Texas Service Sector Sees Unprecedented Decline in Activity

Texas Service Sector Outlook Survey

March 31, 2020

Texas Service Sector Sees Unprecedented Decline in Activity

What’s New This Month

For this month’s survey, Texas business executives were asked supplemental questions on the impacts of the coronavirus (COVID-19). Results for these questions from the Texas Manufacturing Outlook Survey, Texas Service Sector Outlook Survey and Texas Retail Outlook Survey have been released together. Read the special questions results.

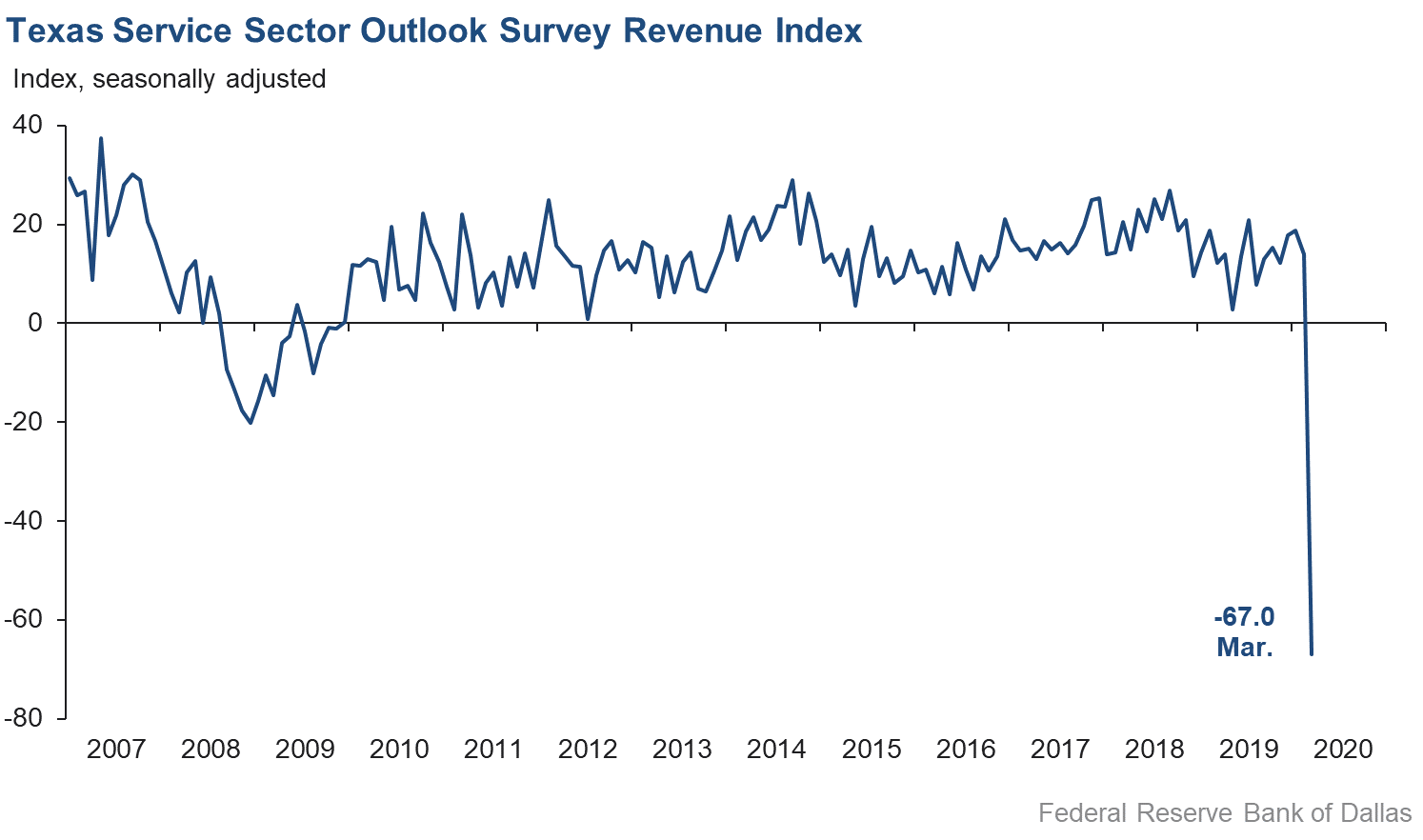

The Texas service sector saw a dramatic decline in March amid the ongoing coronavirus (COVID-19) pandemic and related measures, according to business executives responding to the Texas Service Sector Outlook Survey. The revenue index, a key measure of state service sector conditions, plummeted from 14.0 in February to -67.0 in March, an all-time low reading for the survey.

Labor market indicators reflected a sharp contraction in employment and significantly shortened workweeks. The employment index fell from 6.1 to -23.8, its lowest reading on record. The hours worked index drastically dropped over 47 points to -43.0, with nearly half of respondents noting a cut in employee hours.

Perceptions of broader business conditions turned extremely pessimistic in March, while uncertainty surged. The general business activity index fell over 85 points to -78.8, while the company outlook index dove 80 points to a reading of -75.3, setting a new record low for both indexes. Tellingly, all respondents noted either no change or a decline in both of these measures compared with last month. Meanwhile, the outlook uncertainty index surged to 37.6, its highest reading since the question was added to the survey in 2018.

