Dallas-Fort Worth Economic Indicators

The Dallas–Fort Worth economy expanded at a modest pace. Employment growth was subdued in November, with DFW adding jobs at the slowest pace in seven months. Overall, the DFW economy remains solid, with 2 percent annualized job growth year to date (nearly 68,000 jobs). Business-cycle indexes for both metros pointed to continued expansion. Home sales fell for the second straight month in November, and inventory ticked up but remains tight. House price appreciation has moderated, particularly in Dallas.

Labor Market

Job Growth Slows in November

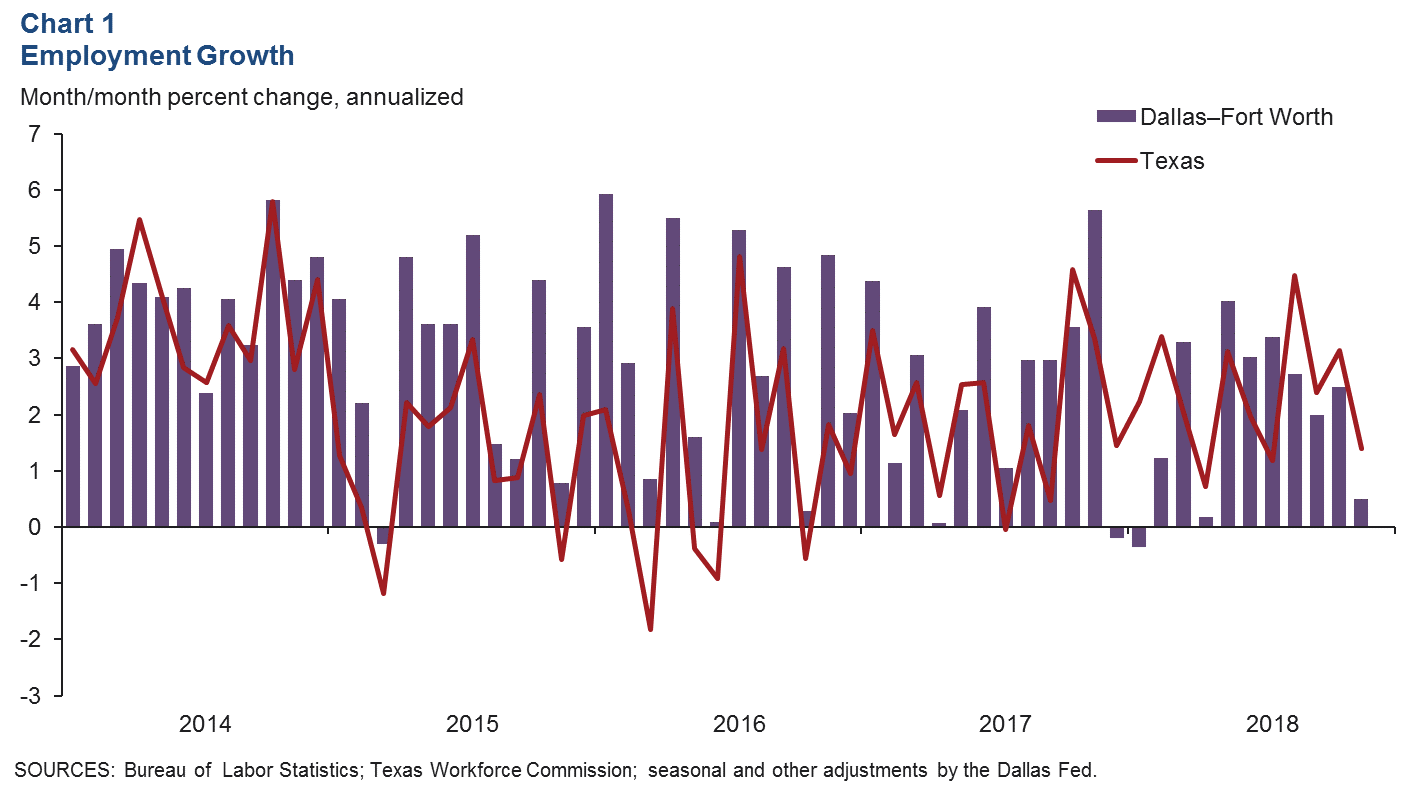

DFW payrolls grew by 1,560 jobs in November, or a 0.5 percent annualized increase, following gains of 7,600 in October (Chart 1). Year-to-date employment growth of 2 percent (annual rate) is lagging last year’s 2.5 percent pace.

