Term funding premium: Time is money even absent interest rate risk

Term premium refers to the incremental return investors demand for lending at a fixed rate for a specific period (e.g., 10 years), over the expected return from repeatedly rolling short-term loans over that same horizon. In general, this incremental return is the investor’s compensation for taking on an assortment of risks, such as interest rate risk, credit risk and liquidity risk. In the context of Treasuries, typically assumed to be free of credit risk and highly liquid, the premium is viewed largely as compensation for interest rate risk.

Neither expected returns nor the premium are directly observable, necessitating model-based estimation. Nevertheless, term premium can be a useful lens through which to interpret interest-rate trends. It has also at times been an explicit target of monetary policy, most notably during the Fed's quantitative easing programs in response to the Global Financial Crisis of 2008, and more recently during the pandemic. In these periods, large-scale asset purchases were designed to deliver monetary stimulus by reducing term premium.

Many well-regarded models have been developed to estimate term premium, including those of Adrian, Crump and Moench, Kim and Wright and Christensen and Rudebusch.[1] Approaches vary, but they share a common philosophical undercurrent. Most models attribute term premium entirely or mostly to the stochastic nature of interest rates; the term premium is the investor's compensation for accepting interest rate risk.[2] We argue here and in a related working paper that this picture is incomplete. In today’s markets, where the act of providing term financing can be unbundled from the act of accepting interest rate risk, there is considerable evidence that suggests investors also require compensation for the mere act of extending term financing even without any interest-rate exposure.

Treasury floating rate notes provide evidence of a distinct premium

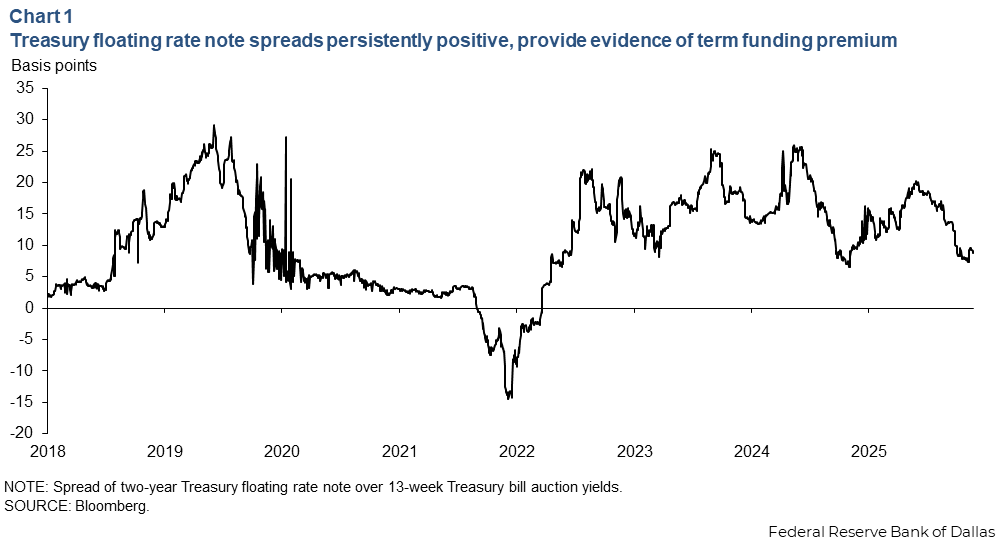

The most unambiguous evidence comes from Treasury floating rate notes. The Treasury introduced the two-year note in January 2014. It pays a floating coupon linked to 13-week Treasury bill yields, plus an additional spread determined at the auction. Because the coupon moves with short-term rates, floating rate notes carry little to no interest-rate risk, especially relative to rolling short-term T-bill positions.

Nonetheless, a significant spread suggests that investors require a premium to buy floating rate notes over rolling T-bills.[3] This is strong and direct evidence of a term funding premium for extending financing over a longer term. The floating rate note spread has been persistently and significantly positive (Chart 1).

At least three conceptual reasons exist for such a premium. By committing to a longer term, the investor forgoes alternative uses of that capital that might become more lucrative over the period. Economically, this commitment resembles selling a put option on those alternatives, which warrants a premium. Levered investors face an additional consideration: variable balance-sheet costs, which can change significantly and alter investment economics over a longer-term. Lastly, once a term funding premium exists, its own variability through time creates spread risk that in principle requires its own premium.