Wage and price pressures largely evaporated in March. The wages and benefits index declined 30 points to -12.4, its first negative reading since 2009. The input prices index fell from 26.6 to 0.1 suggesting no net price changes compared with February, while the selling prices index saw an unprecedented fall from 8.0 to -44.5.

Respondents’ expectations regarding future business conditions deteriorated sharply compared with February. The future company outlook index decreased from 15.8 to -49.1, while the future general business activity index plummeted 62 points to a reading of -50.4. For both indexes, fewer than 15 percent of respondents noted an increase compared with last month. Other indexes of future service sector activity, such as revenue and employment, declined to all-time lows and suggest expectations of ongoing weakness over the next six months.

Texas Retail Outlook Survey

March 31, 2020

Texas Retail Sales Plummet

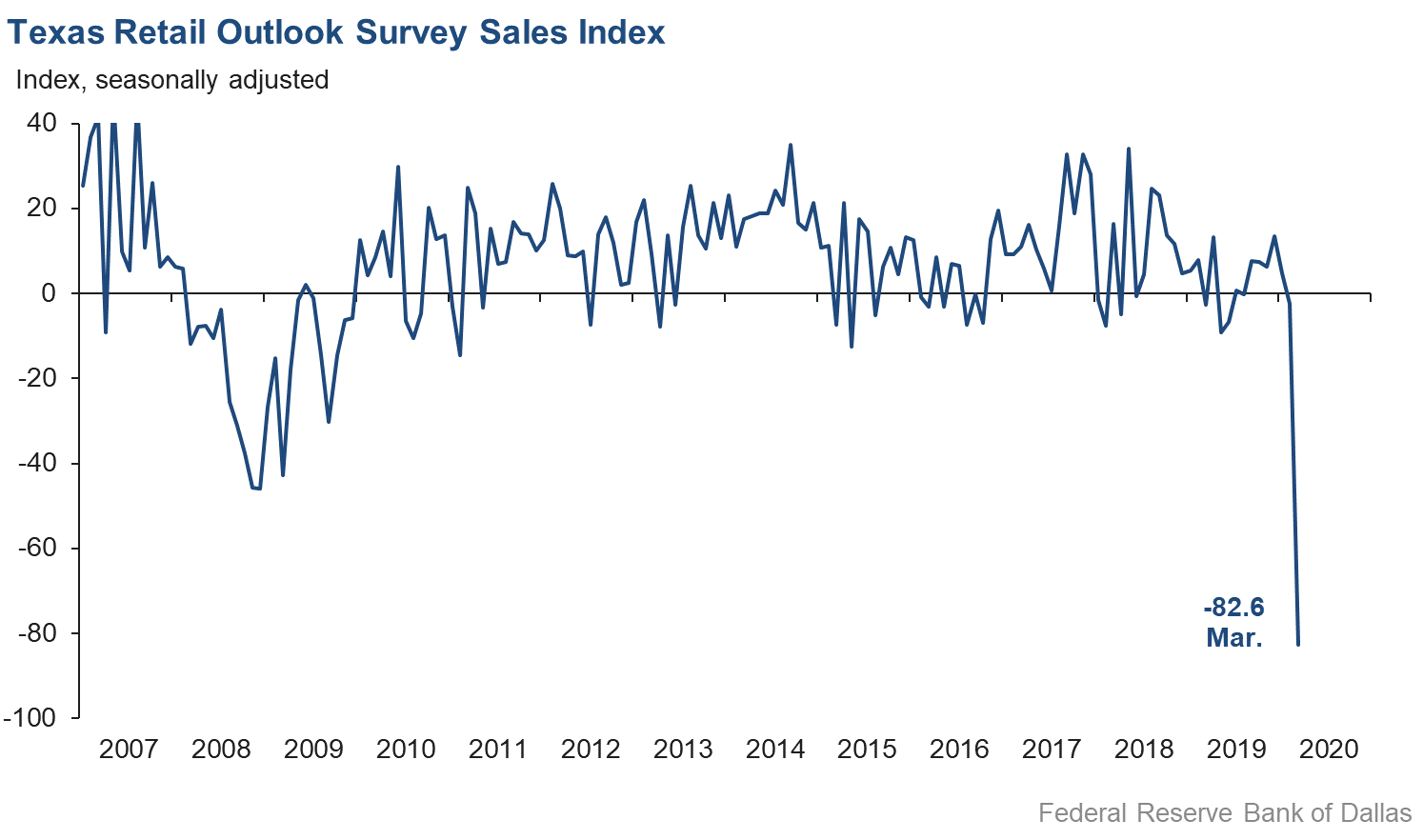

Retail sales fell sharply in March, according to business executives responding to the Texas Retail Outlook Survey. The sales index dropped from -2.5 in February to an all-time low of -82.6 in March, with fewer than 1 percent of respondents noting an increase in sales. Inventories declined precipitously, with the inventories index weakening from -9.7 to -42.6.

Retail labor market indicators pointed to sharp cuts in employment and workweek hours in March. The employment index fell from -1.0 to -28.4, a postrecession low, while the hours worked index plunged to a record low of -58.1, as all respondents noted no change or a decline in hours compared with February.

Retailers’ perceptions of broader business conditions deteriorated to all-time lows in March, while outlook uncertainty hit an all-time high. The general business activity index plunged from -5.0 to -84.2, while the company outlook index declined from -10.3 to -83.8—both record lows.

Retail prices and wages declined in March. The input prices index fell from 19.9 to a postrecession low of -12.0, while the selling prices index collapsed 63 points to -35.5, near a record-low reading. The wages and benefits index fell from 14.7 to -20.6.