The November softening in job growth reflects weakness in the service sector. Employment in professional and business services saw a steep decline of 10.7 percent (annualized). Other sectors that fell less sharply in the month were leisure and hospitality, education and health services, and other services. However, only the other services sector has shed jobs year to date. Payroll growth in the goods-producing sector remained solid in November.

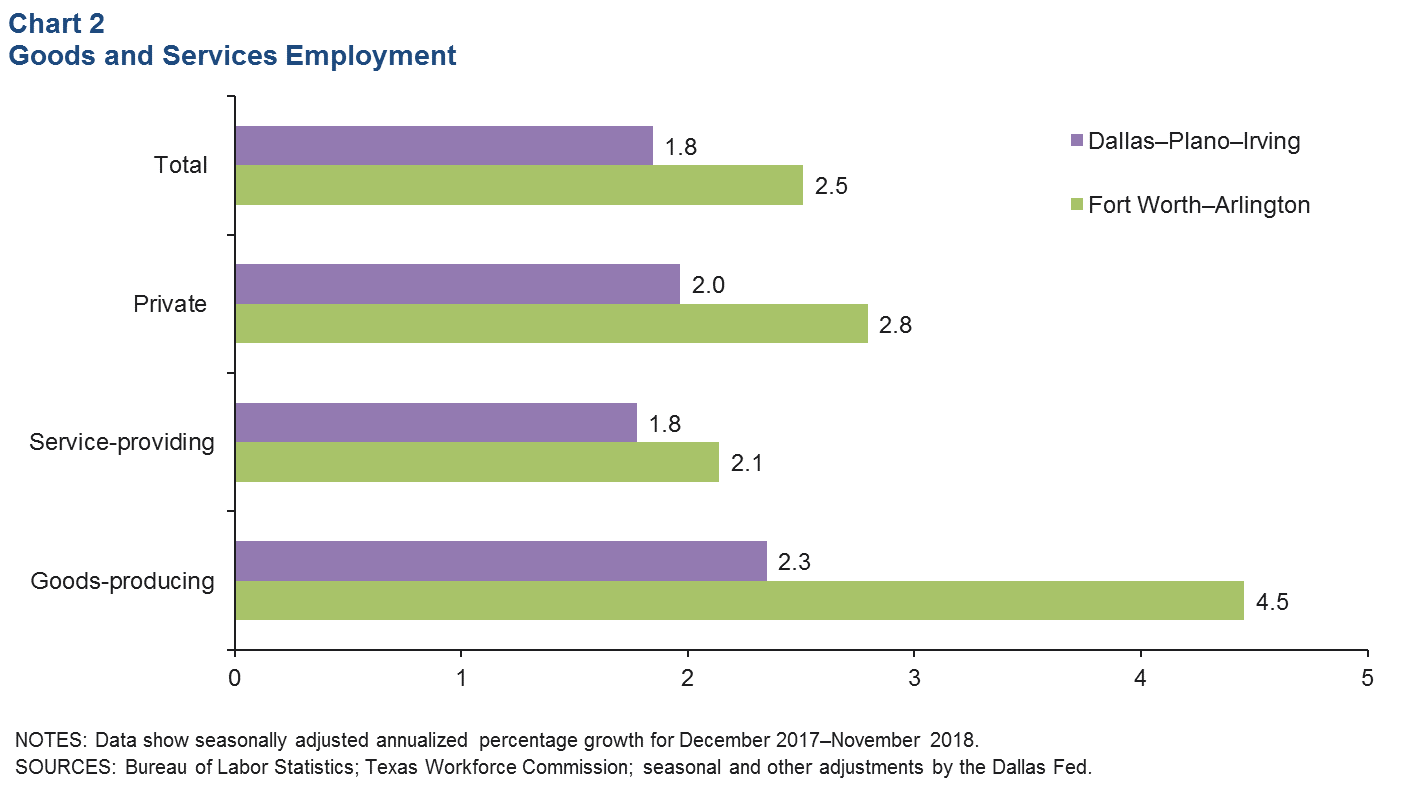

Goods-Producing Sector Outperforms Services

Payrolls in the goods-producing sector (manufacturing and construction and mining) have expanded at a faster clip than service-related employment year to date (Chart 2). Growth has been particularly strong at an annualized 4.5 percent in Fort Worth’s goods-producing sector, which comprises 16 percent of its employment. This compares with a 2.1 percent increase in Fort Worth’s service sector payrolls. Job growth in Dallas’ goods-producing sector at 2.3 percent has also outpaced its services sector growth rate of 1.8 percent. Through November, payroll expansion in Fort Worth at 2.5 percent has outperformed that in Dallas.