Term funding premium a broad-based market feature

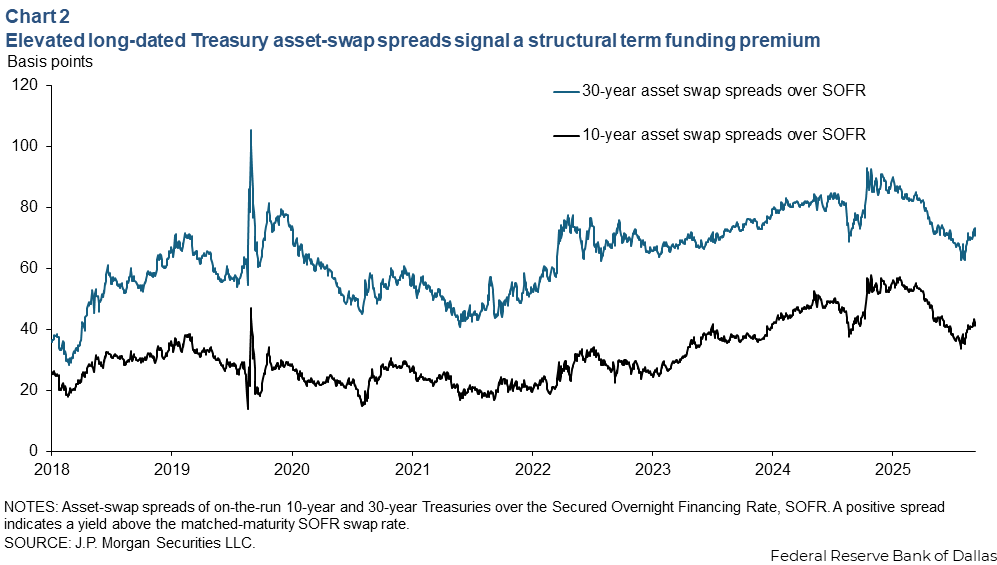

If term funding premium was limited to floating rate notes, it would be tempting to simply dismiss it as a quirk of a niche market sector. But any Treasury security can be transformed into a synthetic floating rate note via an asset-swap—the investor purchases a Treasury security and simultaneously enters into an interest rate swap with a counterparty. The fixed coupon earned from the Treasury is exchanged for a floating coupon linked to SOFR (the Secured Overnight Financing Rate, a risk-free overnight interest rate on loans collateralized by Treasuries) plus a spread.

Since 2018, SOFR has become the dominant floating rate benchmark in the U.S. swap market. This means that asset-swapping a Treasury produces a synthetic floating rate note with floating coupons that reset daily linked to an overnight Treasury rate, plus a spread. This spread is called the asset swap spread (not to be confused with the swap spread, which denotes the negative of the asset swap spread in U.S. market parlance). The 10-year and 30-year Treasury asset-swap spreads have been significantly and persistently positive throughout the SOFR era, beginning in 2018 (Chart 2).

The 10-year asset-swap spread stood near 40 basis points as of June 2026. That is a substantial fraction of the roughly 60-basis-point term premium estimate for the 10-year sector, using the Adrian, Crump and Moench term premium model. Thus, interpreting term premium as compensation solely or mostly for interest-rate risk is difficult to sustain.

Although term funding risk has been studied in the context of bank lending, it has received little formal attention as a premium embedded in Treasury securities. Several factors have likely contributed to this. The floating rate note market did not exist until 2014, removing the most direct evidence. Moreover, before the transition to SOFR as a risk-free benchmark in 2018, swap spreads incorporated a bank-credit element through LIBOR (London inter-Bank Offered rate), obscuring the picture. And in the era before the Global Financial Crisis of 2008, when the stock of sovereign debt was considerably smaller and bank balance sheet costs were lower, the term funding premium was generally low or near zero, making it less conspicuous.