Negative sentiment surrounding retailers’ perceptions of future conditions surged this month. The future general business activity index lost nearly 65 points and dropped to -66.0, while the future company outlook index similarly shed 65 points, plunging to -62.4. Other indexes of future retail activity, such as sales and employment, moved into deeply negative territory and point to expectations of further declines over the next six months.

The Texas Retail Outlook Survey is a component of the Texas Service Sector Outlook Survey that uses information only from respondents in the retail and wholesale sectors.

Next release: April 28, 2020

|

Data were collected March 17–25, and 248 Texas service sector and 56 retail sector business executives responded to the survey. The Dallas Fed conducts the Texas Service Sector Outlook Survey monthly to obtain a timely assessment of the state’s service sector activity. Firms are asked whether revenue, employment, prices, general business activity and other indicators increased, decreased or remained unchanged over the previous month. Survey responses are used to calculate an index for each indicator. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease. Data have been seasonally adjusted as necessary. |

Texas Service Sector Outlook Survey

March 31, 2020

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Current (versus previous month) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend* | % Reporting Increase | % Reporting No Change |

% Reporting Decrease |

|

Revenue |

–67.0 |

14.0 |

–81.0 |

11.7 |

1(–) |

2.4 |

28.2 |

69.4 |

|

Employment |

–23.8 |

6.1 |

–29.9 |

6.5 |

1(–) |

3.4 |

69.4 |

27.2 |

|

Part–Time Employment |

–21.4 |

4.1 |

–25.5 |

1.6 |

1(–) |

2.8 |

73.0 |

24.2 |

|

Hours Worked |

–43.0 |

4.4 |

–47.4 |

2.5 |

1(–) |

4.2 |

48.6 |

47.2 |

|

Wages and Benefits |

–12.4 |

17.7 |

–30.1 |

14.5 |

1(–) |

8.4 |

70.8 |

20.8 |

|

Input Prices |

0.1 |

26.6 |

–26.5 |

25.3 |

131(+) |

16.2 |

67.6 |

16.1 |

|

Selling Prices |

–44.5 |

8.0 |

–52.5 |

5.2 |

1(–) |

0.0 |

55.5 |

44.5 |

|

Capital Expenditures |

–22.7 |

11.1 |

–33.8 |

10.6 |

1(–) |

8.6 |

60.2 |

31.3 |

| General Business Conditions Current (versus previous month) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend** | % Reporting Improved | % Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–75.3 |

5.1 |

–80.4 |

5.7 |

1(–) |

0.0 |

24.7 |

75.3 |

|

General Business Activity |

–78.8 |

7.0 |

–85.8 |

3.5 |

1(–) |

0.0 |

21.2 |

78.8 |

| |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend* | % Reporting Increase | % Reporting No Change |

% Reporting Decrease |

|

Outlook Uncertainty† |

37.6 |

4.6 |

+33.0 |

12.0 |

26(+) |

65.7 |

6.2 |

28.1 |

| Business Indicators Relating to Facilities and Products in Texas Future (six months ahead) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend* | % Reporting Increase | % Reporting No Change |

% Reporting Decrease |

|

Revenue |

–40.3 |

39.9 |

–80.2 |

37.4 |

1(–) |

24.0 |

11.7 |

64.3 |

|

Employment |

–32.3 |

26.9 |

–59.2 |

22.0 |

1(–) |

10.1 |

47.5 |

42.4 |

|

Part–Time Employment |

–23.4 |

8.2 |

–31.6 |

6.5 |

1(–) |

5.6 |

65.3 |

29.0 |

|

Hours Worked |

–18.2 |

4.9 |

–23.1 |

5.3 |

1(–) |

11.9 |

58.0 |

30.1 |

|

Wages and Benefits |

1.7 |

37.0 |

–35.3 |

36.3 |

159(+) |

23.9 |

53.8 |

22.2 |

|

Input Prices |

9.6 |

40.0 |

–30.4 |

44.2 |

159(+) |

26.9 |

55.9 |

17.3 |

|

Selling Prices |

–16.7 |

25.9 |

–42.6 |

23.2 |

1(–) |

16.3 |

50.6 |

33.0 |

|

Capital Expenditures |

–23.4 |

23.4 |

–46.8 |

23.9 |

1(–) |

12.7 |

51.2 |

36.1 |

| General Business Conditions Future (six months ahead) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend** | % Reporting Improved | % Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–49.1 |

15.8 |

–64.9 |

16.6 |

1(–) |

14.9 |

21.1 |

64.0 |

|

General Business Activity |

–50.4 |

12.0 |

–62.4 |

13.2 |

1(–) |

11.0 |

27.6 |

61.4 |

Texas Retail Outlook Survey

March 31, 2020

Historical data are available from January 2007 to the most current release month.

| Business Indicators Relating to Facilities and Products in Texas Retail (versus previous month) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend* | % Reporting Increase | % Reporting No Change |

