Tokenized deposits use blockchain structure in traditional banking framework

Commercial banks have begun exploring adoption of tokenized deposits, traditional deposits on digital ledgers. Tokenized deposits could improve payment efficiency for retail and institutional clients.

Such tokens resemble stablecoins, for which a regulatory framework was authorized in 2025 under the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act). Deposit tokens rely on blockchain technology, which allows payments to settle almost instantaneously and dictates the conditions under which funds move (programmability).

While GENIUS-compliant stablecoins are backed one-to-one by a pool of low-risk, liquid assets such as Treasuries, deposit tokens are a claim on an issuing bank and ultimately backed by the assets on a bank’s balance sheet and remain embedded within the regulated banking system. These tokens preserve the safeguards associated with bank deposits, including deposit insurance and Bank Secrecy Act compliance.

Maintaining these properties requires deposit tokens to circulate within the issuing institution’s defined compliance boundary. To be meaningful, however, digital payments must flow across many institutions, requiring netting and reconciliation of accounts. We describe here how banks are organizing tokenized deposit solutions to facilitate these flows.

From a customer’s point of view, the value proposition of tokenized deposits depends on the number and type of entities accessible through the network. Banks with a large and diversified client base can offer access to a large network, increasing the potential use and the convenience value of their deposit tokens. Smaller banks, lacking such a deep deposit base, may organize into consortiums and associations to create similar network effects.

Banks’ appetite to adopt tokenized deposits depends on their tolerance for, and ability to minimize external liquidity concerns—for example, the need to set aside liquidity when a lag exists between settlement of customers’ transactions and netting across banks. Where such a lag exists, banks end up holding the liabilities of other banks.

Because the size of the associated interbank credit depends on the nature and flow of the transactions, the organizational design of tokenized deposit networks varies based on the tolerance for credit exposures.

What tokenization changes, what remains the same

A deposit token is still a commercial bank deposit and remains on the issuing banks’ balance sheet. It is redeemable for cash at face value, and transactions are subject to bank supervisory frameworks.

Deposit tokenization, however, changes the delivery framework. Under emerging models, customers may transfer deposits through digital wallets in near real time. Transfers that traditionally have required a series of payment steps for completion can instead be executed on a digital platform with greater transparency and speed. From an end user’s perspective, settlement may appear instantaneous. This is analogous in function to some consumer payment applications, such as Zelle and Venmo, which can rely on the Automated Clearing House (ACH) network to settle payments that also appear instantaneous to the user.

Yet, the acceleration of the delivery does not necessarily imply simultaneous discharge of bank obligations. In these emerging models, customer transfers settle on-chain while interbank obligations might be resolved later—either through bilateral netting between participating institutions or through a shared clearing and settlement structure.

Tokenization can therefore accelerate the front-end transactions while leaving interbank settlement anchored in existing infrastructures, such as Fedwire, the Federal Reserve’s real-time gross settlement system.

Models for deposit tokenization

The models emerging from current projects provide an early view into how institutions are addressing trade-offs between speed and liquidity management.