A model-independent measure of the term funding premium

While positive asset-swap spreads point to the existence of the term funding premium, the two are not the same. Asset-swap spreads on individual Treasury securities can be influenced by other factors, such as specialness (in financing) in repo markets, a bond’s unique desirability (such as cheapest-to-deliver status into a futures contract) or fluctuations in dealer balance-sheet availability and cost. Swap spreads at any single maturity might capture idiosyncratic effects alongside the underlying term funding premium.

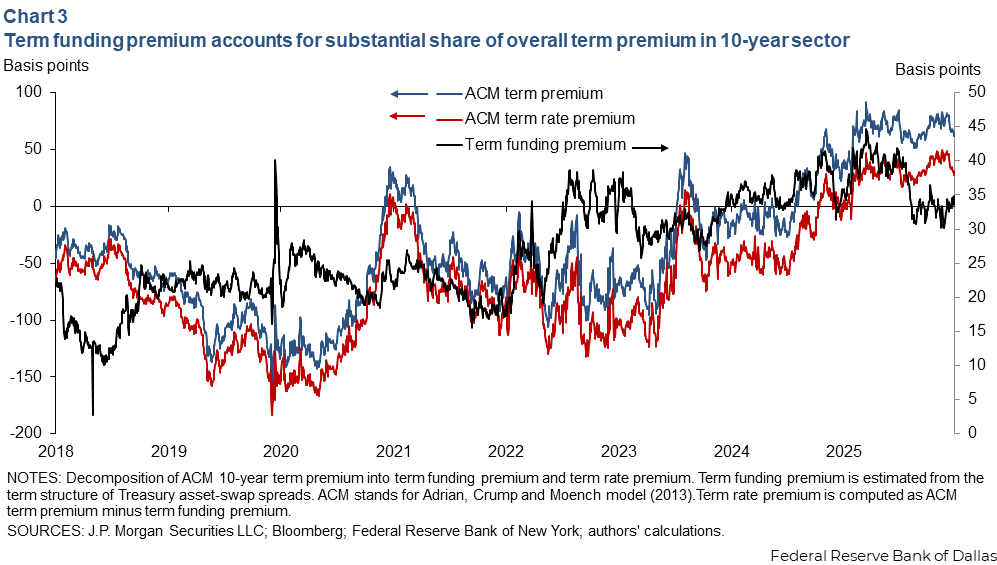

Our approach extracts term funding premium from the entire term structure of asset-swap spreads. We rely on the observation that asset-swap spreads across benchmark Treasury maturities at a particular time are well approximated by a linear function of each bond's modified duration—a measure of bond price sensitivity to yield changes that also serves as a convenient transformed measure of time to maturity. The slope of this linear relationship captures the incremental funding premium per unit of duration extension. We call this slope the unit marginal extension premium (UMEP). Term funding premium at any given maturity is then simply the product of UMEP and the bond's modified duration.

This construction has an important practical advantage: By fitting a single slope across the full maturity spectrum, the resulting term funding premium estimate is far less sensitive to noise in any individual sector. With the term funding premium thus defined, the term rate premium is the residual, that is, term premium (estimated from any of the standard models), minus the term funding premium. This decomposes to:

Term premium = Term funding premium + Term rate premium.[4]

Chart 3 shows the history of this decomposition in the 10-year sector, using the Adrian, Crump and Moench estimate for term premium. Two features stand out. First, the term funding premium has risen materially during the current fiscal expansion, accounting for a substantial share of overall current term premium. Second, term rate premium does not always move in step with the term funding premium. The distinction between the two has become increasingly material in recent years.

Term funding premium, term rate premium respond to different forces

The utility of decomposing term premium into these two components comes from the fact that they are genuinely distinct market phenomena that respond to different market and macroeconomic drivers. We document this by regressing the 10-year term funding premium and the 10-year term rate premium (from three different models) against a common set of five factors. They are primary dealer holdings of Treasuries, rate volatility, net monthly supply of Treasury duration to private investors, the rolling equity-bond correlation and the unemployment gap relative to its natural rate.[5]

The most statistically significant driver of term funding premium is primary dealer holdings of Treasuries (Table 1).