% Reporting Decrease |

Retail Activity in Texas |

||||||||

|

Sales |

–82.6 |

–2.5 |

–80.1 |

6.2 |

2(–) |

0.7 |

16.0 |

83.3 |

|

Employment |

–28.4 |

–1.0 |

–27.4 |

2.2 |

2(–) |

0.7 |

70.2 |

29.1 |

|

Part–Time Employment |

–25.5 |

0.0 |

–25.5 |

–1.8 |

1(–) |

3.6 |

67.3 |

29.1 |

|

Hours Worked |

–58.1 |

–1.7 |

–56.4 |

–1.6 |

2(–) |

0.0 |

41.9 |

58.1 |

|

Wages and Benefits |

–20.6 |

14.7 |

–35.3 |

9.7 |

1(–) |

4.1 |

71.2 |

24.7 |

|

Input Prices |

–12.0 |

19.9 |

–31.9 |

18.9 |

1(–) |

7.8 |

72.4 |

19.8 |

|

Selling Prices |

–35.5 |

27.5 |

–63.0 |

10.3 |

1(–) |

1.0 |

62.5 |

36.5 |

|

Capital Expenditures |

–37.5 |

6.0 |

–43.5 |

8.9 |

1(–) |

5.4 |

51.8 |

42.9 |

|

Inventories |

–42.6 |

–9.7 |

–32.9 |

3.6 |

2(–) |

1.6 |

54.2 |

44.2 |

Companywide Retail Activity |

||||||||

|

Companywide Sales |

–83.0 |

–2.1 |

–80.9 |

7.9 |

2(–) |

0.0 |

17.0 |

83.0 |

|

Companywide Internet Sales |

–45.6 |

16.2 |

–61.8 |

6.7 |

1(–) |

0.3 |

53.8 |

45.9 |

| General Business Conditions, Retail Current (versus previous month) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend** | % Reporting Improved | % Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–83.8 |

–10.3 |

–73.5 |

3.8 |

2(–) |

0.5 |

15.2 |

84.3 |

|

General Business Activity |

–84.2 |

–5.0 |

–79.2 |

–0.6 |

3(–) |

0.7 |

14.4 |

84.9 |

| Outlook Uncertainty Current (versus previous month) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend* | % Reporting Increase | % Reporting No Change |

% Reporting Decrease |

|

Outlook Uncertainty† |

46.4 |

2.0 |

+44.4 |

10.7 |

3(+) |

71.4 |

3.6 |

25.0 |

| Business Indicators Relating to Facilities and Products in Texas, Retail Future (six months ahead) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend* | % Reporting Increase | % Reporting No Change |

% Reporting Decrease |

Retail Activity in Texas |

||||||||

|

Sales |

–49.8 |

17.1 |

–66.9 |

32.0 |

1(–) |

16.9 |

16.4 |

66.7 |

|

Employment |

–46.1 |

–0.2 |

–45.9 |

12.0 |

2(–) |

0.8 |

52.3 |

46.9 |

|

Part–Time Employment |

–23.2 |

6.1 |

–29.3 |

0.7 |

1(–) |

7.9 |

61.0 |

31.1 |

|

Hours Worked |

–24.7 |

–1.5 |

–23.2 |

2.5 |

2(–) |

11.6 |

52.1 |

36.3 |

|

Wages and Benefits |

–3.5 |

23.2 |

–26.7 |

27.2 |

1(–) |

19.7 |

57.1 |

23.2 |

|

Input Prices |

–7.3 |

33.3 |

–40.6 |

32.9 |

1(–) |

18.2 |

56.4 |

25.5 |

|

Selling Prices |

–10.7 |

29.7 |

–40.4 |

28.9 |

1(–) |

16.1 |

57.1 |

26.8 |

|

Capital Expenditures |

–34.5 |

6.4 |

–40.9 |

17.7 |

1(–) |

7.3 |

50.9 |

41.8 |

|

Inventories |

–31.4 |

–14.7 |

–16.7 |

8.0 |

2(–) |

17.2 |

34.1 |

48.6 |

Companywide Retail Activity |

||||||||

|

Companywide Sales |

–36.5 |

20.4 |

–56.9 |

30.7 |

1(–) |

18.4 |

26.7 |

54.9 |

|

Companywide Internet Sales |

–6.5 |

22.2 |

–28.7 |

21.7 |

1(–) |

15.2 |

63.0 |

21.7 |

| General Business Conditions, Retail Future (six months ahead) |

||||||||

| Indicator | Mar Index | Feb Index | Change | Series Average |

Trend** | % Reporting Improved | % Reporting No Change |

% Reporting Worsened |

|

Company Outlook |

–62.4 |

2.3 |

–64.7 |

16.7 |

1(–) |

5.6 |

26.4 |

68.0 |

|

General Business Activity |

–66.0 |

–1.3 |

–64.7 |

12.5 |

2(–) |

6.6 |

20.8 |

72.6 |

*Shown is the number of consecutive months of expansion or contraction in the underlying indicator. Expansion is indicated by a positive index reading and denoted by a (+) in the table. Contraction is indicated by a negative index reading and denoted by a (–) in the table.

**Shown is the number of consecutive months of improvement or worsening in the underlying indicator. Improvement is indicated by a positive index reading and denoted by a (+) in the table. Worsening is indicated by a negative index reading and denoted by a (–) in the table.

†Added to survey in January 2018.

Data have been seasonally adjusted as necessary, with the exception of the outlook uncertainty index which does not yet have a sufficiently long time series to test for seasonality.

Texas Service Sector Outlook Survey

March 31, 2020

Texas Retail Outlook Survey

March 31, 2020

Texas Service Sector Outlook Survey

March 31, 2020

Comments from Survey Respondents

These comments are from respondents’ completed surveys and have been edited for publication.