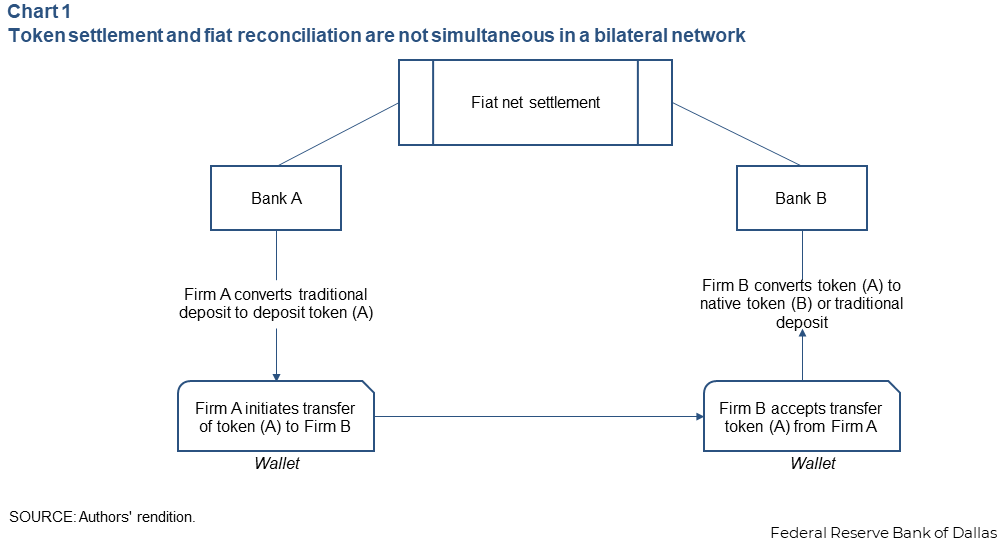

We begin by considering a bilateral settlement network with deposit tokens issued by individual banks. In this example, Bank A and B both tokenize their deposits into A and B tokens, respectively.

A customer of Bank A transfers an A token to a customer of Bank B. Upon receiving an A token in his wallet, a Bank B customer converts it either to a traditional deposit at Bank B or to a B token. Bank B facilitates this conversion by accepting the A Token at par value and providing one of its own liabilities to the customer (Chart 1).

After a series of these transactions, Banks A and B net their wallets. If a residual exists, say in Bank A, Bank B transfers the corresponding fiat amount through the banks’ master accounts at the Fed or through the traditional correspondent banking network, if Banks A and B are in different jurisdictions.

This model’s main feature is speed, enabling fast front-end on-chain settlement for customer transactions, while still relying on interbank transfers via legacy arrangements. Because the fiat settlement does not occur for every trade, each bank carries some credit risk, as the other bank might default on its obligations before fiat currency settlement occurs.

This type of bilateral settlement might be appropriate for larger institutions positioned to manage credit risk (and access liquidity) and whose token flows tend to be offsetting.

An alternative arrangement involves deposit networks and central settlement. Banks join an authorized network that uses a commonly issued token through a settlement agent. The agent acts as a private clearing house or correspondent bank for the participating banks.

Participating banks keep records of token movements and balance deposit accounts. This arrangement has one advantage: There is only one token circulating among the network banks’ customers. Transactions settle on-chain but still require reconciliation of deposit accounts.

This could happen in two ways. Banks can instantly synchronize cash deposit reconciliations with on-chain transfers (known as atomic settlement). Alternatively, it can occur in batches, much as Bank A and Bank B in the bilateral network example. Regardless of how they’re completed, reconciliations happen through accounts held by the participating banks at a settlement bank.

By resembling other, existing clearing and settlement organizational structures, deposit networks allow mutual insurance mechanisms—in the form of liquidity provisions or loss mutualization—to mitigate adverse events.

That said, participating banks remain exposed to risks associated with the issuer entity’s ability to operate the network, monitor and maintain adequate funding of participants’ accounts and address liquidity issues.

Bank-specific tokens with a stablecoin bridge provide another option. Banks, with their own deposit tokens, could also utilize a wholesale stablecoin as a bridge to transfer value between banks. A network structure would still be required to fund the reserves backing the stablecoin.

However, this structure significantly reduces the need for trust across the participating institutions, because credit exposure does not accumulate. To allow around-the-clock transactions, participating banks would pre-fund their accounts at the stablecoin issuer.

This arrangement critically differs in one respect: The asset backing the stablecoin would be isolated (in line with the GENIUS Act), providing stablecoin holders priority in case of a forced resolution.

The three models all expose banks to some credit risk. It arises either directly involving another bank’s liabilities or via an institution that operates as a central settlement agent, through a series of pre-funded accounts.

