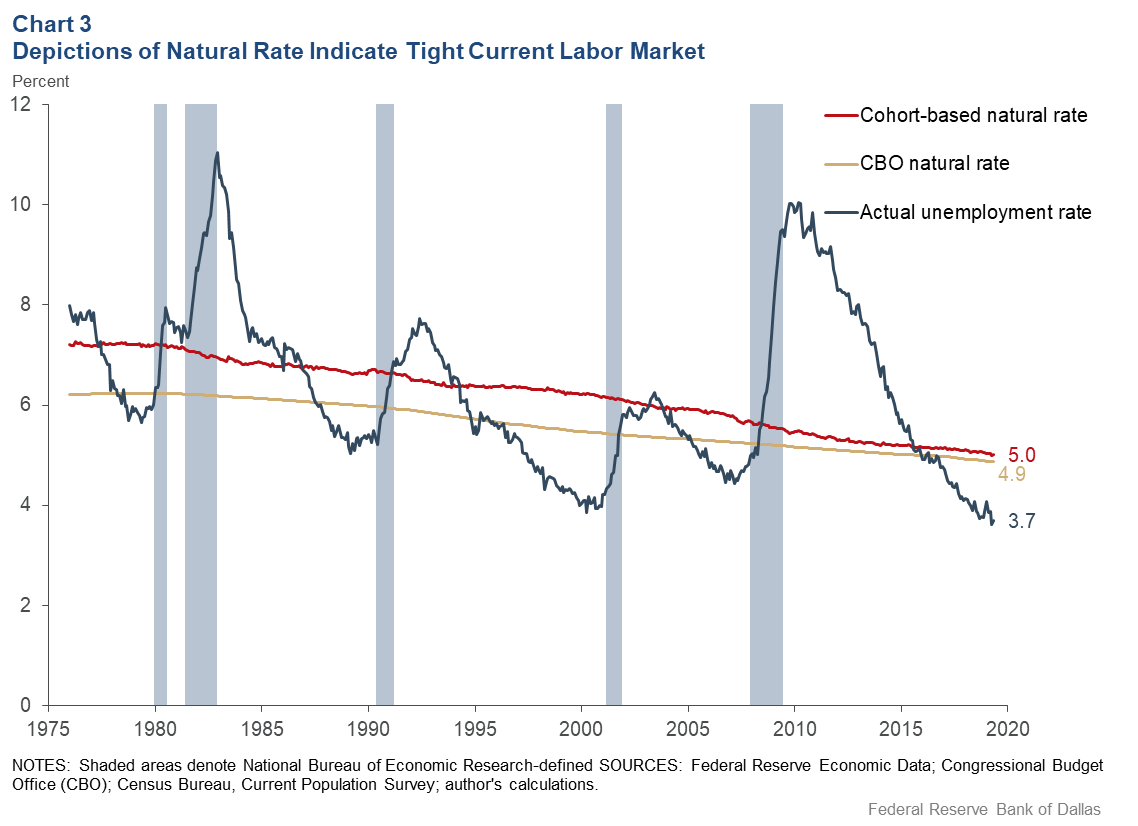

To gauge labor market conditions, we compare the actual unemployment rate to the natural rate (Chart 3). When the actual unemployment rate exceeds the natural unemployment rate—there is “slack” in the labor market. In contrast, when the actual unemployment rate is below the natural rate of unemployment, conditions in the labor market are “tight.” Both natural rate series indicate that the current labor market is tight.

Assessing labor market tightness, slack

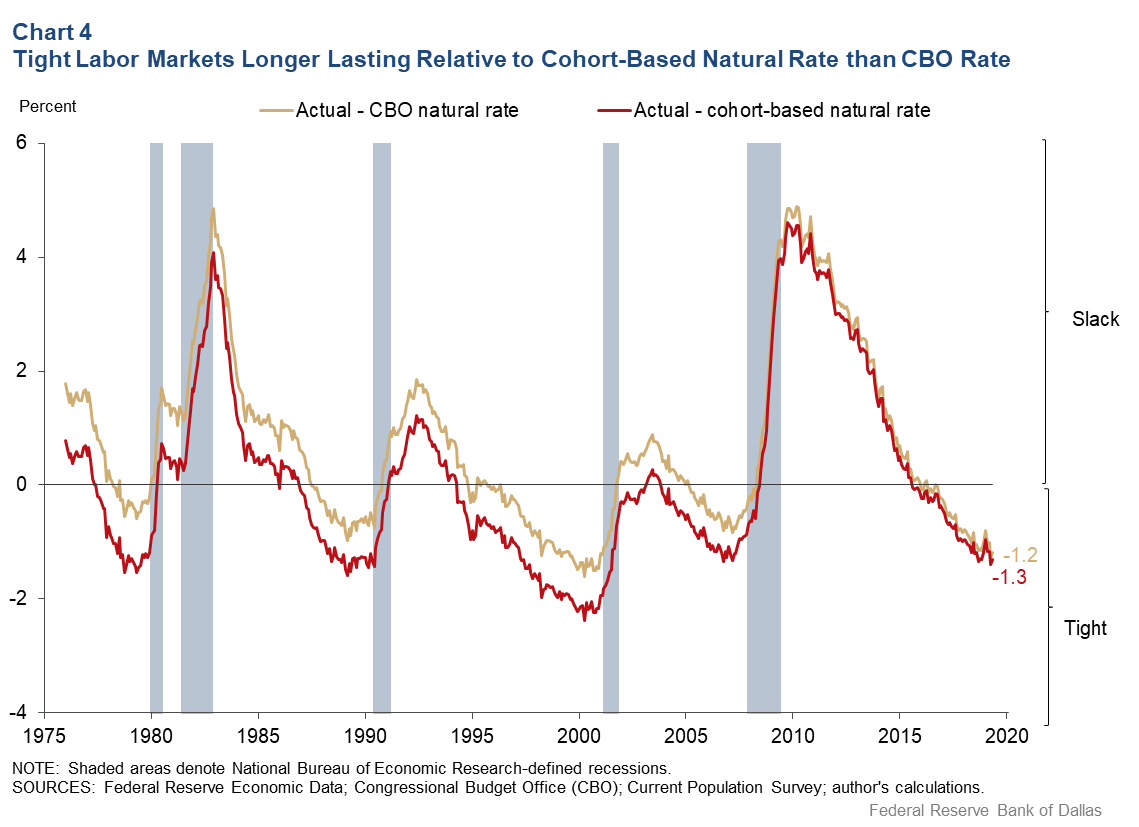

Information about the relationship between the unemployment rate and the natural rate can be summarized by the “unemployment gap”—the difference between the unemployment rate and the estimated natural rate of unemployment.

Comparing the CBO unemployment gap to the cohort-based measure, the CBO unemployment gap suggests that the labor market is more likely to have slack than be tight—and, when it is tight, this condition does not last long (Chart 4). By comparison, the cohort-based unemployment gap indicates relatively more balance over time between slack and tight labor market conditions.

Additionally, the cohort-based natural rate of unemployment measure underlying our unemployment gap estimate indicates that tight labor markets tend to begin earlier and last longer than the CBO measure suggests. In particular, the cohort-based unemployment gap indicates that the current economic expansion eliminated labor market slack stemming from the Great Recession by mid-2015—nearly a year earlier than the CBO measure shows.

About the Authors

Michael Morris

Morris is a former research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Robert Rich

Rich is a senior economic and policy advisor in the Research Department at the Federal Reserve Bank of Cleveland.

Joseph Tracy

Tracy is executive vice president and senior advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.