Support Activities for Mining

- The outlook and uncertainty have worsened considerably with the coronavirus impact and government's reaction to it. We are looking for ways to cut costs to deal with the certain downturn and uncertain outlook.

Utilities

- I have never seen this much uncertainty. It's much worse than 2008–09. We need to see detailed plans from the federal government.

Transportation Equipment Manufacturing

- The impact of COVID-19 is substantial and disproportionate for some industries, creating a high level of uncertainty. As we are unable to predict the duration of the impact of the shock on the activities, we try to preserve the skills we have built by investing in recruiting, training, etc., when the job market was tight. Adding to the complexities of the managerial decision-making are the wide differences in local governments' decisions and impact on the workforce, the lack of clear, universal ruling from the federal government and the uncertain benefits for employees that could be adversely impacted. It is a time to be a responsible manager as well as citizen.

Truck Transportation

- We are a transportation service company facing very uncertain times.

- No one is spending money they don't have to until the coronavirus is dead.

Pipeline Transportation

- There is a severe liquidity crunch in the high-yield market that has the potential to drive many energy companies out of business.

Support Activities for Transportation

- We are seeing global supply chain disruptions. Our revenue has fallen by 60 percent. We are not making enough to cover overhead. I am keeping all of our staff for as long as we can. Everyone is working remotely.

- The Mexican peso rate of exchange is a threat.

- We see decreases the next 30 days due to COVID-19, such as a 30-day stoppage of cruise ship activity.

Warehousing and Storage

- [Our Port] remains open as an essential service and will continue to do so under all potential scenarios. We are heavily concentrated on liquid bulk and its processing, and that will take several months to truly decline, but once it does, we expect it to be stark. New capital projects will be delayed, and new investment decisions in export terminals will be deferred by our customers indefinitely. We fully expect the remainder of the year to be pretty stark before the recovery fully takes hold.

Publishing Industries (Except Internet)

- The SXSW® [South by Southwest®] Austin event was canceled, which had AR/XR [augmented reality/extended reality] demonstrations scheduled regarding a couple of near-term orders, which are currently more uncertain.

Broadcasting (Except Internet)

- COVID-19 is devastating businesses all around us. We will not lay off any employees, but we terminated employees who were underperforming. We expect sales volumes to return within six months, but we anticipate that pricing will be lower for a period of time.

Data Processing, Hosting and Related Services

- Fortunately, our company has a recurring revenue model, so we anticipate keeping most of our monthly revenues intact. At this moment (end of March) there are very many unknowns. We will likely modify our hiring plans to hold on new hires until the economy rebounds. At this time, we do believe the economy will rebound quickly once the virus storm ends.

Credit Intermediation and Related Activities

- The raging challenge facing everyone now is the pandemic planning and trying to manage the environment of increasing panic. There are so many unknowns, and all that we can do is to prepare our employees and customers for the threat of the spread of the virus. We have not witnessed very much in cash withdrawals, but have heard reports of some banks seeing the trend grow. We are trying to assess the potential risk the bank will be dealing with. There are no reports of cases of the virus in our immediate area, but all we hear is that it is inevitable. We have discussed closing access to the lobby and working most transactions through the drive-thru, except by appointment only for face-to-face visits. Our concern is to avoid aiding and abetting a panic by perception.

- The coronavirus has already affected our business, and we anticipate it getting worse over the next month or so. We are hopeful things will improve after 60 days.

- We have eight businesses under our umbrella. While some are likely to experience severe stress (consumer lending), others are capitalizing on this time (high-tech training for smart cars). We are eager to see the hysteria diminish and firmly believe that entrepreneurial drive will show creative ways to move ahead in an economically beneficial way.

Securities, Commodity Contracts, and Other Financial Investments and Related Activities

- The current pause of business activity is beginning to be felt in our businesses. Fear seems to be taking over the consumer. We will likely need assistance to keep people employed beginning in late April/early May.

- As a financial services company, I expect significant revenue and profit declines for my region immediately, lasting at least through this year. Our revenues tend to lag on the uptrend but declines show up much more quickly. I expect market conditions will slow down recruiting and hiring for the remainder of the year. People tend to stay put versus a job change when uncertainty exists. Capital expenditures may be reduced, depending on the depth and length of the revenue and profit dip.

- The COVID-19 virus has had an impact on the customer base (less spending), resulting in less loan demand.

- Good rain is offset by the sharp drop in oil prices. Uncertainty has ground business to a very slow pace.

Insurance Carriers and Related Activities

- We provide virtual health care services (including telemedicine) to employers and their employees, so our business has been crazy with coronavirus communications to all our clients. Can’t tell yet if this will help or hurt our business. We have a few clients asking to add more employees so they have access to care, and a few have asked to hold onboarding or been forced to cancel our service because their business is in jeopardy.

- Insurance prices continue to increase as storms in Texas become more severe. The general level of business activity has to be termed “unsettled to irrational” as the stock market swings uncontrollably and the future of the coronavirus' effect on the economy is unknown.

- As an insurance intermediary, the coronavirus has caused significant disruption in how we market and process our business. The advances in technology we have implemented have been invaluable in adjusting our marketing and underwriting activities.

Real Estate

- It may be too soon to make a six-month forecast. This is a fluid situation with multiple outcome scenarios.