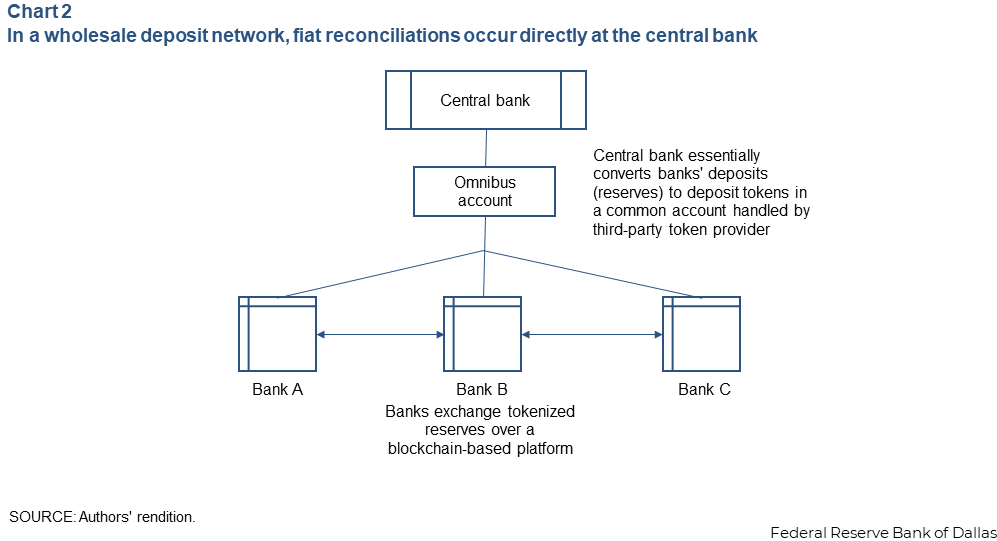

Wholesale tokens backed by central bank reserves present another approach to reduce such credit risk. Wholesale tokens move settlement to an account at the central bank. The token is thus tied to central bank reserves. A similar arrangement already exists in the U.K., where the Bank of England has authorized a project sponsored by six large banks.

In this structure, a private payment system operator makes use of an omnibus (or pooled) account at a central bank (Chart 2).

Financial institutions that want to participate in this payments system move funds from their individual central bank accounts to the omnibus account held by the operator. The operator then provides these institutions with deposit tokens on a one-for-one basis that they can exchange with other institutions in the network, in near real-time and around the clock.

From the point of view of a participating financial institution, prefunding makes this arrangement more expensive than the alternatives. The advantage is that it eliminates credit risk. However, because of the cost, it would likely be used only to reconcile wholesale transfers.

Liquidity transformation and risk

The separation between front-end delivery and back-end settlement introduces a new timing dimension to liquidity and credit risk. In the bilateral model, banks carry counterparty exposure during the time between token transfer and fiat settlement. If flows are balanced, these exposures may net down efficiently. If flows are one-sided, exposures can accumulate until final settlement occurs.

Network models re-allocate risk. Rather than holding each other’s tokens, participating banks either share a common consortium token or convert deposits into a jointly managed wholesale stablecoin transfer. This eliminates bilateral credit risk exposure but centralizes risk in the central clearing and reserve management layer. The operational and legal structure of that shared entity becomes critical to the system’s stability.

In any of these variants, tokenization does not eliminate liquidity transformation. Banks continue to fund longer-term assets with deposits that can now move even faster.

One additional consideration is how speedier transfer mechanisms might interact with liquidity dynamics during periods of stress. Because tokenized deposits can potentially move across institutions and networks more quickly, they may compress the time banks have to manage sudden outflows. This speed may reduce friction in normal conditions but accelerate deposit flight during periods of stress.

Deposit tokens offer entry to digital financial infrastructure

The emergence of deposit token networks may serve as a potential building block for emerging digital financial market infrastructure, enabling more efficient payment and collateral movement on digital ledgers.

However, the tokens also raise broader questions about payment system resilience and risk management. If instant customer transfers occur while simultaneously interbank settlement is deferred, institutions confront challenges involving intraday liquidity and counterparty exposure.

Still unresolved is how new clearing layers involving third-party entities concentrate settlement risk or fragment liquidity across networks. These issues become particularly relevant as various forms of tokenized money simultaneously evolve.

About the authors

Seth Dunbar is a senior risk specialist in the supervisory risk, policy and surveillance division of the Banking Supervision Department at the Federal Reserve Bank of Dallas.

Pon Sagnanert is a policy analyst in the Integrated Policy Department at the Federal Reserve Bank of Dallas.

Guhan Venkatu is a vice president and regional executive at the Federal Reserve Bank of Dallas.

Alessio Saretto is an assistant vice president in the Research Department at the Federal Reserve Bank of Dallas.