| Variable (units) | Term funding premium | Term rate premium (ACM) | Term rate premium (CR) | Term rate premium (KW) |

| Dealer holdings ($ billions) | 0.038* (0.004) | 0.172* (0.05) | 0.071** (0.03) | 0.030 (0.025) |

| 1Yx10Y Swaption implied volatility (3-month moving average; basis points/day) | 4.3* (0.42) | -1.1 (4.7) | 11.5* (3.4) | 10.1* (2.5) |

| Treasury duration ($ billions in 10-year equivalents) | 0.017 (0.01) | 1.0* (0.154) | 0.8* (0.1) | 0.369* (0.08) |

| Equity-bond correlation (6-month rolling; %) | -1.9*** (1.0) | -3.6 (11.8) | 9.6 (8.5) | -6.5 (6.2) |

| Unemployment gap (%) | 0.341*** (0.2) | -7* (2.3) | -4.8* (1.7) | -7.1* (1.2) |

| NOTES: Analysis uses the 10-year Treasury yield decomposition. All regressions are estimated using 82 monthly observations from January 2019 through December 2025, excluding March and April 2020 as outliers. Reported values are coefficients with standard errors in parentheses; *,** and *** denote significance at the 1%, 5% and 10% levels, respectively. The unemployment gap is the unemployment rate minus its estimated neutral value. SOURCES: J.P. Morgan Securities LLC; Bloomberg; authors’ calculations. |

||||

Dealers intermediate any mismatch in the quantity or timing of the supply of Treasuries and end-user demand. But dealers, who fund their holdings in the overnight repo market, are much less able to extend term financing. That compares with end users who are often benchmarked to a bond index and, therefore, obliged to buy Treasuries. Crucially, Treasury duration supply is not a significant driver of term funding premium. While surprising at first glance, this is because dealers typically hedge their Treasury holdings against duration risk.

For term rate premium, duration-weighted Treasury supply matters for all three models. This is unsurprising, as with any economic good, a larger supply of duration risk in the Treasury market results in a larger premium for absorbing the risk.

Rate volatility, as expected, is a significant driver of term rate premium in most estimates. It also has some influence on term funding premium, likely because elevated implied volatility may reflect broader risk-aversion that spills across multiple premia. The unemployment gap matters for term rate premium but is essentially irrelevant for term funding premium. Collectively, these regression results confirm that the two components of term premium capture different economic forces; they are not merely an accounting decomposition but measures of distinct market phenomena.

Potential relevance for policy

Treasury market dysfunction (as distinct from expected volatility-driven illiquidity) can be difficult to identify in real time. Stress as well as policy response expectations can affect measures such as yield levels and term premium. Metrics based on liquidity differentials show more promise as does term funding premium. In particular, since Treasury market stress is frequently the result of exogenous shocks that impose sudden demands on dealer balance sheets, term funding premium likely offers a complementary signal that is particularly sensitive to the typical strains on intermediation that have featured prominently in recent Treasury market stress episodes.

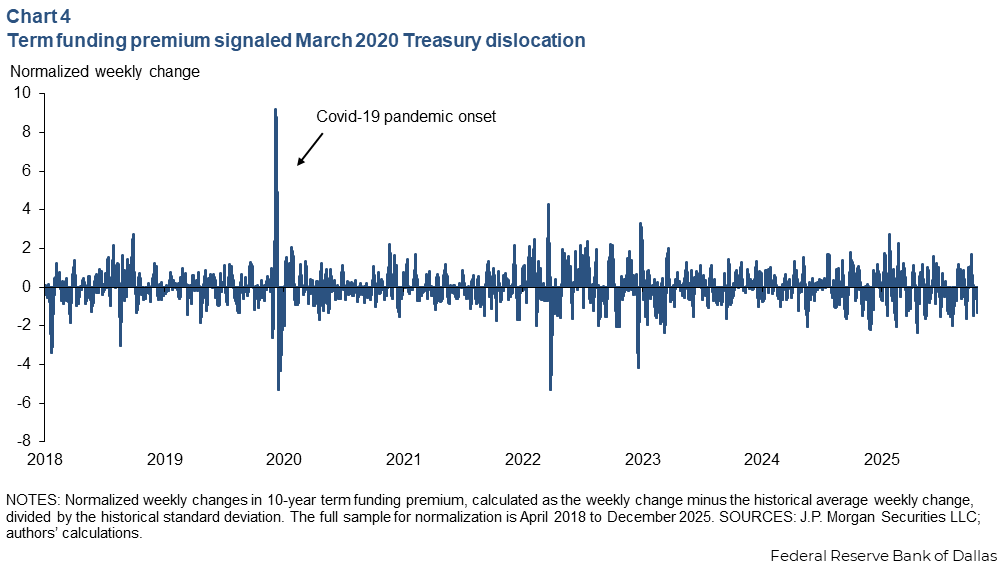

Chart 4 provides evidence of this. It plots the normalized, weekly change in the 10-year term funding premium.

