How falling oil prices in early 2020 weakened the U.S. economy

The benchmark West Texas Intermediate (WTI) price of oil dropped by more than half from Jan. 21 to April 3. There is a long tradition of economists arguing that lower oil prices, all else equal, are good for the United States economy. Thus, one might have expected this dramatic price cut to have been a much-needed piece of welcome news.

Indeed, President Trump tweeted that the oil price drop “is good for the consumer” on March 9. The Wall Street Journal echoed this sentiment, calling low oil prices “a gift to U.S. consumers” on April 2. This view would have seemed reasonable just a few years ago, but it is no longer accurate today.

Instead, we will show that on balance this oil price decline has weakened rather than strengthened the U.S. economy, making this event different from past episodes of falling oil prices.

Consumer spending channel

How much an unexpected shift in the oil price matters for the U.S. economy, in general, depends on how much consumers spend on gasoline as a share of their overall spending. It also depends on how much of that spending is transferred abroad. Every dollar spent on oil or gasoline imported from abroad ends up in the hands of a foreign oil producer who is less likely to spend this revenue in the U.S.

Thus, normally, lower oil prices stimulate U.S. aggregate demand, as consumers have more discretionary income left for other purchases after paying less at the gas pump; conversely, higher oil and gasoline prices reduce aggregate domestic spending and lower economic growth.

Of course, this argument applies only to consumers who actually spend money on gasoline. The first point to keep in mind is that when consumers are cooped up at home with their cars sitting idle in the driveway, they are unlikely to take advantage of lower gasoline prices. Shelter-in-place policies greatly and almost instantaneously reduce the gasoline expenditure share, thereby limiting the direct effect of lower oil prices on domestic consumers.