Business-Cycle Indexes

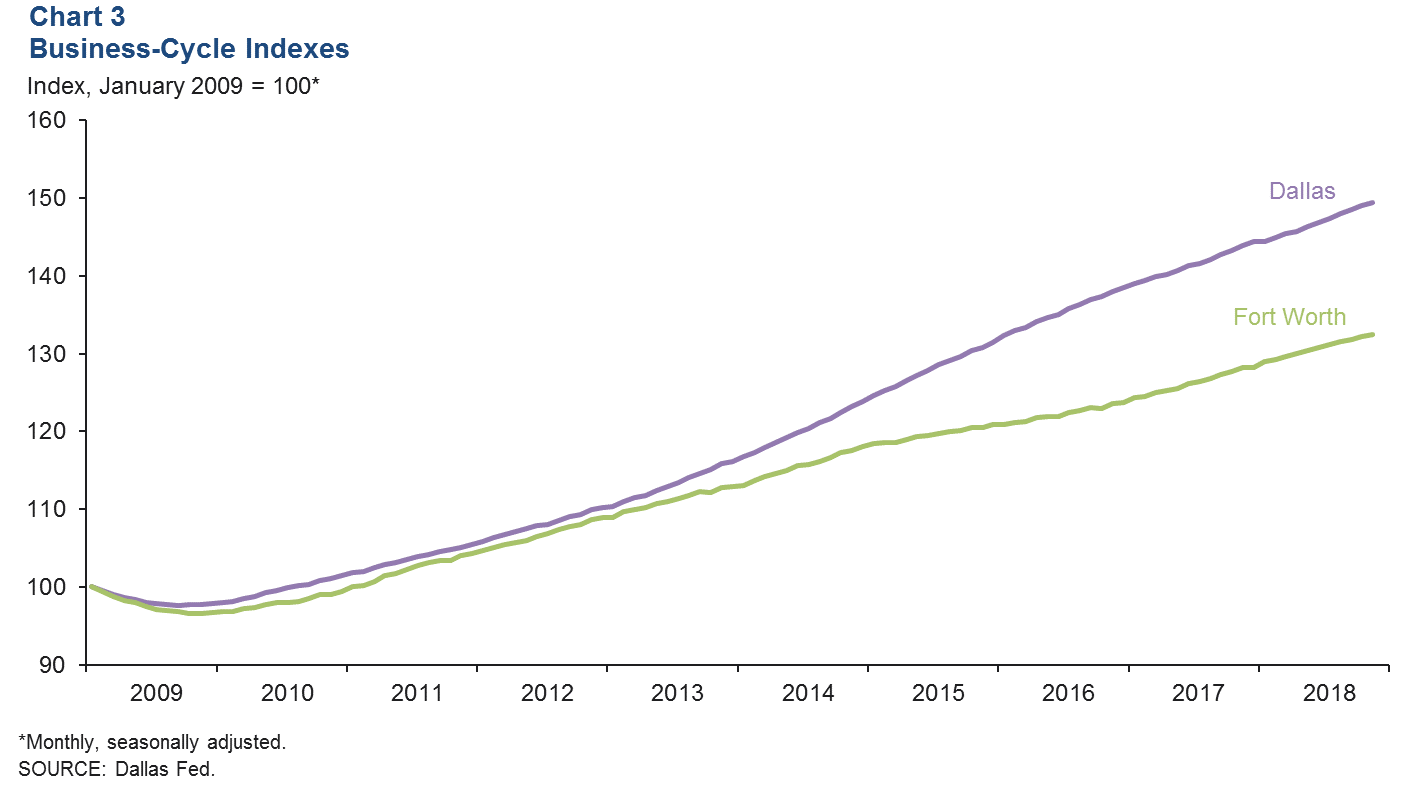

Growth in the Dallas and Fort Worth business-cycle indexes was below its long-run average in November, partly due to tepid job growth during the month (Chart 3). The Dallas index expanded an annualized 3.1 percent, slower than October’s 4.5 percent rate. Growth in the Fort Worth index decelerated to 2.0 percent from 3.7 percent in October. Year over year in November, the Dallas index rose 3.8 percent, and the Fort Worth index was up 3.3 percent.