As the pandemic-driven market dislocation took hold in late February and March 2020, the normalized weekly change in term funding premium rose to extreme levels, far exceeding the yield itself or term rate premium.

Critically, the elevation in term funding premium was persistent: It began to normalize only after the Federal Reserve initiated large-scale Treasury purchases to stabilize the market. Normalized changes in yields and term rate premium, by contrast, quickly reversed direction as markets began pricing in weaker economic growth and lower rates ahead—movements signaling economic weakness, not market dysfunction.

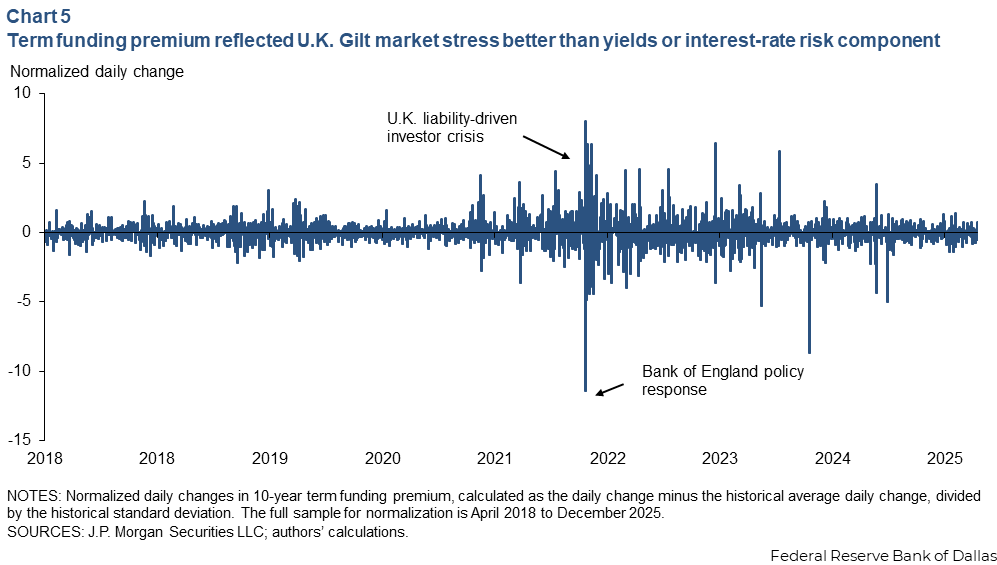

Reassuringly, we observe the same pattern in the U.K. gilt market during the liability-driven investor crisis of September 2022, when a sharp rise in 10-year term funding premium clearly signaled intermediation stress in the gilt market, followed by a retracement after the Bank of England’s market stabilization actions (Chart 5).[6] The infrequent nature of stress episodes makes it difficult to assert the primacy of term funding premium as a gauge of stress, but it shows promise for good reason.

Two further potential applications warrant brief mention. First, term funding premium could offer a cleaner measure of the convenience yield on long-dated Treasuries—the return investors sacrifice for the privilege of holding safe government securities—than alternatives based on comparisons with corporate bond yields. (Such measurements blend the appeal of Treasuries with the illiquidity of corporate debt.) Term funding premium is also likely more robust than swap spreads by themselves. Our measure, extracted from the full maturity spectrum, is less sensitive to idiosyncratic factors in any single sector.

Term funding premium may also have a role to play in assessing the optimal maturity structure of Treasury debt. The Treasury Borrowing Advisory Committee employs an optimal-rule framework as one of many considerations driving its recommendations. This framework uses term premium as one of several variables to which issuance could respond. Incorporating term funding premium and term rate premium as two separate inputs into that framework could enable more nuanced guidance, for instance, favoring floating-rate note issuance in periods when term funding premium is low, but term rate premium is elevated.