- The imposition of mandatory closings and event cancellations will have far-reaching effects, and while they may be appropriate, I think the effects of the closings and cancellations may be as bad or worse than COVID-19. We need to get everyone back to more normal operations and give the public some comfort on an end to the restrictions. Shutting down the country for three to four months and not giving any encouragement of an end date, in my opinion, is overreacting and irresponsible. Consumer confidence drives our economy, and public officials are doing nothing to inspire any shred of confidence in their leadership or the situation even as the pandemic is subsiding in the places it originated. We should already be talking about how we are going to get back to work in six to eight weeks and what we will do to help kick-start the economy. In six to eight weeks, if we need to push it a week or two we can, but offering no clear direction and extreme and vague termination projections is just fueling the uncertainty.

- The coronavirus uncertainty is causing panic.

- The coronavirus has completely changed the business outlook for the worse. The uncertainty to small business activity is affecting our line of business.

- The commercial real estate industry will have great troubles based on the coronavirus, especially retail and hospitality, with apartments following as residents lose their jobs. It’s going to be an interesting time.

- We were having a great start in January and February. Many of those sales are closing in March and April. Many homeowners are not allowing their homes to be shown. I know that it will pick up in the summer.

Rental and Leasing Services

- Oil battles had already turned our industry markets and outlook prior to the “big C” which has now started to kill all business. It's been raining for days, so that never helps construction and industry. So yeah we are bolting down the hatches and anticipating revenues will be off at least as badly as 2009 (-23 percent). In 2001, markets quit flying; in 2008–09, markets quit spending—this time we're going to quit both!

Professional, Scientific and Technical Services

- Between the coronavirus and the Russia/Saudi Arabia oil price war, the energy business is in the tank. My consulting business is also in the tank.

- Everything has decreased due to the coronavirus.

- The projects that we have underway and under contract appear to be moving forward. We understand, though, that conditions related to coronavirus prevention measures are changing throughout the day each day and can impact this. We're uncertain about potential project delays and work stoppages due to preventive safety measures.

- Regarding COVID-19: Until we determine what the new “normal” looks like and its duration, it is a very fluid situation. Workplaces are in flux and making necessary adjustments per governmental edicts. This necessary disruption must subside before ascertaining longer-term consequences.

- Business is at a standstill. Clients are canceling meetings. Transactions have been terminated or postponed indefinitely.

- There are three issues: (1) coronavirus; (2) oil collapse; (3) incompetent federal government response to both. I’m not sure any other comments are required but will elaborate on two other points. A fourth: the government/SEC [Security and Exchange Commission] needs to take a hard look at the impact HFT [high-frequency trading] is having on market volatility. This cannot continue to go unchecked. I know there is some sentiment that they as individual trading houses are not impacting prices, but that is ridiculous. En masse it seems obvious they are; just looking at these momentum shifts, their trade algorithms are impacting and costing everyone. Fifth: The bailouts, once again, are coming. The structure of these will be important. While they are perhaps needed for stability, these should not be free passes for industries to continue deleterious behavior. Company leadership should not be rewarded for a failure to manage properly and adequately prepare for these types of events. Airlines, and any debt-laden entities in focus, have taken on way too much risk with no plan for a downturn. Those chickens have now come to roost.

- COVID-19 and the Russian/Saudi stance on oil production and pricing has and will likely continue to have an adverse effect on our workload.

- The crash of the stock market may have a bigger impact on development and construction business than the virus. Totally unknown at this point.

- The grocery industry is currently positively affected by COVID-19. The longer term is uncertain.

- COVID-19 is scaring everyone, but if we can get it under control and flatten the curve, we can restore the economy quickly. We need to keep construction going if we can.

- COVID-19 is obviously having a dramatic effect on the market. Legal services are fortunate that we can work remotely, and we have all the infrastructure in place and have made a smooth transition. Demand for client services has spiked in the near term (with inquiries on how clients need to respond to current market conditions). Medium-term demands (30 days into shelter-in-place orders) is unknown. Long term (return to normalcy), we expect a high demand for services as clients readjust and rebuild. We are concerned that clients will begin to ration their own payment priorities that could impact their prioritization for paying legal invoices, which could lead to a cash crunch for many law firms. We are well-capitalized and have run multiple scenarios and don't believe we will have any cash concerns, but others may. We are too soon into this crisis to see what we will need to do medium term with employees. Right now, everyone is being fully paid.

- I expect little to no impact on my business from the current health pandemic. In 2013, I began taking client information electronically via a secure document portal. Some clients still want face-to-face meetings, but most of my client contact is accomplished via phone, email, text messages and the secure portal. Cloud-based applications have made physical transfers of data files almost extinct, and even when required, I can get those electronically.

- As a CPA firm, demand for tax returns with refunds has increased, as well as help for loans for businesses.

- Obviously, coronavirus will affect all of us.

- These are unprecedented times, and no one knows how deep the recession is going to be. The stimulus package coming out will help, but we don’t know if it is going to be enough to save the economy from a deep recession.

- We don't yet have a feel for activity levels since the changes of last week. We have moved to remote work and could see a slowdown just because of that. We expect activity in some areas are of course likely to slow down, with increases in others. We would speculate we will see a decrease in hours and revenue for a few months.

- We are having to make adjustments for employees working out of their homes and setting up software and processes to comply with HIPAA [Health Insurance Portability and Accountability Act], Texas Department of Insurance, SEC and FINRA [Financial Industry Regulatory Authority]. We were ready to hire new employees and are now putting everything on hold.

- COVID-19 and the oil price downturn are the two economic shocks that have worsened the outlook.