Housing

Home-Price Appreciation Cools

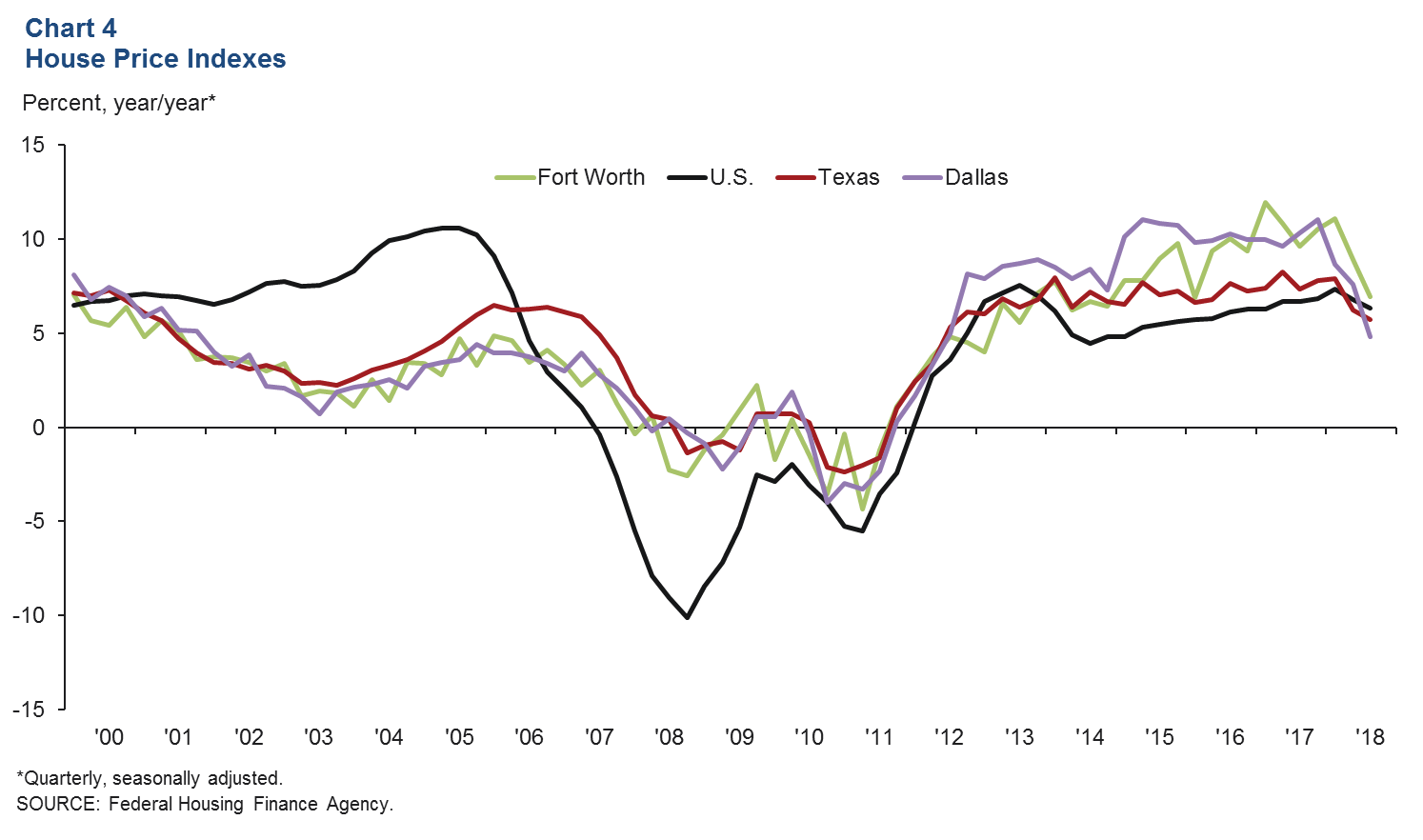

DFW home prices edged up in third quarter 2018 as continued job creation and tight home inventories propelled price increases in the area. Prices rose 0.4 percent in Dallas and 0.3 percent in Fort Worth in the third quarter, but gains lagged the state’s 1.1 percent and nation’s 1.3 percent increase, according to the Federal Housing Finance Agency’s house price purchase-only index. On a year-over-year basis, prices were up 4.8 percent in Dallas—slower than the Texas rate of 5.7 percent and the nation’s 6.3 percent (Chart 4). Conversely, an annual increase of 7.0 percent in Fort Worth is ahead of both the state and national figures.