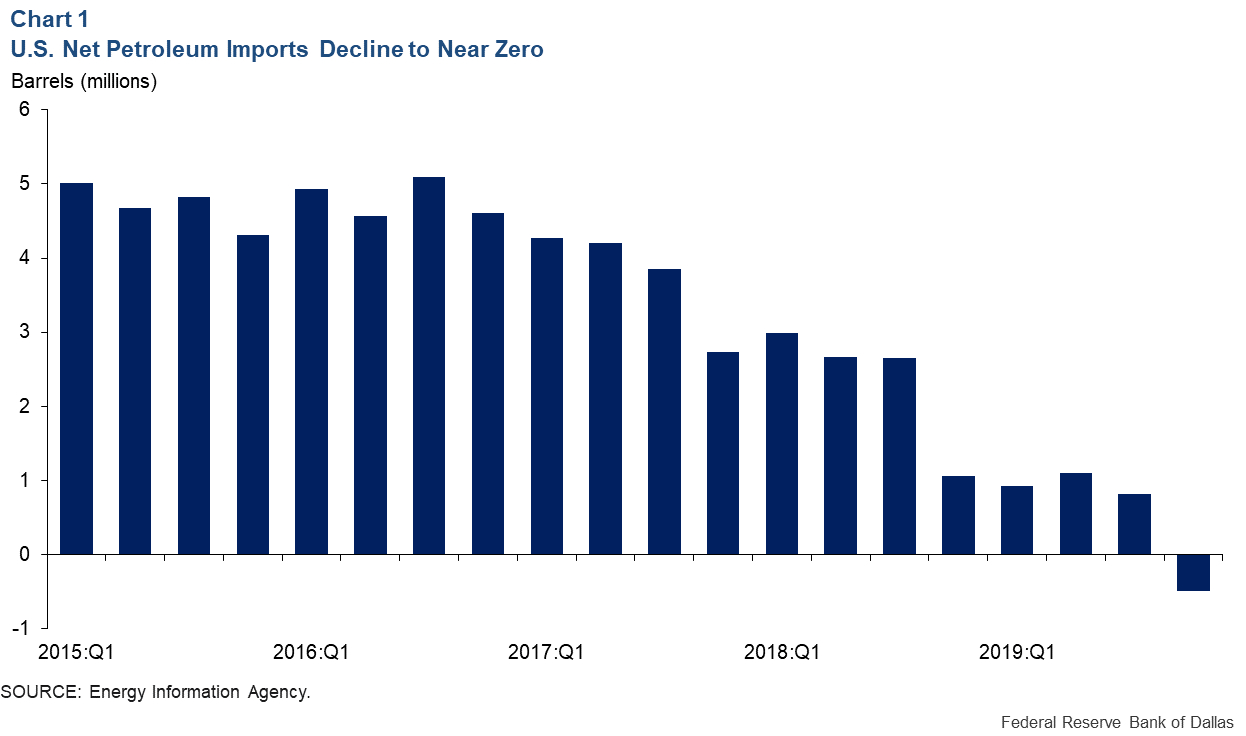

A second point is that the U.S. economy has undergone major changes in the wake of the shale oil revolution. Historically, the U.S. economy was heavily dependent on petroleum imports. By late 2019, net petroleum imports on average had reached about zero (Chart 1). Thus, regardless of how much more consumers spend on gasoline, lower oil and gasoline prices do not mean that aggregate spending in the U.S. economy goes up.

A third caveat is that the 2020 oil price decline in part was driven by lower U.S. demand for fuels, as state and local governments issued stay-at-home orders and many businesses shut down. This fact further helps explain why this time lower oil prices did not cause a boom in consumption and non-oil business investment.

Oil sector investment spending channel

It may seem that businesses more broadly should benefit from lower production costs, as oil prices decline, but that effect tends to be negligible in practice for most industries. A more important component of the transmission of lower oil prices to the U.S. economy is that they cause the oil sector to cut back on fixed-investment expenditures.

This effect occurs independently of whether there is a consumption boom and can be large enough in the aggregate to offset any consumption stimulus. In the current environment, the sharp reduction in capital expenditures by oil companies explains why this oil price decline, on balance, actually hurt U.S. investment spending—and hence, economic growth—not only in oil-producing regions, but overall. Capital expenditures by the industry are projected to decline by an additional 30 percent from previously announced levels and are likely to fall further, consistent with a sharp reduction in oil investment in 2020.

Implications for the banking system

Independently of these expenditure shifts, there has also been concern that lower oil prices may undermine the stability of the banking system with potential spillovers to the economy at large. Because bank loans are securitized by oil reserves that are valued based on the oil futures curve—a measure of what investors believe oil will be worth in the future—a dramatic drop in oil prices matters to banks that are heavily involved in lending to oil companies. One measure of this effect is the decline in banks’ stock valuations when confronted with a large decline in the price of oil.

This argument is reminiscent of the housing crisis of 2007–09. Prior to that crisis, banks nationwide had 37 percent of their loan portfolios in residential mortgages. As house prices collapsed in 2007–09, the return on bank stocks cumulatively declined by 32 percent more than the overall stock market because banks had become overly exposed to house price corrections.

There is no evidence, however, that banks today are similarly dependent on oil-sector lending. Even for the most-exposed banks, the share of bank loans to the energy sector was no larger than 18 percent in the fourth quarter of 2019. Few banks had an exposure greater than 2 percent. Moreover, tighter regulations have forced banks to hold more reserves against potential loan losses.

Standard & Poor’s 500 bank stocks dropped by 19 percent relative to the overall stock market between Jan. 21—when awareness of the COVID-19 virus in the U.S. emerged—and April 3, compared with a decline of 23 percent for S&P 500 energy companies. Put differently, the excess decline experienced by bank stocks relative to the market has been about half of the excess decline of bank stocks during the housing crisis. Thus, there is no evidence to date that the crisis in the oil sector has spilled over into the banking sector more broadly.

In fact, there are many other reasons why bank stocks were hit particularly hard during the current crisis—notably the stress experienced by the broader financial system and falling interest rates. Thus, our analysis likely overstates the systemic impact of lower oil prices on banks’ stock returns.

About the Authors

Lutz Kilian

Kilian is a senior economic policy advisor in the Research Department of the Federal Reserve Bank of Dallas.

Michael D. Plante

Plante is a senior economist and advisor in the Research Department of the Federal Reserve Bank of Dallas.

Xiaoqing Zhou

Zhou is a senior economist in the Research Department of the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.