Management of Companies and Enterprises

- We are in uncharted times and territory.

Administrative and Support Services

- The biggest drag, COVID-19, has affected us as of March 12, 2020. All sectors except industrial-oil machined parts production were up and positive. We are hoping the recent Fed [Federal Reserve] actions and the "hope" for some type of treatment will lift the sectors somewhat. We, being in the aviation sector, are scrambling to find a way to survive for six months without bankruptcy.

- Uncertainty is the name of the game right now. Our backlog is still strong, and we continue high production. It is just hard to know where we go from here with regard to the virus' impact on the country. We will use the opportunity to hire better people if we are presented with that opportunity.

- Since we are a temporary staffing service, with offices in several south central Texas cities, we have several thousand temporary employees working at various companies at different times. New federal vacation and sick leave laws will include all of our temporary employees just as if they were full-time employees at other companies. We want the best for our temporary employees, but we do not feel that it is fair to pay the costs associated with full-time employees to temporary employees who may work for only several weeks.

- The travel industry is a key facilitator in the economy. The damage inflicted on this industry has been, and will be felt, for months if not years. The trickle-down effect will be felt far and wide.

- Travel service providers have suffered a drastic loss of business. As government contractors, we hope that in the next 60 days it will improve. We have long-standing contracts.

- Business activity is declining due to COVID-19. Closing of schools, child care centers and layoffs in hospitality sectors are impacting the local area.

- Harris County ordered bars, cafes and restaurants to close except for drive-thru, delivery or take out. There had already been panic buying at many of the local grocery stores. We expect the new social distancing regulations to dramatically slow down economic and other activity and result in an increase in unemployment and negative impact on families living paycheck to paycheck.

- Business was pretty solid until the coronavirus.

- Any revenue gains for the fiscal year (Oct. 1) start have been completely wiped out; it is anticipated there will be no revenue coming in for at least eight weeks, and then revenues will return but at a 15–25 percent drop-off.

Waste Management and Remediation Services

- In the short term, demand for our product—paper and cardboard collected for recycling—has picked up. The problem is that the supply for both commodity grades has decreased (potentially increasing the price for these grades in April). As more employees are working from home, the supply of office paper is contracting. Boxes are increasing but are not making their way into the clean supply stream. Many boxes are for Amazon home deliveries and end up in the homeowner's recycle bin. These boxes get mixed in the other commodities in the bin, becoming contaminated and lowering the recyclability. Weird times.

Educational Services

- COVID-19 is directly affecting our business as it's prohibiting us from working with school leaders in the schools. We are currently looking for innovative ways to continue to support the students, teachers and leaders we serve in a remote setting.

- The underlying fundamentals in our business model remain the same; it's the exogenous variables that are uncontrollable. As the pandemic subsides, and it will, I think we will regain a sense of normalcy and our local economy will respond accordingly.

- As an educational institution, we have had to move to complete online delivery with little time to prepare. We are concerned that we may lose current students who dislike that mode. We also worry that loss of income for potential students may cause them to defer education. And finally, the need to provide refunds and the loss of revenue from auxiliary services and athletics will negatively impact our financial position.

Ambulatory Health Care Services

- In the current environment, we cannot project out six months.

- We are currently at 12 percent of normal volume and see that decreasing to 5 percent. We are in the process of drawing down our line of credit and securing additional financing in order to support our employees. The plan is to allow them to draw down PTO then support all at a rate of 24 hours/week plus benefits. We anticipate being able to survive three to four months but will require additional financing to ramp up again. Despite being in health care, we have no PPE [personal protective equipment] and therefore cannot image patients for COVID-19. This is a black swan of the worst kind. I anticipate being down 100 percent soon. We cannot open until everyone has masks, everyone can be tested and everyone who is sick has a bed. Terrible preparation on the part of our government and emergency systems. I started preparing at the end of January but with supply chain disruptions, was unable to secure masks or PPE even back then. Simply stated, a disaster of biblical proportions.

Nursing and Residential Care Facilities

- As with most businesses, COVID-19 is already impacting our retirement community. For the safety of our residents, we have closed the campus to outside visitors and nonessential workers.

Social Assistance

- All of our outlook is a reflection of our response to the COVID-19 pandemic.

Performing Arts, Spectator Sports and Related Industries

- All our issues are due to COVID-19 and the government shutting down businesses.

Museums, Historical Sites and Similar Institutions

- We are closed to the public with zero income and an unknown timeline for the future. We take care of live animals so our daily costs and many activities remain the same. As a nonprofit, our status for receiving SBA [Small Business Administration] loans or other such [help] is unlikely. We will probably have to rely on government handouts.

Accommodation

- It’s impossible to predict the lasting impact of the virus on future occupancy levels. We expect that we will end the year at 25 percent below last year’s revenue levels, as even after the virus has been stabilized, travel will be slow to recover.

- No one can predict the future right now. The world has changed.

- Seems pretty obvious, but due to COVID-19, our business has effectively shut down. Meetings are canceled through May, and many are trying to cancel as far out as January 2021. There is no individual transient travel occurring currently, and we have no idea how long that will continue. We have furloughed almost 90 percent of our staff.

Food Services and Drinking Places

- We are hopeful that things will get better.

- Sales are down dramatically with new regulations. Not sure how long restrictions will last, but they are of course having a severe impact on business.

- The coronavirus is killing my business. I may file bankruptcy.