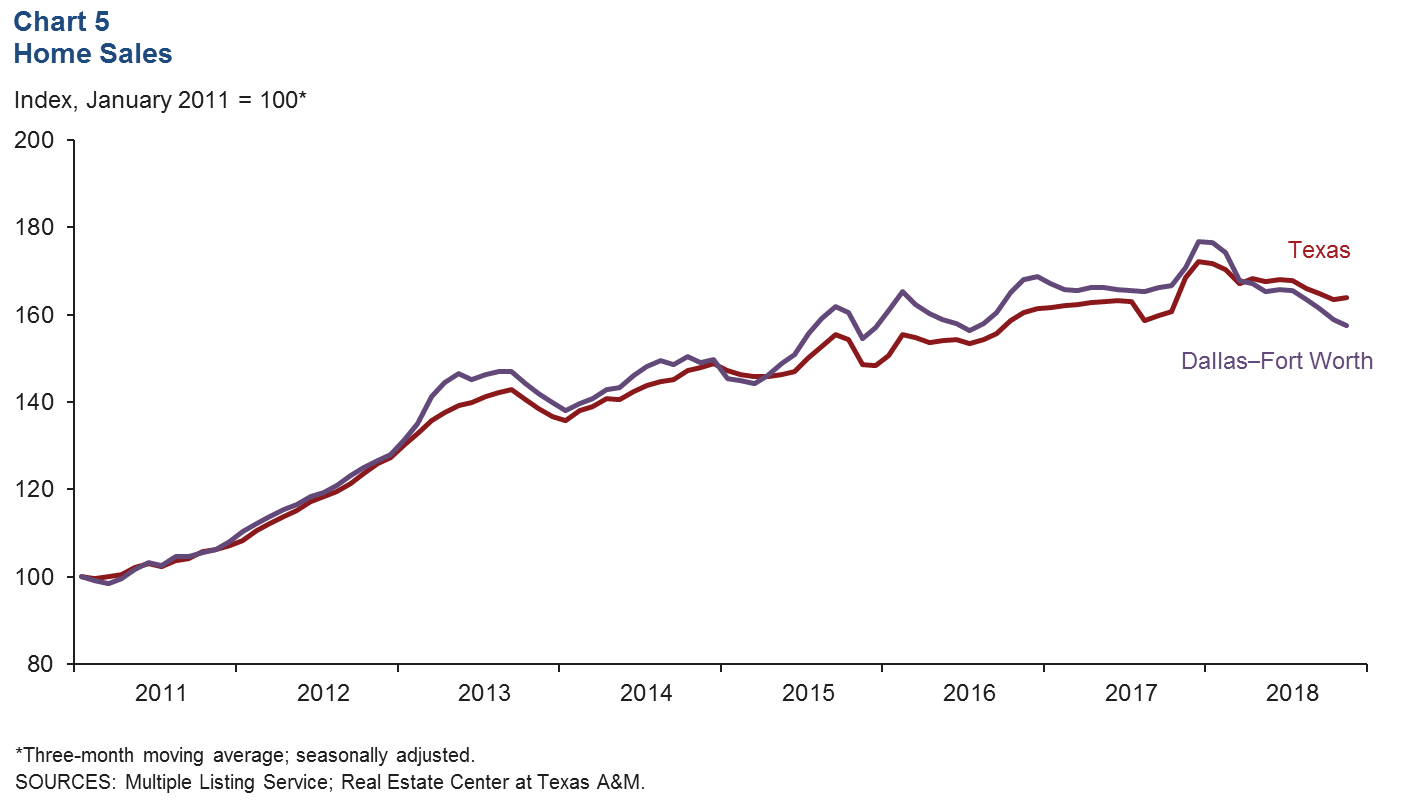

Home Sales Soften Further

DFW existing-home sales (seasonally adjusted) edged down for the second straight month in November. The three-month moving average also shows sales steadily declining in the metroplex since mid-2018 (Chart 5). Through November, total home sales are trailing those for the same period in 2017 by 2.2 percent, while statewide sales are up 1.8 percent. Rising home prices and higher mortgage rates are likely affecting affordability, and hence, sales activity. Additionally, sales of entry-level homes (those priced below $200,000) have been sliding since 2014 due to a lack of inventory.