Future directions

We have argued that the standard interpretation of term premium as compensation solely for bearing interest-rate risk is incomplete. Evidence from Treasury floating rate notes and from Treasury asset-swap spreads since SOFR became the benchmark rate clearly points to the existence of term funding premium, a premium investors demand for extending the maturity of their commitment, independently of any interest-rate exposure.

We present a model-independent approach to measuring it, based on the slope of the term structure of swap spreads and show that the residual, the term rate premium, responds to different economic forces than the term funding premium does. At a practical level, we provide evidence that term funding premium may be a more reliable real-time indicator of Treasury market stress than overall yield or standard term-premium measures, because it isolates the intermediation premium that rises when dealer capacity is strained.

Further research is needed to develop formal term-structure models, which treat both components endogenously, to validate the stress-indicator application across more historical episodes, and to refine the applications to convenience-yield measurement and optimal issuance frameworks.

Notes

- Three commonly used term premium models that we reference here are those of Adrian, Crump and Moench (“Pricing the Term Structure with Linear Regressions,” by Tobias Adrian, Richard K. Crump, and Emanuel Moench, Journal of Financial Economics, vol. 110, no. 1, 2013, pp. 110–138), Kim and Wright (“An Arbitrage-Free Three-Factor Term Structure Model and the Recent Behavior of Long-Term Yields and Distant-Horizon Forward Rates,” by Don H. Kim and Jonathan H. Wright, Federal Reserve Board, Finance and Economics Discussion Series, 2005), and Christensen and Rudebusch (“The Affine Arbitrage-Free Class of Nelson-Siegel Term Structure Models,” by Jens H.E. Christensen, Francis X. Diebold and Glenn D. Rudebusch, Journal of Econometrics, vol. 164, no. 1, 2011, pp.4–20). For surveys of term premium estimation methods, see Kim and Orphanides ("The Bond Market Term Premium: What is it, and How Can We Measure It?," by Don H. Kim & Athanasios Orphanides, BIS Quarterly Review, Bank for International Settlements, 2007) and Cohen et al. (“Term Premia: Models and Some Stylized Facts,” by Benjamin H. Cohen, Peter Hördahl and Fan Dora Xia,BIS Quarterly Review, Bank for International Settlements, 2018).

- Durham (“Nominal U.S. Treasuries Embed Liquidity Premiums, Too,” by J. Benson Durham, Journal of Financial and Quantitative Analysis, vol. 60, no. 3, 2025, pp. 1310–1341) and D’Amico et al. (“Tips from TIPS: The informational content of Treasury inflation-protected security prices,” Stefania D’Amico, Don H. Kim, and Min Wei, Journal of Financial and Quantitative Analysis, 53(1):395–436, 2018) include liquidity as a factor in their models.

- The spread can be zero for technical reasons. Floating rate note coupons reset weekly, but a strategy of rolling 13-week T-bills will experience returns that are fixed for 13 weeks at a time. In stable interest-rate environments, this slippage is negligible and cannot account for persistently positive FRN spreads, especially during Fed-on-hold periods.

- By construction, term rate premium inherits the model-dependence of the term premium estimate from which it is derived. Term funding premium, by contrast, is computed directly from observable asset-swap spreads and is model-independent.

- Regressions use monthly data from January 2019 through December 2025 (82 observations; March and April 2020 excluded as outliers). For historical charts that extend into the pre-SOFR era, we use fed funds overnight index swap (OIS) spreads as an approximation to SOFR swap spreads. Overnight SOFR typically trades close to the fed funds rate.

- The U.K. gilt market analysis applies the same unit marginal extension premium methodology to U.K. government bond asset-swap spreads denominated in sterling.

About the authors

Srini Ramaswamy is a senior financial economist in the Research Department at the Federal Reserve Bank of Dallas.

Seth Searls is a vice president of financial sector and policy analysis in the Research Department at the Federal Reserve Bank of Dallas.

Hugo De Vere is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Ipek Ozil is an executive director and head of U.S. Fixed Income Derivative Strategy at J.P. Morgan Securities LLC.