- We have been required to close down our businesses. As soon as we are over the virus, we will get back to normal for the rest of the year.

- Oil is down.

- The effects of the coronavirus and how long it will affect the economy are unknown.

Repair and Maintenance

- COVID-19 has greatly impacted our business.

Religious, Grantmaking, Civic, Professional and Similar Organizations

- COVID-19 is impacting our business as we are unable to host events and we anticipate membership dues from businesses declining.

- COVID-19 has created unprecedented uncertainty for all businesses but particularly on nonprofits and economic developers.

- The impact of the virus has placed a great uncertainty on our operation, which has a negative effect.

- COVID-19 is killing our business in the short term, and I am deeply concerned about what will happen over the long term.

- Let’s keep these banks from foreclosing on small business and working families.

- Our entire organization is now telecommuting due to coronavirus concerns through at least March 30.

- COVID-19 has had an obvious impact. As a social services organization providing basic necessities to low-income families, we expect increases in activity over the next month to six months.

Merchant Wholesalers, Durable Goods

- This survey is riddled with uncertainty related to COVID-19. Our most significant concern is when will export production begin in China so we do not end up in an inventory shortage? Secondarily, will the number of new COVID-19 cases flatten so that businesses and the economy begin to recover? If the supply chain opens up, some of our products would be available to our current and potential customers in unrestricted quantities.

- Due to the coronavirus, and the present uncertainty on how to do and maintain business, our board of directors in China has decided to discontinue operations soon. We will lose 14 more employees.

- With everything shut down, people just freeze, so no sales are going to happen until maybe a month after society returns to normalcy.

- COVID-19 and oil prices both are significantly impacting metalworking manufacturing in North Texas. We are a wholesale distributor of machine shop and industrial supplies.

- COVID-19 has made the short-term outlook difficult. I do feel that once we have the pandemic behind us, business will feel a real surge and improve.

- The virus has affected all businesses. Texas and our residential construction industry remain vibrant and strong but have been affected by the virus and market headwinds. Our company is in a position to support our customers (and their customers’) needs, whether it is a soft landing (mild economic impact) or a hard landing and more severe economic impact. I personally feel market fundamentals are strong and the market will rebound fairly quickly if the right policies are enacted timely.

Merchant Wholesalers, Nondurable Goods

- We sell wholesale to restaurants. In the past week, we have learned from most markets we serve (Puerto Rico, South America, Hawaii) that restaurants have closed their dining rooms to combat the spread of COVID-19. As restaurant sales decrease, it’s only a matter of time before we see a slowdown in orders as well. As people are furloughed or laid off from employment, we will also see lasting impact to restaurant sales after the pandemic eases (people won’t be able to afford to eat out).

- Coronavirus has had an immediate impact. How this impacts buying patterns over the next six months to a year remains to be seen for retail. The consumer will pull back regardless to prepare for market shocks in the future. The economic free for all and rampant consumer consumption will end for a long time. Just like the Great Depression had an impact on an entire generation, this too will have a similar economic impact on a large part of the world economy.

Motor Vehicle and Parts Dealers

- Our answers appear to be contradictory; however, we feel this may be a "buying opportunity," and we plan to attempt acquisitions during the immediate downturn in hopes that it will not be prolonged.

- Obviously, the closure of so many restaurants, clubs, gyms and retail establishments has taken much spendable income away from the consumer. These are tough times in the near term but will not last long term I think.

- I believe that the coronavirus will impact all retail business negatively.

- COVID-19 is changing almost everything. As an essential business, we will not be closing but may be adjusting hours and staff on duty.

- We are seeing continued employee fear and uncertainty regarding their desire to work and be in contact with customers. We are, however, selling and servicing vehicles at a surprising rate given the circumstances. There is a lot of concern that the federal sick leave bill will leave us short of workforce. Another huge issue is the extremely fast drop in used vehicle prices; this has the potential to shake our economy from many perspectives.

Building Material and Garden Equipment and Supplies Dealers

- If they don’t open up the economy soon, most businesses will be broke. We must open it back up as soon as possible.

- We are reacting daily to the changes taking place. Employee safety is put first, and this will definitely affect revenue and profits. It is questionable just how long and deep this will extend.

Clothing and Clothing Accessories

- The majority of our stores have been forced to close due to the coronavirus.

Nonstore Retailers

- Most of our business has gone to zero except for essential locations such as hospitals, military bases and prisons. As a vending company, we know we are "less essential" to these businesses, so we anticipate our business could go to zero due to the current COVID-19 situation. We are contemplating at this moment sending most employees home while our owners determine whether they can afford to pay reduced salaries and cover benefits for a short period while we see if things improve or worsen. Most of our administrative team already has the capability to work remotely, and there will be plenty of work to keep them occupied full time, unless we need to totally shut down.

Historical Data

Historical data can be downloaded dating back to January 2007.

Indexes

Download indexes for all indicators. For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

All Data

Download indexes and components of the indexes (percentage of respondents reporting increase, decrease, or no change). For the definitions of all variables, see Data Definitions.

Texas Service Sector Outlook Survey |

Texas Retail Outlook Survey |

| Unadjusted | Unadjusted |

| Seasonally adjusted | Seasonally adjusted |

Questions regarding the Texas Service Sector Outlook Survey can be addressed to Christopher Slijk at christopher.slijk@dal.frb.org.

Sign up for our email alert to be automatically notified as soon as the latest Texas Service Sector Outlook Survey is released on the web.