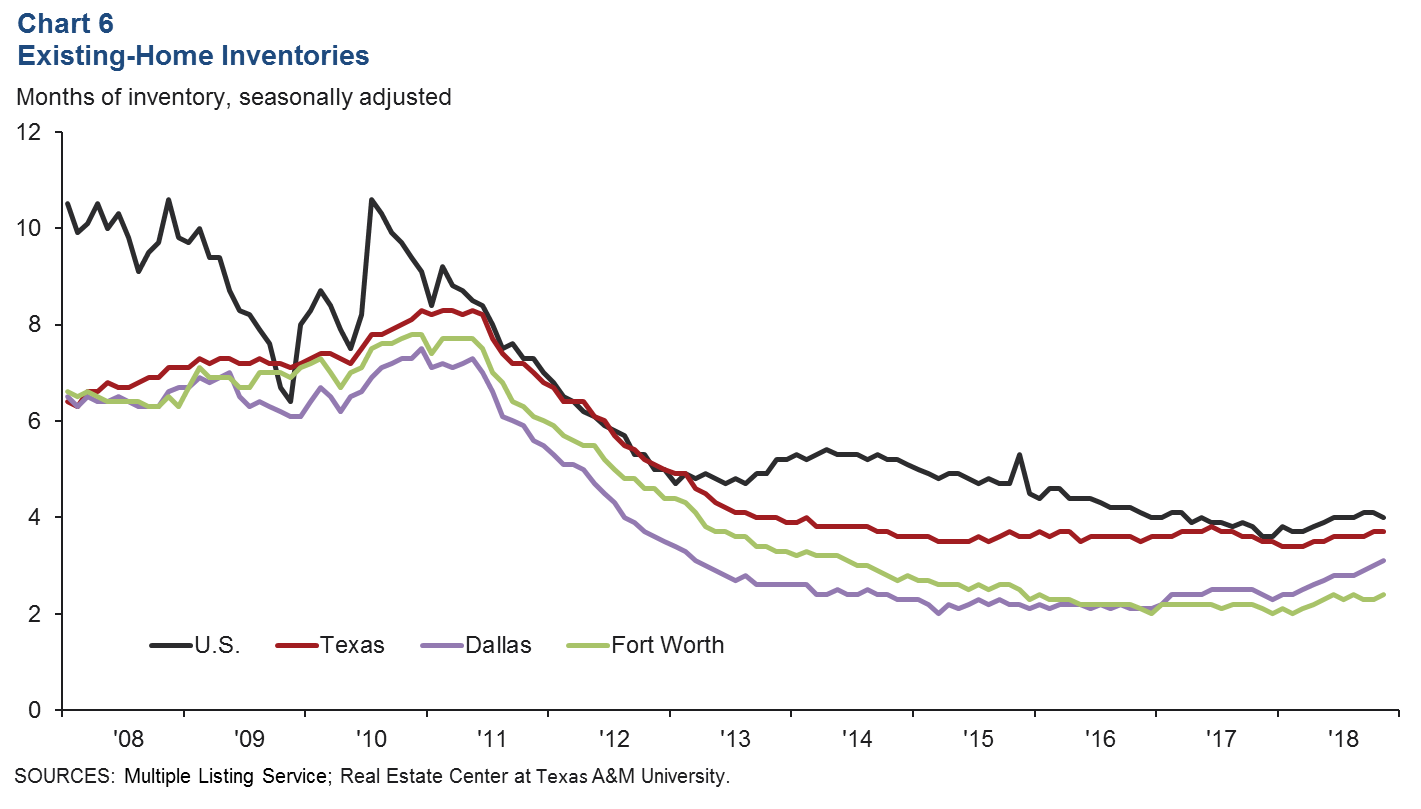

Inventories Tick Up

DFW existing-home inventories remained tight and well below the six months’ supply typically associated with a balanced market. In November, overall inventories edged up to 3.1 months in Dallas and 2.4 months in Fort Worth but remained below the U.S. and Texas levels (Chart 6). Inventories of entry-level homes (those priced below $200,000) remain the tightest at 1.5 months of supply or less. Inventories of mid-priced homes ($300,000–$499,999) are also low at 3.7 months but have been gradually moving up since earlier in the year.

NOTE: Data may not match previously published numbers due to revisions.

About Dallas–Fort Worth Economic Indicators

Questions can be addressed to Laila Assanie at laila.assanie@dal.frb.org. Dallas–Fort Worth Economic Indicators is published every month on the Tuesday after state and metro employment data are released.